Экономика

ЭкономикаПохожие презентации:

The audit report

1.

Chapter VIIIThe audit report

2.

Introduction• After the final audit, the last step is to prepare and issue an audit report including the opinion of the

auditor concerning the truth and fairness of the financial statements and if the auditee is maintaining

adequate accounting records.

• In general, there are two types of audit opinion:

- Modified

- Unmodified (better)

However, there are three types of Modified opinions:

-a qualified opinion (better than adverse) --- investors should be careful, but they can trust financial

statements

-an adverse opinion

- A disclaimer of opinion. (I do not know – no opinion) – the auditor did not find the info

3.

The format and content of the audit report• The format and content of the audit report are prescribed by the International

Standard on Auditing 700 (ISA 700). In France, the professional standard NEP700 is

also used.

• In general, the audit report includes the following:

- An introduction identifying the FS that have been audited and the financial reporting

framework adopted for their preparation

- A description of the scope of the audit and the auditing standard applied during the

audit process.

- The opinion of the auditor

4.

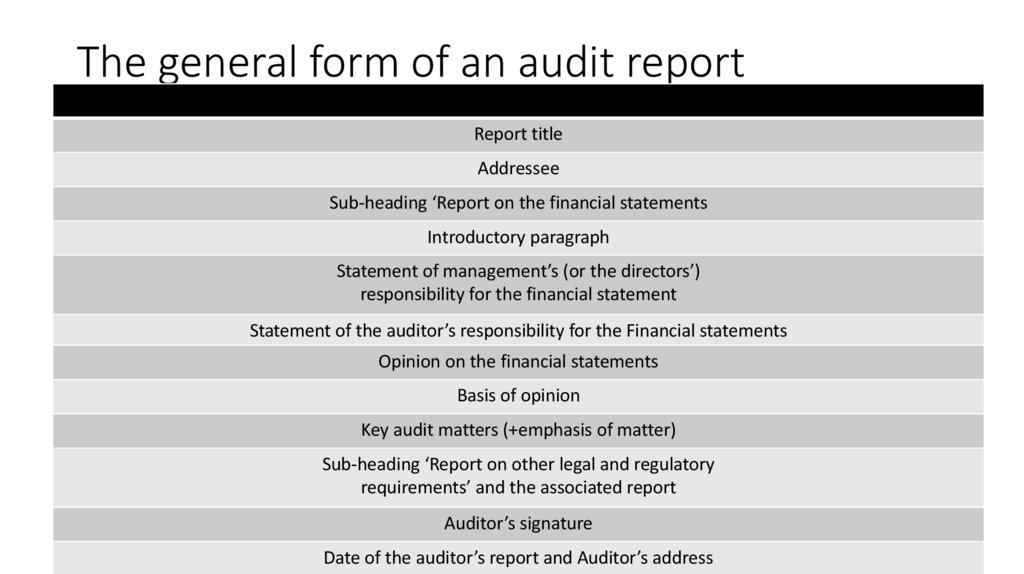

The general form of an audit reportReport title

Addressee

Sub-heading ‘Report on the financial statements

Introductory paragraph

Statement of management’s (or the directors’)

responsibility for the financial statement

Statement of the auditor’s responsibility for the Financial statements

Opinion on the financial statements

Basis of opinion

Key audit matters (+emphasis of matter)

Sub-heading ‘Report on other legal and regulatory

requirements’ and the associated report

Auditor’s signature

Date of the auditor’s report and Auditor’s address

5.

