Финансы

ФинансыПохожие презентации:

Russian Standard Bank

Restructuring Considerations DISCLAIMER NOT FOR RELEASE OR DISTRIBUTION OR PUBLICATION IN WHOLE OR IN PART IN OR INTO ANY JURISDICTION WHERE TO DO SO MIGHT CONSTITUTE A VIOLATION OF LOCAL SECURITIES LAWS OR REGULATIONS.

The Materials are provided subject to (i) the terms of this Disclaimer, and (ii) the 'Important Securities Law Notice' on pages (iii)– (vi) of the Scheme Document which appears on the scheme website (http://sites.dfkingltd.com/rsb).

If there is any inconsistency between this Disclaimer and the s aid Notice, the said Notice shall prevail to the extent of that inconsistency.

The information contained herein (the “Materials”) have been prepared by Russian Standard Bank (the “Company”) and its subsidiaries (the “Group”) solely for use at this presentation.

By accepting the Materials or attending this presentation, you are agreeing to maintain absolute confidentiality regarding the inf ormation disclosed in the Materials and further agree to the following limitations and notifications.

The Materials have been provided to you solely for your information and background and are subject to amendment.

The Materials (or any part of them) may not be reproduced or redistributed, passed on, or the contents otherwise divulged, directly or indirectly, to any oth er person or published in whole or in part for any purpose without the prior written consent of the Company.

Failure to comply with this restriction may constitute a violation of applica ble securities laws.

The Materials are not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, c ountry or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jur isdiction.

The Materials do not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the secu rities referred to herein in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration, exemption from registration or qualification under the securities laws of any jurisdiction.

The Materials are not for public release, publication or distribution, directly or indirectly, in or into the United States (in cluding its territories and possessions, any State of the United States and the District of Columbia).

This communication is not and does not constitute or form a part of any offer of, or solicitation to purchase or subscribe for, any securities in the United States.

Any such securities have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “Securities Act”).

Any such securities may not be offered or sold in the United States or to, or for the account or benefit of, U.S.

persons (as such term is defined in Regulation S under the Securities Act), excep t pursuant to an exemption from the registration requirements of the Securities Act.

No public offering of securities will be made in the United States of America.

The Materials are addressed only to and directed only at (i) persons who are outside the United Kingdom or (ii) investment prof essionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”) and (iii) high net worth entities, a nd other persons to whom it may lawfully be communicated, falling within Article 49(2) of the Order (all such persons together being referred to as “relevant persons”).

Any investment activity to which this communication relates will only be available to and will only be engaged with, relevant persons.

Any person who is not a relevant person should not act or rely on this docu ment or any of its contents.

In any EEA member state that has implemented EU Directive 2003/71/EC, as amended (together with any applicable implementing meas ures in any Member State, the “Prospectus Directive”), these Materials are addressed only to and directed solely at “qualified investors” (as defined in Prospectus Dir ective) in that Member State.

The Materials are an advertisement and not a prospectus for the purposes of applicable measures implementing the Prospectus Directive and as such do not constitut e an offer to sell or the solicitation of an offer to purchase securities.

The Materials are not an offer, or an invitation to make offers, to sell, exchange or otherwise transfer securities in the Russ ian Federation to or for the benefit of any Russian person or entity and does not constitute an advertisement or offering of securities in the Russian Federation within the meaning of Russi an securities laws.

Information contained in herein is not intended for any persons in the Russian Federation who are not “qualified investors” within the meaning of Article 51.2 of th e Federal Law No.

39- FZ “On the Securities Market” dated 22 April 1996, as amended (the “Russian QIs”) and must not be distributed or circulated into the Russian Federation or made avai lable in the Russian Federation to any persons who are not Russian QIs, unless and to the extent they are otherwise permitted to access such information under Russian law.

Under Russian law, the New Notes are securities of a foreign issuer.

The New Notes are not eligible for initial offering in the Russian Federation.

Neither the issue of the New Notes nor the Mater ials have been or will be registered or approved in the Russian Federation and is intended for “placement” or “circulation” in the Russian Federation (each as defined in Russian sec urities laws) unless and to the extent otherwise permitted under Russian law.

The information contained in the Materials does not purport to be comprehensive and has not been independently verified.

The in formation contained in the Materials is subject to updating, completion, revision, verification and amendment and such information may change materially.

The Company is under no obligation to update or keep current the information contained in the Materials or in the presentation to which it relates and any opinions expressed in them are subject to change without notice.

No representation or warranty, expressed or implied, is made by the Company and any of its affiliates as to the fairness, accuracy, reasonableness or completeness of the i nformation contained herein and no reliance should be placed on it.

Neither the Company nor any other person accepts any liability for any loss howsoever arising, directly or indire ctly, from reliance on the Materials.

The Company and its affiliates, advisors and representatives shall have no liability whatsoever (in negligence or otherwise) for any loss whatsoeve r arising from any use of the Materials.

The Materials largely comprise a summary of information contained in the scheme documentation which has already been made avail able to bondholders.

Reading the Materials is not a substitute for reading the scheme documentation in its entirety and bondholders should ensure that they read the scheme documen tation rather than simply rely upon the Materials.

Russian Standard Finance S.A has not independently verified or diligenced this presentation or any of the information included in this presentation.

Executive summary Russian Standard Bank (“RSB”) was founded in 1999 as a financial innovator effectively creating the Russian market for consumer lending and credit cards Today RSB is one of the largest full-service banks in Russia that has attracted 30 million clients, offering a unique product p roposition and a broad multi-channel distribution network covering the country– the Bank remains a leader in its core consumer finance segments, with core focus on credit cards issuance Being a leader of financial innovation allowed RSB to generate healthy profits while during economic downturns, RSB has been ab le to successfully optimise its business model and return to profitability within a short period of time Many investors have been working with RSB for over 10 years and have always had good returns on investments The current macroeconomic and geopolitical situation in Russia has affected the banking industry and particularly the retail se gment, which has resulted in a sharp increase in provision requirements and cost of funding, reduction in the proportion of “good” borrowers to extend the new loans to, leading to a negative impact on financial results of Russian banks– One of the strongest effects of the Russian economy downturn has been felt in the credit cards industry– Credit cards business is inherently highly profitable yet highly cyclical: in the growth environment this allows banks to record significant profits, but during the downturns credit card companies start recording losses, which puts their capital adequacy a t risk– this is a universal rule for credit card companies globally Being one of the leaders in the Russian credit cards market, RSB has found itself in the current recession temporarily facing s ignificant losses, which has led to a need for additional Tier 1 capital in order to comply with regulatory capital adequacy requirements.

Additional Tier 1 capital will allow RSB to withstand pressures of the current crisis, and recover and revert to profitability at the end of 2016 Prior to that, however, RSB is expected to continue recording elevated losses, as driven by protracted amortization of the “old” loan portfolio that can take up to 12 months;

gradual recovery of new loan sales over the next 12-15 months, which currently stand near historic minimum ;

temporary increase in operating expenditure during ongoing headcount optimisation and significant severance payments;

funding costs that are expected to remain elevated at least until the first half of 20162 Executive summary (cont’d)3 At the moment, in order to avoid a breach by RSB of its regulatory capital adequacy ratios which, in turn, would lead to a write-down in full of the subordinated notes due 2020 and 2024 (the "Notes"), RSB requires a restructuring of the Notes The restructuring will provide the holders of the Notes with an immediate partial repayment of the notes due 2020 and 2024 (being 10% of the outstanding principal together with aggregate Accrued Interest Amounts) and an exchange of the remainder (90%) for new notes issued by an SPV and secured by 49% of the shares in RSB.

The resulting profit obtained by RSB will improve RSB’s capital position, enabling it to comply with its regulatory capital adequacy ratios and avoid the significant negative consequences ofany breach for all stakeholders The restructuring of the Notes also forms part of RSB's wider recapitalisation plan.

