Финансы

Финансы Английский язык

Английский языкПохожие презентации:

Accounting principles and concepts

1.

Государственный комитет Российской Федерации по рыболовствуКамчатский государственный технический университет

Кафедра иностранных языков

АНГЛИЙСКИЙ ЯЗЫК

Сборник текстов и упражнений

для студентов специальности 060500

"Бухгалтерский учет, анализ и аудит"

Петропавловск-Камчатский 2003

2.

УДК 4И (Англ)ББК 81.2 (Англ)

Г95

Рецензент:

Н.П. Дьякова,

доцент кафедры иностранных языков

Гурская Т. А.

Г95

Английский язык. Сборник текстов и упражнений для студентов

специальности 060500 "Бухгалтерский учет, анализ и аудит". –

Петропавловск-Камчатский: КамчатГТУ, 2003. – 39 с.

Методические указания составлены в соответствии с требованиями

к обязательному минимуму содержания основной образовательной

программы подготовки специалиста по специальности 060500 "Бухгалтерский учет, анализ и аудит" государственного образовательного стандарта

высшего профессионального образования.

Рекомендовано к изданию решением ученого совета КамчатГТУ

(протокол № 6 от 18 апреля 2003 г.).

УДК 4И (Англ)

ББК 81.2 (Англ)

© КамчатГТУ, 2003

© Гурская Т.А., 2003

2

3.

I. ACCOUNTING1. ACCOUNTING PRINCIPLES AND CONCEPTS

Vocabulary list

accounting

to a significant extent

phase

capture

processing

communication

recording

book-keeping

record

at a profit

to meet one's commitments

to fall

accounting equation

assets

liabilities

owner's equity

financial statements

balance sheet

income statement

profit and loss account

double-entry book-keeping

entry

account

cash basis

accrual basis

debit

debit side

credit

credit side

бухгалтерский учет

в значительной степени

стадия, фаза

(зд.) получение (информации)

обработка (информации)

передача (информации)

запись (информации)

счетоводство

запись, записывать, отражать в отчетности

с прибылью

выполнять обязательства

dueнаступать (об обязательствах), подлежать

оплате, подлежать выполнению

бухгалтерское равенство

активы

пассивы

собственный (акционерный)

капитал компании

финансовая отчетность

балансовый отчет, баланс

отчет о прибылях и убытках

счет прибылей и убытков

бухгалтерский учет по методу двойной записи

запись, проводка

счет

метод записи доходов и издержек на счетах

только при их поступлении и выплате,

кассовая база

метод вычислений при учете доходов

и издержек, запись доходов и издержек

в момент завершения операции

дебет

левая сторона баланса, дебет счета

кредит

правая сторона баланса, кредит счета

3

4.

TEXTAn accounting system in a given country is one of the key elements of the economic system. It is determined to a significant extent by the level and direction of the

economic system's development.

The most important theoretical concept of the Anglo-American accounting may be

summed up as follows: the subject of accounting is the calculation of the financial results of an economic entity's business activity.

Accounting is used to describe the transactions entered into by all kinds of organizations.

Accounting can be divided into three phases: capture, processing and communication of financial information.

The first phase, the process of capturing financial information and recording it,

is called book-keeping. Accounting extends far beyond the actual making of records. It

includes their analysis and interpretation, it shows the relationship between the financial results and events, which have created them.

Accounting can show the managers or owners of a business whether or not the

business is operating at a profit, whether or not the business will be able to meet the

commitments as they fall due.

Accounting is based on the accounting equation, which states that a firm's assets

must equal its liabilities plus its owners' equity.

Assets and liabilities, profits and losses are listed in financial statements. The two

main types of financial statements are the balance sheet and the income statement

(profit and loss account).

The balance sheet lists a firm's assets, liabilities and owner's equity at a point of time.

Changes in the balance sheet are made according to the principle of double-entry

book-keeping. This principle states that each transaction must be recorded on the balance sheet as two separate entries so that the totals of each side will always equal one

another, and that this will always be true no matter;how many transactions are entered

into.

