Образование

ОбразованиеПохожие презентации:

Social Tax

1.

Social TaxWeek 4

2.

8.1 IntroductionThis week, we learn

• What is social tax

• Who pays social tax

• Payment by certain categories of individuals

3.

Social TaxIs intended to mobilize funds to realize the right of citizens to state

pension and social security (insurance) and medical care.

The tax is calculated on a monthly basis based on the tax base and

the established tax rates.

4.

Taxpayers of social tax are:• legal entities of the Republic of Uzbekistan;

• legal entities who are non-residents of the Republic of

Uzbekistan which operate in the Republic of Uzbekistan through

permanent establishments (doimiy muassasa), representative

offices (vakolatxonalari) and branches of foreign legal entities

• certain categories of individuals* who pay social taxes

5.

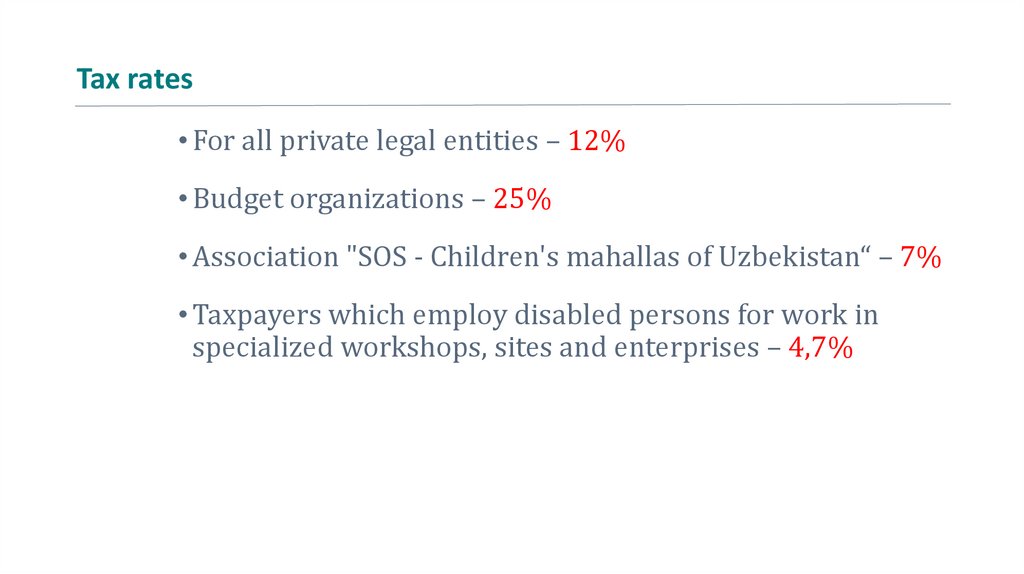

Tax rates• For all private legal entities – 12%

• Budget organizations – 25%

• Association "SOS - Children's mahallas of Uzbekistan“ – 7%

• Taxpayers which employ disabled persons for work in

specialized workshops, sites and enterprises – 4,7%

6.

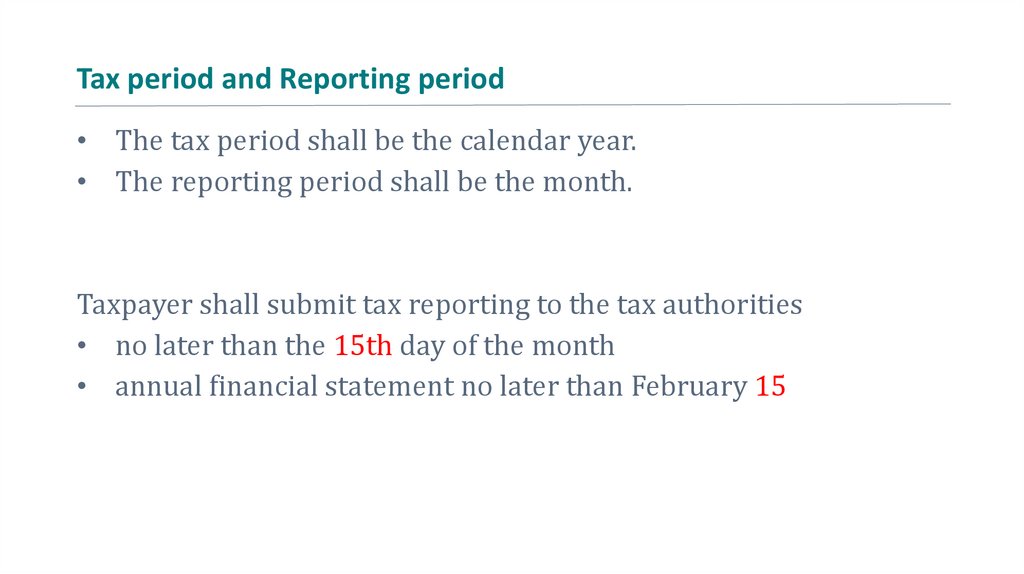

Tax period and Reporting period• The tax period shall be the calendar year.