Should the restructuring be successful, fu rther financial support from the shareholder and the government would remain open to RSB, which would assist with its return to profitability by the end of 2016– If RSB is in compliance with all applicable regulatory requirements, RSB would remain eligible for state financial support of RUB 5bn and, subject to Russian Government resolution and CBR approval, an extension of RUB 5bn of existing subordinated loans from VEB– The Shareholder has already invested approximately RUB 14bn in RSB's Tier 1 capital (without such injections RSB's N1.1 ratio would have fallen to 2.5% already) and will be considering additional investment to further improve RSB's capital adequacy ratios The proposed bond exchange is a fair and effective solution:– It allows RSB to comply with regulatory requirements avoiding a Write Down Event and writedown for the 20s and 24s– Whilst not giving bondholders direct legal recourse to RSB or its assets, it nevertheless positions bondholders to recover their investment once RSB returns to profitability or pays any form of dividend Executive summary (cont’d)4 We have developed a new business model that would make RSB profitable again by the end of 2016 provided that there will be no further substantial negative macroeconomic and geopolitical disruptions The key pillars of the new model are based on innovations that have been already successfully implemented in many markets by our global partners and strategic consultants– Offering simple low risk products to “good” clients with healthy credit ratings– Maintaining attractive yields across the loan portfolio: prudent pricing across the credit quality spectrum– Lower cost of funding and hedging costs following general market trends– Reduction of operating expenses and continued cost cutting initiatives : create an effective and profitable distribution network with extensive use of remote channels– Intellectual Data Analysis as a competitive advantage : new scoring models using a wide range of data sources, risk management and collection improvement– Non-credit business development : participation in commercial margin of merchants using innovative loyalty platforms and our current wide acquiring network;

increasing non-interest income through transaction commissions, banking insurance, online and mobile services We have already implemented a number of business optimisation initiatives that are bringing significant results– Introduced new products, including instalment credit cards for the mass segment– Improved credit policies and scoring models, which has already resulted in a significant reduction of risks on new sales– Focused resources on collection and improved procedures and policies– Reduced its expenses base and exited low-return, non-core projects We are confident that the new business model will bring RSB back to profitability by the end of 2016 while the proposed exchange offer will allow RSB to comply successfully with its regulatory capital ratios, avoid a Write Down Event and eventually ensure bondholders recover their investment We ask bondholders to support this win-win solution and vote in favour of the exchange offer RSB has a track record of providing high and reliable returns to international bondholders Historic placements and successful repayments by RSB Issue date Instrument type Ranking Principal amount Coupon rate, p.a.

Maturity date Status Sep-2003 Credit-linked notes Senior unsecured US$30mm 10% Mar-2004 Fully repaid on schedule Nov-2003 Loan participation notes Senior unsecured US$30mm 11% May-2005 Fully repaid on schedule Apr-2004 (incr.

Nov-2014) Loan participation notes Senior unsecured US$150mm + US$150mm 8.75% Apr-2007 Fully repaid on schedule Sep-2004 Loan participation notes Senior unsecured US$300mm 7.8% Sep-2007 Fully repaid on schedule Apr-2005 Loan participation notes Senior unsecured US$300mm 8.125% Apr-2008 Fully repaid on schedule Sep-2005 Loan participation notes Senior unsecured US$500mm 7.5% Oct-2010 Fully repaid on schedule Dec-2005 Loan participation notes Subordinated Lower-Tier 2 US$200mm 8.875%, re-set to 7.73% in 2010 Dec-2015, call option in Dec-2010 US$147mm publicly outstanding– prompt coupon payments to date, buybacks and a tender in 2015 Jan-2006 Loan participation notes Senior unsecured US$200mm 6.72% Feb-2007 Fully repaid on schedule Apr-2006 Loan participation notes Senior unsecured US$350mm 8.625% May-2011 Fully repaid on schedule Sep-2006 Loan participation notes Senior secured EUR400mm 6.825% Sep-2009 Fully repaid on schedule Nov-2006 Loan participation notes Subordinated Lower-Tier 2 US$200mm 9.75%, re-set to 7.561% in 2011 Dec-2016, call option in Dec-2011 US$169mm publicly outstanding– prompt coupon payments to date, buybacks and a tender in 2015 Apr-2007 Eurocommercial paper (ECP) Senior unsecured US$215mm Zero, implied yield 8.1% at issue Apr-2008 Fully repaid on schedule Jun-2007 Loan participation notes Senior unsecured US$400mm 8.485% Jun-2010 Fully repaid on schedule Oct-2010 Eurocommercial paper (ECP) Senior unsecured US$100mm Zero, implied yield 9.1% at issue Oct-2011 Fully repaid on schedule Nov-2011 Eurocommercial paper (ECP) Senior unsecured US$150mm Zero, implied yield 8.5% at issue May-2012 Fully repaid on schedule Apr-2012 Eurocommercial paper (ECP) Senior unsecured US$150mm Zero, implied yield 5.5% at issue Apr-2013 Fully repaid on schedule Jul-2012 (incr.

Nov-2012) Loan participation notes Senior unsecured US$350mm + US$175mm 9.25% Jul-2017, put option in Jul-2015 US$38mm outstanding– prompt coupon payments to date, buybacks and a tender in 2014- 2015, US$284mm put in 2015 Feb-2013 (incr.

Mar-2013) Loan participation notes Senior unsecured CNY500mm + CNY750mm 8% Feb-2015 Fully repaid on schedule Note: The list excludes the most recently issued RSB due 2020 (originally due 2018) and due 2024 bonds to be targeted via propo sed restructuring5 Total principal amount of Eurobonds issued by RSB to date: US$4.6bn equivalent Total number of Eurobond placements completed by RSB to date: 18 (incl.

taps) RSB vs.

peers in Eurobond marketsRSB US$4.6bn raised via 18 placements Alfa-Bank US$6.7bn raised via 16 placements Prom- svyazbank (PSB) US$3.6bn raised via 19 placements Nomos (Bank Otkritie) US$2.7bn raised via 9 placements Renais- sance Credit US$1.2bn raised via 10 placements Credit Bank of Moscow US$1.2bn raised via 3 placements Tinkoff Bank US$0.7bn raised via 5 placements Bank St.

Pet’burg (BSPB) US$0.5bn raised via 5 placements Note: Based on Bloomberg & RSB Downturn in Russian economy has negatively affected profitability of banks The slowdown from 2011 to 2014 was largely a result of a drop in oil and gas exports, less investment in the Russian economy, increased capital outflows and a decrease in the Russian Government’s international reserves A combination of US/EU sanctions, Russia’s countersanctions, terms of trade shock and significant tightening of monetary policy have resulted in sharp economic contraction and downward revision of near- term GDP growth forecasts Recent decrease in oil price has been one of the main factors for currency weakness, which has pushed up inflation levels Profitability of Russian banks has been negatively impacted by the spike in CBR rate in Dec-14 Real GDP growth (actual)6 Russian macroeconomic forecasts Oil price and US$/RUB evolution Source: Bloomberg as of 28 September 2015, Central Bank of Russia ¹ Y-o-Y growth as of Jul-15 6.6% 6.5% 11.4% 14.5%¹ Inflation 32.9 65.7 100.4 47.52040608010012020304050607080 Jan-14Jun-14Dec-14 Jun-15 US$/RUB Brent price (US$/bbl) 3.4% 1.3% 0.6% (2.8%)-5%-3%-1%1%3%5% 201220132014 2015E Without the restructuring, RSB will breach Russian capital requirement regulation in Q4 20157 Escalating loan loss provisions and a decline in net interest income due to a deterioration in asset quality are expected to le ad to significant losses over the following months Given RSB’s current capital levels and expected short term profitability the Bank will breach regulatory capital requirements in Q4’15 RSB’s capital position with no restructuring in place RUBmm, under RAS¹ Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Q3’16 Q4’16 Profit for the period 340 1,207 (110) 205 (3,500) (3,689) (7,456) (3,113) (2,958) (2,969) (2,777) (2,502) (21,760) (4,948) (3,625) Base Capital 23,834 24,998 24,868 25,245 21,622 17,805 11,427 8,491 5,360 2,217 7,652 7,655 7,332 4,835 1,006 Additional Capital (5,292) (5,287) (5,279) (5,276) (5,274) (5,271) (4,430) (2,952) (2,950) (2,949) (2,947) (2,945) (2,944) (2,939) (2,933) Main Capital 23,834 24,998 24,868 25,245 21,622 17,805 11,427 8,491 5,360 2,217 7,652 7,655 7,332 4,835 1,006 Additional Capital 38,252 39,205 43,491 41,929 40,232 40,232 39,258 38,121 38,121 37,323 29,866 27,866 8,089 4,711 3,914 Own funds 62,086 64,203 68,359 67,175 61,853 58,037 50,685 46,612 43,481 39,541 37,518 35,520 15,420 9,547 4,920 Risk Weighted Assets for N1.1 and N1.2 376,288 394,223 397,047 397,360 401,678 394,759 394,267 402,160 398,157 381,454 378,128 374,185 360,895 342,173 354,944 Risk Weighted Assets for N1.0 377,032 394,889 397,674 397,995 402,314 395,396 394,904 402,646 398,642 381,939 378,613 374,671 361,380 342,658 355,430 N.1.1 (5%) 6.3% 6.3% 6.3% 6.4% 5.4% 4.5% 2.9% 2.1% 1.3% 0.6% 2.0% 2.0% 2.0% 1.4% 0.3% N.1.2 (6%) 6.3% 6.3% 6.3% 6.4% 5.4% 4.5% 2.9% 2.1% 1.3% 0.6% 2.0% 2.0% 2.0% 1.4% 0.3% N.1.0 (10%) 16.5% 16.3% 17.2% 16.9% 15.4% 14.7% 12.8% 11.6% 10.9% 10.4% 9.9% 9.5% 4.3% 2.8% 1.4% ¹All numbers presented in the presentation are under Russian Accounting Standards (“RAS”), unless otherwise noted Write down event following closing of RAS accounts for the end of February 2016 N.1.1 ratio is kept at 2% temporarily as the notes are being written down Full write down following closing of RAS accounts for August 2016 RESTRUCTURING PLAN Restructuring of the Bank’s liabilities will help the Bank to boost its N1.1 and N1.2 capital levels Proposed debt restructuring program Capital impact at the Bank level Total amount of bonds Transaction impact Capital contribution to N1.1 & N1.2 RUB22,750mm US$350mm 10% cash: RUB2,275mm 90% profit in income statement from write-off Value: RUB20,475mm US$315mm RUB13,000mm US$200mm 90% profit in income statement from write-off Value: RUB11,700mm US$180mm Total profit from restructuring recorded as part of capital: Value: RUB32,175mm US$495mm 10-04-2020 T2 bond (13.0%) 17-01-2024 T2 bond (11.5%)9 The Bank is proposing to restructure its US$350mm Notes due April 2020 and US$200mm Notes due January 2024 Without restructuring the Bank is expecting to breach N.1.2 capital adequacy ratio of the Central Bank by the end of October 20 15, which will eventually lead to occurrence of a write-down event for the Notes and loss of the full investment for the bondholders Current bondholders of both Notes are offered an upfront 10% cash payment, in addition to upfront cash repayment of all accrued and unpaid interest, and an exchange bond of US$495mm that is to be issued by a RHL subsidiary SPV– no haircut is proposed to bondholders Exchange bond security is to:– Pay a 13% coupon;

