Экономика

ЭкономикаПохожие презентации:

(ge) and World Economic Relations (WER)")

")

Profit repatriation in Сhina

1. PROFIT REPATRIATION IN CHINA

1PROFIT

REPATRIATION IN

CHINA

Бизнес и предпринимательство в

странах Азии 2017

Сучкова Александра, Намсараева

Норжима, Птичкина Анастасия

2. For foreign companies with subsidiaries in China, repatriating profit from their subsidiaries has always been an important and

2For foreign companies

with subsidiaries in China,

repatriating profit from

their subsidiaries has

always been an important

and challenging issue

China maintains a strict system of foreign

exchange controls, meaning funds flowing into

and out of China are tightly regulated.

It is important for foreign investors to

incorporate a profit repatriation strategy into

the set-up planning of a subsidiary in China to

ensure its ability to access the profits earned

and to achieve significant cost savings.

3. WAYS TO REPATRIATE PROFIT FROM CHINA

31. Company’s China-based entity pays dividends

WAYS TO

REPATRIATE

PROFIT FROM

CHINA

directly to its foreign parent company.

BUT: only profits that have undergone annual audit

can be repatriated, and the gross profit will be

subject to 25 percent CIT (Corporate Income Tax).

Dividends are subject to a further 10 percent

withholding CIT when distributed to foreign

investors.

4. WAYS TO REPATRIATE PROFIT FROM CHINA

4WAYS TO REPATRIATE PROFIT FROM CHINA

FIE (Foreign Invested Enterprise) can only

distribute dividends out of its accumulated

profits (and its prior accumulated losses

must be more than offset by its profits in

other years, including the current year).

An FIE its prior accumulated losses must

be more than offset by its profits in other

years, including the current year

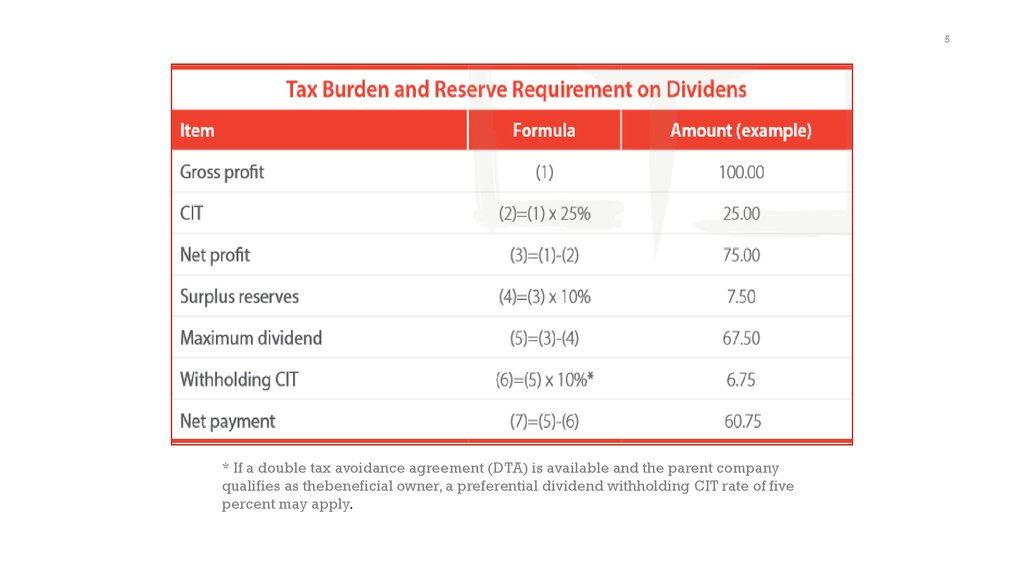

5.

5* If a double tax avoidance agreement (DTA) is available and the parent company

qualifies as thebeneficial owner, a preferential dividend withholding CIT rate of five

percent may apply.

6.

