Бизнес

БизнесПохожие презентации:

")

Corporate Strategy

1.

Corporate Strategy2. Models of Corporate Influence

Catherine Magelssen

London Business School

April 30, 2018

2.

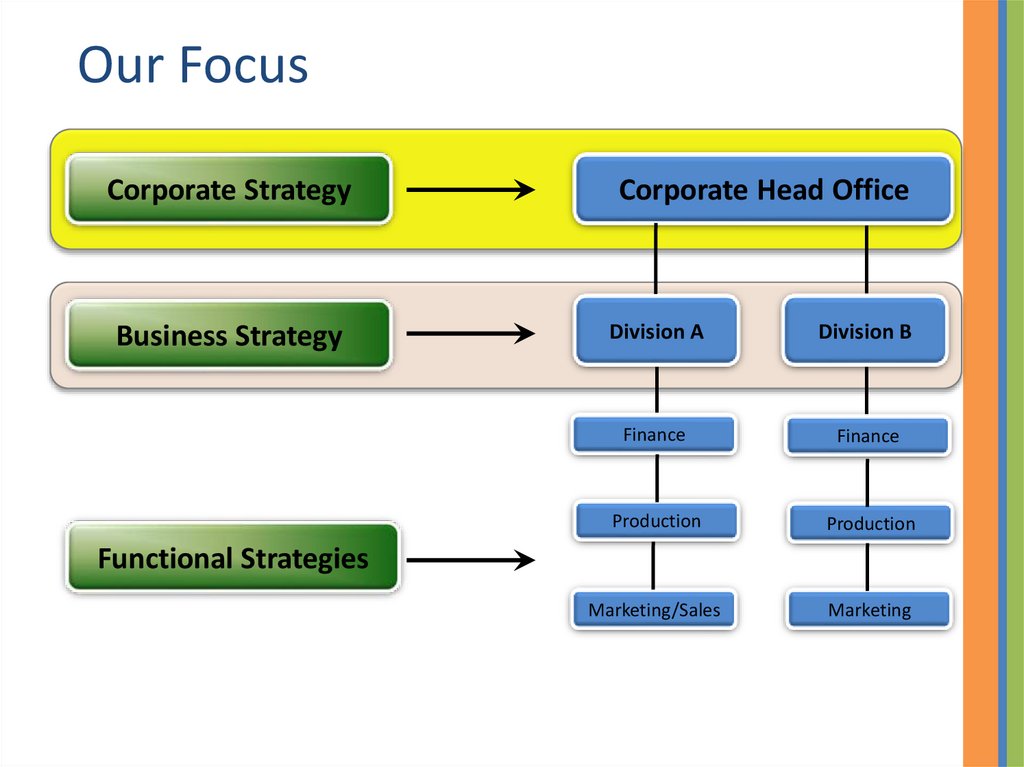

Our FocusCorporate Strategy

Corporate Head Office

Business Strategy

Division A

Division B

Finance

Finance

Production

Production

Marketing/Sales

Marketing

Functional Strategies

3.

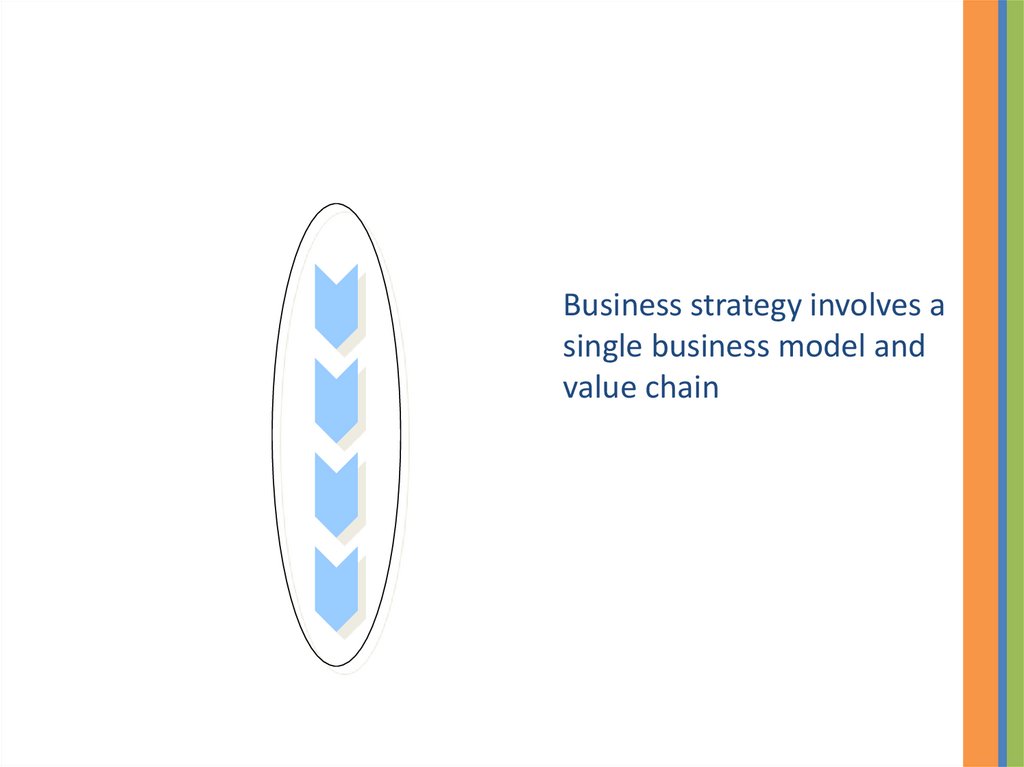

Business strategy involves asingle business model and

value chain

4.

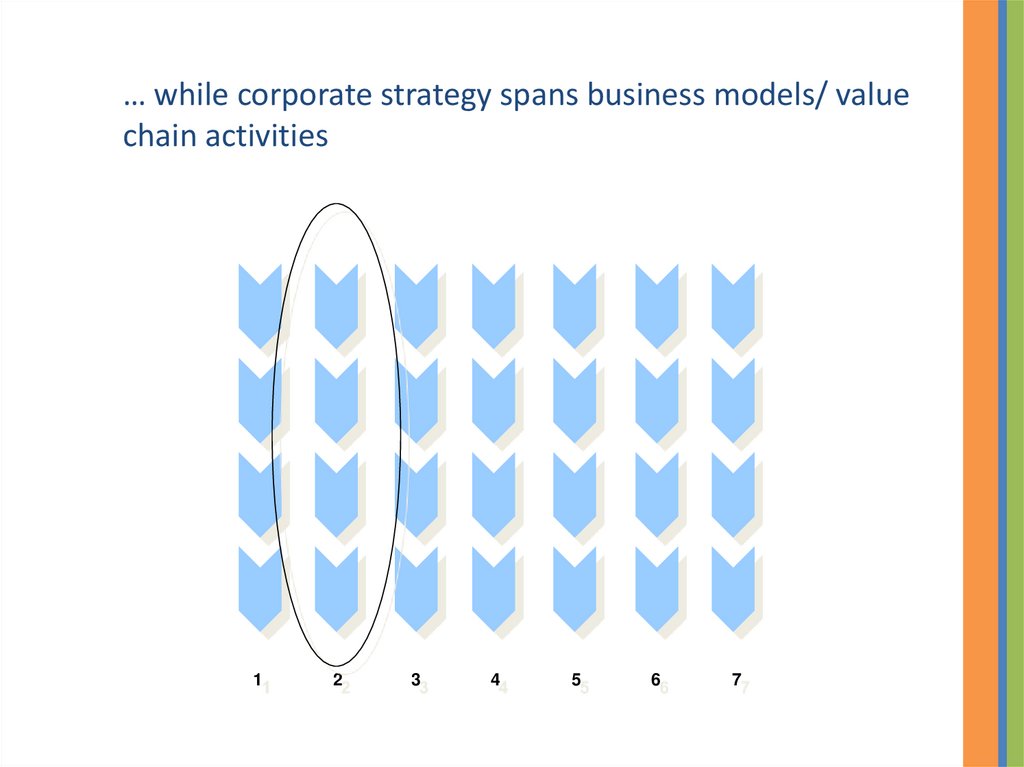

… while corporate strategy spans business models/ valuechain activities

1

2

3

4

5

6

7

5.

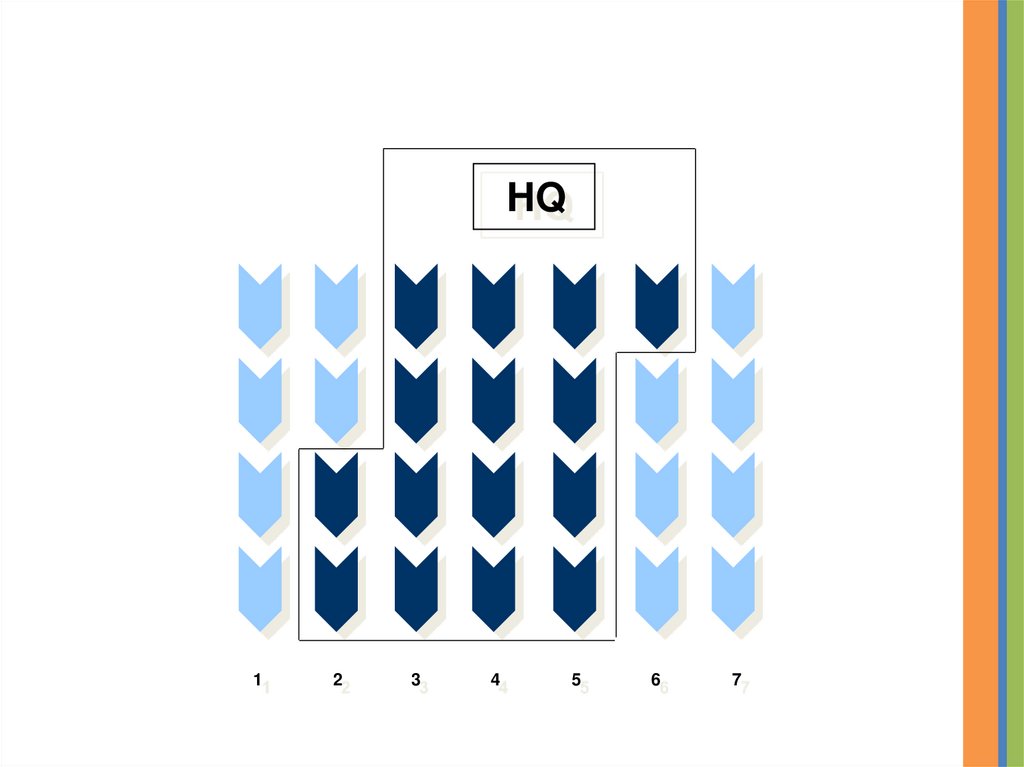

HQ1

2

3

4

5

6

7

6.

A corporation is a portfolio of value chainactivities

Corporate advantage exists if portfolio

performance exceeds the sum of performance

of individual activities

7.