PIK until the Bank becomes profitable or pays any form of dividends, cash coupon thereafter– Have a 49% share pledge in JSC Russian Standard Bank;

49% proportion is to be maintained over the life of the bond 10% cash: RUB1,300mm Note: Constant FX rate of US$/RUB=65.00 used Indicative term sheet10 Target Securities US$350,000,000 Notes due April 2020 US$200,000,000 Notes due January 2024 Transaction Format UK Scheme of Arrangement Upfront Cash Repayment US$55,000,000 (10% of aggregate amount outstanding), plus accrued but unpaid interest on Target Securities Exchange Bond Size US$495,000,000 (90% of aggregate amount outstanding) Exchange Bond Issuer Russian Standard Ltd.

(“RSL”) (Single-purpose SPV, restricted from conducting any other business or incurring any additional indebtedness, subsidiary of Roust Holdings Limited) Status Senior, secured Exchange Bond Security 49% shares in JSC Russian Standard Bank pledged to Noteholders– 49% proportion to be maintained over the life of the bond, limitations on creation of other classes of shares by RSB, which may have a dilutive effect on the shares pledged Exchange Bond Coupon 13% per annum, fixed, payable in equal instalments semi-annually Exchange Bond Coupon Type PIK until Trigger event, cash thereafter Trigger event– RSB’s profitability over two quarters according to IFRS, or payment of dividends Exchange Bond Maturity Expected 26 October 2022 (7 years from issue date) Issuer Call Option At any time in full or in part at outstanding principal amount plus accrued interest to call date Change of Control Put Option At par (100) plus any accrued and unpaid interest if Mr.

Roustam Tariko ceases to ultimately own: - 100% of voting share capital of RSL - at least 50% plus one share of voting share capital of RSB Amortization Commencing at the earlier of: year 5 of the bond or Trigger event Trigger event– payment of dividends by RSB (for the periods preceding year 5) Amortization Schedule If no dividends paid: year 5 - $150m;

year 6 - $200m;

year 7– remaining amount, payable on a semi-annual basis each year If dividends paid by RSB before year 5: full amount of net income according to IFRS for the period less cash coupon (up to year 5) Exchange Bond Listing Frankfurt SE (application will be made prior to settlement) Denominations $180,000.00 and integral multiples of $1.00 in excess thereof Restructuring is to be accompanied by reconfiguration of the Bank’s operating strategy6 key drivers of RSB’s recovery business plan Successful restructuring and implementation of the new business plan allows the Bank to return to viability with sufficient capital through the medium term Maintaining attractive yields across the loan portfolio2 Lower cost of funding3 Continued cost cutting initiatives4 Intellectual Data Analysis as a competitive advantage5 “Back to basics”: offering simple and low risk products to good clients111 Non-credit business development6 Bank will return to profitability at the end of 2016 and reach stable growth in 2019 Bank’s business model evolution12 2015 Market stabilization 2016 New model implementation 2017 Sustained profitability 2019-2021 Stable growth Return to overall growth of the loan portfolio Return to annual positive profit generation Fulfillment of all mandatory regulatory ratios Refocus on development of infrastructure Complex measures for recapitalization Strict fulfillment of CBR obligatory ratios Improvement in collection to the 95.5% level Stabilization of the macroeconomic situation Aggressive sales growth strategy Continued cost optimization Returning to profit in Q4’16 Return to strategic growth and recovery of market position FINANCIAL PERFORMANCE POST RESTRUCTURING Medium term annual forecasts of the new business plan post restructuring Balance sheet Annual balance sheet evolution (FY’12 – FY’21, under RAS)14 Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Assets Cash and balances with CBR 28,739 43,479 48,006 33,670 34,323 38,167 40,941 43,984 44,125 46,485 Due from other banks 4,916 5,402 4,545 5,367 5,367 5,367 5,367 5,367 5,367 5,367 HFT and AFS securities 44,257 43,746 146,002 191,154 183,259 167,567 130,945 105,946 61,129 55,116 Federal loan bonds of RF (OFZ) 0 0 0 5,000 5,000 5,000 5,000 5,000 5,000 5,000 Corporate Shares 6,473 6,473 6,473 15,404 15,404 15,404 15,404 15,404 15,404 15,404 Loans and advances to customers 185,962 243,392 200,751 144,289 156,281 203,752 263,536 320,103 365,069 394,327 o/w retail loans 177,671 231,318 179,378 113,169 126,438 176,872 237,121 293,349 337,603 365,948 Investment in subsidiaries 8,354 8,800 8,873 7,262 7,262 7,262 7,262 7,262 7,262 7,262 Fixed and intangible assets 5,183 5,686 4,787 3,756 2,676 3,489 4,512 5,481 6,251 6,752 Other assets 8,347 13,250 9,901 7,568 11,818 15,408 19,929 24,207 27,607 29,820 Total assets 292,230 370,228 429,337 413,470 421,390 461,415 492,896 532,754 537,214 565,532 Liabilities Due to banks 12,519 37,598 109,060 151,727 145,727 133,849 106,128 87,205 53,282 48,730 Customer accounts (deposits) 173,028 212,058 171,666 182,265 220,629 269,707 315,303 357,928 379,070 393,760 Debt securities in issue 36,807 41,442 47,752 4,439 2,500 0 0 0 0 0 Subordinated loan 33,271 36,902 59,595 17,959 8,959 8,959 8,959 8,959 8,959 8,959 Subordinated debt (OFZ) 0 0 0 5,000 5,000 5,000 5,000 5,000 5,000 5,000 Other liabilities 6,284 2,342 2,344 1,910 1,910 1,910 1,910 1,910 1,910 1,910 Total liabilities 261,909 330,341 390,417 363,300 384,725 419,425 437,300 461,002 448,221 458,359 Equity Share capital and premium 1,781 6,781 6,644 6,616 6,616 6,616 6,616 6,616 6,616 6,616 Retained earnings and other reserves 28,540 33,106 32,275 43,554 30,049 35,374 48,980 65,135 82,376 100,557 Shareholders' equity 30,321 39,887 38,919 50,170 36,665 41,990 55,596 71,751 88,992 107,173 Total equity and liabilities 292,230 370,228 429,337 413,470 421,390 461,415 492,896 532,754 537,214 565,532 Balance sheet Incomest.

