Бизнес

БизнесПохожие презентации:

Accelerating Growth For Mobile Money Payments in Africa

1.

Accelerating GrowthFor Mobile Money

Payments in Africa

Trusted by:

Investor Deck Draft Q4 2025

2.

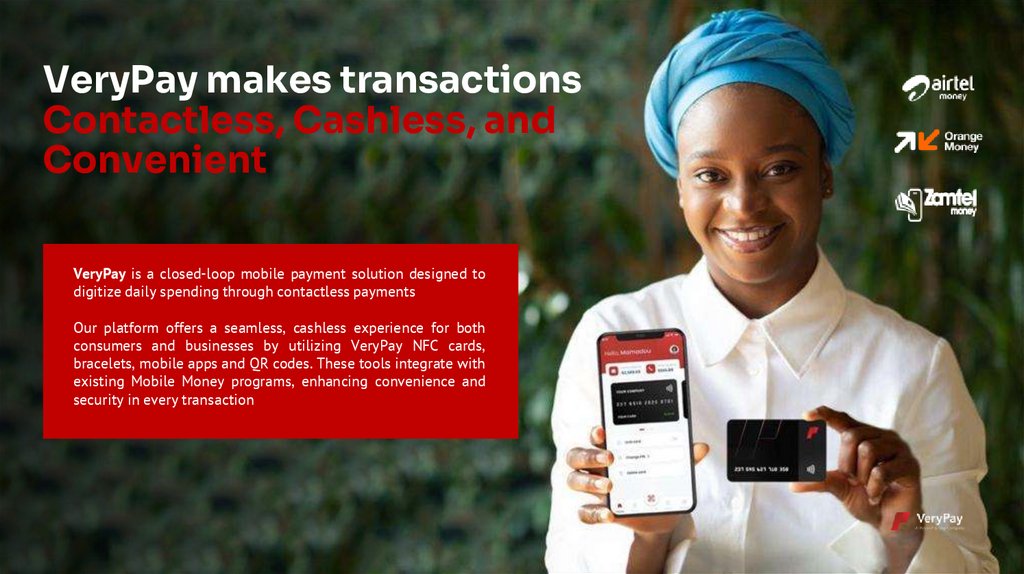

VeryPay makes transactionsContactless, Cashless, and

Convenient

VeryPay is a closed-loop mobile payment solution designed to

digitize daily spending through contactless payments

Our platform offers a seamless, cashless experience for both

consumers and businesses by utilizing VeryPay NFC cards,

bracelets, mobile apps and QR codes. These tools integrate with

existing Mobile Money programs, enhancing convenience and

security in every transaction

www.verypay.ch

@copyright VERYPAY 2024

2

3.

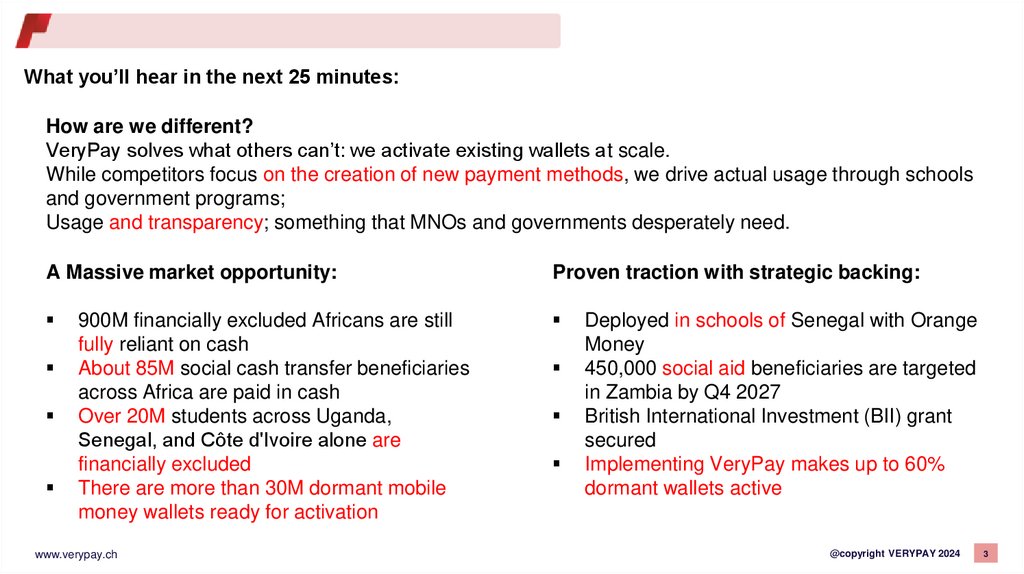

What you’ll hear in the next 25 minutes:How are we different?

VeryPay solves what others can’t: we activate existing wallets at scale.

While competitors focus on the creation of new payment methods, we drive actual usage through schools

and government programs;

Usage and transparency; something that MNOs and governments desperately need.

A Massive market opportunity:

Proven traction with strategic backing:

900M financially excluded Africans are still

fully reliant on cash

About 85M social cash transfer beneficiaries

across Africa are paid in cash

Over 20M students across Uganda,

Senegal, and Côte d'Ivoire alone are

financially excluded

There are more than 30M dormant mobile

money wallets ready for activation

www.verypay.ch

Deployed in schools of Senegal with Orange

Money

450,000 social aid beneficiaries are targeted

in Zambia by Q4 2027

British International Investment (BII) grant

secured

Implementing VeryPay makes up to 60%

dormant wallets active

@copyright VERYPAY 2024

3

4.