1. All strategy depends on marketimperfections.

In addition to the market imperfections you looked at in core

strategy (e.g. barriers to entry), important market

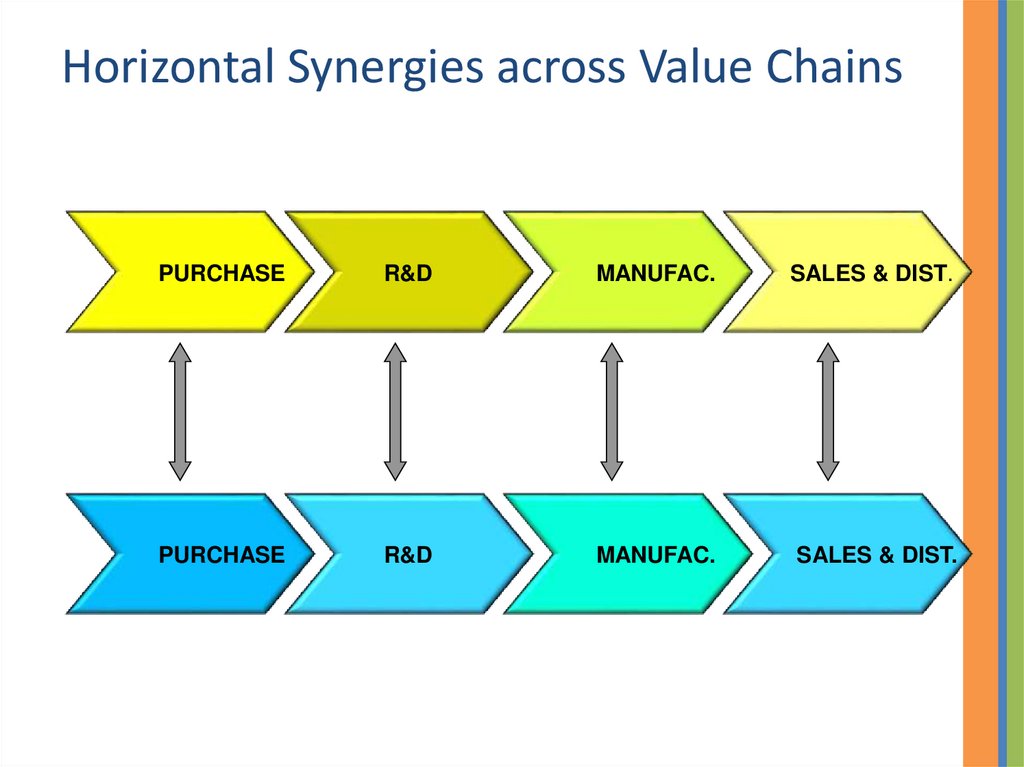

imperfections in corporate strategy are

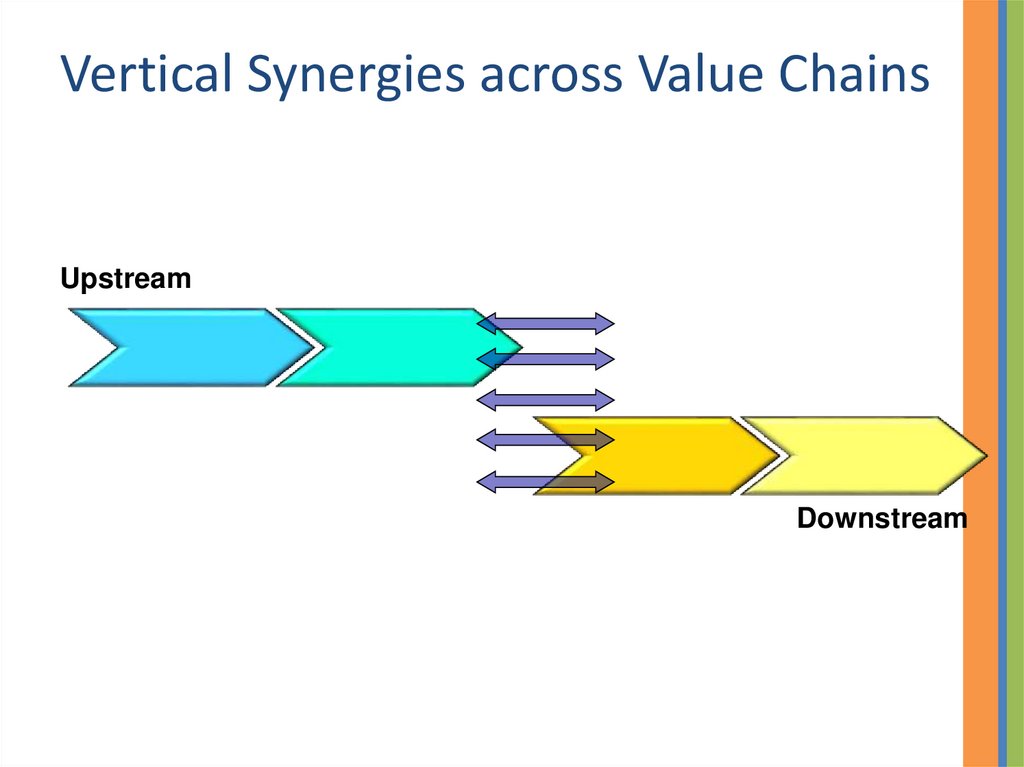

capital market imperfections (which help some firms grow

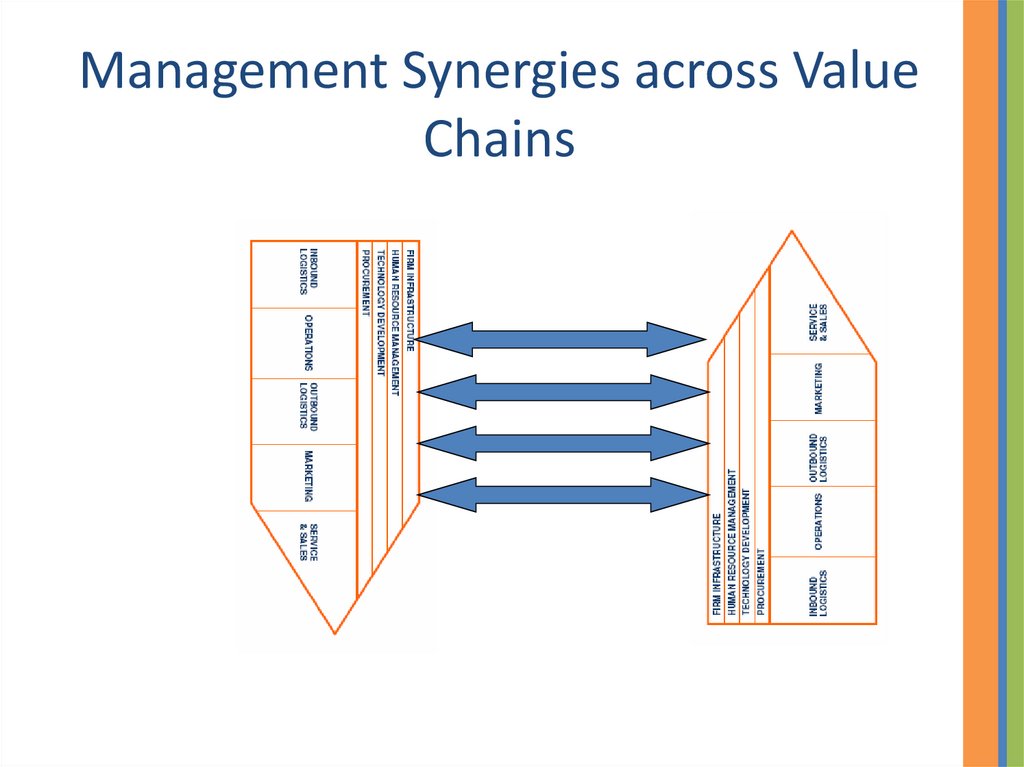

faster than others),

imperfect human resource markets (which help some firms

gain talent more cheaply than others),

and political capital (which give some firms privileged

rights to operate).

8.

2. Strategy is easy for incumbents whenmarket imperfections are high.

In the 50s-70s, Grand Met could acquire multiple companies

without doing anything to add value to their operations.

As capital markets became more perfect, adding value

through operational improvements became imperative.

9.

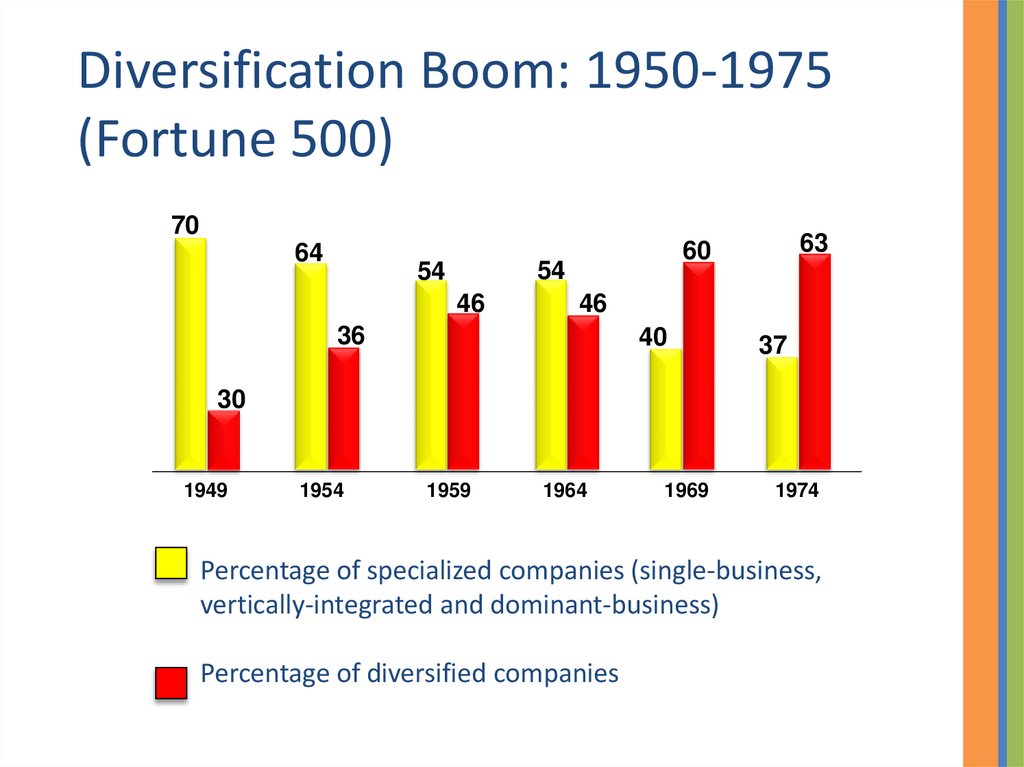

Diversification Boom: 1950-1975(Fortune 500)

70

64

54

54

46

63

60

46

36

40

37

30

1949

1954

1959

1964

1969

1974

Percentage of specialized companies (single-business,

vertically-integrated and dominant-business)

Percentage of diversified companies

10.

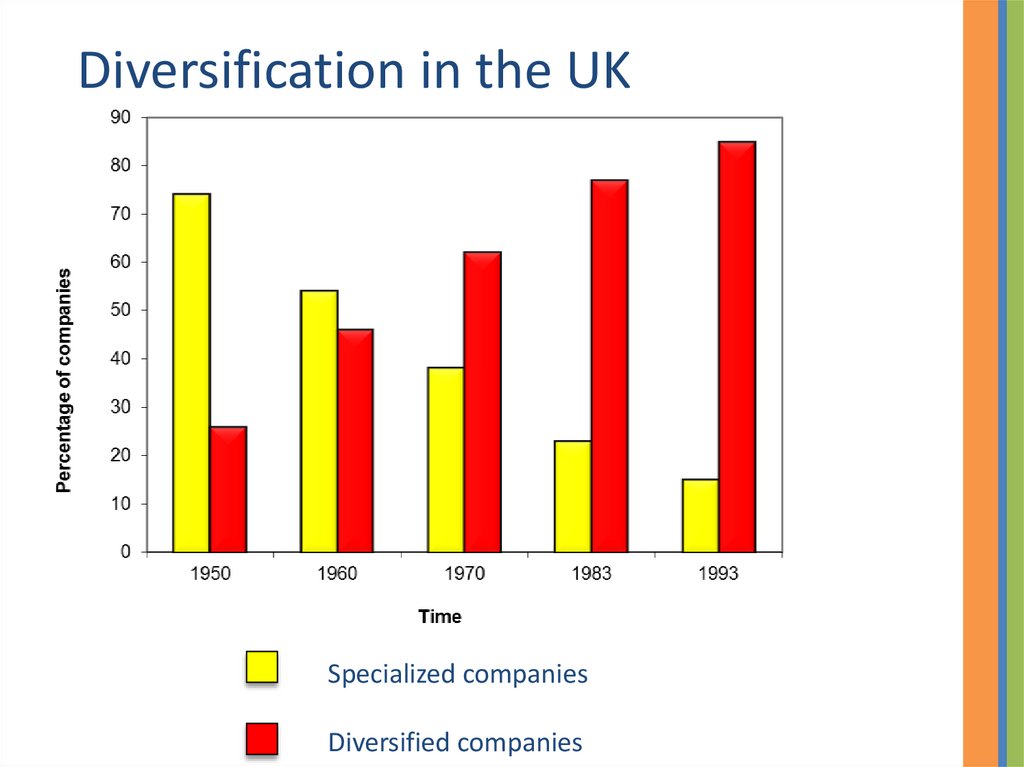

Diversification in the UKSpecialized companies

Diversified companies

11. What Explains the Diversification Boom?

Good economic conditionsFirms emphasized growth over profitability

Rise to eminence of consulting firms

Spread of the M-form (multidivisional)

structure

Belief in general management techniques and

skills

Portfolio management techniques

12.