Capital Medium term annual forecasts of the new business plan post restructuring Income statement Annual income statement evolution (FY’12 – FY’21, under RAS)15 Expected cash coupon payments under the New Notes– to be serviced by the New Issuer (RSL) Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Cash coupon payments by RSL*N/A PIK coupon accrual 2,526 5,053 5,053 4,736 3,363 Notes: Assumes PIK coupon accrual until 1H 2017 inclusive;

cash coupon servicing commencing in 2H 2017 positive net income gene rated in 1H 2017 No early principal amortization;

scheduled amortization to commence in 2020 Constant FX rate of US$/RUB=65.00 used Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Total interest income 49,313 74,057 71,973 52,791 45,759 58,228 73,804 85,807 94,222 101,666 Total interest expense (16,470) (26,708) (26,820) (38,801) (29,880) (27,391) (29,201) (30,858) (31,281) (30,545) Net interest income 32,843 47,349 45,153 13,989 15,879 30,837 44,604 54,949 62,941 71,121 Net fee & commission income 9,705 15,133 13,660 6,197 7,231 8,683 11,913 15,146 17,904 20,358 New Product Development (Acq.

Margin ) 0 0 0 65 598 897 939 1,109 1,279 1,449 Other income 2,351 4,052 15,383 61,009 10,281 12,129 10,808 9,254 8,294 7,618 Net income / loss on FX operations (1,169) (2,140) (3,308) 6,147 9,204 8,791 7,083 5,094 3,390 1,846 Trading portfolio result 0 275 8,984 5,576 (768) (768) (768) (1,024) (1,024) (1,024) Profit from insurance operations 1,900 5,250 3,572 707 450 1,038 1,132 1,282 1,425 1,568 Financial Aid received¹ 0 0 0 14,221 0 0 0 0 0 0 Other operating results 1,973 1,464 6,826 2,683 2,100 3,934 4,424 5,135 5,859 6,635 Depositary Insurance Agency's fee (353) (796) (692) (500) (705) (865) (1,063) (1,232) (1,356) (1,408) Subordinated debt restructuring 0 0 0 32,175 0 0 0 0 0 0 Total operating income 44,899 66,534 74,196 81,260 33,989 52,546 68,264 80,459 90,418 100,546 Operating expenses (24,317) (29,253) (23,964) (18,528) (15,960) (18,560) (22,272) (25,613) (28,174) (30,991) Pre-provision income 20,582 37,281 50,232 62,732 18,029 33,986 45,992 54,846 62,244 69,554 Loan loss provisions (12,000) (33,815) (47,845) (51,591) (34,910) (27,589) (29,268) (34,972) (41,049) (47,220) Profit before tax 8,582 3,466 2,387 11,141 (16,881) 6,397 16,724 19,874 21,195 22,334 Tax expense (2,644) (1,220) (1,341) 180 3,376 (1,072) (3,118) (3,718) (3,954) (4,153) Net income 5,938 2,247 1,046 11,321 (13,505) 5,325 13,606 16,156 17,241 18,181 Balance sheet Incomest.

Capital Short term quarterly forecasts of the new business plan post restructuring Capital16 Quarterly capital evolution ( Q1’15 – Q4’16) Historical Forecast RUBmm Q1’15A Q2’15A Q3’15E Q4’15E Q1’16E Q2’16E Q3’16E Q4’16E N1.1 & N1.2 N1.1 capital 22,697 23,834 25,248 32,248 25,587 32,366 29,611 29,550 N1.2 capital 22,697 23,834 25,248 32,248 25,587 32,366 29,611 29,550 N1.1 & N1.2 RWAs 362,835 376,288 397,363 402,545 419,074 425,248 413,961 425,053 N1.1 ratio 6.3% 6.3% 6.4%¹ 8.0% 6.1% 7.6% 7.2% 7.0% N1.2 ratio 6.3% 6.4% 8.0% 6.1% 7.6% 7.2% 7.0% Capital surplus / (gap) For N1.1– 5% requirement 1.3% 1.3% 1.4% 3.0% 1.1% 2.6% 2.2% 2.0% For N1.2– 6% requirement 0.3% 0.3% 0.4% 2.0% 0.1% 1.6% 1.2% 1.0% N1.0 N1.0 capital 64,171 62,086 67,177 55,535 49,453 44,362 45,058 44,447 N1.0 RWAs 363,516 377,032 397,998 403,182 419,560 425,734 414,446 425,539 N1.0 ratio 17.7% 16.5% 16.9% 13.8% 11.8% 10.4% 10.9% 10.4% Capital surplus / (gap) For N1.0– 10% requirement 7.7% 6.5% 6.9% 3.8% 1.8% 0.4% 0.9% 0.4% Balance sheet Incomest.

Capital Medium term annual forecasts of the new business plan post restructuring Capital Annual capital evolution (FY’15 – FY’21)17 Balance sheet Incomest.

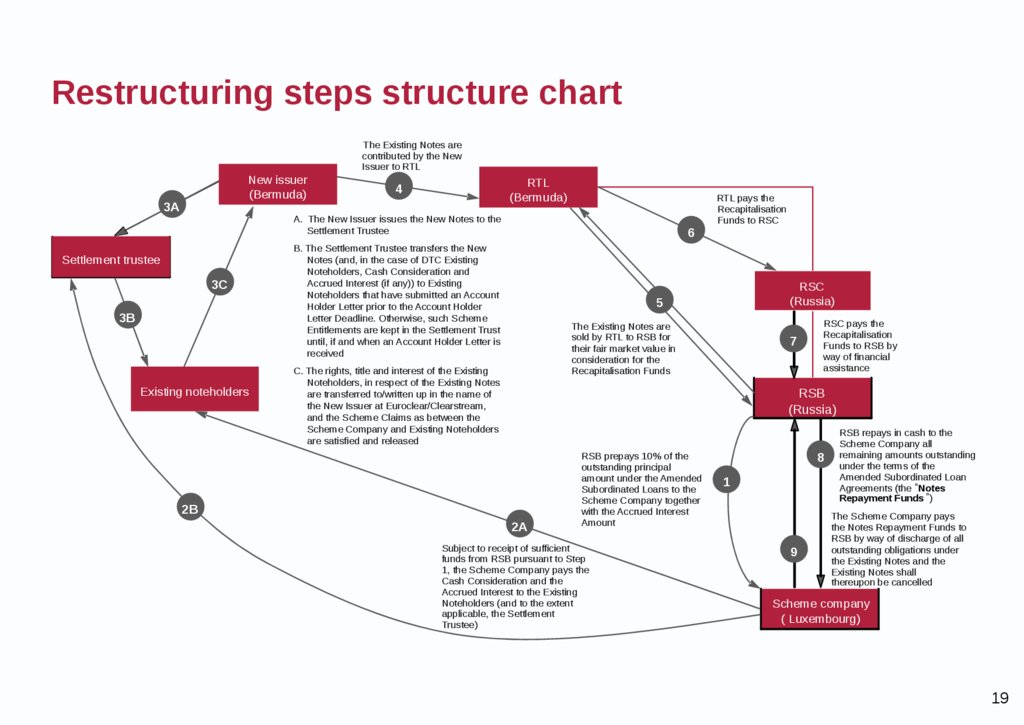

Capital RUBmm FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Profit for the period 11,321 (13,505) 5,325 13,606 16,156 17,241 18,181 Base Capital 32,248 29,550 31,517 38,118 53,084 70,855 88,256 Additional Capital (4,430) (2,933) (1,457) 0 0 0 0 Main Capital 32,248 29,550 31,517 38,118 53,084 70,855 88,256 Additional Capital 23,288 14,897 19,094 25,583 26,341 25,635 24,782 Own funds 55,535 44,447 50,611 63,701 79,425 96,490 113,038 Risk Weighted Assets for N1.1 and N1.2 402,545 425,053 426,623 450,570 528,139 595,806 629,125 Risk Weighted Assets for N1.0 403,182 425,539 426,958 450,754 528,322 595,989 629,309 N.1.1 (5%) 8.0% 7.0% 7.4% 8.5% 10.1% 11.9% 14.0% N.1.2 (6%) 8.0% 7.0% 7.4% 8.5% 10.1% 11.9% 14.0% N.1.0 (10%) 13.8% 10.4% 11.9% 14.1% 15.0% 16.2% 18.0% APPENDIX Restructuring steps structure chart19 Scheme company ( Luxembourg)RSB (Russia)) Existing noteholdersRSC (Russia)RTL (Bermuda) The Existing Notes are contributed by the New Issuer to RTL The Existing Notes are sold by RTL to RSB for their fair market value in consideration for the Recapitalisation Funds RTL pays the Recapitalisation Funds to RSC RSC pays the Recapitalisation Funds to RSB by way of financial assistance RSB repays in cash to the Scheme Company all remaining amounts outstanding under the terms of the Amended Subordinated Loan Agreements (the“ Notes Repayment Funds”) RSB prepays 10% of the outstanding principal amount under the Amended Subordinated Loans to the Scheme Company together with the Accrued Interest Amount Subject to receipt of sufficient funds from RSB pursuant to Step 1, the Scheme Company pays the Cash Consideration and the Accrued Interest to the Existing Noteholders (and to the extent applicable, the Settlement Trustee) The Scheme Company pays the Notes Repayment Funds to RSB by way of discharge of all outstanding obligations under the Existing Notes and the Existing Notes shall thereupon be cancelled Settlement trustee A.