Balance sheets are diawn up periodically: monthly, quarterly, half-yearly, annually.

There is an account for every asset, every liability and capital. Accounts can be

prepared either on a cash or accrual basis. Each account should be shown on a separate page.

The double entry system divides each page into two halves. The left-hand side is

called the debit side, while the right-hand side is called the credit side.

The balance sheet shows a lot of useful financial information, but it does not show

everything. A firm's sales, costs, and profits for a given period are shown in an income statement.

Answer the questions on the text:

1. What role does an accounting system play in an economy?

2. Into what phases is accounting broken down?

3. What is an accounting equation?

4

5.

4. What is the most widely practised principle of book-keeping?5. What does the balance sheet list?

6. What is shown in the income statement?

Find English equivalents for the following Russian phrases from the text:

ключевой элемент экономической системы; финансовые результаты хозяйственной деятельности хозяйствующего субъекта; сделки, в которые вступают

различные организации; получение, обработка и передача информации; отражение информации в финансовой отчетности; работать с прибылью; выполнять

свои обязательства; бухгалтерское равенство; активы должны быть равны пассивам; в балансе отражаются ... ; учет по принципу двойной записи; отражать

в балансе, составлять баланс; счет прибылей и убытков.

Say in a few words what the text is about. Use the following opening phrases:

The text looks at (the problem of...)...;

The text deals with the issue of...;

It is clear from the text that...;

Among other things the text raises the issue of...;

The problem of ... is of great importance. One of the main points to be single out is ...;

Great importance is also attached to ...;

In this connection, I'd like to say ...;

It further says that ..;

I find the question of... very important because ...;

We shouldn't forget that...;

I think that ... should be mentioned here as a very important mechanism of... .

2. ACCOUNTANCY IN A FREE-MARKET ECONOMY

Vocabulary list

Accountancy

Performance

economic status

managerial

outside user

financial accounting

going-concern basis

assumption

economic substance

relevance

timeliness

prudence

reliability

бухгалтерский учет

показатели деятельности, результаты работы

экономическое положение

accounting управленческий учет

внешний пользователь

финансовый учет

принцип работающего предприятия

посыл, предположение, допущение

экономическая сущность

релевантность

своевременность

предусмотрительность

надежность

5

6.

materialityconsistency

comparability

harmonize

материальность, существенность

неизменность, преемственность

сравнимость, сопоставимость

гармонизировать, сближать

TEXT

In a free-market environment, accounting provides a means for transmitting information about the performance of enterprises to those with an interest in it.

The basic functions of accounting in a market economy are to measure economic

activity of an enterprise and its profit, to show changes in its financial position and

ensure that a fair report of the economic status and performance is made available

to all those concerned. These functions are performed at two different levels.

The accountants in the US communicate financial information to many people.

What users need financial information?

One branch of accounting, called managerial accounting, provides information that

managers use in making decisions within the firm. Other accountants prepare financial

reports for outside users. This branch of accounting is known QS financial accounting.

American accounting standards and objectives of financial statements fully meet

the users' needs for useful information. The following basic principles ensure the provision of such information in the manner the market requires. First of all, accounts

must be prepared on a going-concern basis. It means accounting is based on the assumption that the business will continue to operate. Besides, accounts must reflect the

economic substance of the situation rather than simply its legal form. Other characteristics that make information useful for the users are relevance, timeliness, prudence,

reliability, materiality, consistency and comparability.

Though these concepts are recognized internationally, users of information often fail

to get a true and fair view of business operations. In the present conditions, there is need

to work harder to harmonize national accounting systems so as to make it easier for users

to assess financial information, particularly taking into account growth of transnational

corporations and increasing interdependence of financial markets.

Answer the questions on the text:

1. What is the role and functions of accountancy in a free-market economy?

2. Who uses financial information?

3. What are the major objectives of financial statements?

4. What is "useful" information for users?

Find English equivalents for the following Russian phrases from the text:

передавать информацию; измерять; изменения в финансовом положении

предприятия; финансовый учет; управленческий учет; цели финансовой отчетности; принцип работающего предприятия; экономическая сущность; давать истинное представление о деятельности фирмы; сближать принципы учета.