The 1970s13.

Portfolio Planning Models: BCG GrowthShare MatrixAnnual real rate of market growth (%)

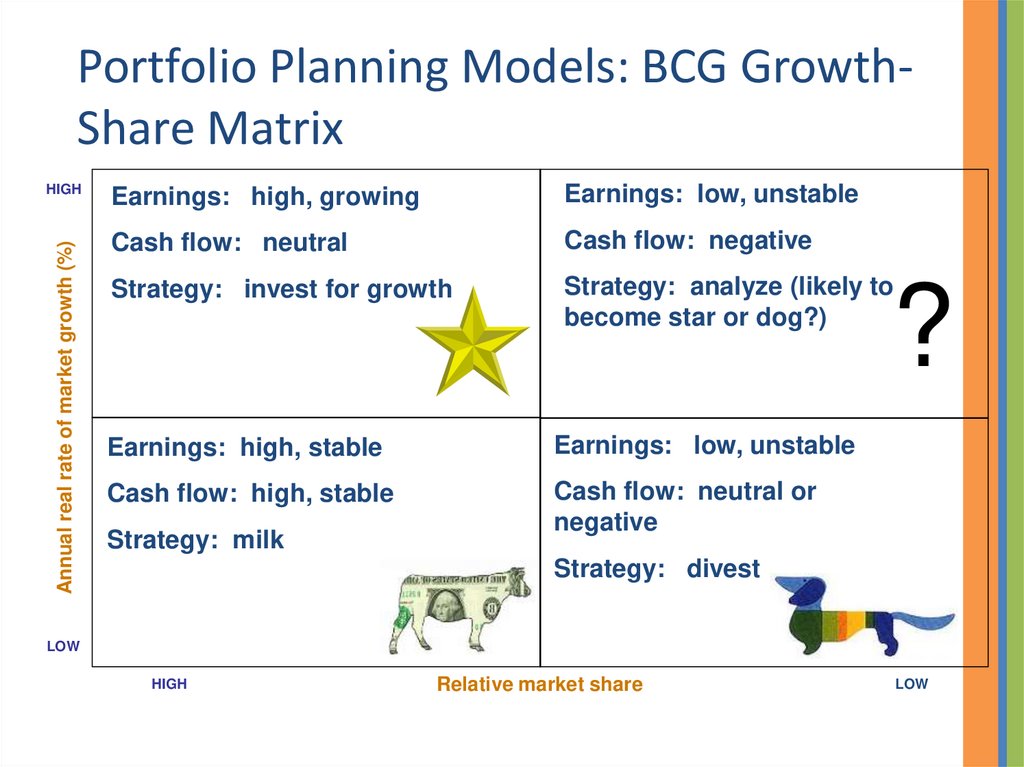

HIGH

Earnings: high, growing

Earnings: low, unstable

Cash flow: neutral

Cash flow: negative

Strategy: invest for growth

Strategy: analyze (likely to

become star or dog?)

Earnings: high, stable

Earnings: low, unstable

Cash flow: high, stable

Cash flow: neutral or

negative

Strategy: milk

?

Strategy: divest

LOW

HIGH

Relative market share

LOW

14.

Annual real rate of market(%)

growth

10

8

6

4

2

0

-2

Portfolio Planning Models: Applying the BCG

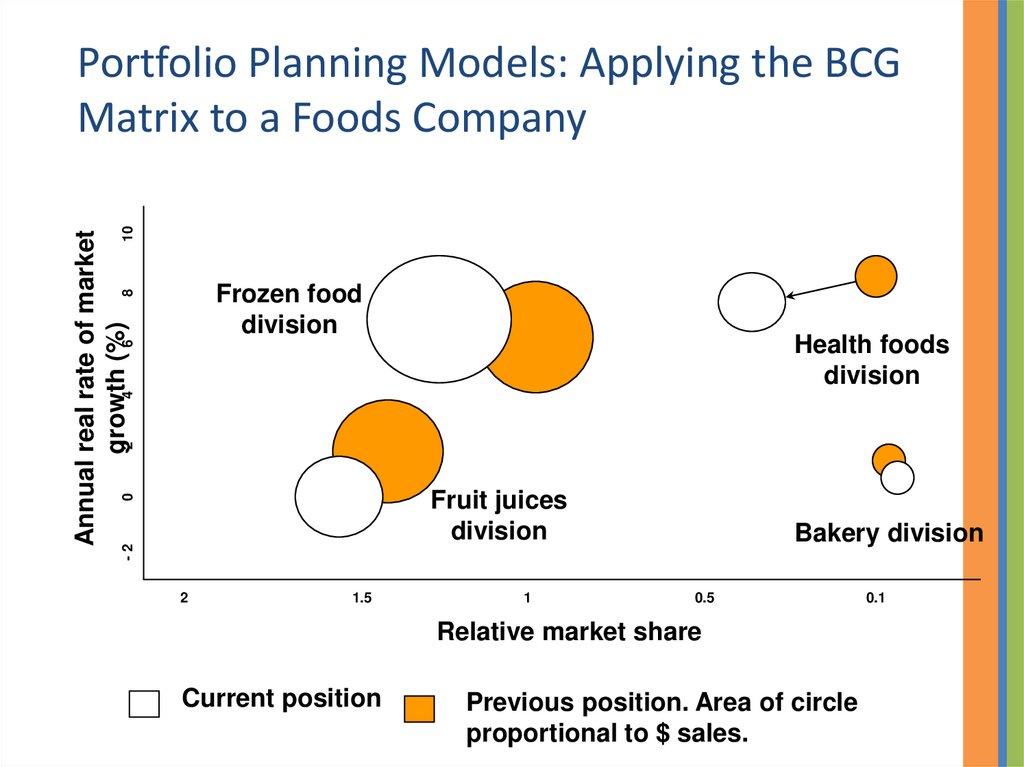

Matrix to a Foods Company

Frozen food

division

Health foods

division

Fruit juices

division

2

1.5

1

Bakery division

0.5

Relative market share

Current position

Previous position. Area of circle

proportional to $ sales.

0.1

15.

Portfolio Planning Models: The GE/McKinseyMatrix

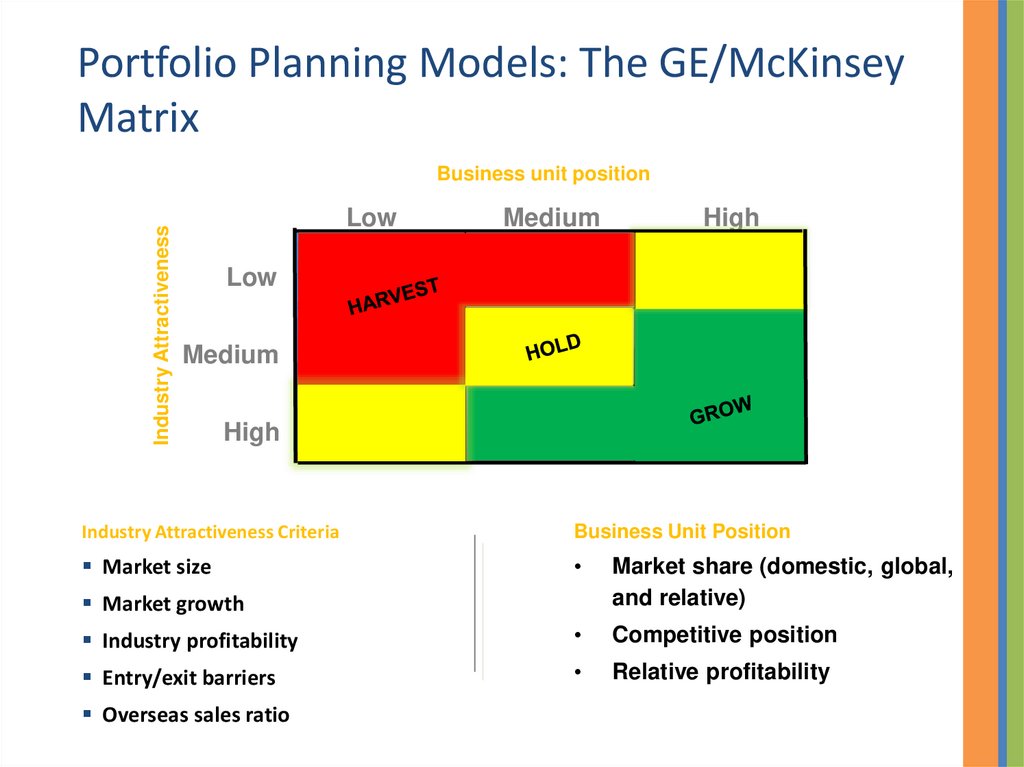

Industry Attractiveness

Business unit position

Low

Medium

High

Low

Medium

High

Industry Attractiveness Criteria

Business Unit Position

Market size

Market share (domestic, global,

and relative)

Industry profitability

Competitive position

Entry/exit barriers

Relative profitability

Market growth

Overseas sales ratio

16.

Do Portfolio Planning Models Helpor Hinder Corporate Strategy?

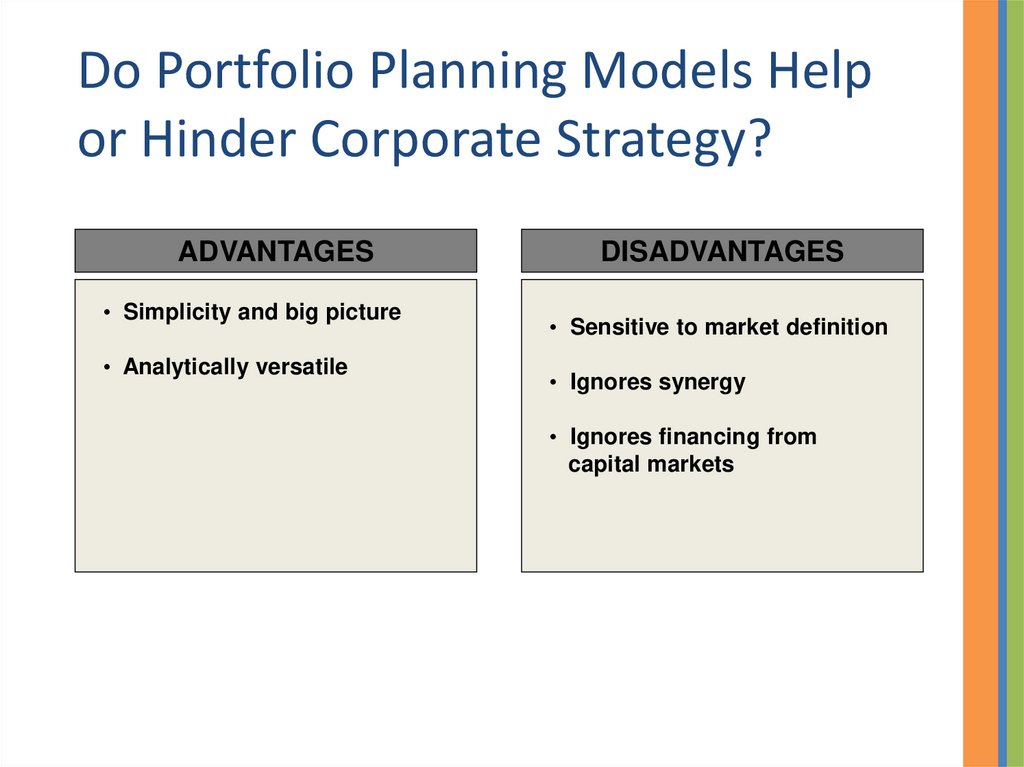

ADVANTAGES

• Simplicity and big picture

• Analytically versatile

DISADVANTAGES

• Sensitive to market definition

• Ignores synergy

• Ignores financing from

capital markets

17.