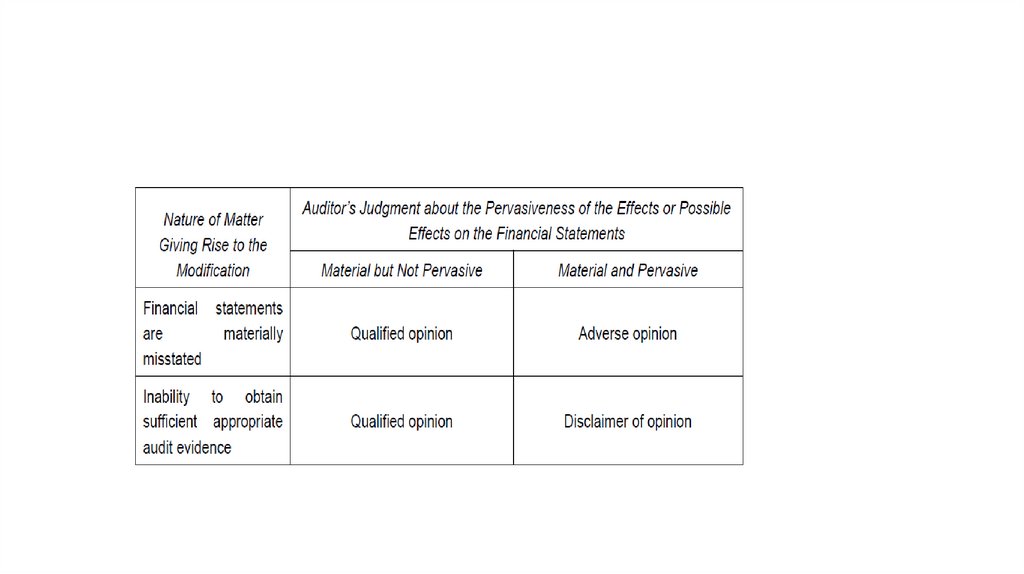

A report with a Modified audit opinion• A modified opinion is expressed when the auditor:

- Concludes that there are material misstatements in the financial statements, or

- Is unable to obtain sufficient appropriate audit evidence to conclude that there are no

material misstatements on the FS.

There are 3 forms of modification depending on the Pervasiveness of the Effects or

Possible Effects on the Financial Statements : (1) A qualified opinion, (2) an adverse

opinion, or (3) a disclaimer of opinion.

6.

A modified opinion because FS are materiallymisstated

• Material misstatements: when accounting policy is not appropriate or not correctly

used (mistakes) or when some required accounting disclosures are missing or not

disclosed following the applicable accounting framework.

- If misstatements are material but not pervasive, a qualified opinion is expressed. The

auditor thinks that the FS gives a true and fair view of the entity’s financial position

and performance except for the matter identified in the audit report.

- If misstatements are material and pervasive and, therefore, FS are seriously

misleading, an adverse opinion is expressed. The auditor thinks that the FS do not give

a true and fair view.

7.

A modified opinion because of the inability to obtainsufficient evidence

• The auditor’s inability to obtain sufficient appropriate audit evidence (also referred to as a

limitation on the scope of the audit) may arise from:

-Circumstances beyond the control of the entity: for example, the entity’s accounting records

have been destroyed or have been seized indefinitely by governmental authorities

- circumstances relating to the nature or timing of the auditor’s work: for example, the timing of

the auditor’s appointment is such that the auditor is unable to observe the counting of the

physical inventories

- Limitations imposed by management: for example, management prevents the auditor from

observing the counting of the physical inventory or requesting external confirmation.

8.

A modified opinion because of the inability to obtainsufficient evidence

• If, in the audit opinion, the effect of this limitation is:

-material but not pervasive, a qualified opinion is expressed. The auditor thinks that the

FS gives a true and fair view of the entity’s financial position and performance except

for the matter identified in the audit report.

-material and pervasive, and therefore, the auditor is unable to form an opinion on the

FS, the auditor disclaims an opinion.

9.

10.

The format of a report containing a modified opinion- A paragraph is inserted prior to the paragraph containing the auditor’ opinion which

explain the reason(s) for the modified opinion.

- The modified opinion with determining the Type of Modification to the Auditor’s

Opinion

11.

Exercise• What is your opinion, on these cases:

- The management prevented you from attending the physical inventory, you used

alternative techniques to assess the quantity and value of the ending inventory. Your

investigation did not show material misstatements on the FS. (unmodified – but he can

mention it in the “key audit matters” )

- The management prevented you from attending the physical inventory and you were not

able to use alternative techniques. Inventory is not a significant item on the total asset

(only 3% of the value of total assets). (qualified)

- The management prevented you from attending the physical inventory and you were not

able to use alternative techniques. Inventory is an important item on the total asset (40%

of the value of total assets). (disclaimer)

- You detected that some methods used to evaluate inventory are not appropriate leading

to a material misstatement on inventory entries but given the low value of inventories

compared to total assets, this has no material impact on the entire balance sheet.