The New Issuer issues the New Notes to the Settlement Trustee B.

The Settlement Trustee transfers the New Notes (and, in the case of DTC Existing Noteholders, Cash Consideration and Accrued Interest (if any)) to Existing Noteholders that have submitted an Account Holder Letter prior to the Account Holder Letter Deadline.

Otherwise, such Scheme Entitlements are kept in the Settlement Trust until, if and when an Account Holder Letter is received C.

The rights, title and interest of the Existing Noteholders, in respect of the Existing Notes are transferred to/written up in the name of the New Issuer at Euroclear/Clearstream, and the Scheme Claims as between the Scheme Company and Existing Noteholders are satisfied and released153C87642A93B2B New issuer (Bermuda)3A Corporate structure chartRHL (BVI)RTL (Bermuda) New Issuer (Bermuda)RSC (Russia)RSB (Russia) Scheme Company (Luxembourg)RSI (Russia) Existing Noteholders 99.999% 9.1% (direct) Existing Subordinated Loans 90.8% (direct) 14.5% (direct) 85.5% (direct) 100% (direct) 100% (direct) Existing Notes20

The Materials are provided subject to (i) the terms of this Disclaimer, and (ii) the 'Important Securities Law Notice' on pages (iii)– (vi) of the Scheme Document which appears on the scheme website (http://sites.dfkingltd.com/rsb).

If there is any inconsistency between this Disclaimer and the s aid Notice, the said Notice shall prevail to the extent of that inconsistency.

The information contained herein (the “Materials”) have been prepared by Russian Standard Bank (the “Company”) and its subsidiaries (the “Group”) solely for use at this presentation.

By accepting the Materials or attending this presentation, you are agreeing to maintain absolute confidentiality regarding the inf ormation disclosed in the Materials and further agree to the following limitations and notifications.

The Materials have been provided to you solely for your information and background and are subject to amendment.

The Materials (or any part of them) may not be reproduced or redistributed, passed on, or the contents otherwise divulged, directly or indirectly, to any oth er person or published in whole or in part for any purpose without the prior written consent of the Company.

Failure to comply with this restriction may constitute a violation of applica ble securities laws.

The Materials are not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, c ountry or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jur isdiction.

The Materials do not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the secu rities referred to herein in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration, exemption from registration or qualification under the securities laws of any jurisdiction.

The Materials are not for public release, publication or distribution, directly or indirectly, in or into the United States (in cluding its territories and possessions, any State of the United States and the District of Columbia).

This communication is not and does not constitute or form a part of any offer of, or solicitation to purchase or subscribe for, any securities in the United States.

Any such securities have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “Securities Act”).

Any such securities may not be offered or sold in the United States or to, or for the account or benefit of, U.S.

persons (as such term is defined in Regulation S under the Securities Act), excep t pursuant to an exemption from the registration requirements of the Securities Act.

No public offering of securities will be made in the United States of America.

The Materials are addressed only to and directed only at (i) persons who are outside the United Kingdom or (ii) investment prof essionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the “Order”) and (iii) high net worth entities, a nd other persons to whom it may lawfully be communicated, falling within Article 49(2) of the Order (all such persons together being referred to as “relevant persons”).

Any investment activity to which this communication relates will only be available to and will only be engaged with, relevant persons.

Any person who is not a relevant person should not act or rely on this docu ment or any of its contents.

In any EEA member state that has implemented EU Directive 2003/71/EC, as amended (together with any applicable implementing meas ures in any Member State, the “Prospectus Directive”), these Materials are addressed only to and directed solely at “qualified investors” (as defined in Prospectus Dir ective) in that Member State.

The Materials are an advertisement and not a prospectus for the purposes of applicable measures implementing the Prospectus Directive and as such do not constitut e an offer to sell or the solicitation of an offer to purchase securities.

The Materials are not an offer, or an invitation to make offers, to sell, exchange or otherwise transfer securities in the Russ ian Federation to or for the benefit of any Russian person or entity and does not constitute an advertisement or offering of securities in the Russian Federation within the meaning of Russi an securities laws.

Information contained in herein is not intended for any persons in the Russian Federation who are not “qualified investors” within the meaning of Article 51.2 of th e Federal Law No.

39- FZ “On the Securities Market” dated 22 April 1996, as amended (the “Russian QIs”) and must not be distributed or circulated into the Russian Federation or made avai lable in the Russian Federation to any persons who are not Russian QIs, unless and to the extent they are otherwise permitted to access such information under Russian law.

Under Russian law, the New Notes are securities of a foreign issuer.

The New Notes are not eligible for initial offering in the Russian Federation.

Neither the issue of the New Notes nor the Mater ials have been or will be registered or approved in the Russian Federation and is intended for “placement” or “circulation” in the Russian Federation (each as defined in Russian sec urities laws) unless and to the extent otherwise permitted under Russian law.

The information contained in the Materials does not purport to be comprehensive and has not been independently verified.

The in formation contained in the Materials is subject to updating, completion, revision, verification and amendment and such information may change materially.

The Company is under no obligation to update or keep current the information contained in the Materials or in the presentation to which it relates and any opinions expressed in them are subject to change without notice.

No representation or warranty, expressed or implied, is made by the Company and any of its affiliates as to the fairness, accuracy, reasonableness or completeness of the i nformation contained herein and no reliance should be placed on it.

Neither the Company nor any other person accepts any liability for any loss howsoever arising, directly or indire ctly, from reliance on the Materials.

The Company and its affiliates, advisors and representatives shall have no liability whatsoever (in negligence or otherwise) for any loss whatsoeve r arising from any use of the Materials.

The Materials largely comprise a summary of information contained in the scheme documentation which has already been made avail able to bondholders.

Reading the Materials is not a substitute for reading the scheme documentation in its entirety and bondholders should ensure that they read the scheme documen tation rather than simply rely upon the Materials.

Russian Standard Finance S.A has not independently verified or diligenced this presentation or any of the information included in this presentation.

Executive summary Russian Standard Bank (“RSB”) was founded in 1999 as a financial innovator effectively creating the Russian market for consumer lending and credit cards Today RSB is one of the largest full-service banks in Russia that has attracted 30 million clients, offering a unique product p roposition and a broad multi-channel distribution network covering the country– the Bank remains a leader in its core consumer finance segments, with core focus on credit cards issuance Being a leader of financial innovation allowed RSB to generate healthy profits while during economic downturns, RSB has been ab le to successfully optimise its business model and return to profitability within a short period of time Many investors have been working with RSB for over 10 years and have always had good returns on investments The current macroeconomic and geopolitical situation in Russia has affected the banking industry and particularly the retail se gment, which has resulted in a sharp increase in provision requirements and cost of funding, reduction in the proportion of “good” borrowers to extend the new loans to, leading to a negative impact on financial results of Russian banks– One of the strongest effects of the Russian economy downturn has been felt in the credit cards industry– Credit cards business is inherently highly profitable yet highly cyclical: in the growth environment this allows banks to record significant profits, but during the downturns credit card companies start recording losses, which puts their capital adequacy a t risk– this is a universal rule for credit card companies globally Being one of the leaders in the Russian credit cards market, RSB has found itself in the current recession temporarily facing s ignificant losses, which has led to a need for additional Tier 1 capital in order to comply with regulatory capital adequacy requirements.

Additional Tier 1 capital will allow RSB to withstand pressures of the current crisis, and recover and revert to profitability at the end of 2016 Prior to that, however, RSB is expected to continue recording elevated losses, as driven by protracted amortization of the “old” loan portfolio that can take up to 12 months;

gradual recovery of new loan sales over the next 12-15 months, which currently stand near historic minimum ;

temporary increase in operating expenditure during ongoing headcount optimisation and significant severance payments;

funding costs that are expected to remain elevated at least until the first half of 20162 Executive summary (cont’d)3 At the moment, in order to avoid a breach by RSB of its regulatory capital adequacy ratios which, in turn, would lead to a write-down in full of the subordinated notes due 2020 and 2024 (the "Notes"), RSB requires a restructuring of the Notes The restructuring will provide the holders of the Notes with an immediate partial repayment of the notes due 2020 and 2024 (being 10% of the outstanding principal together with aggregate Accrued Interest Amounts) and an exchange of the remainder (90%) for new notes issued by an SPV and secured by 49% of the shares in RSB.

The resulting profit obtained by RSB will improve RSB’s capital position, enabling it to comply with its regulatory capital adequacy ratios and avoid the significant negative consequences ofany breach for all stakeholders The restructuring of the Notes also forms part of RSB's wider recapitalisation plan.