The 1980s18.

Re-focusing in the 1980sDrop in diversification index of Fortune

500 by 33% between 1980 and 1990

M&A levels were high, but divestments

were even higher

19.

Stick to Your KnittingIdea comes from In Search of Excellence

(Peters and Waterman, 1982)

Most widely held library book in the US

Based on study of 43 “excellent companies”

These companies focused on

business sectors they knew well,

And had lean HQ.

20.

But…?Is the sample reliable?

Need to understand the practices of

unsuccessful firms too

Atari, Wang Laboratories…

Compare In Search of Stupidity

21.

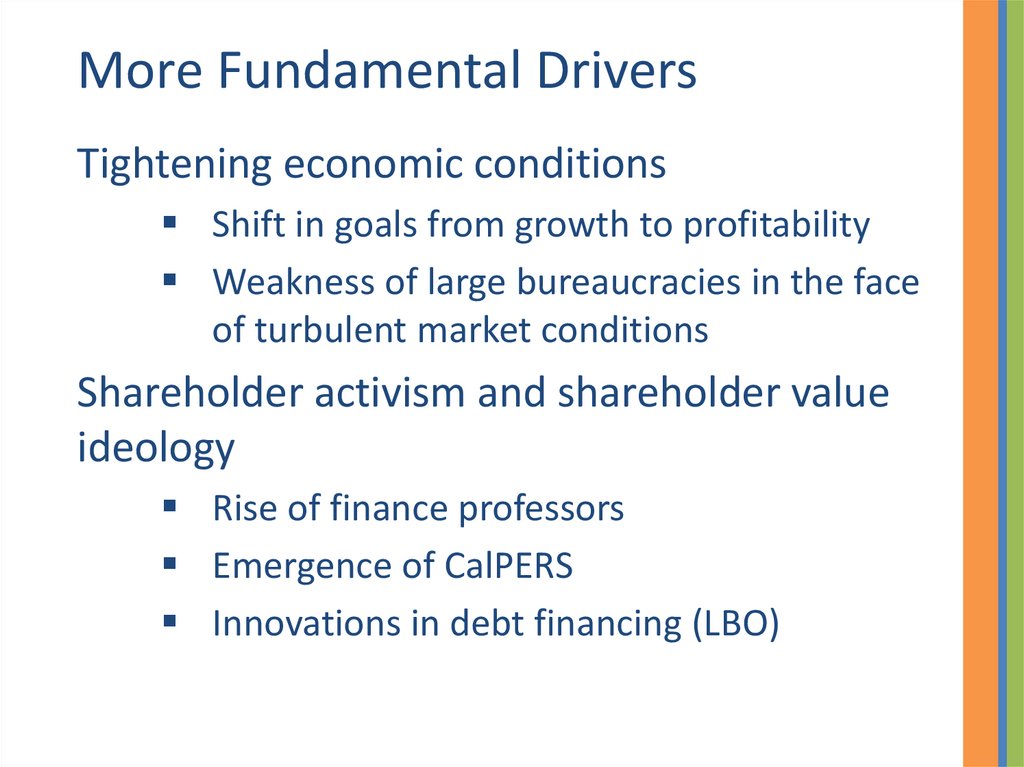

More Fundamental DriversTightening economic conditions

Shift in goals from growth to profitability

Weakness of large bureaucracies in the face

of turbulent market conditions

Shareholder activism and shareholder value

ideology

Rise of finance professors

Emergence of CalPERS

Innovations in debt financing (LBO)

22.

23.

Founded 1984 - 198724.

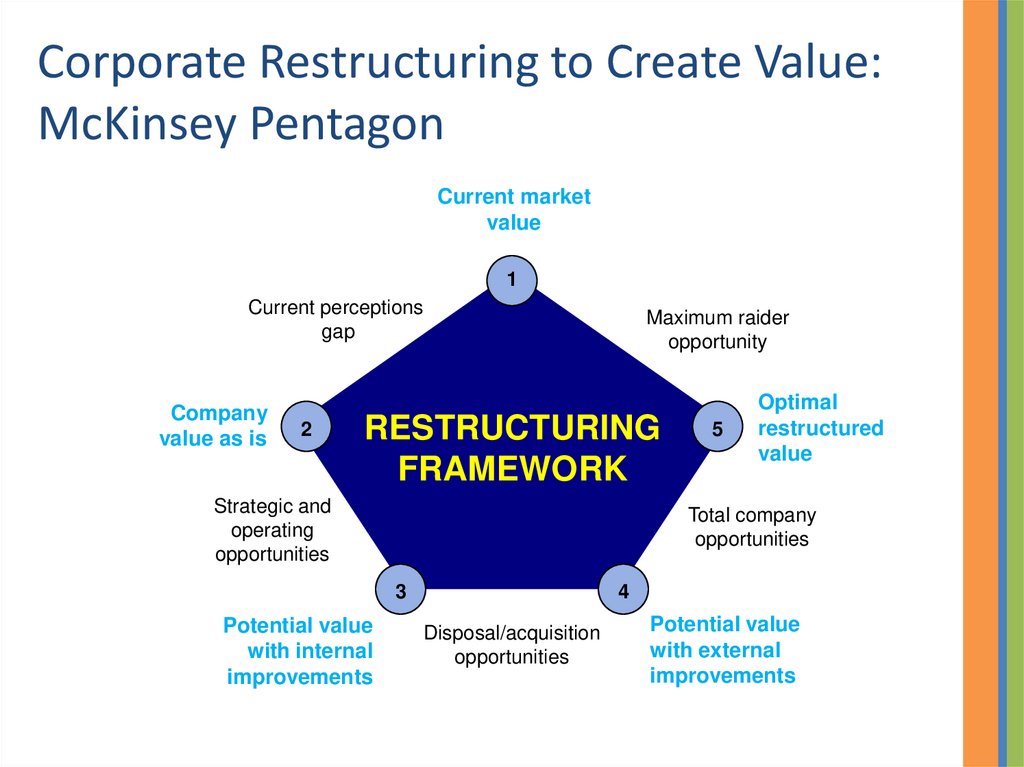

Corporate Restructuring to Create Value:McKinsey Pentagon

Current market

value

1

Current perceptions

gap

Company

value as is

2

Maximum raider

opportunity

RESTRUCTURING

FRAMEWORK

Strategic and

operating

opportunities

Total company

opportunities

3

Potential value

with internal

improvements

5

Optimal

restructured

value

4

Disposal/acquisition

opportunities

Potential value

with external

improvements

25.

The 1990s onwards26.

27.

Honda’scompetence in

small, highpowered engines

28.

Corporate Strategy in the 1990sDistinguishing related from unrelated

diversification

Not all diversification is bad

Diversify around your core competence

Organizational economics

Multiple alternatives for entering new

businesses

M&A, alliances, JVs

29.

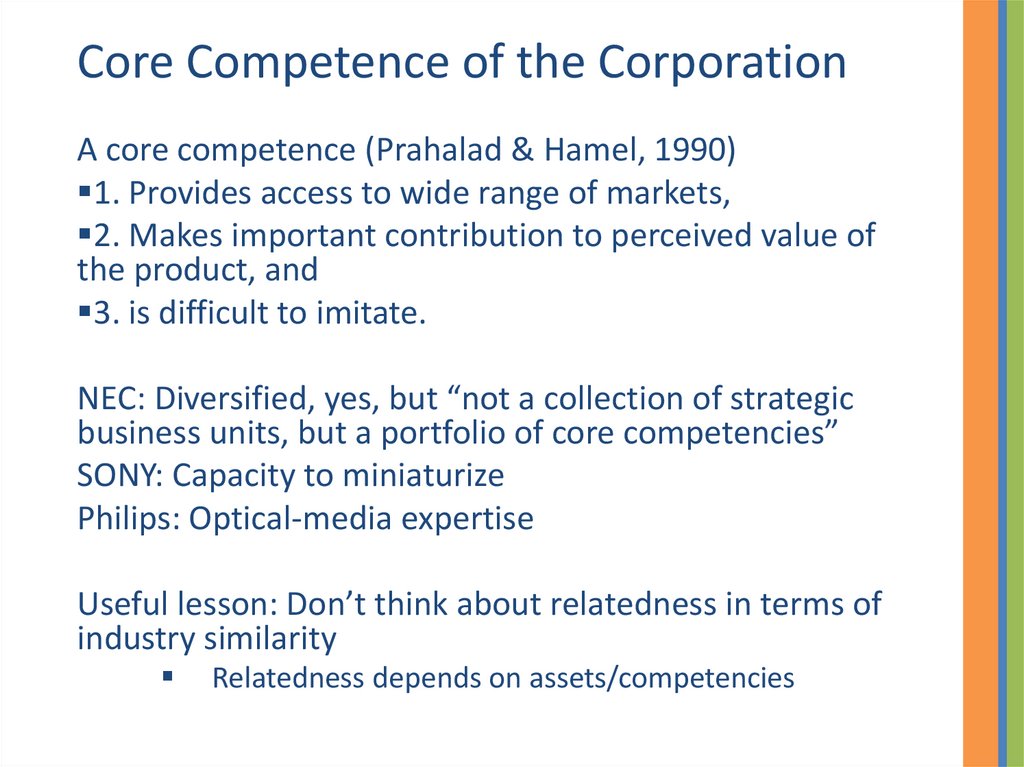

Core Competence of the CorporationA core competence (Prahalad & Hamel, 1990)

1. Provides access to wide range of markets,

2. Makes important contribution to perceived value of

the product, and

3. is difficult to imitate.

NEC: Diversified, yes, but “not a collection of strategic

business units, but a portfolio of core competencies”

SONY: Capacity to miniaturize

Philips: Optical-media expertise

Useful lesson: Don’t think about relatedness in terms of

industry similarity

Relatedness depends on assets/competencies

30.

