Английский язык

Английский языкПохожие презентации:

")

")

")

Insurance policy formation. Lecture 3

1. Lecture 3 Insurance policy formation

Hasan UmarovFinance Department

2. Lecture 3. Learning Outcomes:

• Describe the structure, function and content of aninsurance policy

• Explain why there are certain common policy exceptions

and conditions

• Differentiate between excesses, deductibles and

Lecture 3.

franchises

Learning Outcomes: • Explain how excesses, franchises and deductibles are

applied

• Differentiate between warranties, conditions and

representations

• Explain the significance of procedures relating to renewals

• Explain the meaning and significance of the cancellation

clause

Finance Department

2

3. Introduction

There are three things to remember about the insurance policy:1. the policy will contain the details of the terms and conditions;

2. generally speaking, neither party can rely on any negotiations leading up to

the contract, only on the contract itself; and

3. the policy is only evidence of the contract and not the contract itself.

Finance Department

3

4. Structure, form and content

A policy is generally issued in a scheduled form, i.e. the policy wording is preprinted, often in a booklet, and a schedule is incorporated into the policy. The policyschedule contains all the variable information concerning the insured and details of

the risks insured.

Every insurer has its own form of policy for the various classes of business it offers,

and these vary considerably in style and length.

Finance Department

4

5. Structure, form and content

The basic structure of all general insurance policies:HEADING

PREAMBLE

SIGNATURE

CLAUSE

• It includes the name of the insurer and identifies the class of the policy and is

displayed at the top of the first page. This section states what kind of policy it

is, whether it’s a motor insurance policy, fire policy, marine policy, etc.

• It primarily states that the insured has paid the premium and signed the

proposal form, which forms the basis of this insurance contract.

• Below the preamble, there will frequently be the pre-printed signature of an

official from the company (this tradition is coming from the old times, when

policies were prepared by hand and it’s not strictly necessary today).

Finance Department

5

6. Structure, form and content

• It details the type of the event insured. This contains the promise of insurance company tocompensate for any loss or damage suffered due to the operation of the peril insured under the

policy. The detailed list of perils covered under the policy is captured to ensure that both parties are

OPERATIVE

on the same page regarding the coverage offered.

CLAUSE

• It gives details of the items specifically not covered under the insurance

contract. This is very important to clarify what may not be covered to avoid

EXCLUSIONS

any disputes.

• They capture the standard conditions as applicable to the insurance contract.

The conditions specify the rights & duties of both insured and insurer. Also

treatment of some specific circumstances is also detailed to avoid any

CONDITIONS

dispute.

Finance Department

6

7. Structure, form and content

SCHEDULE• The schedule captures the specific details of the insured and the

property insured like name, address, sum insured, details of the items

covered, period of insurance, etc.

• This may include definitions of words/phrases used in the wording;

customer service standards statement (e.g. response times), complaints

procedure, claims information (e.g. what to do in case of event of loss)

INFORMATION

& FACILITIES

Finance Department

7

8. Exclusions & Exceptions

Exclusions & ExceptionsExclusion and exceptions are used interchangeably. For practical purposes they

mean the same sing. All insurance policies contain some general exceptions.

Most general insurance policies will contain two types of exclusion:

• General – these apply to all sections of the policy and allow the insurer to deny

cover under the policy, regardless of the section concerned.

• Specific – these apply to particular parts of the policy. For example, under a

household contents policy there may be an exclusion relating to antiques and

works of art. This clearly wouldn’t be relevant to the buildings section.

Some general exclusions are common to all general insurance policies and are

called market or standard exclusions.

Finance Department

8

9. Most typical exclusions & exceptions

Most typical exclusions & exceptionsExclusions include systemic losses, which impact multiple policyholder at once:

1. War and related perils only physical war, not cyber war. It is a fundamental risk

(meaning that it applies to the whole society) and it is usually the responsibility of the

government. Marine and aviation policies can be extended to war risks. Fundamental

risks can be insured in certain regions (e.g. earthquake is the fundamental risk in

California, but can be insured in Uzbekistan);

2. Radioactive contamination and explosive nuclear assemblies it is a

contamination as a result of a nuclear accident and liability for nuclear installations. It is

usually accepted (if accepted) by “market pools” (by several insurers&reinsurers in

accordance their underwriting capacity);

Finance Department

9

10. Most typical exclusions & exceptions

Most typical exclusions & exceptions3. Terrorism

4. Pollution and/or contamination it exists in most property policies, as insurance is

extended to the property only, not the liability of the property owner. However, if pollution

and/or contamination causes a damage to the property, then it is covered.