Say in a few words what the text is about. Use the opening phrases given above.

6

7.

3. PUBLIC AND PRIVATE ACCOUNTANTSVocabulary List

public accountant

private accountant

practise

judgement

certified public accountant

holder of a license

be authorized

to grant a license

state government

to keep knowledge up to date

integrity

confidentiality

to be held in low esteem

to have much in common

auditing

consulting services

tax planning

cost accounting

capital budgeting

budgeting for current

financial information system

professional body

частнопрактикующий (лицензированный)

бухгалтер

бухгалтер, действующий в пределах

одной фирмы

иметь частную практику

мнение, суждение

дипломированный частнопрактикующий

бухгалтер

владелец (держатель) лицензии

иметь право, быть уполномоченным

предоставлять лицензию

правительство штата

поддерживать знания на современном уровне

(зд.) высокая профессиональная репутация

конфиденциальность

не пользоваться уважением

иметь много общего

аудит

консультационные услуги

планирование налогообложения

производственный учет

составление смет капитальных расходов

operations составление смет текущих расходов

финансовая информационная система

профессиональная организация

TEXT

The accounting profession in the market economy consists of public and private accountants. Public accountants are independent professionals who provide services for a fee.

Accountants who are employed by business firms are known as private accountants.

The main form of business organization in the accounting profession is partnership, though some public accountants practise alone and the others have formed professional corporations. Public accountants try to avoid limited liability, because they

believe that professionals should take full responsibility for their judgements.

The title certified public accountant refers to the holder of a license to practise

public accounting. The license is granted by a state government. It is granted to people

who meet educational and experience requirements and pass an examination. All American certified public accountants are expected to keep their knowledge up to date and to

7

8.

maintain the highest standard of integrity, professional independence and confidentiality.In Russia accountants also try and do their best to keep up high professional standards. For many years they were held in a very low esteem in the country, now the

situation is changing for the better. Public accountants in Russia offer different services. The main service is auditing. Besides, public accounting firms offer consulting

services, some accountants are also active in tax planning and preparation of tax returns. Russian and American public accountants have much in common.

The work of private accountants in Russia differs greatly from what American accountants employed by business firms do because Russia is only entering a market

economy.

Accountants who work for the US business firms have wide responsibilities. Their

duties include cost accounting, capital budgeting for current operations, tax planning,

they must know how to design financial information systems, and do may other

things.

Answer the questions on the text:

1. What are public accountants?

2. What are private accountants?

3. How do public accountants organize their activities?

4. Who can get a license to practise public accounting?

5. What services do Russian public accountants provide?

Find English equivalents for the following Russian phrases from the text:

заниматься чем-либо; предоставлять услуги на платной основе; организовать

товарищество; избегать ограниченной ответственности;

брать на себя ответственность за свои решения; иметь право выдавать лицензию; удовлетворять требованиям в отношении уровня образования и опыта

работы; сдать экзамен; профессиональная репутация; конфиденциальность;

поддерживать высокие профессиональные стандарты; аудит; иметь много общего; отличаться в значительной степени;

производственный учет; составление смет капитальных расходов; составление смет текущих расходов.

Say in a few words what the text is about Use the opening phrases given above.

4. EXERCISES

Work on vocabulary and grammar

Exercise 1.

a) Study the key words in the dictionary:

Balance sheet, account, depreciation, cost, expenses, assets, loss.

b) Think of the words describing characteristics that make information useful.

8

9.

c) Think of the nouns that are most often used with the following verbs:to measure, to ensure, to communicate, to prepare, to debit, to credit, to draw up,

to disclose, to report.

d) Match the verbs from (1) with the nouns from (2) below:

1) to meet

2)

needs

to ensure

provision of information

to harmonize

standards

to develop

performance

to assess

service

to provide

license

to grant

accounting standards

Exercise 2.

a) Supply the articles where necessary.

b) Write down 3-5 questions on the text.

c) Explain what information must be disclosed in the accounting records. Say what

you have learned from the text about the UK rules for the preparation of accounting

records.