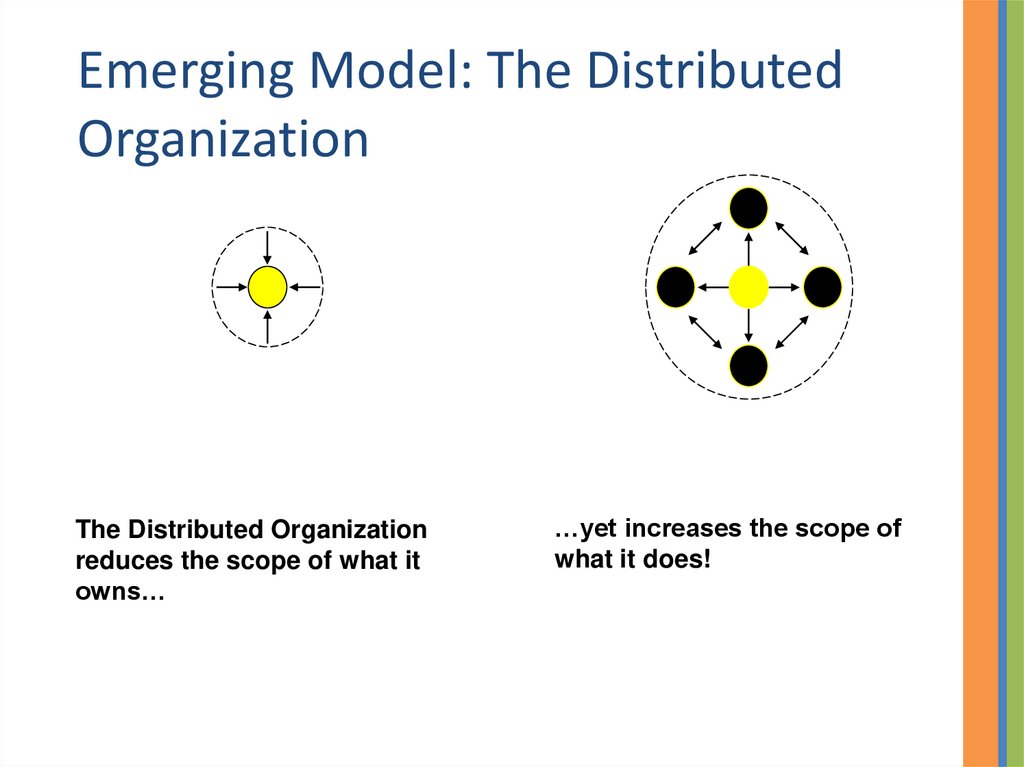

Emerging Model: The DistributedOrganization

The Distributed Organization

reduces the scope of what it

owns…

…yet increases the scope of

what it does!

31.

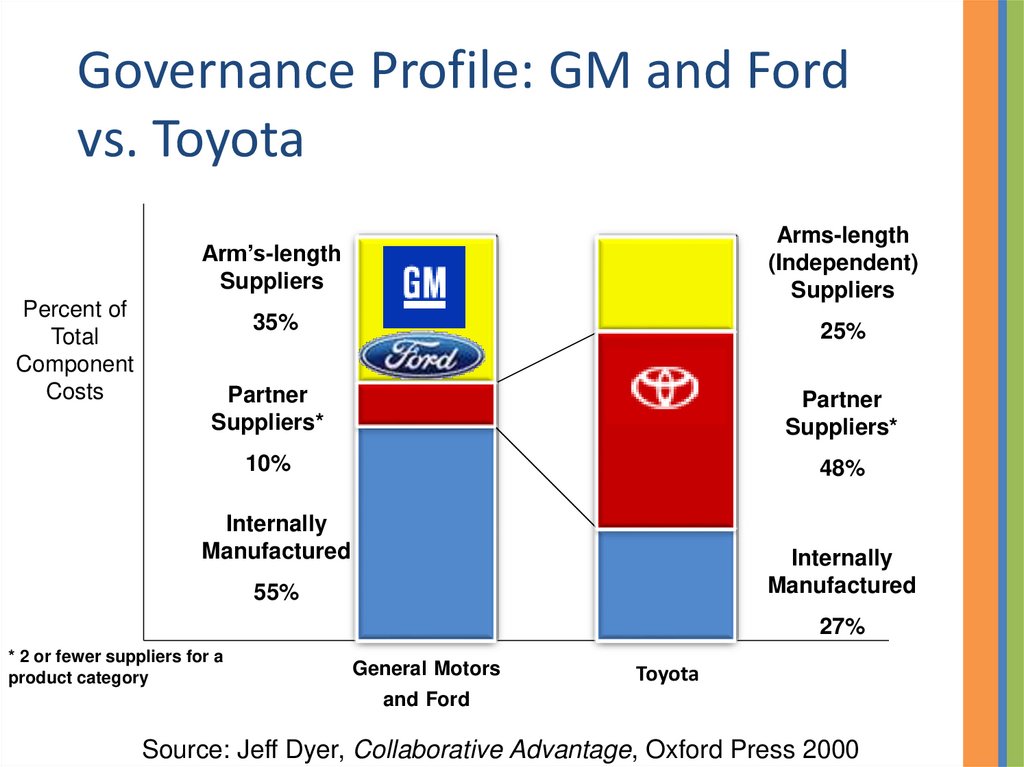

Governance Profile: GM and Fordvs. Toyota

Percent of

Total

Component

Costs

Arm’s-length

Suppliers

Arms-length

(Independent)

Suppliers

35%

25%

Partner

Suppliers*

Partner

Suppliers*

10%

48%

Internally

Manufactured

Internally

Manufactured

55%

27%

* 2 or fewer suppliers for a

product category

General Motors

Toyota

and Ford

Source: Jeff Dyer, Collaborative Advantage, Oxford Press 2000

32.

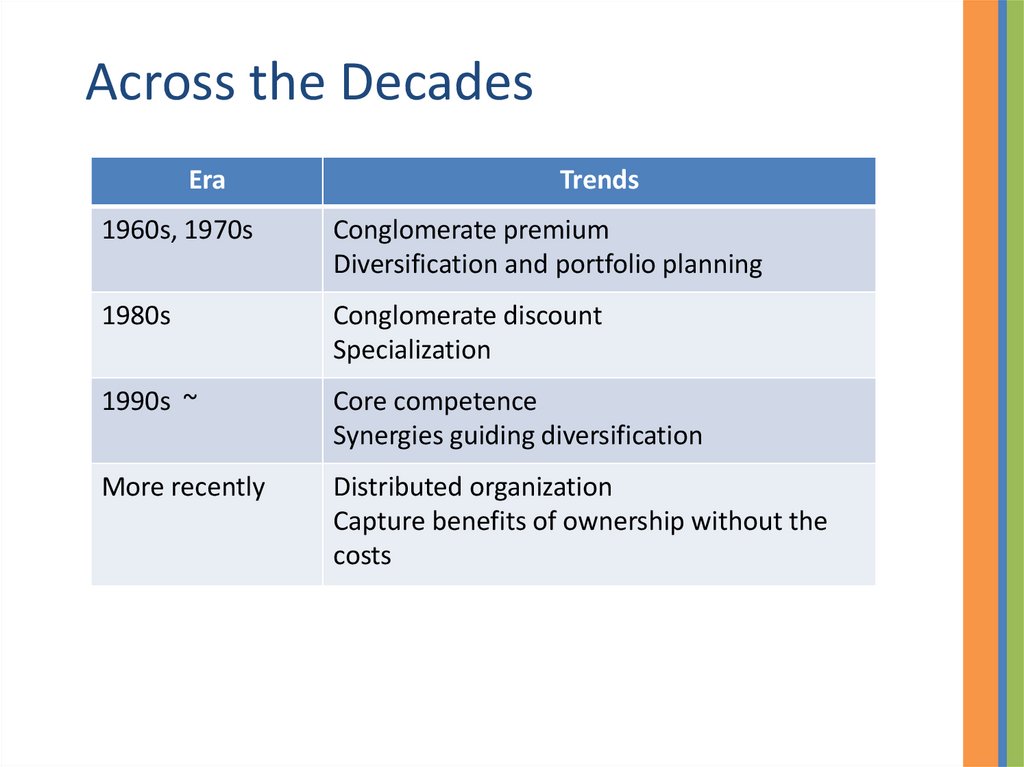

Across the DecadesEra

Trends

1960s, 1970s

Conglomerate premium

Diversification and portfolio planning

1980s

Conglomerate discount

Specialization

1990s ~

Core competence

Synergies guiding diversification

More recently

Distributed organization

Capture benefits of ownership without the

costs

33.

Publicis GroupeCase Discussion

34.

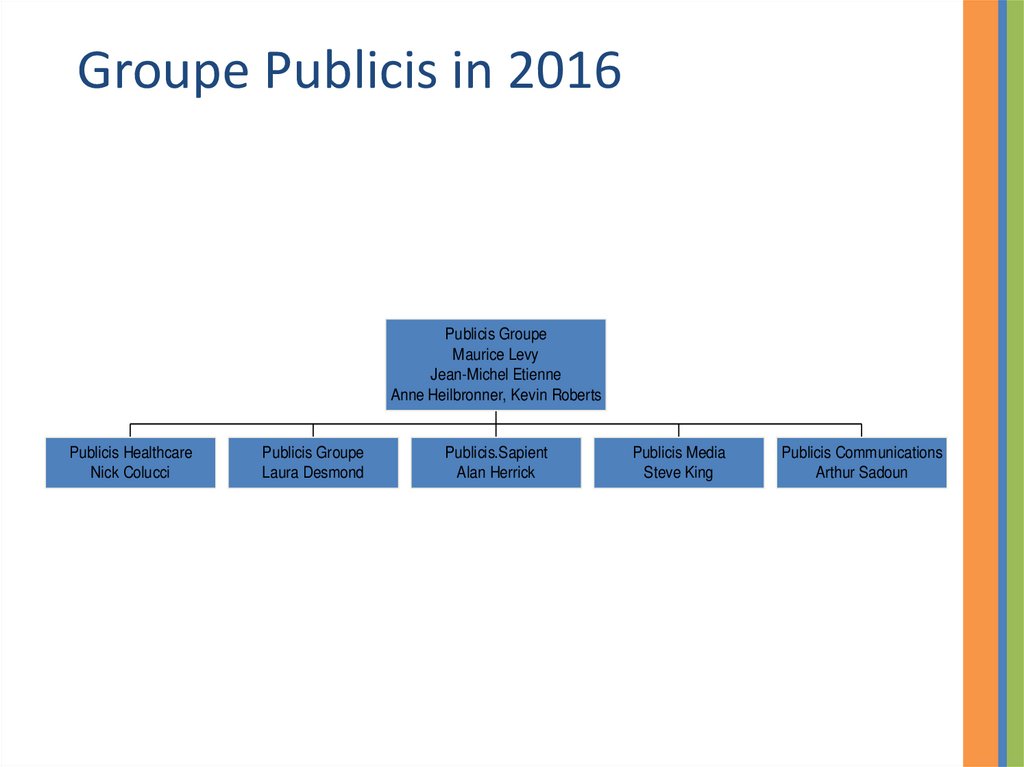

Publicis Groupe35.

Groupe Publicis in 2016Publicis Groupe

Maurice Levy

Jean-Michel Etienne

Anne Heilbronner, Kevin Roberts

Publicis Healthcare

Nick Colucci

Publicis Groupe

Laura Desmond

Publicis.Sapient

Alan Herrick

Publicis Media

Steve King

Publicis Communications

Arthur Sadoun

36. In 2016

How well are they doing?37.

LEVY’S ACHIEVEMENT• Third largest advertising and marketing

communications company in the world

Grown through acquisitions

Many accolades and awards

38.