Should the restructuring be successful, fu rther financial support from the shareholder and the government would remain open to RSB, which would assist with its return to profitability by the end of 2016– If RSB is in compliance with all applicable regulatory requirements, RSB would remain eligible for state financial support of RUB 5bn and, subject to Russian Government resolution and CBR approval, an extension of RUB 5bn of existing subordinated loans from VEB– The Shareholder has already invested approximately RUB 14bn in RSB's Tier 1 capital (without such injections RSB's N1.1 ratio would have fallen to 2.5% already) and will be considering additional investment to further improve RSB's capital adequacy ratios The proposed bond exchange is a fair and effective solution:– It allows RSB to comply with regulatory requirements avoiding a Write Down Event and writedown for the 20s and 24s– Whilst not giving bondholders direct legal recourse to RSB or its assets, it nevertheless positions bondholders to recover their investment once RSB returns to profitability or pays any form of dividend Executive summary (cont’d)4 We have developed a new business model that would make RSB profitable again by the end of 2016 provided that there will be no further substantial negative macroeconomic and geopolitical disruptions The key pillars of the new model are based on innovations that have been already successfully implemented in many markets by our global partners and strategic consultants– Offering simple low risk products to “good” clients with healthy credit ratings– Maintaining attractive yields across the loan portfolio: prudent pricing across the credit quality spectrum– Lower cost of funding and hedging costs following general market trends– Reduction of operating expenses and continued cost cutting initiatives : create an effective and profitable distribution network with extensive use of remote channels– Intellectual Data Analysis as a competitive advantage : new scoring models using a wide range of data sources, risk management and collection improvement– Non-credit business development : participation in commercial margin of merchants using innovative loyalty platforms and our current wide acquiring network;

increasing non-interest income through transaction commissions, banking insurance, online and mobile services We have already implemented a number of business optimisation initiatives that are bringing significant results– Introduced new products, including instalment credit cards for the mass segment– Improved credit policies and scoring models, which has already resulted in a significant reduction of risks on new sales– Focused resources on collection and improved procedures and policies– Reduced its expenses base and exited low-return, non-core projects We are confident that the new business model will bring RSB back to profitability by the end of 2016 while the proposed exchange offer will allow RSB to comply successfully with its regulatory capital ratios, avoid a Write Down Event and eventually ensure bondholders recover their investment We ask bondholders to support this win-win solution and vote in favour of the exchange offer RSB has a track record of providing high and reliable returns to international bondholders Historic placements and successful repayments by RSB Issue date Instrument type Ranking Principal amount Coupon rate, p.a.

Maturity date Status Sep-2003 Credit-linked notes Senior unsecured US$30mm 10% Mar-2004 Fully repaid on schedule Nov-2003 Loan participation notes Senior unsecured US$30mm 11% May-2005 Fully repaid on schedule Apr-2004 (incr.

Nov-2014) Loan participation notes Senior unsecured US$150mm + US$150mm 8.75% Apr-2007 Fully repaid on schedule Sep-2004 Loan participation notes Senior unsecured US$300mm 7.8% Sep-2007 Fully repaid on schedule Apr-2005 Loan participation notes Senior unsecured US$300mm 8.125% Apr-2008 Fully repaid on schedule Sep-2005 Loan participation notes Senior unsecured US$500mm 7.5% Oct-2010 Fully repaid on schedule Dec-2005 Loan participation notes Subordinated Lower-Tier 2 US$200mm 8.875%, re-set to 7.73% in 2010 Dec-2015, call option in Dec-2010 US$147mm publicly outstanding– prompt coupon payments to date, buybacks and a tender in 2015 Jan-2006 Loan participation notes Senior unsecured US$200mm 6.72% Feb-2007 Fully repaid on schedule Apr-2006 Loan participation notes Senior unsecured US$350mm 8.625% May-2011 Fully repaid on schedule Sep-2006 Loan participation notes Senior secured EUR400mm 6.825% Sep-2009 Fully repaid on schedule Nov-2006 Loan participation notes Subordinated Lower-Tier 2 US$200mm 9.75%, re-set to 7.561% in 2011 Dec-2016, call option in Dec-2011 US$169mm publicly outstanding– prompt coupon payments to date, buybacks and a tender in 2015 Apr-2007 Eurocommercial paper (ECP) Senior unsecured US$215mm Zero, implied yield 8.1% at issue Apr-2008 Fully repaid on schedule Jun-2007 Loan participation notes Senior unsecured US$400mm 8.485% Jun-2010 Fully repaid on schedule Oct-2010 Eurocommercial paper (ECP) Senior unsecured US$100mm Zero, implied yield 9.1% at issue Oct-2011 Fully repaid on schedule Nov-2011 Eurocommercial paper (ECP) Senior unsecured US$150mm Zero, implied yield 8.5% at issue May-2012 Fully repaid on schedule Apr-2012 Eurocommercial paper (ECP) Senior unsecured US$150mm Zero, implied yield 5.5% at issue Apr-2013 Fully repaid on schedule Jul-2012 (incr.

Nov-2012) Loan participation notes Senior unsecured US$350mm + US$175mm 9.25% Jul-2017, put option in Jul-2015 US$38mm outstanding– prompt coupon payments to date, buybacks and a tender in 2014- 2015, US$284mm put in 2015 Feb-2013 (incr.

Mar-2013) Loan participation notes Senior unsecured CNY500mm + CNY750mm 8% Feb-2015 Fully repaid on schedule Note: The list excludes the most recently issued RSB due 2020 (originally due 2018) and due 2024 bonds to be targeted via propo sed restructuring5 Total principal amount of Eurobonds issued by RSB to date: US$4.6bn equivalent Total number of Eurobond placements completed by RSB to date: 18 (incl.

taps) RSB vs.

peers in Eurobond marketsRSB US$4.6bn raised via 18 placements Alfa-Bank US$6.7bn raised via 16 placements Prom- svyazbank (PSB) US$3.6bn raised via 19 placements Nomos (Bank Otkritie) US$2.7bn raised via 9 placements Renais- sance Credit US$1.2bn raised via 10 placements Credit Bank of Moscow US$1.2bn raised via 3 placements Tinkoff Bank US$0.7bn raised via 5 placements Bank St.