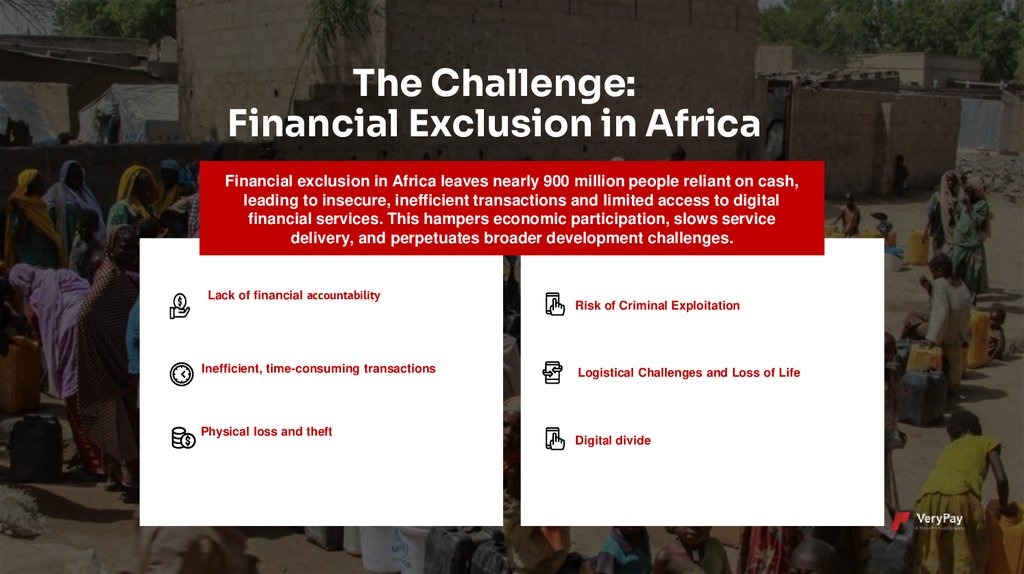

The Challenge:Financial Exclusion in Africa

Financial exclusion in Africa leaves nearly 900 million people reliant on cash,

leading to insecure, inefficient transactions and limited access to digital

financial services. This hampers economic participation, slows service

delivery, and perpetuates broader development challenges.

Lack of financial accountability

Inefficient, time-consuming transactions

Physical loss and theft

Risk of Criminal Exploitation

Logistical Challenges and Loss of Life

Digital divide

5.

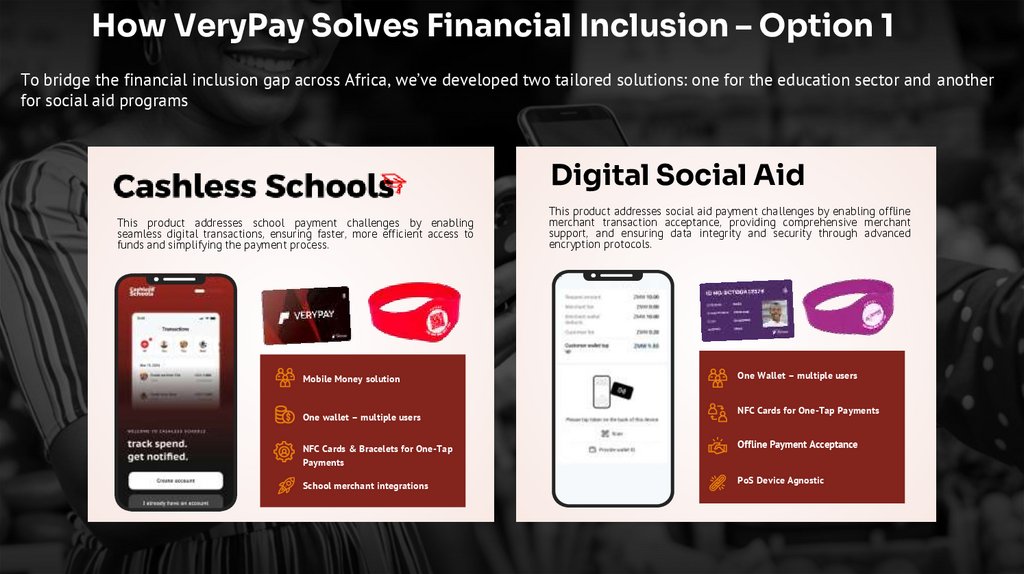

How VeryPay Solves Financial Inclusion – Option 1To bridge the financial inclusion gap across Africa, we’ve developed two tailored solutions: one for the education sector and another

for social aid programs

Digital Social Aid

This product addresses school payment challenges by enabling

seamless digital transactions, ensuring faster, more efficient access to

funds and simplifying the payment process.

Mobile Money solution

One wallet – multiple users

NFC Cards & Bracelets for One-Tap

Payments

School merchant integrations

This product addresses social aid payment challenges by enabling offline

merchant transaction acceptance, providing comprehensive merchant

support, and ensuring data integrity and security through advanced

encryption protocols.

One Wallet – multiple users

NFC Cards for One-Tap Payments

Offline Payment Acceptance

PoS Device Agnostic

6.