This exclusion became especially important after the “Exxon Valdez” oil spill in 1989 and

the Bhopal disaster in 1984.

Public liability insurance policies cover risks from an unexpected, identifiable events, not a

gradually operating cause. Gradual pollution is insured under an ”Environmental

impairment policy”;

Finance Department

10

11. Most typical exclusions & exceptions

Most typical exclusions & exceptions5. E-risks insurers are concerned regarding cumulative effect of “e-risks”. But, some

this exclusion can be “buy-backed” in some policies for additional premium;

6. Marine policies they are different from other insurance policies, regulated

specifically by “Marine Insurance Act 1906”, presence of international risks, etc. Besides,

there is a necessity to avoid double insurance;

7. Contractual liability insurance does not apply to liability assumed by the insured

under any contract or agreement

8. Sonic bangs damage arising from pressure waves from aircraft or aerial devices

travelling at sonic or super-sonic speeds

Finance Department

11

12. Conditions

Conditions can be either implied or express. The main conditions that appear areas follows:

1. Duties of the insured

2. Alteration the insured is obliged to notify the insurer about any changes that

might increase or worsen the “quality” of the risk

3. Action by the insured in the event of a claim how soon the claim should be

notified; the method of notification, etc.

4. Fraud there are severe consequences in case of fraudulent acts

5. Reasonable precautions fundamental condition - the insured should always

act as it is not insured. Insurance policy should not be an excuse for

carelessness or inactivity

Finance Department

12

13. Conditions

6. Contribution in case of presence of other insurance coverage. If any item isinsured under two policies (i.e. dual insurance), the insured should not get more

than its value (this is principle of indemnity);

7. Subrogation

8. Average this is applied in case of underinsurance. The formula would be

(value insured under the policy / value at risk) x the loss

9. Arbitration

10. Cancellation

Finance Department

13

14. Excesses, deductibles and franchises

An excess is the first amount of each and every claim for which the insured isresponsible. Theoretically, the insured is their own insurer for the value of the

excess. Excesses may be:

• compulsory: imposed on the insured by the insurer;

• voluntary: being accepted by the insured in return for a premium discount.

A deductible is, essentially, a very large excess. This is increasingly prevalent with

commercial insurances.

A franchise is a fixed amount or period that acts as a threshold to determine

whether claims are payable. Once the amount or period is exceeded, the claim is

payable in full: nothing is deducted. If it is not exceeded, however, nothing is

payable.

Finance Department

14

15. Examples of insurance policies

1. https://anyflip.com/skys/omww/basic2. https://www.generalicentrallife.com/media/391420/fg-saral-bima_policydocument_tracked.pdf

3. https://www.generalicentralinsurance.com/downloads/health-insurance/fg-healthabsolute/policy-wording/fg-health-absolute-policy-wordings.pdf

4. https://s3.ap-south-1.amazonaws.com/dittopartners/Smart_Super_Health_Policy_Wordings_445920df63.pdf

Finance Department

15

16. Insurance policy vs. Insurance Contract

Although the words “insurance policy” and “insurance contract” are often usedinterchangeably, there are important distinctions.

• No legal obligations are created by the mere existence of a written insurance policy. It is

simply a recitation of terms&conditions, which do not attach to a particular person, item or

interest.

• By contrast, an insurance contract creates contractual obligations between the

parties. The formation of insurance contracts is governed by the law of contracts. There

must be offer and acceptance, and agreement on all material terms, including the

premium, the nature and duration of the risk to be covered, and the extent of liability.

• An insurance policy may evidence the existence of an insurance contract because parties

will often agree, as part of their contract, to be bound by the terms and conditions as set

out in the policy.

See the Ontario Court of Appeal's decision in Van Huizen v. Trisura Guarantee Insurance Company, 2020 ONCA 222

Finance Department

16

17.