Accounting Records

Every company must keep accounting records sufficient:

- to show and explain ... company's transactions;

- to disclose ... financial position of the company at any time with reasonable

accuracy;

- to enable the directors to ensure that... annual accounts comply with ... statutory

requirements.

The records may contain entries of daily receipts and payments,... record of assets

and liabilities and, where the business involves dealing in goods, stocktaking records

and details of goods bought and sold.

The directors of every company have a duty to prepare annual accounts. The accounts must be made up to .. .company's accounting date (its financial year-end)

and in accordance with the specified accounting principles. In ... UK, for example,

they include ... following:

- The company is presumed to be ... going concern.

- Accounting policies are applied consistently from ... year to year.

- The amount of any item is determined on ... prudent basis.

- The accounts are prepared on ... accrual basis.

Details of any departure from these principles, the reasons for it, and its effect

must be explained in ... note to the accounts.

In ... UK company accounts are almost invariably prepared using the historical

cost accounting convention, with or without modification to reflect changes in ... value of certain assets. However, ... Company Act 1985 provides alternative accounting

rules which permit company to recognize ... full impact of inflation and changing

prices in their accounts.

9

10.

Along with ... rules applying to the preparation of accounts, there is ... overridingrequirement that the balance sheet must give ... "true and fair" view of the state of affairs of the company and that... profit and less account must give ... "true and fair"

view of the company's profit and loss.

Until 1992, cash basis accounting was ... only method recognized in ... Russia. Although the new accounting regulation permits the administration to select... method of

recognized revenue and expenses,... traditional methods is sill dominant.

Words you may need:

accounting records

stocktaking records

accounting date

accrual basis

departure

Companies Act

overriding

бухгалтерские счета, бухгалтерская отчетность

книга учета запасов

отчетная дата

принцип начислений

(зд.) отклонение

Закон о компаниях

первостепенный

Exercise 3.

a) Open the brackets putting the verbs in the correct form.

b) Say what is a Chart of Accounts in Russia and what it provides for.

In the West each company (to have) a certain freedom in the design of its own set

of accounts so as to reflect the nature of its business and the needs of its management

in directing that business. In Russia this process (to regulate) centrally, there (to be) a

tradition of using a uniform Chart of Accounts.

The first uniform Chart of Accounts (to appear) in Russia in the 1920s. It (to intend)

for industries only and was revised periodically. In 1961 the first national uniform Chart

of Accounts (to create) and put into operation. With only insignificant changes, this

chart (to use) in accounting practice until 1992. In 1992 transition to a new chart (to

make). The current Chart of Accounts (to consist) of about 100 accounts and 60 subaccounts grouped into 10 main sections. All accounts included in this uniform chart

(to call) "synthetic" (main or summary) accounts. On the basis of this chart, each enterprise also may create a set of "analytic" (supporting) accounts if needed to supplement the synthetic accounts. The Chart of Accounts can be considered the most important element of the accounting system in Russia because it (to determine) the

accounting practice and other elements of the system.

The Chart (to provide) for the following: an interrelated classification, grouping,

and generalization of information about business activities of enterprises, a unified

methodological basis for the organization of accounting in the whole national economy, an effective system of control of indicators for business activities, comparability

of accounting procedures used and information generated in the accounting systems

of different enterprises, etc.

10

11.

Words you may need:Chart of Accounts

set of accounts

план счетов

перечень счетов

Exercise 4.

a) Fill each gap with a suitable word from the box.

b) Sum up the text in 5-7 sentences and present your summary in class.

c) Name the most important events in the development of the accountancy profession in the world.

accountants principles

organized members

Back profession

creation throughout

Number role

organizations functions

Accountancy Profession

The organization of the accountancy profession dates __ to January 1853 when

eight accountants in Edinburgh, Scotland met for the purpose of seeking recognition

of their __ as a separate and distinct profession. Their discussion of their professional

situation resulted in the __ of the Institute of Chartered Accountants of Edinburgh.