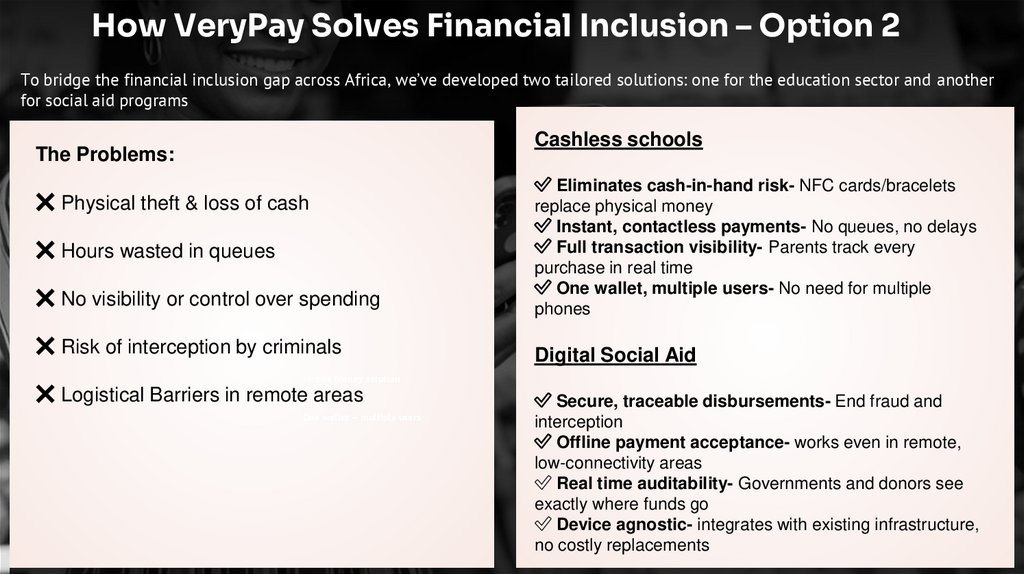

How VeryPay Solves Financial Inclusion – Option 2To bridge the financial inclusion gap across Africa, we’ve developed two tailored solutions: one for the education sector and another

for social aid programs

Cashless schools

The Problems:

❌ No visibility or control over spending

✅ Eliminates cash-in-hand risk- NFC cards/bracelets

replace physical money

✅ Instant, contactless payments- No queues, no delays

✅ Full transaction visibility- Parents track every

purchase in real time

✅ One wallet, multiple users- No need for multiple

phones

❌ Risk of interception by criminals

Digital Social Aid

❌ Physical theft & loss of cash

❌ Hours wasted in queues

Mobile Money solution

❌ Logistical Barriers in remote areas

One wallet – multiple users

✅ Secure, traceable disbursements- End fraud and

interception

✅ Offline payment acceptance- works even in remote,

low-connectivity areas

✅ Real time auditability- Governments and donors see

exactly where funds go

✅ Device agnostic- integrates with existing infrastructure,

no costly replacements

7.

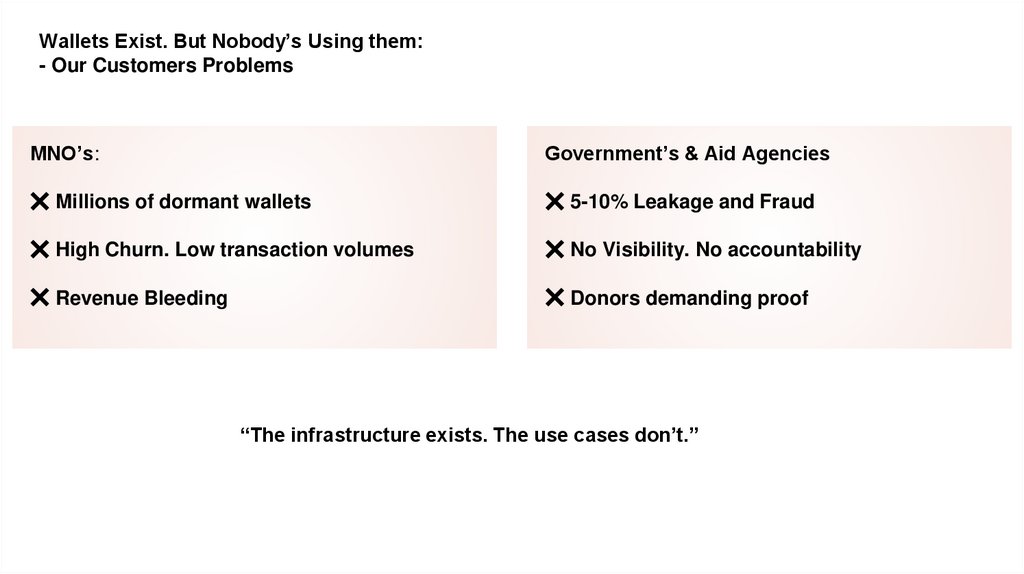

Wallets Exist. But Nobody’s Using them:- Our Customers Problems

MNO’s:

Government’s & Aid Agencies

❌ Millions of dormant wallets

❌ 5-10% Leakage and Fraud

❌ High Churn. Low transaction volumes

❌ No Visibility. No accountability

❌ Revenue Bleeding

❌ Donors demanding proof

“The infrastructure exists. The use cases don’t.”

8.