• The reporting period shall be the month.

Taxpayer shall submit tax reporting to the tax authorities

• no later than the 15th day of the month

• annual financial statement no later than February 15

7.

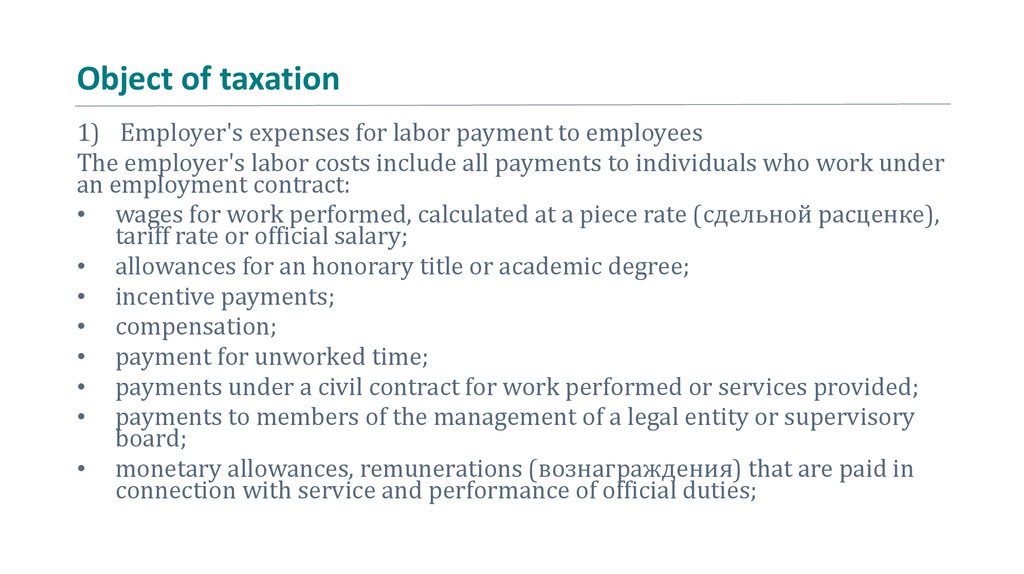

Object of taxation1) Employer's expenses for labor payment to employees

The employer's labor costs include all payments to individuals who work under

an employment contract:

• wages for work performed, calculated at a piece rate (сдельной расценке),

tariff rate or official salary;

• allowances for an honorary title or academic degree;

• incentive payments;

• compensation;

• payment for unworked time;

• payments under a civil contract for work performed or services provided;

• payments to members of the management of a legal entity or supervisory

board;

• monetary allowances, remunerations (вознаграждения) that are paid in

connection with service and performance of official duties;

8.

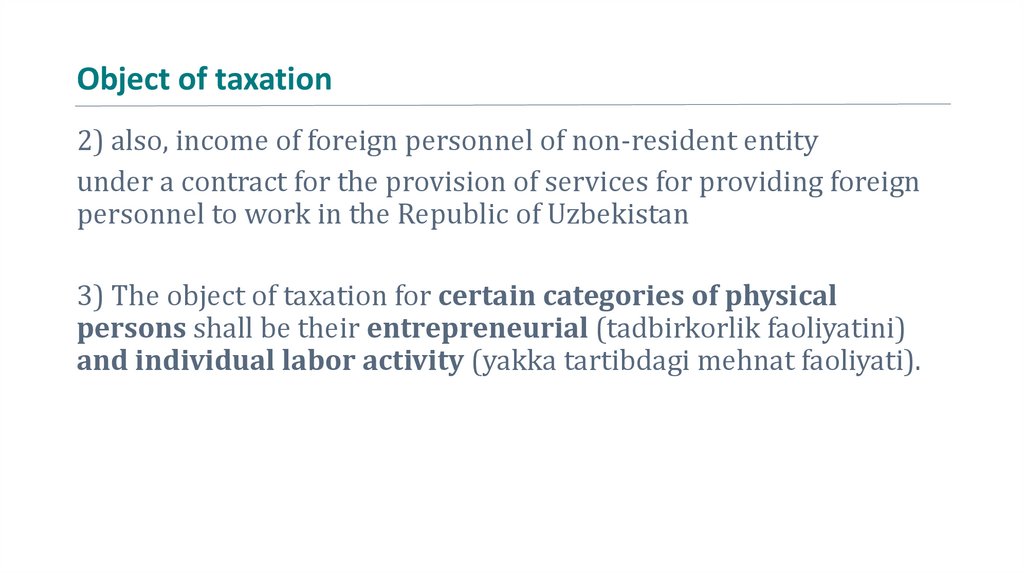

Object of taxation2) also, income of foreign personnel of non-resident entity

under a contract for the provision of services for providing foreign

personnel to work in the Republic of Uzbekistan

3) The object of taxation for certain categories of physical

persons shall be their entrepreneurial (tadbirkorlik faoliyatini)

and individual labor activity (yakka tartibdagi mehnat faoliyati).