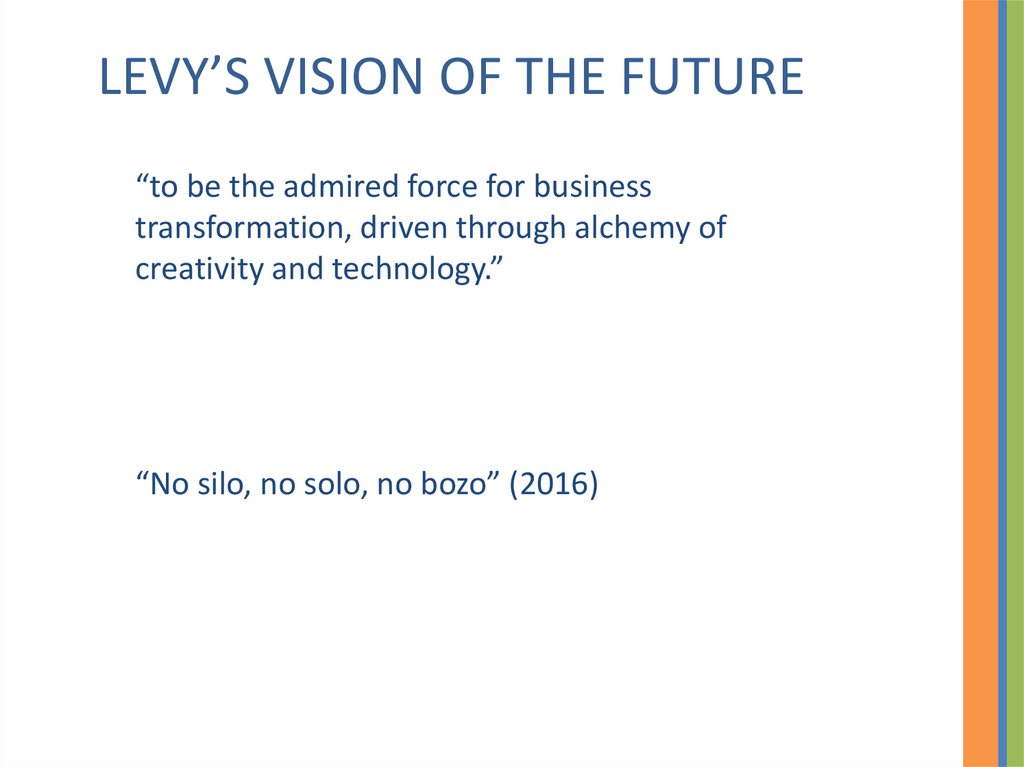

LEVY’S VISION OF THE FUTURE“to be the admired force for business

transformation, driven through alchemy of

creativity and technology.”

“No silo, no solo, no bozo” (2016)

39.

THE REALITYFailed Omnicon merger

Many threats

• Ad-blocking

• Lack of transparency

• Disintermediation

• Questionable necessity

40. DEBATE

“The Power of One reorganizationfrom holding company to “connecting

company” will be a success for Groupe

Publicis.”

41.

A corporation is a portfolio of value chainactivities

Corporate advantage exists if portfolio

performance exceeds the sum of performance

of individual activities

42.

How does Publicis Groupe AddValue?

Financial

Accounting, finance, treasury

Human resources

Compensation, hiring

Strategic development

Partnerships, synergy, leverage

Procurement

Practice development

Virtual companies

43.

ObstaclesConflict of interest

Collaboration with particular businesses

rather than with Publicis Groupe in

general

Best for customer vs. best for Publicis

Groupe

Potentially only small gains from

collaboration for larger businesses

How to overcome these?

44.

Opportunities:Media buying

New technology/media

Emerging markets

Internal communication

Recruitment

45.

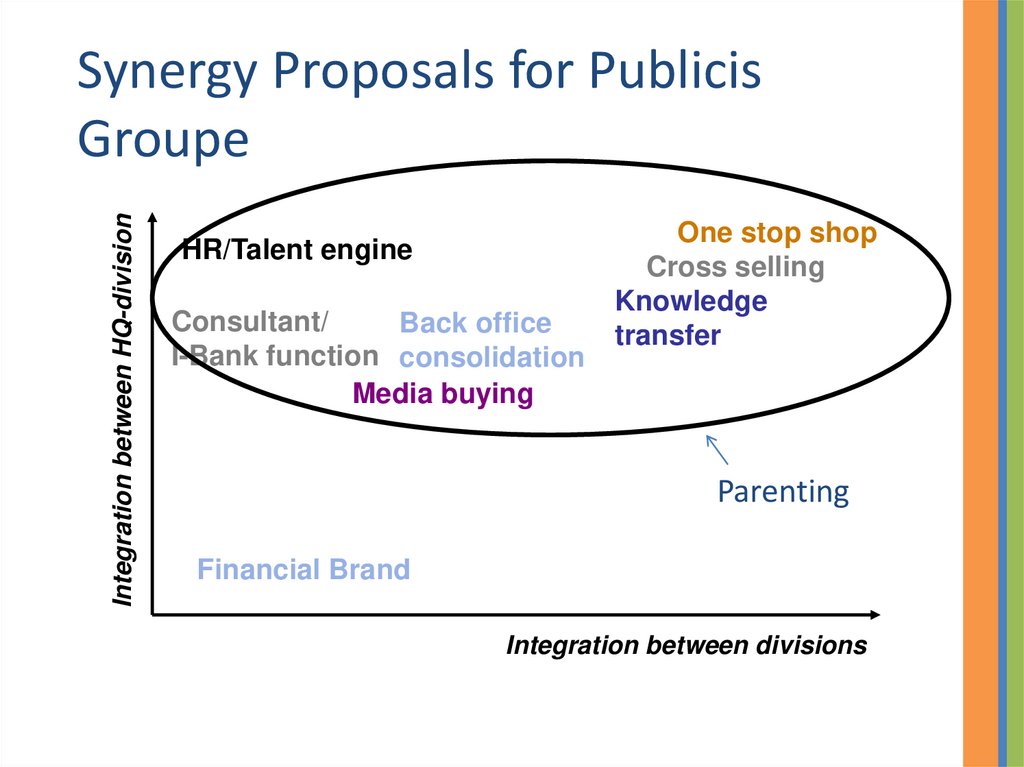

Integration between HQ-divisionSynergy Proposals for Publicis

Groupe

HR/Talent engine

Consultant/

Back office

I-Bank function consolidation

Media buying

One stop shop

Cross selling

Knowledge

transfer

Parenting

Financial Brand

Integration between divisions

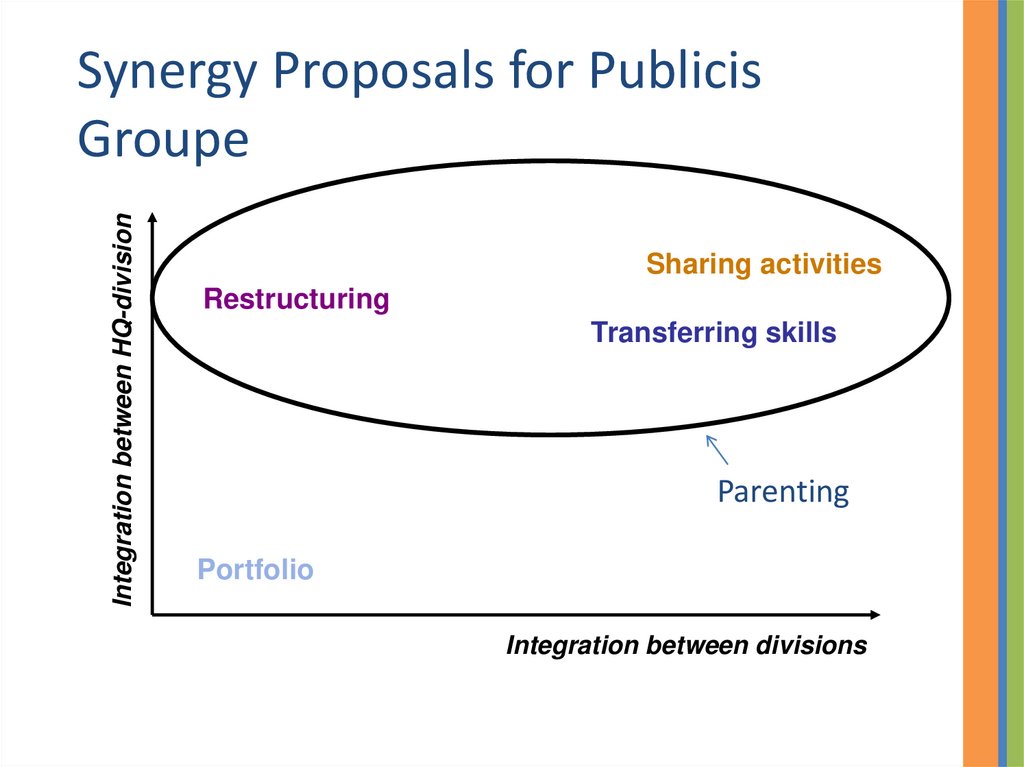

46.

Integration between HQ-divisionSynergy Proposals for Publicis

Groupe

Sharing activities

Restructuring

Transferring skills

Parenting

Portfolio

Integration between divisions

47.

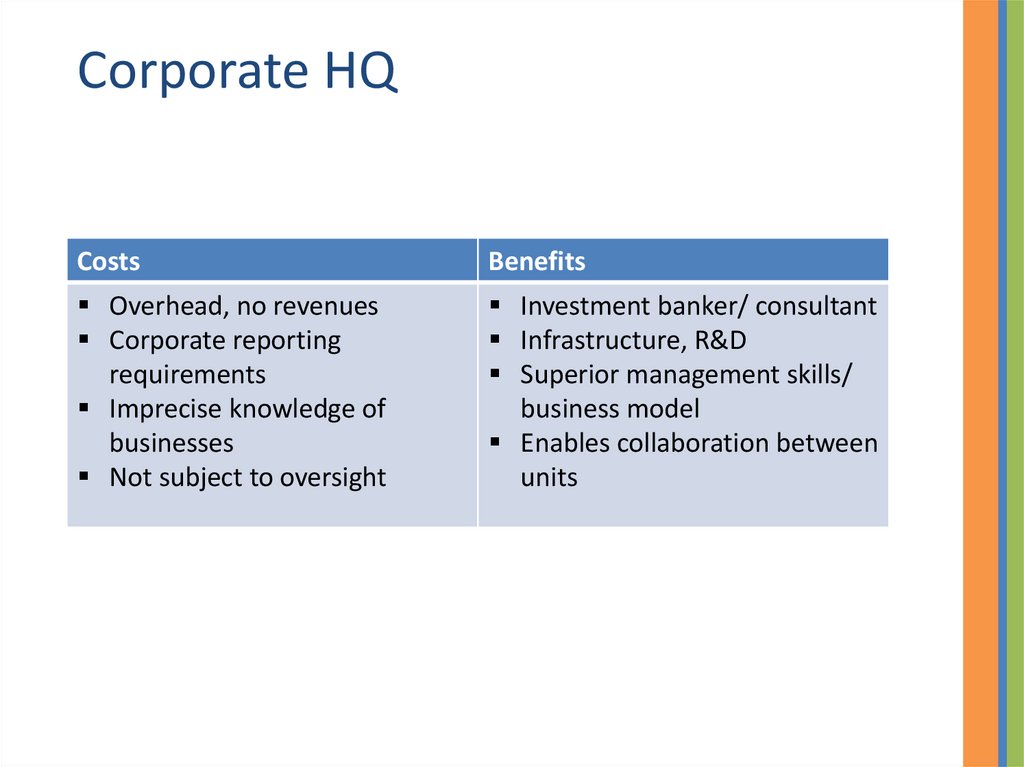

Corporate HQCosts

Benefits

Overhead, no revenues

Corporate reporting

requirements

Imprecise knowledge of

businesses

Not subject to oversight

Investment banker/ consultant

Infrastructure, R&D

Superior management skills/

business model

Enables collaboration between

units

48.