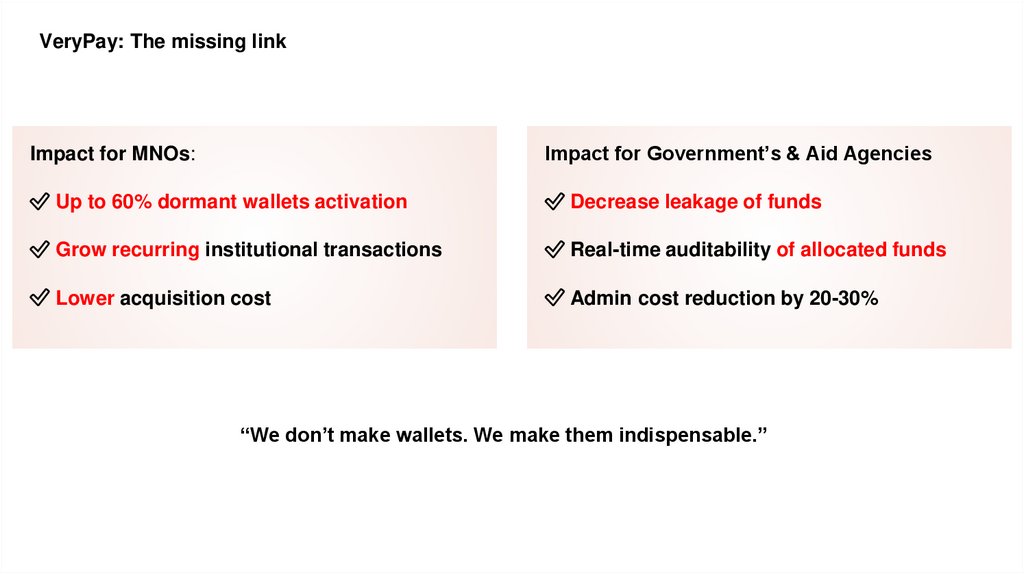

VeryPay: The missing linkImpact for MNOs:

Impact for Government’s & Aid Agencies

✅ Up to 60% dormant wallets activation

✅ Decrease leakage of funds

✅ Grow recurring institutional transactions

✅ Real-time auditability of allocated funds

✅ Lower acquisition cost

✅ Admin cost reduction by 20-30%

“We don’t make wallets. We make them indispensable.”

9.

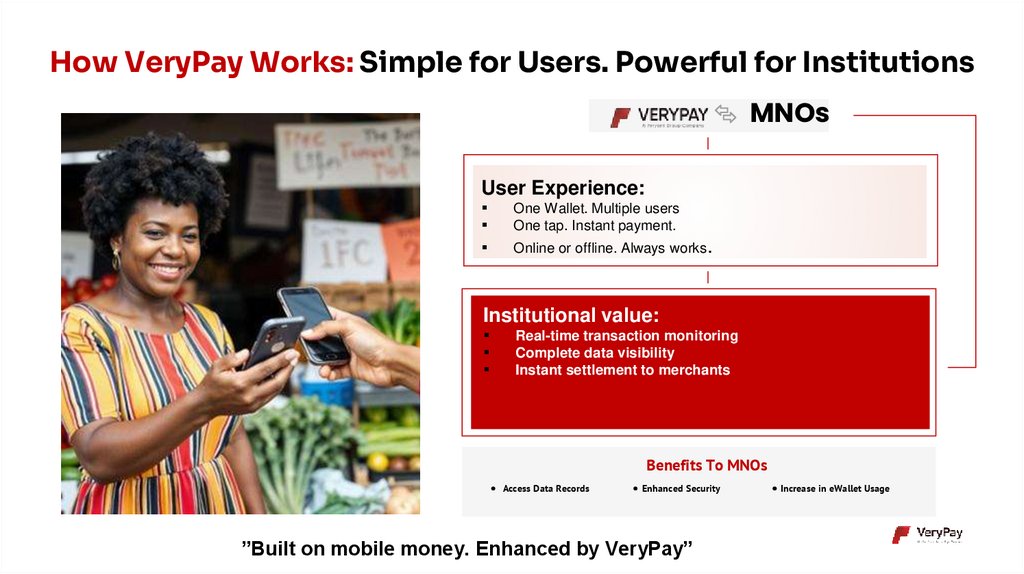

How VeryPay Works: Simple for Users. Powerful for InstitutionsMNOs

User Experience:

One Wallet. Multiple users

One tap. Instant payment.

Online or offline. Always works.

Institutional value:

Real-time transaction monitoring

Complete data visibility

Instant settlement to merchants

Benefits To MNOs

Access Data Records

Enhanced Security

”Built on mobile money. Enhanced by VeryPay”

Increase in eWallet Usage

10.

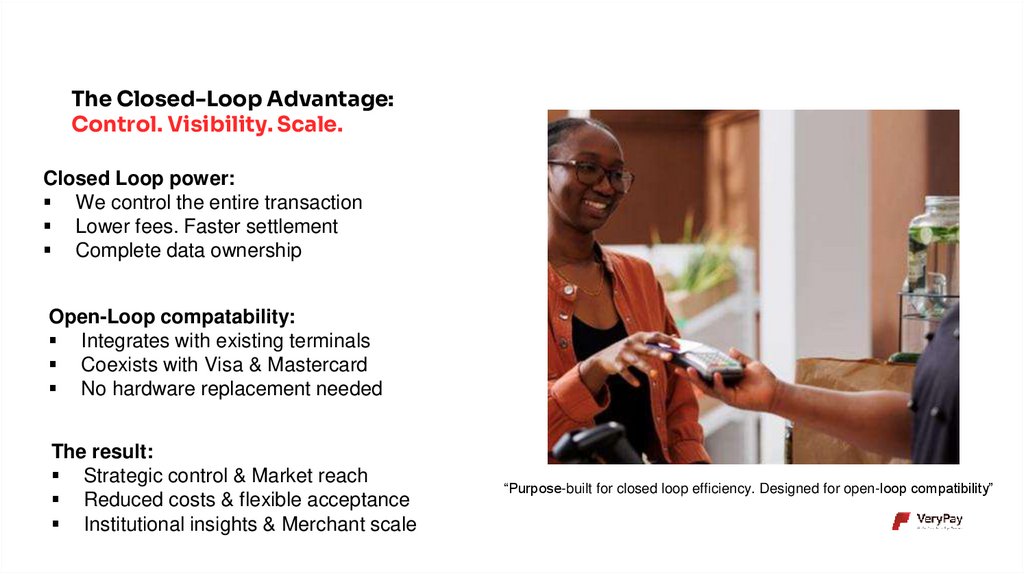

The Closed-Loop Advantage:Control. Visibility. Scale.