Pet’burg (BSPB) US$0.5bn raised via 5 placements Note: Based on Bloomberg & RSB Downturn in Russian economy has negatively affected profitability of banks The slowdown from 2011 to 2014 was largely a result of a drop in oil and gas exports, less investment in the Russian economy, increased capital outflows and a decrease in the Russian Government’s international reserves A combination of US/EU sanctions, Russia’s countersanctions, terms of trade shock and significant tightening of monetary policy have resulted in sharp economic contraction and downward revision of near- term GDP growth forecasts Recent decrease in oil price has been one of the main factors for currency weakness, which has pushed up inflation levels Profitability of Russian banks has been negatively impacted by the spike in CBR rate in Dec-14 Real GDP growth (actual)6 Russian macroeconomic forecasts Oil price and US$/RUB evolution Source: Bloomberg as of 28 September 2015, Central Bank of Russia ¹ Y-o-Y growth as of Jul-15 6.6% 6.5% 11.4% 14.5%¹ Inflation 32.9 65.7 100.4 47.52040608010012020304050607080 Jan-14Jun-14Dec-14 Jun-15 US$/RUB Brent price (US$/bbl) 3.4% 1.3% 0.6% (2.8%)-5%-3%-1%1%3%5% 201220132014 2015E Without the restructuring, RSB will breach Russian capital requirement regulation in Q4 20157 Escalating loan loss provisions and a decline in net interest income due to a deterioration in asset quality are expected to le ad to significant losses over the following months Given RSB’s current capital levels and expected short term profitability the Bank will breach regulatory capital requirements in Q4’15 RSB’s capital position with no restructuring in place RUBmm, under RAS¹ Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Q3’16 Q4’16 Profit for the period 340 1,207 (110) 205 (3,500) (3,689) (7,456) (3,113) (2,958) (2,969) (2,777) (2,502) (21,760) (4,948) (3,625) Base Capital 23,834 24,998 24,868 25,245 21,622 17,805 11,427 8,491 5,360 2,217 7,652 7,655 7,332 4,835 1,006 Additional Capital (5,292) (5,287) (5,279) (5,276) (5,274) (5,271) (4,430) (2,952) (2,950) (2,949) (2,947) (2,945) (2,944) (2,939) (2,933) Main Capital 23,834 24,998 24,868 25,245 21,622 17,805 11,427 8,491 5,360 2,217 7,652 7,655 7,332 4,835 1,006 Additional Capital 38,252 39,205 43,491 41,929 40,232 40,232 39,258 38,121 38,121 37,323 29,866 27,866 8,089 4,711 3,914 Own funds 62,086 64,203 68,359 67,175 61,853 58,037 50,685 46,612 43,481 39,541 37,518 35,520 15,420 9,547 4,920 Risk Weighted Assets for N1.1 and N1.2 376,288 394,223 397,047 397,360 401,678 394,759 394,267 402,160 398,157 381,454 378,128 374,185 360,895 342,173 354,944 Risk Weighted Assets for N1.0 377,032 394,889 397,674 397,995 402,314 395,396 394,904 402,646 398,642 381,939 378,613 374,671 361,380 342,658 355,430 N.1.1 (5%) 6.3% 6.3% 6.3% 6.4% 5.4% 4.5% 2.9% 2.1% 1.3% 0.6% 2.0% 2.0% 2.0% 1.4% 0.3% N.1.2 (6%) 6.3% 6.3% 6.3% 6.4% 5.4% 4.5% 2.9% 2.1% 1.3% 0.6% 2.0% 2.0% 2.0% 1.4% 0.3% N.1.0 (10%) 16.5% 16.3% 17.2% 16.9% 15.4% 14.7% 12.8% 11.6% 10.9% 10.4% 9.9% 9.5% 4.3% 2.8% 1.4% ¹All numbers presented in the presentation are under Russian Accounting Standards (“RAS”), unless otherwise noted Write down event following closing of RAS accounts for the end of February 2016 N.1.1 ratio is kept at 2% temporarily as the notes are being written down Full write down following closing of RAS accounts for August 2016 RESTRUCTURING PLAN Restructuring of the Bank’s liabilities will help the Bank to boost its N1.1 and N1.2 capital levels Proposed debt restructuring program Capital impact at the Bank level Total amount of bonds Transaction impact Capital contribution to N1.1 & N1.2 RUB22,750mm US$350mm 10% cash: RUB2,275mm 90% profit in income statement from write-off Value: RUB20,475mm US$315mm RUB13,000mm US$200mm 90% profit in income statement from write-off Value: RUB11,700mm US$180mm Total profit from restructuring recorded as part of capital: Value: RUB32,175mm US$495mm 10-04-2020 T2 bond (13.0%) 17-01-2024 T2 bond (11.5%)9 The Bank is proposing to restructure its US$350mm Notes due April 2020 and US$200mm Notes due January 2024 Without restructuring the Bank is expecting to breach N.1.2 capital adequacy ratio of the Central Bank by the end of October 20 15, which will eventually lead to occurrence of a write-down event for the Notes and loss of the full investment for the bondholders Current bondholders of both Notes are offered an upfront 10% cash payment, in addition to upfront cash repayment of all accrued and unpaid interest, and an exchange bond of US$495mm that is to be issued by a RHL subsidiary SPV– no haircut is proposed to bondholders Exchange bond security is to:– Pay a 13% coupon;

PIK until the Bank becomes profitable or pays any form of dividends, cash coupon thereafter– Have a 49% share pledge in JSC Russian Standard Bank;

49% proportion is to be maintained over the life of the bond 10% cash: RUB1,300mm Note: Constant FX rate of US$/RUB=65.00 used Indicative term sheet10 Target Securities US$350,000,000 Notes due April 2020 US$200,000,000 Notes due January 2024 Transaction Format UK Scheme of Arrangement Upfront Cash Repayment US$55,000,000 (10% of aggregate amount outstanding), plus accrued but unpaid interest on Target Securities Exchange Bond Size US$495,000,000 (90% of aggregate amount outstanding) Exchange Bond Issuer Russian Standard Ltd.

(“RSL”) (Single-purpose SPV, restricted from conducting any other business or incurring any additional indebtedness, subsidiary of Roust Holdings Limited) Status Senior, secured Exchange Bond Security 49% shares in JSC Russian Standard Bank pledged to Noteholders– 49% proportion to be maintained over the life of the bond, limitations on creation of other classes of shares by RSB, which may have a dilutive effect on the shares pledged Exchange Bond Coupon 13% per annum, fixed, payable in equal instalments semi-annually Exchange Bond Coupon Type PIK until Trigger event, cash thereafter Trigger event– RSB’s profitability over two quarters according to IFRS, or payment of dividends Exchange Bond Maturity Expected 26 October 2022 (7 years from issue date) Issuer Call Option At any time in full or in part at outstanding principal amount plus accrued interest to call date Change of Control Put Option At par (100) plus any accrued and unpaid interest if Mr.

Roustam Tariko ceases to ultimately own: - 100% of voting share capital of RSL - at least 50% plus one share of voting share capital of RSB Amortization Commencing at the earlier of: year 5 of the bond or Trigger event Trigger event– payment of dividends by RSB (for the periods preceding year 5) Amortization Schedule If no dividends paid: year 5 - $150m;

year 6 - $200m;

year 7– remaining amount, payable on a semi-annual basis each year If dividends paid by RSB before year 5: full amount of net income according to IFRS for the period less cash coupon (up to year 5) Exchange Bond Listing Frankfurt SE (application will be made prior to settlement) Denominations $180,000.00 and integral multiples of $1.00 in excess thereof Restructuring is to be accompanied by reconfiguration of the Bank’s operating strategy6 key drivers of RSB’s recovery business plan Successful restructuring and implementation of the new business plan allows the Bank to return to viability with sufficient capital through the medium term Maintaining attractive yields across the loan portfolio2 Lower cost of funding3 Continued cost cutting initiatives4 Intellectual Data Analysis as a competitive advantage5 “Back to basics”: offering simple and low risk products to good clients111 Non-credit business development6 Bank will return to profitability at the end of 2016 and reach stable growth in 2019 Bank’s business model evolution12 2015 Market stabilization 2016 New model implementation 2017 Sustained profitability 2019-2021 Stable growth Return to overall growth of the loan portfolio Return to annual positive profit generation Fulfillment of all mandatory regulatory ratios Refocus on development of infrastructure Complex measures for recapitalization Strict fulfillment of CBR obligatory ratios Improvement in collection to the 95.5% level Stabilization of the macroeconomic situation Aggressive sales growth strategy Continued cost optimization Returning to profit in Q4’16 Return to strategic growth and recovery of market position FINANCIAL PERFORMANCE POST RESTRUCTURING Medium term annual forecasts of the new business plan post restructuring Balance sheet Annual balance sheet evolution (FY’12 – FY’21, under RAS)14 Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Assets Cash and balances with CBR 28,739 43,479 48,006 33,670 34,323 38,167 40,941 43,984 44,125 46,485 Due from other banks 4,916 5,402 4,545 5,367 5,367 5,367 5,367 5,367 5,367 5,367 HFT and AFS securities 44,257 43,746 146,002 191,154 183,259 167,567 130,945 105,946 61,129 55,116 Federal loan bonds of RF (OFZ) 0 0 0 5,000 5,000 5,000 5,000 5,000 5,000 5,000 Corporate Shares 6,473 6,473 6,473 15,404 15,404 15,404 15,404 15,404 15,404 15,404 Loans and advances to customers 185,962 243,392 200,751 144,289 156,281 203,752 263,536 320,103 365,069 394,327 o/w retail loans 177,671 231,318 179,378 113,169 126,438 176,872 237,121 293,349 337,603 365,948 Investment in subsidiaries 8,354 8,800 8,873 7,262 7,262 7,262 7,262 7,262 7,262 7,262 Fixed and intangible assets 5,183 5,686 4,787 3,756 2,676 3,489 4,512 5,481 6,251 6,752 Other assets 8,347 13,250 9,901 7,568 11,818 15,408 19,929 24,207 27,607 29,820 Total assets 292,230 370,228 429,337 413,470 421,390 461,415 492,896 532,754 537,214 565,532 Liabilities Due to banks 12,519 37,598 109,060 151,727 145,727 133,849 106,128 87,205 53,282 48,730 Customer accounts (deposits) 173,028 212,058 171,666 182,265 220,629 269,707 315,303 357,928 379,070 393,760 Debt securities in issue 36,807 41,442 47,752 4,439 2,500 0 0 0 0 0 Subordinated loan 33,271 36,902 59,595 17,959 8,959 8,959 8,959 8,959 8,959 8,959 Subordinated debt (OFZ) 0 0 0 5,000 5,000 5,000 5,000 5,000 5,000 5,000 Other liabilities 6,284 2,342 2,344 1,910 1,910 1,910 1,910 1,910 1,910 1,910 Total liabilities 261,909 330,341 390,417 363,300 384,725 419,425 437,300 461,002 448,221 458,359 Equity Share capital and premium 1,781 6,781 6,644 6,616 6,616 6,616 6,616 6,616 6,616 6,616 Retained earnings and other reserves 28,540 33,106 32,275 43,554 30,049 35,374 48,980 65,135 82,376 100,557 Shareholders' equity 30,321 39,887 38,919 50,170 36,665 41,990 55,596 71,751 88,992 107,173 Total equity and liabilities 292,230 370,228 429,337 413,470 421,390 461,415 492,896 532,754 537,214 565,532 Balance sheet Incomest.