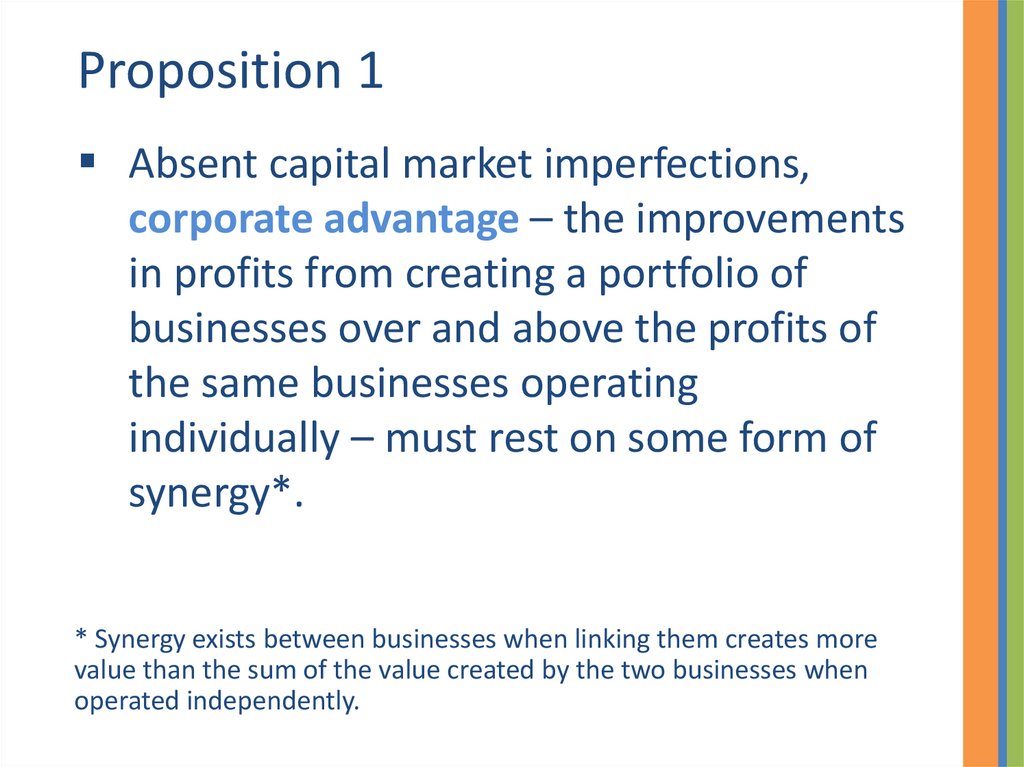

Proposition 1Absent capital market imperfections,

corporate advantage – the improvements

in profits from creating a portfolio of

businesses over and above the profits of

the same businesses operating

individually – must rest on some form of

synergy*.

* Synergy exists between businesses when linking them creates more

value than the sum of the value created by the two businesses when

operated independently.

49.

Corporate AdvantageValue

Independent

Businesses

Integrated

Corporation

50.

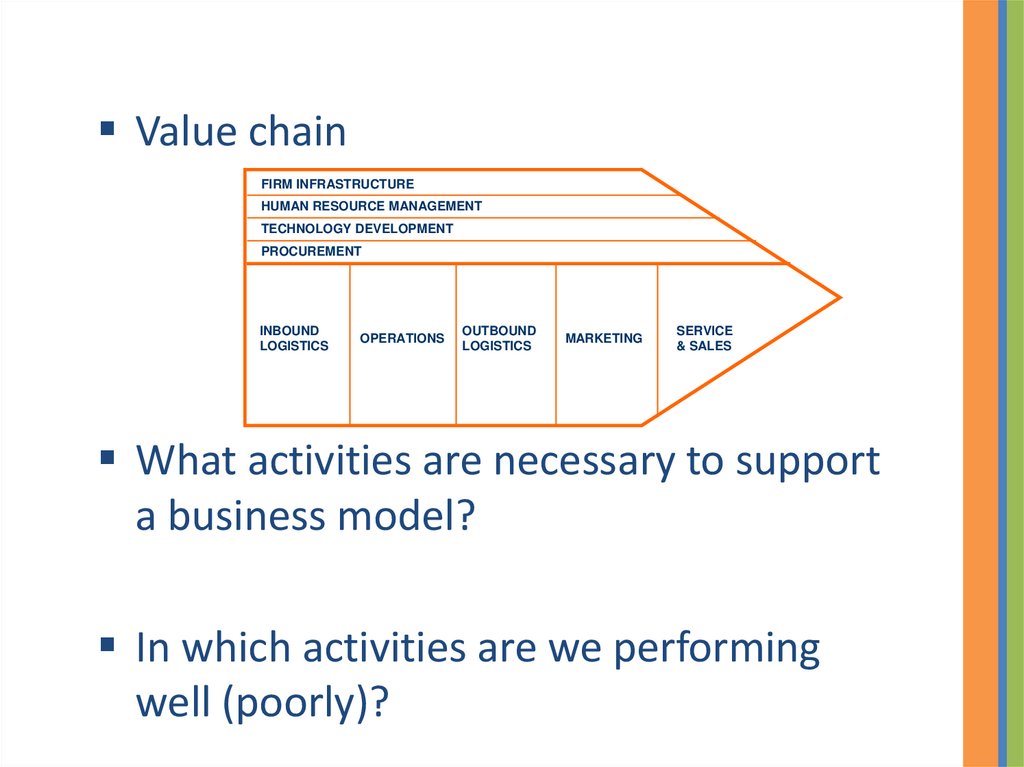

Value chainFIRM INFRASTRUCTURE

HUMAN RESOURCE MANAGEMENT

TECHNOLOGY DEVELOPMENT

PROCUREMENT

INBOUND

LOGISTICS

OPERATIONS

OUTBOUND

LOGISTICS

MARKETING

SERVICE

& SALES

What activities are necessary to support

a business model?

In which activities are we performing

well (poorly)?

51.

Horizontal Synergies across Value ChainsPURCHASE

R&D

MANUFAC.

SALES & DIST.

PURCHASE

R&D

MANUFAC.

SALES & DIST.

52.

Vertical Synergies across Value ChainsUpstream

Downstream

53.

Management Synergies across ValueChains

54.

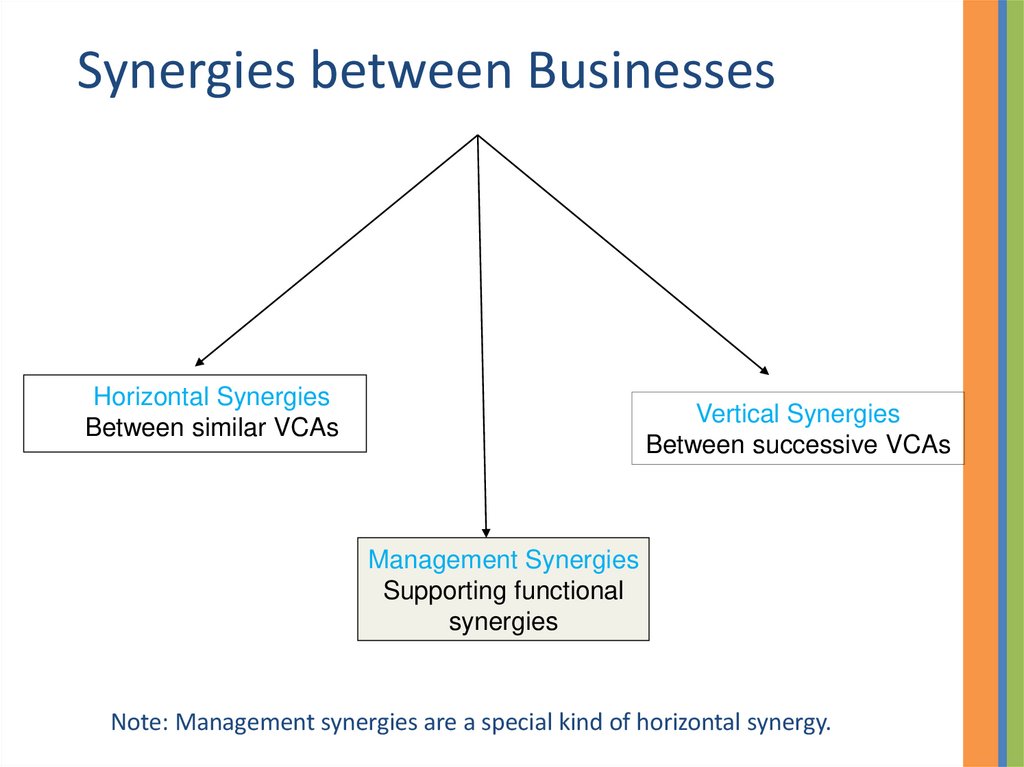

Synergies between BusinessesHorizontal Synergies

Between similar VCAs

Vertical Synergies

Between successive VCAs

Management Synergies

Supporting functional

synergies

Note: Management synergies are a special kind of horizontal synergy.

55.

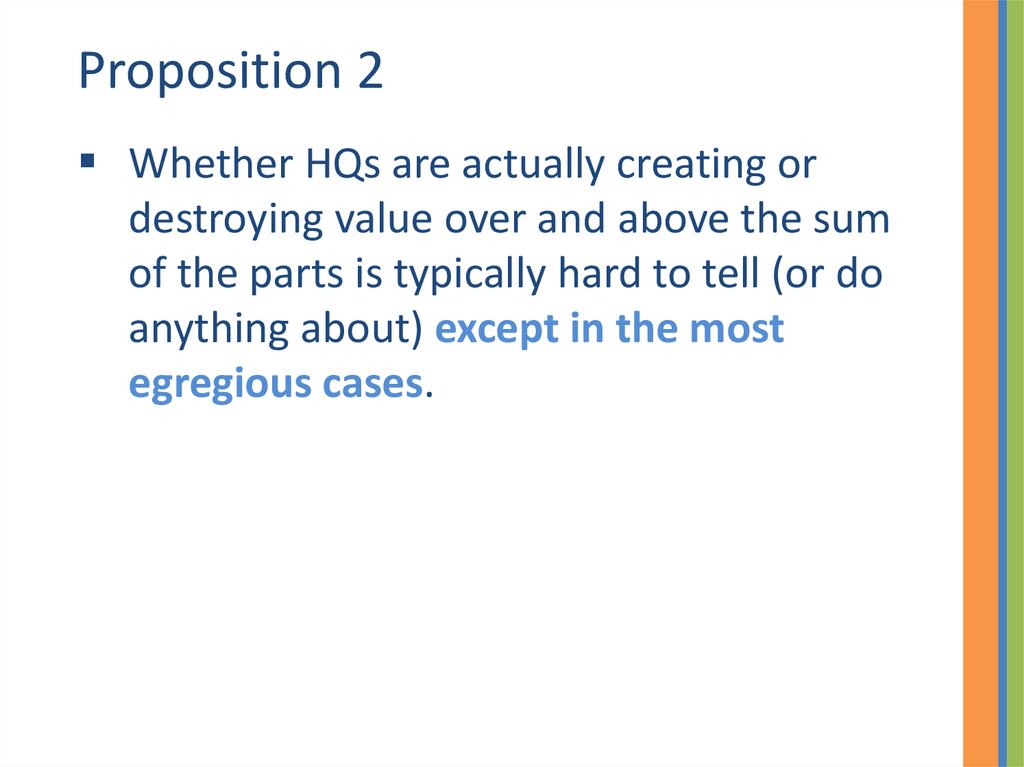

Proposition 2Whether HQs are actually creating or

destroying value over and above the sum

of the parts is typically hard to tell (or do

anything about) except in the most

egregious cases.

56.