9.

Not the object of taxation• employer's expenses in the form of compensation to the

employee for harm connected with labor injury or other damage

to health

• expenses for labor payment to physical persons, involved in

seasonal agricultural work with respect to picking cotton, for the

performance of this work.

10.

Not the object of taxationThe object of taxation of social tax is

the employer's expenses for wages, therefore, this tax is not

charged on:

income that is not included in the total income of an individual;

property income;

income in the form of material benefits;

other income.

11.

Payment by certain categories of individuals*Social tax is compulsory irrespective of the number of days the

taxpayer worked in a calendar month:

1) individual entrepreneurs — in the amount of not less than one

minimum monthly wage rate (330 000 from 1 May 2023)

2) physical persons who are in labor relations with an individual

entrepreneur operating in shopping malls and markets — in the

amount of 50 % of minimum wage

12.

Payment by certain categories of individuals*3) by family members carrying out activities in the form of family

business without forming a legal entity:

• by a family member registered as an individual

entrepreneur - in the amount of not less than 1

minimum monthly wage rate;

• by other family members (except for those under

the age of eighteen) - in the amount of 50

percent of the minimum monthly wage rate;

13.

Payment by certain categories of individuals*4) the subjects of handicraft activities registered in rural areas and

carrying out their activities, which are members of the

“Hunarmand" Association - in the first two years of their activity

they pay 50% of the minimum monthly wage rate.

5) students of “Usta-shogird” schools during the period of work up

to 25 years of age. The tax amount is at least 2.5 times the size of the

gross tax per year;

6) Physical persons who receive income from an employer and who

are not responsible for calculating and withholding social tax.

14.

From April 1, 2022 to January 1, 2025, the social tax rate was set at 1percent to:

• retail trade and catering;

• hotel (accommodation) services;

• passenger and cargo transportation by motor

vehicle;

• repair and maintenance of vehicles;

• computer services;

• repair of household appliances;

• provision of agro and veterinary services;

• providing services in entertainment venues.

15.

From April 1, 2022 to January 1, 2025, the social tax rate was set at 1percent to:

This privilege is given to business entities, if their income from the

above types of activities is at least 60% of the total income at the

end of the current reporting (tax) period.

16.

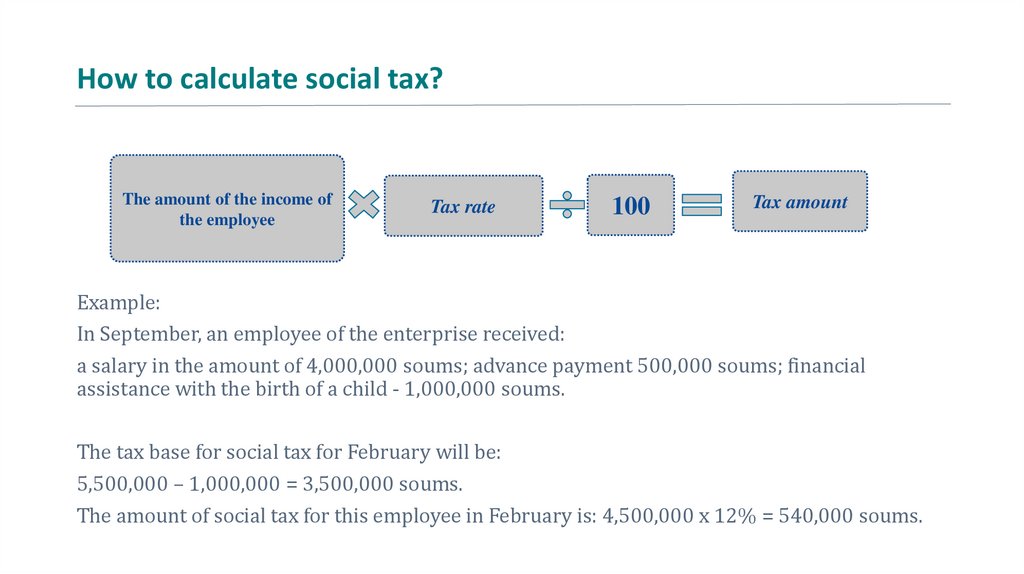

How to calculate social tax?The amount of the income of

the employee

Tax rate

100

Tax amount

Example:

In September, an employee of the enterprise received:

a salary in the amount of 4,000,000 soums; advance payment 500,000 soums; financial

assistance with the birth of a child - 1,000,000 soums.

The tax base for social tax for February will be:

5,500,000 – 1,000,000 = 3,500,000 soums.

The amount of social tax for this employee in February is: 4,500,000 x 12% = 540,000 soums.