Closed Loop power:

We control the entire transaction

Lower fees. Faster settlement

Complete data ownership

Open-Loop compatability:

Integrates with existing terminals

Coexists with Visa & Mastercard

No hardware replacement needed

The result:

Strategic control & Market reach

Reduced costs & flexible acceptance

Institutional insights & Merchant scale

“Purpose-built for closed loop efficiency. Designed for open-loop compatibility”

11.

Case Study: Orange Money x VeryPay- Powering Financialinclusion in Senegal

The problem:

Orange money facing

declining market sharelosing ground to Wave

money in Senegal

Limited agent and

payment infrastructure,

especially for schools

and salary

disbursements

Needed rapid, scalable

user acquisition and

engagement solutions

Why they chose VeryPay:

Proven, flexible proposition

targeting unbanked segments

Seamless card & digital wallet

solution adaptable for education,

retail and payroll sectors

Faster go-to-market and lower

integration costs than competing

fintech's

Track record of innovation,

flexibility and ability to generate

new transaction volume

Impact:

Deployed in schools

with significant adoption

and transaction growth

Expansion approved for

universities, retail and

salary payments in 2026

Strengthened Orange

money’s competitive

position against Wave

Driving financial

inclusion for teachers,

students and salary

earners across Senegal

and beyond

12.

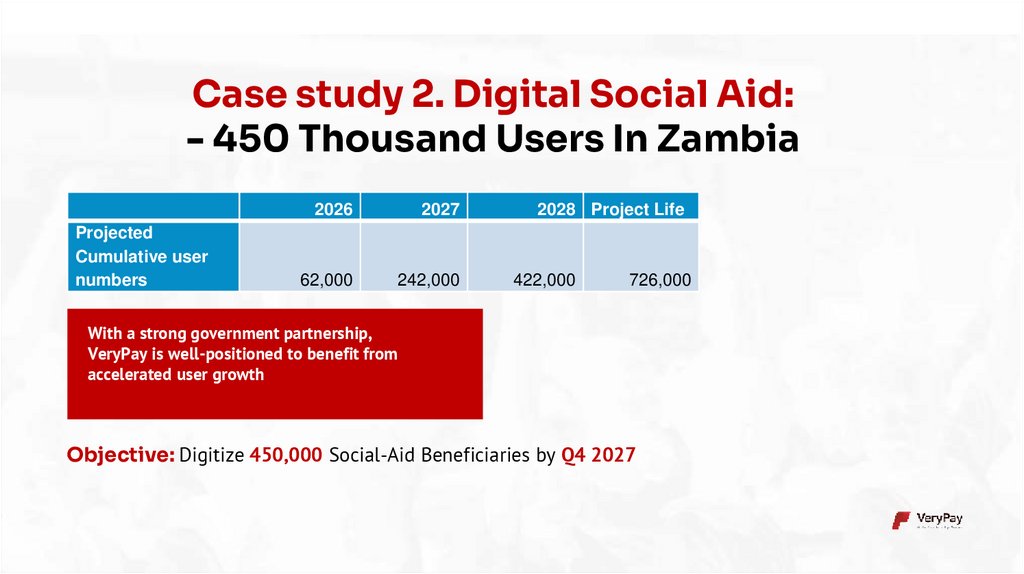

Case study 2. Digital Social Aid:- 450 Thousand Users In Zambia

Projected

Cumulative user

numbers

2026

2027

62,000

242,000

2028 Project Life

422,000

726,000

With a strong government partnership,

VeryPay is well-positioned to benefit from

accelerated user growth

Objective: Digitize 450,000 Social-Aid Beneficiaries by Q4 2027

13.