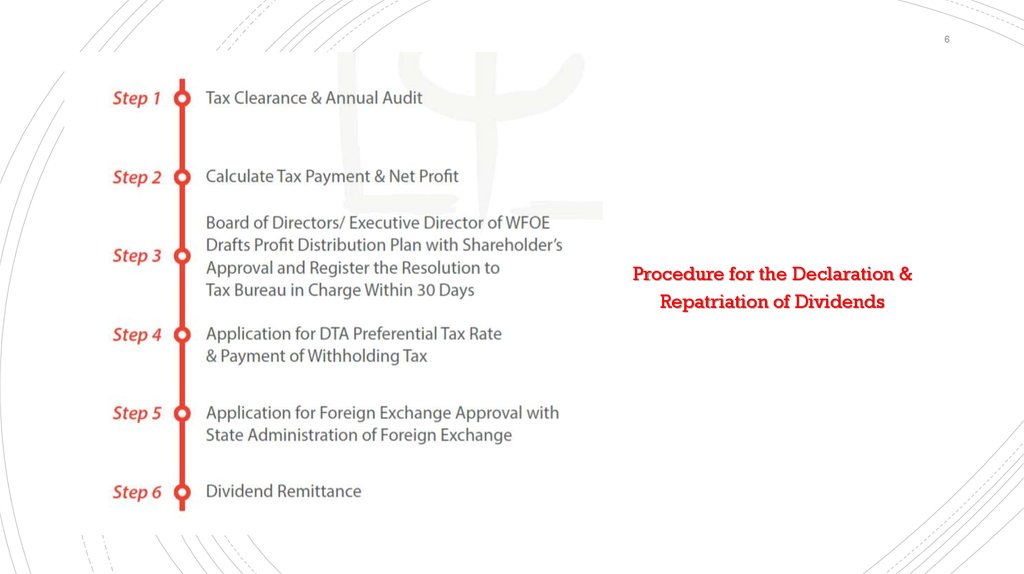

6Procedure for the Declaration &

Repatriation of Dividends

7.

7Many multinational corporations

have adopted certain implicit

policies, such as minimizing their

profits in China in a legitimate

manner

via

intercompany

payments (i.e. charging their

Chinese entity royalty or service

fees);

These transactions will be subject

to turnover tax, and possible

withholding

CIT

(Corporate

Income Tax), the fees

are deductible from the CIT taxable

income and thus are exempt from

the 25 percent CIT, resulting

in significant cost savings.

8. Service fees

8Service fees

9.

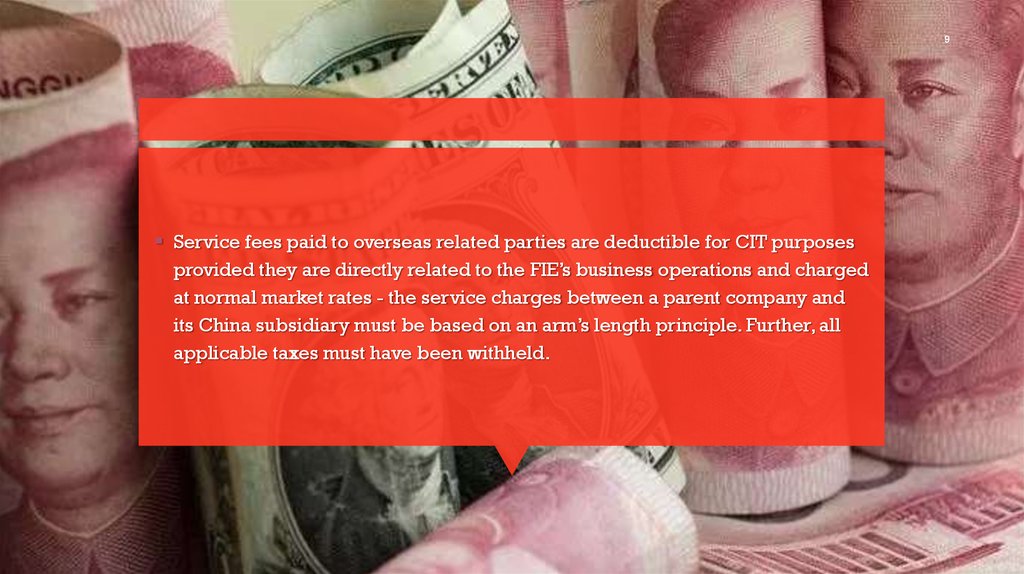

9Service fees paid to overseas related parties are deductible for CIT purposes

provided they are directly related to the FIE’s business operations and charged

at normal market rates - the service charges between a parent company and

its China subsidiary must be based on an arm’s length principle. Further, all

applicable taxes must have been withheld.

10. service fees are subject to:

10service fees are

subject to:

VAT (Value-Added Tax);

construction and maintenance tax (UCMT);

education surcharge (ES);

local education surcharge (LES);

The parent company is liable for these taxes.

The China subsidiary is responsible for withholding and

paying these taxes.

11.