Capital Medium term annual forecasts of the new business plan post restructuring Income statement Annual income statement evolution (FY’12 – FY’21, under RAS)15 Expected cash coupon payments under the New Notes– to be serviced by the New Issuer (RSL) Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Cash coupon payments by RSL*N/A PIK coupon accrual 2,526 5,053 5,053 4,736 3,363 Notes: Assumes PIK coupon accrual until 1H 2017 inclusive;

cash coupon servicing commencing in 2H 2017 positive net income gene rated in 1H 2017 No early principal amortization;

scheduled amortization to commence in 2020 Constant FX rate of US$/RUB=65.00 used Historical Forecast RUBmm FY’12A FY’13A FY’14A FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Total interest income 49,313 74,057 71,973 52,791 45,759 58,228 73,804 85,807 94,222 101,666 Total interest expense (16,470) (26,708) (26,820) (38,801) (29,880) (27,391) (29,201) (30,858) (31,281) (30,545) Net interest income 32,843 47,349 45,153 13,989 15,879 30,837 44,604 54,949 62,941 71,121 Net fee & commission income 9,705 15,133 13,660 6,197 7,231 8,683 11,913 15,146 17,904 20,358 New Product Development (Acq.

Margin ) 0 0 0 65 598 897 939 1,109 1,279 1,449 Other income 2,351 4,052 15,383 61,009 10,281 12,129 10,808 9,254 8,294 7,618 Net income / loss on FX operations (1,169) (2,140) (3,308) 6,147 9,204 8,791 7,083 5,094 3,390 1,846 Trading portfolio result 0 275 8,984 5,576 (768) (768) (768) (1,024) (1,024) (1,024) Profit from insurance operations 1,900 5,250 3,572 707 450 1,038 1,132 1,282 1,425 1,568 Financial Aid received¹ 0 0 0 14,221 0 0 0 0 0 0 Other operating results 1,973 1,464 6,826 2,683 2,100 3,934 4,424 5,135 5,859 6,635 Depositary Insurance Agency's fee (353) (796) (692) (500) (705) (865) (1,063) (1,232) (1,356) (1,408) Subordinated debt restructuring 0 0 0 32,175 0 0 0 0 0 0 Total operating income 44,899 66,534 74,196 81,260 33,989 52,546 68,264 80,459 90,418 100,546 Operating expenses (24,317) (29,253) (23,964) (18,528) (15,960) (18,560) (22,272) (25,613) (28,174) (30,991) Pre-provision income 20,582 37,281 50,232 62,732 18,029 33,986 45,992 54,846 62,244 69,554 Loan loss provisions (12,000) (33,815) (47,845) (51,591) (34,910) (27,589) (29,268) (34,972) (41,049) (47,220) Profit before tax 8,582 3,466 2,387 11,141 (16,881) 6,397 16,724 19,874 21,195 22,334 Tax expense (2,644) (1,220) (1,341) 180 3,376 (1,072) (3,118) (3,718) (3,954) (4,153) Net income 5,938 2,247 1,046 11,321 (13,505) 5,325 13,606 16,156 17,241 18,181 Balance sheet Incomest.

Capital Short term quarterly forecasts of the new business plan post restructuring Capital16 Quarterly capital evolution ( Q1’15 – Q4’16) Historical Forecast RUBmm Q1’15A Q2’15A Q3’15E Q4’15E Q1’16E Q2’16E Q3’16E Q4’16E N1.1 & N1.2 N1.1 capital 22,697 23,834 25,248 32,248 25,587 32,366 29,611 29,550 N1.2 capital 22,697 23,834 25,248 32,248 25,587 32,366 29,611 29,550 N1.1 & N1.2 RWAs 362,835 376,288 397,363 402,545 419,074 425,248 413,961 425,053 N1.1 ratio 6.3% 6.3% 6.4%¹ 8.0% 6.1% 7.6% 7.2% 7.0% N1.2 ratio 6.3% 6.4% 8.0% 6.1% 7.6% 7.2% 7.0% Capital surplus / (gap) For N1.1– 5% requirement 1.3% 1.3% 1.4% 3.0% 1.1% 2.6% 2.2% 2.0% For N1.2– 6% requirement 0.3% 0.3% 0.4% 2.0% 0.1% 1.6% 1.2% 1.0% N1.0 N1.0 capital 64,171 62,086 67,177 55,535 49,453 44,362 45,058 44,447 N1.0 RWAs 363,516 377,032 397,998 403,182 419,560 425,734 414,446 425,539 N1.0 ratio 17.7% 16.5% 16.9% 13.8% 11.8% 10.4% 10.9% 10.4% Capital surplus / (gap) For N1.0– 10% requirement 7.7% 6.5% 6.9% 3.8% 1.8% 0.4% 0.9% 0.4% Balance sheet Incomest.

Capital Medium term annual forecasts of the new business plan post restructuring Capital Annual capital evolution (FY’15 – FY’21)17 Balance sheet Incomest.

Capital RUBmm FY’15E FY’16E FY’17E FY’18E FY’19E FY’20E FY’21E Profit for the period 11,321 (13,505) 5,325 13,606 16,156 17,241 18,181 Base Capital 32,248 29,550 31,517 38,118 53,084 70,855 88,256 Additional Capital (4,430) (2,933) (1,457) 0 0 0 0 Main Capital 32,248 29,550 31,517 38,118 53,084 70,855 88,256 Additional Capital 23,288 14,897 19,094 25,583 26,341 25,635 24,782 Own funds 55,535 44,447 50,611 63,701 79,425 96,490 113,038 Risk Weighted Assets for N1.1 and N1.2 402,545 425,053 426,623 450,570 528,139 595,806 629,125 Risk Weighted Assets for N1.0 403,182 425,539 426,958 450,754 528,322 595,989 629,309 N.1.1 (5%) 8.0% 7.0% 7.4% 8.5% 10.1% 11.9% 14.0% N.1.2 (6%) 8.0% 7.0% 7.4% 8.5% 10.1% 11.9% 14.0% N.1.0 (10%) 13.8% 10.4% 11.9% 14.1% 15.0% 16.2% 18.0% APPENDIX Restructuring steps structure chart19 Scheme company ( Luxembourg)RSB (Russia)) Existing noteholdersRSC (Russia)RTL (Bermuda) The Existing Notes are contributed by the New Issuer to RTL The Existing Notes are sold by RTL to RSB for their fair market value in consideration for the Recapitalisation Funds RTL pays the Recapitalisation Funds to RSC RSC pays the Recapitalisation Funds to RSB by way of financial assistance RSB repays in cash to the Scheme Company all remaining amounts outstanding under the terms of the Amended Subordinated Loan Agreements (the“ Notes Repayment Funds”) RSB prepays 10% of the outstanding principal amount under the Amended Subordinated Loans to the Scheme Company together with the Accrued Interest Amount Subject to receipt of sufficient funds from RSB pursuant to Step 1, the Scheme Company pays the Cash Consideration and the Accrued Interest to the Existing Noteholders (and to the extent applicable, the Settlement Trustee) The Scheme Company pays the Notes Repayment Funds to RSB by way of discharge of all outstanding obligations under the Existing Notes and the Existing Notes shall thereupon be cancelled Settlement trustee A.

The New Issuer issues the New Notes to the Settlement Trustee B.

The Settlement Trustee transfers the New Notes (and, in the case of DTC Existing Noteholders, Cash Consideration and Accrued Interest (if any)) to Existing Noteholders that have submitted an Account Holder Letter prior to the Account Holder Letter Deadline.

Otherwise, such Scheme Entitlements are kept in the Settlement Trust until, if and when an Account Holder Letter is received C.

The rights, title and interest of the Existing Noteholders, in respect of the Existing Notes are transferred to/written up in the name of the New Issuer at Euroclear/Clearstream, and the Scheme Claims as between the Scheme Company and Existing Noteholders are satisfied and released153C87642A93B2B New issuer (Bermuda)3A Corporate structure chartRHL (BVI)RTL (Bermuda) New Issuer (Bermuda)RSC (Russia)RSB (Russia) Scheme Company (Luxembourg)RSI (Russia) Existing Noteholders 99.999% 9.1% (direct) Existing Subordinated Loans 90.8% (direct) 14.5% (direct) 85.5% (direct) 100% (direct) 100% (direct) Existing Notes20