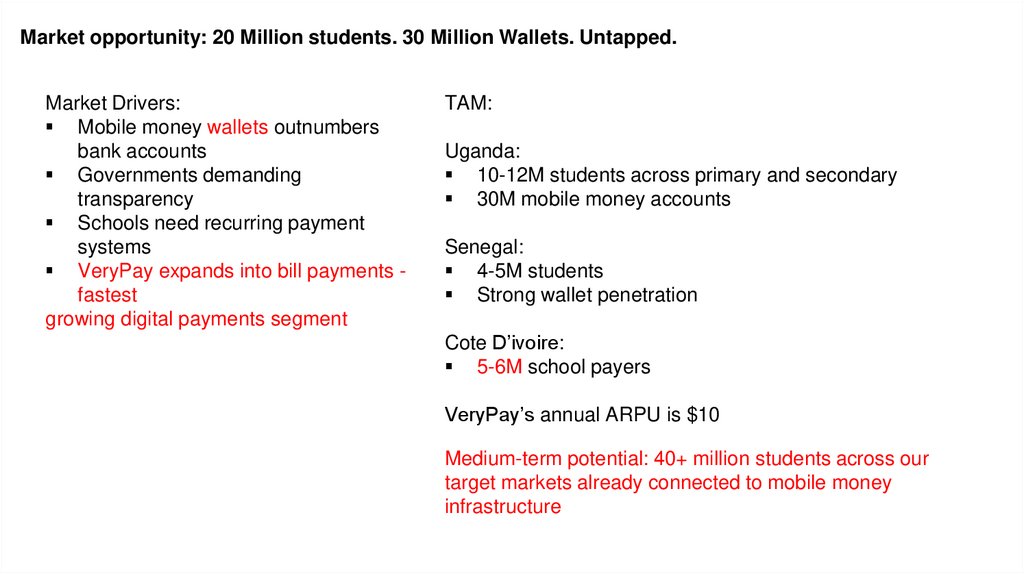

Market opportunity: 20 Million students. 30 Million Wallets. Untapped.Market Drivers:

Mobile money wallets outnumbers

bank accounts

Governments demanding

transparency

Schools need recurring payment

systems

VeryPay expands into bill payments fastest

growing digital payments segment

TAM:

Uganda:

10-12M students across primary and secondary

30M mobile money accounts

Senegal:

4-5M students

Strong wallet penetration

Cote D’ivoire:

5-6M school payers

VeryPay’s annual ARPU is $10

Medium-term potential: 40+ million students across our

target markets already connected to mobile money

infrastructure

14.

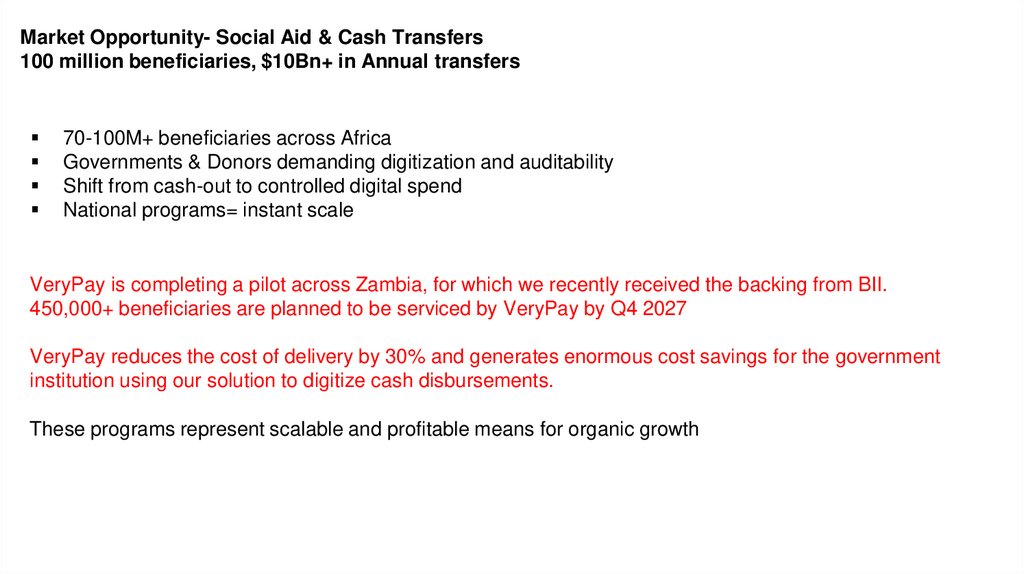

Market Opportunity- Social Aid & Cash Transfers100 million beneficiaries, $10Bn+ in Annual transfers

70-100M+ beneficiaries across Africa

Governments & Donors demanding digitization and auditability

Shift from cash-out to controlled digital spend

National programs= instant scale

VeryPay is completing a pilot across Zambia, for which we recently received the backing from BII.

450,000+ beneficiaries are planned to be serviced by VeryPay by Q4 2027

VeryPay reduces the cost of delivery by 30% and generates enormous cost savings for the government

institution using our solution to digitize cash disbursements.

These programs represent scalable and profitable means for organic growth

15.

Projected Growth Across MarketsOver the next 3 - 5 years, VeryPay is poised for strategic and accelerated growth across key markets.

Add financial impact (revenue approx.)

Côte d'Ivoire

Nigeria

50,000

50,000

Students Transacting

Students Transacting

125

125

Merchants onboarded

100

Schools

Merchants onboarded

50

Schools

Senegal

90,000

Students transacting

190

Merchants onboarded

150

Schools

Uganda

Zambia

310,000

450,000

Students transacting

1,125

Merchants onboarded

376

Schools

Digitised Beneficiaries

1000+

Merchants / Agents

Onboarded

16.