Since that time numerous professional accountancy organizations have been established __ the world. The process is going on.

In 1977 the International Federation of Accountants (IFAC) was established.

Its initial membership was 63 organizations representing 49 countries, but within

a decade, the __ grew to 105 organizations from 79 countries. The establishment of

the IFAC recognized the need for international coordination of the objectives of professional accountancy organizations and means of achieving those objectives.

Accountancy is an international profession. Under the conditions of global interdependence of countries through trade, finance, and crossborder investments, the __ of

the IFAC is becoming more important.

The size and principles of accountancy __ vary. Some organizations comprise accountants working in commerce, industry, and government organizations, as well as

in public practice (auditing), others consist solely of members in public practice.

The main follows:

of the accountancy profession may be summarized as

- to protect the public by ensuring the observance by its members of

the highest __ of professional and ethical conduct;

- to promote and increase the knowledge, skills, and proficiency of members

of the organization and students;

- to preserve the professional independence of __ in whatever capacities they

may be serving;

- to maintain the legitimate rights of its __. IFAC was __ in recognition of the growing changes towards inter-nationalization of the world economy, business and trade.

11

12.

Words you may need:Institute of Chartered Accountants

proficiency

Институт дипломированных бухгалтеров

(зд.) опыт

Exercise 5.

Read the dialogue, translate the Russian remarks into English and act it out:

Foreigner: As far as I know, in the past the major function of your accountants

was to control whether enterprises achieved the plan targets. Has the accounting system changed of late?

Russian: Политика экономических реформ вызвала необходимость создания

эффективной системы бухучета. В этом направлении уже проделана большая

работа.

F.: What accounting principles is your system based on at present?

R.: Наша система учета основана на системе двойной записи. Учет в основном ведется на основе кассового принципа учета.

F.: Your system seems to be formalized. It is based on the uniform chart ofaccounts

(план счетов) and forms of record keeping and reporting (формы учета и отчетности).

R.: Стремясь способствовать прямым иностранным инвестициям путем создания совместных предприятий, наше правительство поставило задачу внедрения системы учета, сопоставимой с международными стандартами. Была разработана процедура составления ежегодной финансовой отчетности, одобрен план

счетов для совместных предприятий.

F.: It is also important to recognize that the development of accounting in any

country is impossible without developing the accounting profession. Is anything being

done in this direction?

R.: Да, мы разрабатываем и внедряем новые стандарты, организуем профессиональную подготовку и переподготовку бухгалтеров.

F.: 1 am glad to hear that the full potential of accounting is appreciated in your

country now.

5. DISCUSSION

Exercise 6.

a) Read the texts aud single out the main facts.

b) Present them in a short review and compare the information and viewpoints

in Text (1) and Text (2).

Text (1)

For many years the accounting system in Russia was criticized by Western academicians for its failure to adhere to Western accounting principles. Such criticism

is no longer valid. Since the early 1990s, accounting in the Russian Federation has

changed significantly.

12

13.

The year 1991 was crucial in accounting development in Russia due to the following three events:– Publication of the new Chart of Accounts;

– Production of a new set of financial statements similar to those used in Western Accounting;

– Beginning of preparations for radical change in accounting and auditing regulation.

In 1992, Regulation on Accounting and Reporting in the Russian Federation was

approved by decree of the Government of Russia. The document diminished the control function of accounting and declared the following equal objectives of accounting:

1. Maintenance of control over the availability, movement, and use of material,

manpower and monetary resources according to approved norms and estimates;

2. Provision of full and reliable information about the performance and financial

results of an enterprise, which is indispensable for operational management as well as

for investors, suppliers, customers and creditors, tax, financial, and bank authorities,

and others interested in the financial and business activity of the enterprise.

An essentially new Russian accounting system has come into being with the introduction of the new Chart of Accounts which includes greater cohesion to international

accounting norms.

The essential elements of accounting methodology are as follows:

– Documents form the legal foundation for recording transactions according to

the approved rules of bookkeeping. No entry should be made unless the bookkeeper

has the primary document.