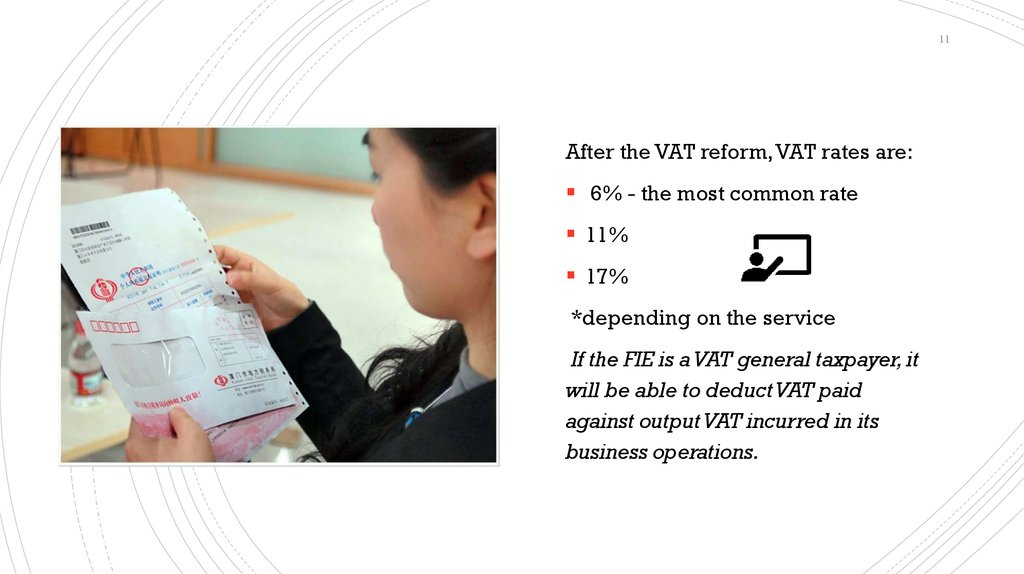

11After the VAT reform, VAT rates are:

6% - the most common rate

11%

17%

*depending on the service

If the FIE is a VAT general taxpayer, it

will be able to deduct VAT paid

against output VAT incurred in its

business operations.

12.

12Services rendered outside China are exempt from CIT (but are

still subject to VAT). The Chinese company should specify the

offshore services that it received in the relevant service

agreements and be prepared to clarify the nature of the services.

If the services are (or deemed to be) provided in China, the

service fees will be subject to CIT at 25% on the deemed profit

rate of 15-50%, unless a CIT exemption applies under a DTA.

13.

13Under most DTAs signed between

China and other countries/regions,

the provision of services in China by a

foreign enterprise overseas will,

constitute a permanen; establishment

(PE) if such activities continue for a

period of more than 183 days within

any 12-month period;

If the headquarter (HQ) is deemed to

have a PE in China, a 25 percent CIT is

payable on the service income;

Tax compliance burden for a PE is

heavier than for a non-PE;

the Chinese subsidiary and HQ should

carefully manage contracts and related

projects in China.

14. It is important to note that the tax officer always has the right to call into question the legitimacy of a service agreement.

14It is important to note that the tax officer always has the right to call into question the legitimacy of a service

agreement. The taxpayer should be prepared to provide further evidence, including a detailed service

agreement to clarify the nature of the services provided.

你有钱吗?

15. ROYALTY REMITTANCES

15Royalties are fees paid in relation to the use of intellectual

property, such as trademarks, patents, copyrights, and

proprietary technology;

Royalties are deductible for CIT purposes provided they are

directly related to the FIE’s business operations and charged at

normal market rates;

ROYALTY

REMITTANCES

The statutory CIT withholding tax rate

of 10% can be reduced to a lower rate

Royalty remittances are subject to a 10% withholding CIT and

6% VAT, as well as UCMT, ES, and LES;

The royalty remittance process is similar to remitting service

fees, with a key difference: royalty agreement must be registered

with the trademark bureau.

16. When services fees are deemed to be royalties

16When services

fees are deemed

to be royalties

The Notice of the State Administration of Taxation on Issues

Relevant to the Execution of the Royalty Clauses of Tax

Treaties (Guo Shui Han [2009] No. 507), where the service

provider uses certain expertise and technologies in the

provision of services under a service contract, but does not

transfer or license such technologies, then such services

shall not fall under the scope of royalties.

The results of the provision of services fall under the scope

of definition of royalties under a DTA (Direct Transfer

Agreement) then the service recipient shall merely have use

rights for such results and the service fees derived shall be

deemed as royalties.

17.

17If, in the course of the

transfer or licensing of

technical know-how, a

licensor assigns personnel

to support and guide the

licensee, then these service

fees will be deemed as

royalty fees.

Accordingly, even if these

services are provided

offshore, they will be

subject to VAT in addition

to 10% CIT withholding

tax.

18. LOANS

18LOANS

A WFOE (Wholly Foreign-Owned Enterprise)

may also remit undistributed profits to a foreign

related company with which it has an equity

relationship by extending a loan. The WFOE’s

interest income will be subject to 25% CIT and

6% VAT, although the CIT paid in China may

later be used to offset tax liability incurred in the

foreign country if there is a DTA in place;

Repatriating funds through an offshore loan has

traditionally not been very common because of

the intricate remittance procedure and

repayment issues.

19. WFOEs may now apply for longer-term offshore loans according to their business needs.

19The situation has changed since

WFOEs may now apply for

longer-term offshore

loans according to their

business needs.

the promulgation of the Hui Fa

[2014] No.2 (Circular 2) by SAFE

in January 2014. Under Circular

2, offshore lending is limited to

30% of the owner’s equity

in a Chinese WFOE unless

special approval has been

obtained from SAFE.

20. References

20References

Tax, Accounting and Audit in China, 2017 (9th

Edition). Ltd, Asia Briefing 2017. pp. 100-107.

21. Thank you for your attention!

21Thank you for your

attention!