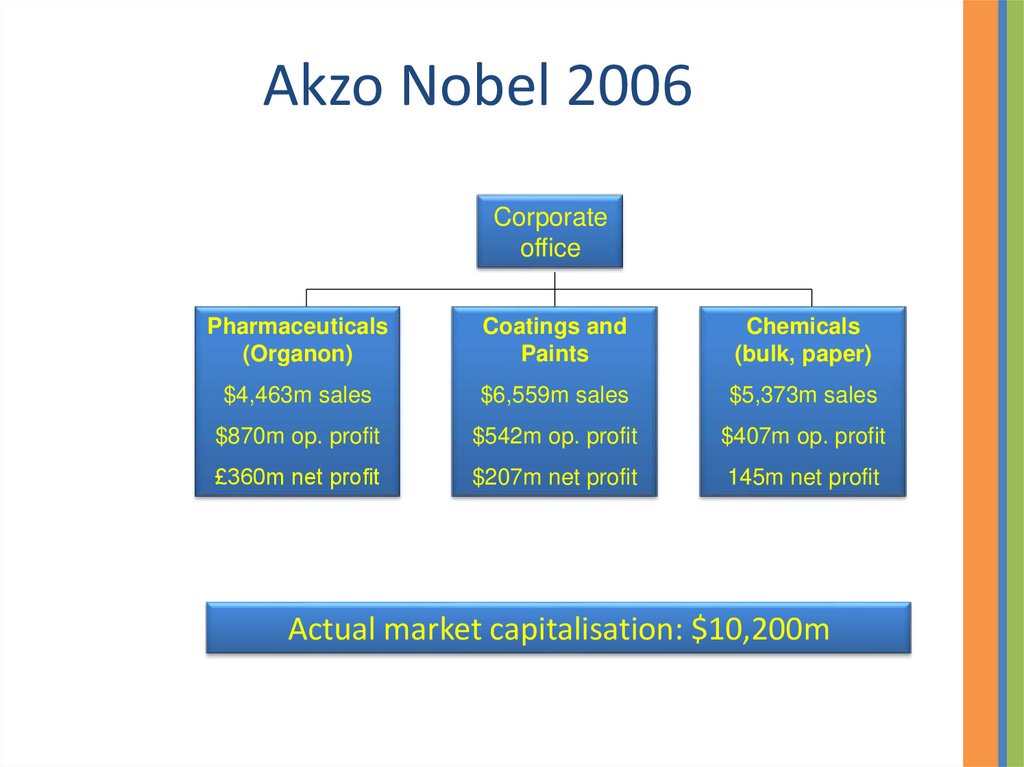

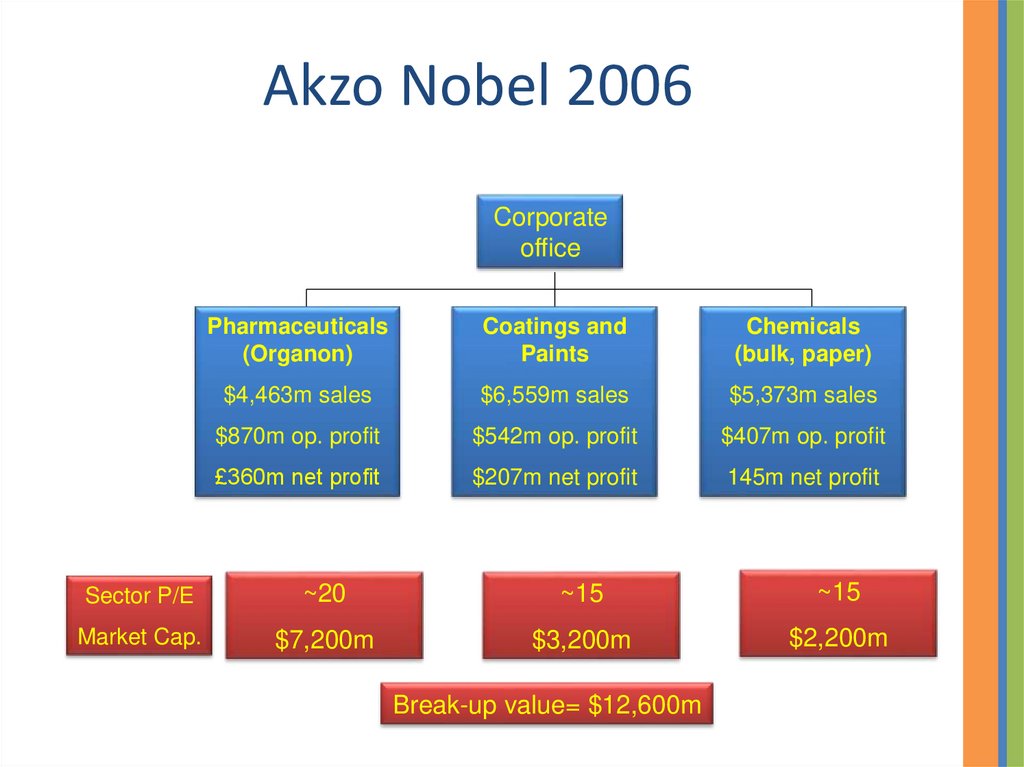

Akzo Nobel 2006Corporate

office

Pharmaceuticals

(Organon)

Coatings and

Paints

Chemicals

(bulk, paper)

$4,463m sales

$6,559m sales

$5,373m sales

$870m op. profit

$542m op. profit

$407m op. profit

£360m net profit

$207m net profit

145m net profit

Actual market capitalisation: $10,200m

57.

Akzo Nobel 2006Corporate

office

Pharmaceuticals

(Organon)

Coatings and

Paints

Chemicals

(bulk, paper)

$4,463m sales

$6,559m sales

$5,373m sales

$870m op. profit

$542m op. profit

$407m op. profit

£360m net profit

$207m net profit

145m net profit

Sector P/E

~20

~15

~15

Market Cap.

$7,200m

$3,200m

$2,200m

Break-up value= $12,600m

58.

Akzo Nobel 2008Corporate

office

Pharmaceuticals

(Organon)

Coatings and

Paints

Chemicals

(bulk, paper)

$4,463m sales

$6,559m sales

$5,373m sales

$870m op. profit

$542m op. profit

$407m op. profit

SOLD to Schering Plough

for $14 billion

Merger with ICI

completed Jan 08

59.

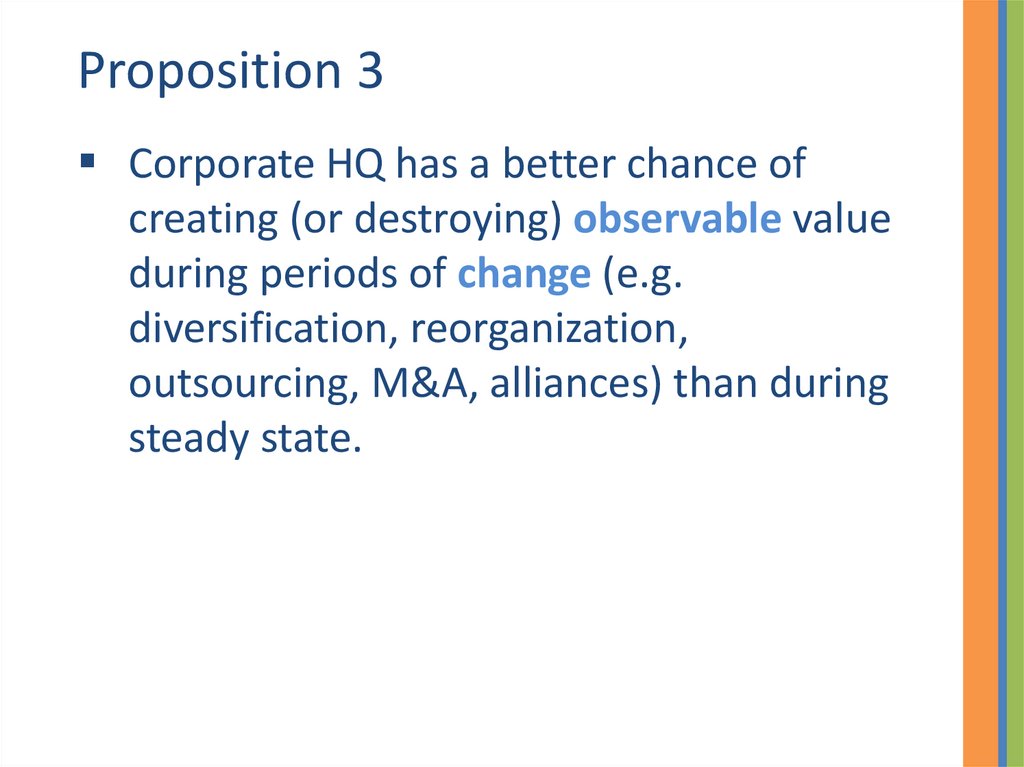

Proposition 3Corporate HQ has a better chance of

creating (or destroying) observable value

during periods of change (e.g.

diversification, reorganization,

outsourcing, M&A, alliances) than during

steady state.

60.

Reflections on Session 21. What synergies might be possible across

different activities in your company?

2. What obstacles do you face in bringing about

collaboration?

3. How can you overcome them?

61. For Next Session

Prepare Ayala caseIf interested, skim Campbell, Goold & Alexander:

Corporate Strategy: The Quest for Parenting

Advantage

62.

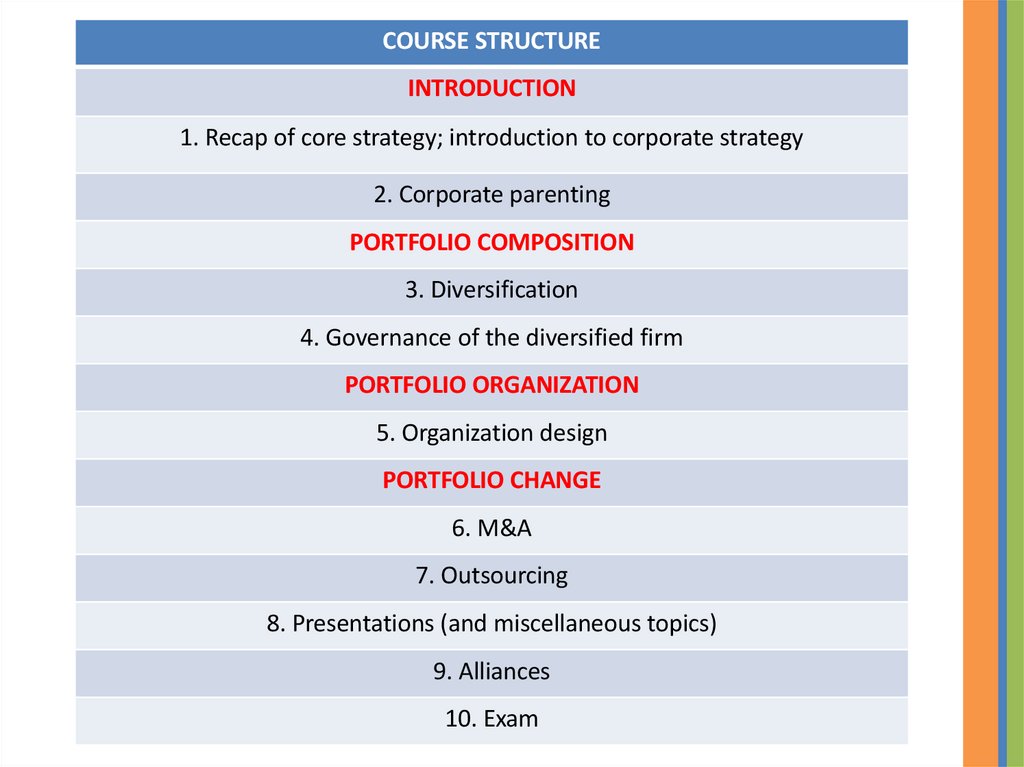

COURSE STRUCTUREINTRODUCTION

1. Recap of core strategy; introduction to corporate strategy

2. Corporate parenting

PORTFOLIO COMPOSITION

3. Diversification

4. Governance of the diversified firm

PORTFOLIO ORGANIZATION

5. Organization design

PORTFOLIO CHANGE

6. M&A

7. Outsourcing

8. Presentations (and miscellaneous topics)

9. Alliances

10. Exam