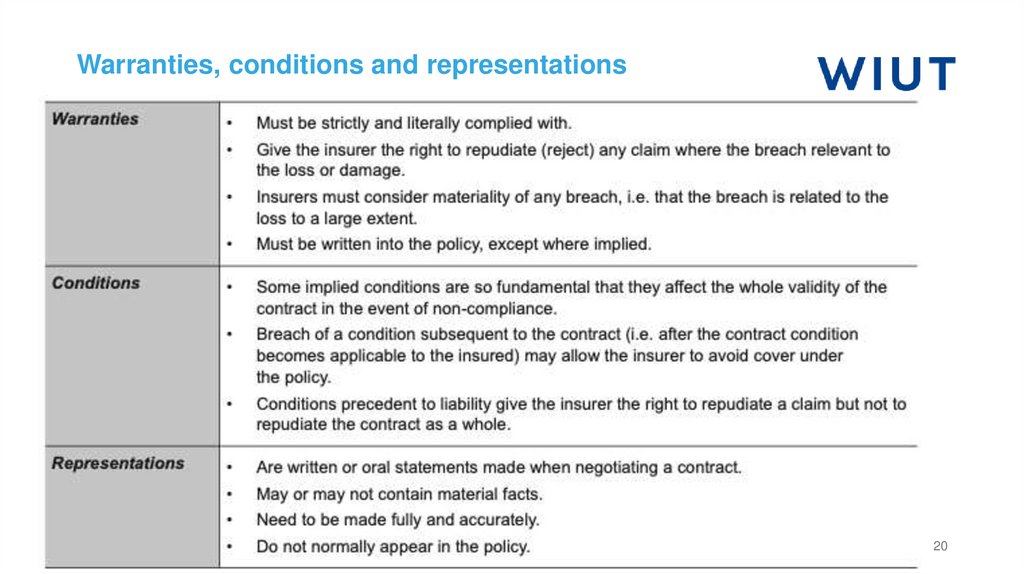

Warranties, conditions and representationsWarranties are promises made by the insured relating to facts or performance concerning

the risk. It is an undertaking by the insured that:

• something will or will not be done (e.g. no inflammable oils may be stored; no movement

of equipment to another place; etc.)

• a certain fact exists or does not exist this is a continuing warranty, meaning that the

insured promises that a state of affairs will continue to exist (e.g. all outside doors to be

locked; the burglar alarm should be on; etc.)

A warranty must be exactly complied with. If it is breached, an insurance cover will not be on

until the breach is fixed.

Finance Department

17

18.

Warranties, conditions and representationsPolicy conditions are terms, which although they are not warranties, impose important

obligations upon the insured. The effect of a breach of condition is very serious and will vary

depending on which of the following categories the condition falls in:

• conditions precedent to the contract (e.g. the policy will not come into effect until the

premium is paid)

• conditions subsequent to the contract (e.g. the employer should keep a record of wages

in proper wages book under the employer’s liability insurance policy)

• conditions precedent to liability (or to recovery) (e.g. notification of loss within a specified

time).

Finance Department

18

19.

Warranties, conditions and representationsRepresentations are written or oral statements made during the negotiations for a contract.

Some may contain material facts and others may not but they need to be made fully and

accurately. Representations do not normally appear in the policy.

Finance Department

19

20.

Warranties, conditions and representationsFinance Department

20

21. Renewals and cancellation

Most general insurance policies are issued for a period of twelve months. Towardsthe end of that period they are said to be due for renewal.

The reasons why insurers keen on to encourage renewal of policies are twofold:

• Statistics If the client base remains stable, statistical information about the

portfolio will be more accurate.

• Cost Policy renewal is a lot cheaper than acquiring new business: think of the

marketing costs involved.

Finance Department

21

22. Renewals and cancellation

Policy renewal should be offered “in good time”.In accordance with the FCA of the UK, insurers at renewal, should:

1. Disclose the previous year’s premium on renewal notices

2. Include text to encourage consumers to check their cover and shop around for

the best deal at each renewal

3. Identify consumers who have renewed with them 4 consecutive years and

give them an additional notice to shop around (these changes happened

following unfairly good conditions given to new customers and absence of

competition at renewal)

Finance Department

22

23. Renewals and cancellation

The cancellation condition in an insurance policy defines how an insurance contract canbe cancelled during its currency, generally by the insurer. The insurer usually has to send at

least seven days' written notice of cancellation by recorded delivery to the insured's last

known address (most often, cancellation period is 30 days).

An insured may also have the right to cancel mid-term but, in this case, a short-period

premium may be charged, giving a less-than-proportionate refund. This is because,

most of the expenses in administrating insurance occurs at the start of the policy (checking

the proposal, giving quotations, setting up the policy, reconciling the premium, etc.).

If the insured claimed a loss and then cancels policy, no refund may be given (if in the 1st

year of policy, the insured had a loss, he can cancel the policy for the 2nd year).

Finance Department

23

24. Renewals and cancellation

Short-term policies (like travel insurance, baggage insurance) for less than 30 days, cannotbe cancelled.

Policy can be cancelled as a result of fulfillment (i.e. total loss of the subject-matter), breach

of a policy condition (i.e. become a voidable contract).

In case of fraudulent claim, the Insurer is not liable to pay the claim / can recover amounts

already paid / can also choose to terminate the contract from the date of the fraudulent act /

does not have to return any premiums.

Finance Department

24

25. Thank you

Finance Department25