Экономика

ЭкономикаПохожие презентации:

")

Introduction to Long-Run Fiscal Policy

1.

Introduction to Long-Run FiscalPolicy

• Fiscal policy isn't just about managing shortterm recessions and inflation.

• This lecture explores how fiscal choices—

particularly deficits and surpluses—affect

long-run outcomes.

• Key focus: How government borrowing

impacts national saving, investment, and

economic growth over time.

2.

National Saving and InvestmentIdentity

• Investment funds in an economy must come

from somewhere:

• - Private savings

• - Government savings (or borrowing)

• - Foreign capital (via trade deficits)

• When the government runs a deficit, it

reduces national saving. The gap must be

filled by:

3.

Ricardian Equivalence Theory• This theory suggests that when the

government borrows, individuals save more in

anticipation of future taxes.

• Globally, evidence is mixed—some offsetting

behavior is observed.

• But in the U.S., this offset doesn’t seem to

occur. Historical deficits were not matched by

higher private savings.

4.

Crowding Out Effect on Investment• Increased government borrowing competes

with the private sector for capital.

• Evidence from the U.S. shows that:

• - 1990s: Surpluses → rising private investment

• - 2000s: Deficits → falling private investment

• Less investment harms innovation and longterm economic growth.

5.

Crowding In Effect on Trade Deficit• Government borrowing can draw in foreign

capital → Larger trade deficits.

• Historical patterns:

• - 1980s and 2000s: Twin deficits—budget and

trade deficits rose together.

• - However, budget surpluses in the 1990s

didn’t produce trade surpluses—investment

absorbed the funds instead.

6.

Short vs. Long-Term Impacts ofDeficits

• Short-term deficits during recessions can help

boost demand—this is often appropriate.

• Long-term, persistent deficits create structural

problems:

• - More borrowing = rising national debt

• - Less flexibility in future fiscal policy

• - Pressure on private investment and trade

balance

7.

U.S. Debt History and Trends• Four major debt surges in the 20th century:

• - WWI, WWII, Great Depression, 1980s

• Debt-to-GDP peaked at ~100% in WWII.

• Dropped to 25% by the 1970s, then rose again

in the 2000s.

• Current debt levels aren’t record-breaking—

but trends point upward.

8.

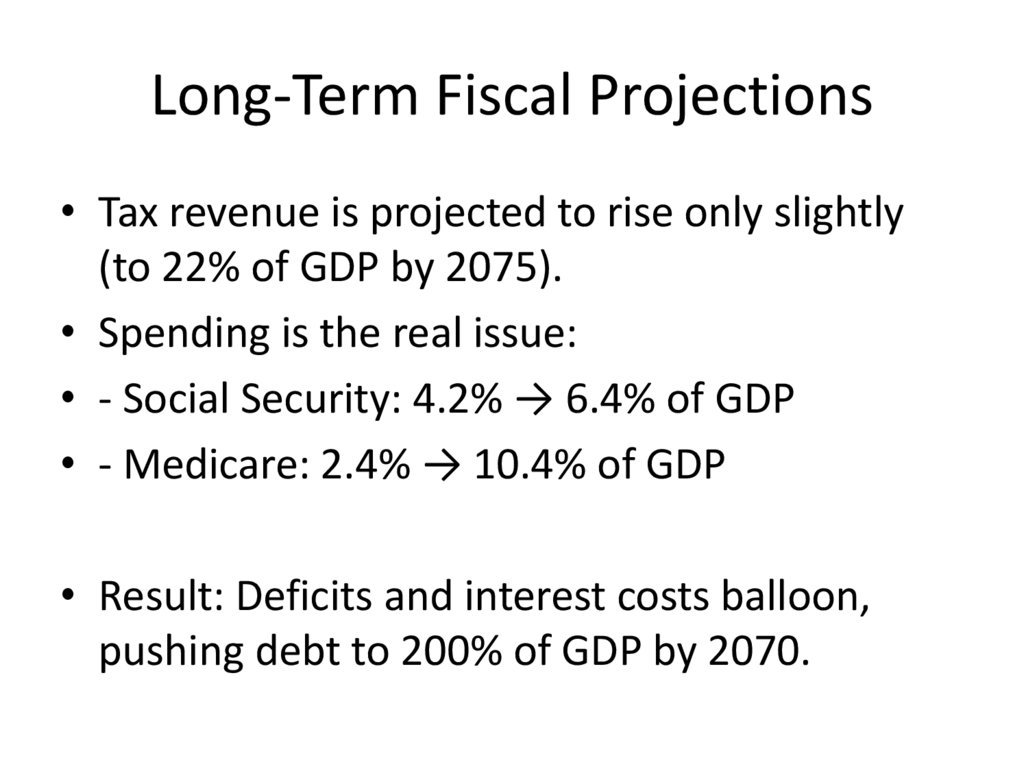

Long-Term Fiscal Projections• Tax revenue is projected to rise only slightly

(to 22% of GDP by 2075).

• Spending is the real issue:

• - Social Security: 4.2% → 6.4% of GDP

• - Medicare: 2.4% → 10.4% of GDP

• Result: Deficits and interest costs balloon,

pushing debt to 200% of GDP by 2070.

9.

The Real Threat—HealthcareSpending

• Medicare and Medicaid are the biggest fiscal

pressures.

• Healthcare alone is set to outgrow all other

federal spending.

• Rising health costs will drive long-term deficits

more than Social Security.

• Interest on debt adds another layer of

compounding risk.

10.

Policy Solutions? Not Easy• Cutting spending: Unlikely due to political

resistance and existing commitments.

• Raising taxes: Would require unprecedented

hikes—doubling federal tax revenue.

• Boosting private saving: Tax-favored accounts

like IRAs/401(k)s haven't worked.

• Most proposals only slow growth of deficits,

not reduce them.

11.

Radical Proposals for Private Saving• New ideas propose mandatory or default

saving systems:

• - Conservative: Private retirement accounts

requiring contributions

• - Liberal: 'Liberal paternalism'—automatic

saving unless you opt out

• These ideas aim to boost saving without direct

tax hikes or spending cuts.

12.

A Grim but Honest Outlook• None of the options look likely:

• - Spending cuts? Politically improbable.

• - Major tax hikes? Unpopular and extreme.

• - Private saving increase? Not enough.

• Without action, huge deficits and trade

imbalances loom.

• “As economist Herb Stein said: 'If something