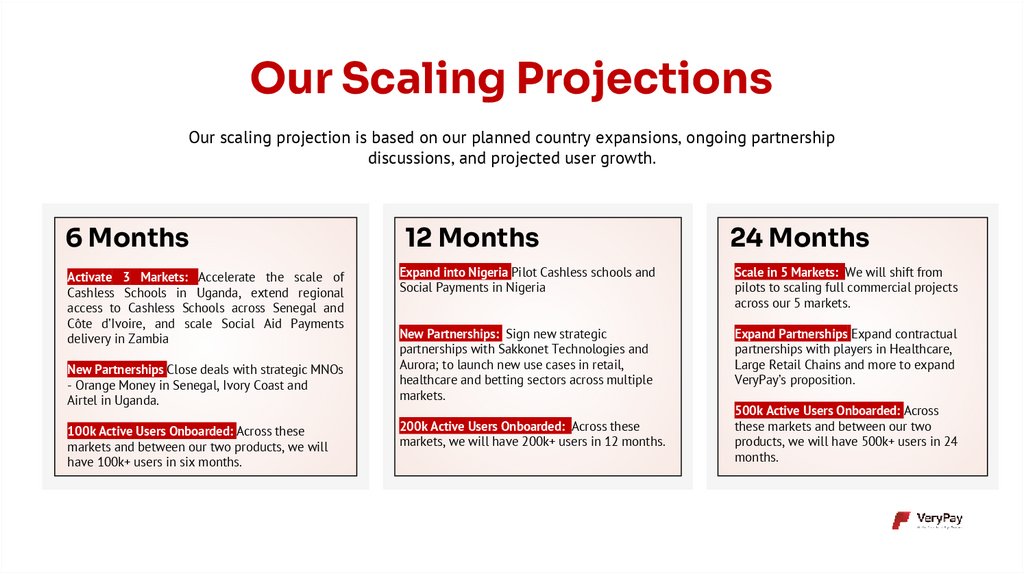

Our Scaling ProjectionsOur scaling projection is based on our planned country expansions, ongoing partnership

discussions, and projected user growth.

6 Months

12 Months

24 Months

Activate 3 Markets: Accelerate the scale of

Cashless Schools in Uganda, extend regional

access to Cashless Schools across Senegal and

Côte d’Ivoire, and scale Social Aid Payments

delivery in Zambia

Expand into Nigeria Pilot Cashless schools and

Social Payments in Nigeria

Scale in 5 Markets: We will shift from

pilots to scaling full commercial projects

across our 5 markets.

New Partnerships: Sign new strategic

partnerships with Sakkonet Technologies and

Aurora; to launch new use cases in retail,

healthcare and betting sectors across multiple

markets.

Expand Partnerships Expand contractual

partnerships with players in Healthcare,

Large Retail Chains and more to expand

VeryPay’s proposition.

New Partnerships Close deals with strategic MNOs

- Orange Money in Senegal, Ivory Coast and

Airtel in Uganda.

100k Active Users Onboarded: Across these

markets and between our two products, we will

have 100k+ users in six months.

200k Active Users Onboarded: Across these

markets, we will have 200k+ users in 12 months.

500k Active Users Onboarded: Across

these markets and between our two

products, we will have 500k+ users in 24

months.

17.

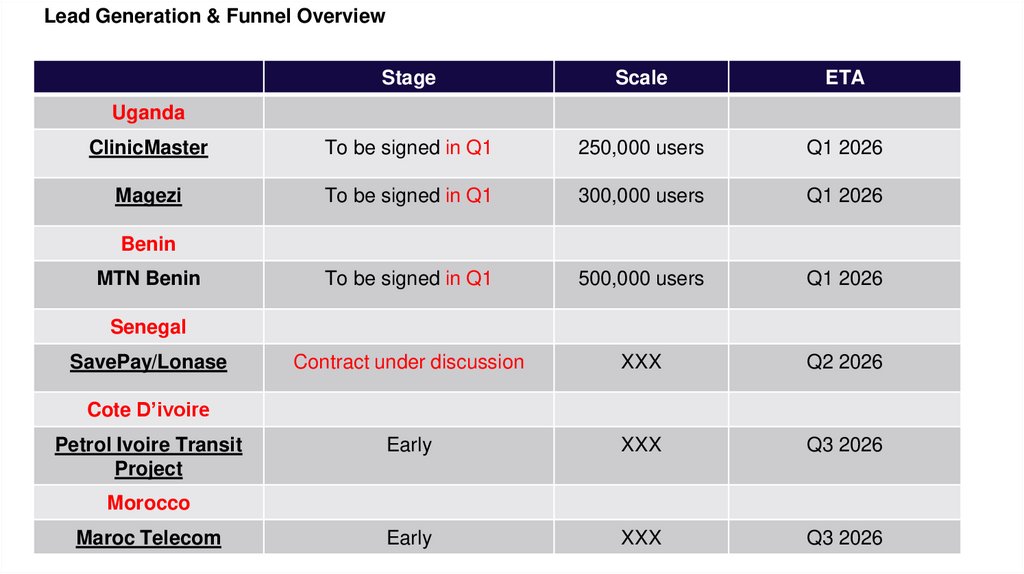

Lead Generation & Funnel OverviewStage

Scale

ETA

ClinicMaster

To be signed in Q1

250,000 users

Q1 2026

Magezi

To be signed in Q1

300,000 users

Q1 2026

To be signed in Q1

500,000 users

Q1 2026

Contract under discussion

XXX

Q2 2026

Early

XXX

Q3 2026

Early

XXX

Q3 2026

Uganda

Benin

MTN Benin

Senegal

SavePay/Lonase

Cote D’ivoire

Petrol Ivoire Transit

Project

Morocco

Maroc Telecom

18.

The VeryPay Leadership TeamAndrey Tikhonov

Joseph Yendork

CEO, VeryPay

Sales Director Africa

Business Development Director,

Francophone Africa

Director of International Partnerships

Adim Isiakpona

Maria Koshkina

Chuong Huynh

Mukupa J. Katema

Head of Marketing

Technical Product Manager.

Head of Product

Country Lead, Zambia

Marietou Sylla

David Drever

19.

VeryPay Board of DirectorsPhilippe Vogeleer

MIKHAIL KRASNOV

PETR KRASNOV

Chairman of the Board of Directors, NED

Co-founder and VERYPAY Board Member

Co-founder and VERYPAY Board Member

Philippe was head of Global Head of

Business

Development

for

the

Vodafone

Group.

He

delivered

investment partnerships with Large

corporations

and

international

organizations such as The World Bank

Group.

Mikhail is an accomplished leader

with a proven track record of almost

35 years in the IT industry. Mikhail

Krasnov is a PhD in economics and

co-founder of Verysell Group.

Petr Krasnov, a Cornell University

graduate and co-founder of Verysell

Group, brings 14 years of legal and

financial experience. He has been on

both sides of multiple M&A deals.

20.

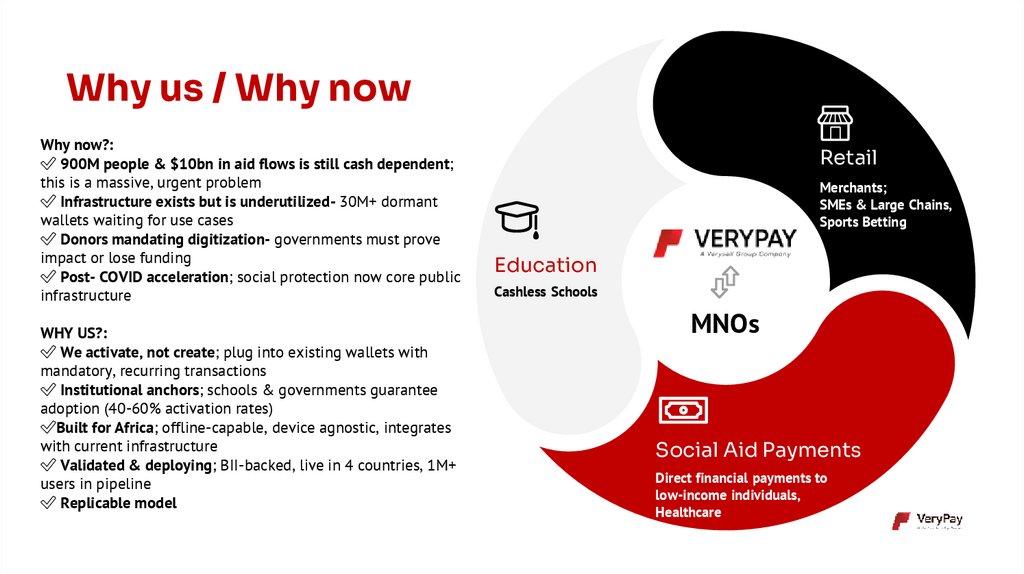

Why us / Why nowWhy now?:

✅ 900M people & $10bn in aid flows is still cash dependent;

this is a massive, urgent problem

✅ Infrastructure exists but is underutilized- 30M+ dormant

wallets waiting for use cases

✅ Donors mandating digitization- governments must prove

impact or lose funding

✅ Post- COVID acceleration; social protection now core public

infrastructure

WHY US?:

✅ We activate, not create; plug into existing wallets with

mandatory, recurring transactions

✅ Institutional anchors; schools & governments guarantee

adoption (40-60% activation rates)

✅Built for Africa; offline-capable, device agnostic, integrates

with current infrastructure

✅ Validated & deploying; BII-backed, live in 4 countries, 1M+

users in pipeline

✅ Replicable model

Retail

Merchants;

SMEs & Large Chains,

Sports Betting

Education

Cashless Schools

MNOs

Social Aid Payments

Direct financial payments to

low-income individuals,

Healthcare

21.

Other Asks: Beyond FundingTo effectively deploy and scale the use of VeryPay solutions across Africa,

we request help and participation from investors in the following areas:

Regulatory Enablement

Navigating complex legal

and regulatory environments

across target geographies.

Stakeholder Engagement

Facilitating local government

engagement with ministries

and aid agencies.

Telecom Partnerships

Facilitating local

engagement with Mobile

Network Operators

Programme Evaluation

Structuring impact assessment

metrics for disbursement

programmes.

Impact Evaluation

Monitoring and evaluation

frameworks to assess

programme impact.

Opportunity Mapping

Identifying additional

programmes across countries

where VeryPay can add value.

22.

DISCLAIMER AND CAUTIONARY STATEMENTMay, 2025

Certain statements in this document are forward-looking statements, including, but not limited to, statements that are predictions of

or indicate future events, trends, plans, or objectives of Verysell Technologies S.A., its subsidiaries or affiliates (collectively referred to

herein as the "Group"). Forward-looking statements include statements regarding the Group’s targeted profit, return on equity targets,

expenses, pricing conditions, and statements regarding the Group’s understanding of general economic, financial, and market

conditions and expected developments. Undue reliance should not be placed on such statements because, by their nature, they are

subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results and plans

and objectives of the Group to differ materially from those expressed or implied in the forward-looking statements (or from past

results). Factors such as (i) general economic conditions and competitive factors, particularly in key markets; (ii) the risk of a global

economic downturn, in the financial services industries in particular; (iii) performance of financial markets; (iv) levels of interest rates

and currency exchange rates; (v) changes in laws and regulations may have a direct bearing on the results of operations the Group and

on whether the targets will be achieved. The Group undertakes no obligation to update or revise any of these forward-looking

statements, whether to reflect new information, future events, circumstances, or otherwise. It should be noted that past performance

is not a guide to future performance. Please also note that interim results do not necessarily indicate full-year results. Persons

requiring advice should consult an independent adviser.

This communication does not constitute an offer or invitation to sell or purchase securities in any jurisdiction.