– Taking inventory is the sole means of controlling the physical safety of assets

and their valuation. It is the main method of supervising persons who are financially

responsible for assets. The safeguarding of assets is always entrusted to a financially

responsible person.

– The uniform Chart of Accounts, which provides the nomenclature of accounts

and correspondence among them, must be used by all types of enterprises.

– Double entry is a traditional accounting concept that is accepted in Russia as it is

in all developed countries.

– Internal reporting includes the general ledger, summary (principal) account

registers, primary documents, inventory data, etc. External reporting includes the Balance Sheet, Statement of Financial Results and Their Uses, and supplemental forms

that are uniform and obligatory for all types of enterprises. Nonprofit organizations

and banks have their own uniform charts of accounts and financial reporting forms.

Reporting is carried out according to the statutory regulation and presented within

strictly prescribed time limits.

– Information generated by the accounting system must be timely, reliable, full,

accurate, and objective.

– Historical cost accounting is the only method of internal and external reporting

permitted.

13

14.

Words you may need:primary document

taking inventory

sole

financially responsible person

nomenclature

correspondence

internal reporting

general ledger

summary account register

inventory data

external reporting

Statement of Financial Results

and Their Uses

financial reporting form

historical cost accounting

первичный документ

инвентаризация

единственный

материально-ответственное лицо

номенклатура (перечень наименований)

корреспонденция (счетов)

внутренняя отчетность

главная бухгалтерская книга

сводный журнал

инвентарные данные

внешняя отчетность

Отчет о финансовых результатах

и их использовании

бланк финансовой отчетности

учет на основе стоимости приобретения

Text (2)

From the international perspective, it is important to remember that while based on

similar principles, Russian accounting does not fully meet international accounting

standards (IAS). The main differences are as follows:

– Sales are usually recorded on a cash basis. The cost of goods/services delivered but not yet paid for remains on the balance slieet until payment is received.

Most Russian taxes are sales-based. As a result, companies try to minimize sales in

their accounts. When sales are recorded on a cash basis, allowances are not made for

bad debt, in spite of the fact that bad debts may represent a considerable share of accounts receivable. Sales figures for Russian companies tend to be understated compared with the accrual sales of Western companies.

– Cost of goods sold. Russian companies report the full cost goods sold, which

includes production costs, transportation, depreciation, marketing, and financial expenses. No cost items are disclosed separately. Social costs are not included in the

cost of goods sold.

– Depreciation. Only a straight-line depreciation method is allowed. The depreciation rates are fixed by the government and are as a rule significantly lower than in

the West. Accelerated straight-line depreciation has been permitted since January 1,

1995 but is still rarely used.

– Fixed assets. Fixed assets pose the most serious problem. Fixed assets are accounted for a historical cost and cover property, plant and equipment. Land is not

treated as a fixed asset and does not appear on the balance sheet at all. Even if depreciation rates are lower than in the West, fixed assets are generally undervalued compared with Western practice.

– Accounts receivable. Since most Russian companies record sales when they

receive payment, the sales margin is not accrued until that time. Therefore accounts

14

15.

receivable are understated given that the sales margin is not reflected. Overdue accounts receivable are not disclosed separately.– Consolidation of accounts. Russian companies, including holding companies,

are not required to submit consolidated reports. No consolidation standards have been

established yet. Some of the holding companies prepare aggregated reports, summing

up 100 % of all subsidiaries and associates without accounting for intragroup transactions and minorities. Consequently, the reported results of Russian holding companies

are usually significantly overstated.

All other aspects of Russian accounting are basically in line with IAS. The Russian

government is taking measures to eliminate the most serious divergences.

Words you may need:

bad debts

accounts receivable

straight-line depreciation method

accelerated straight-line

depreciation method

sales margin

overdue

consolidation of accounts

IAS – international accounting standards

divergence

безнадежные долги

дебиторская задолженность

метод равномерного

начисления износа

метод ускоренного

начисления износа

доход от продаж

просроченный

консолидация счетов

международный бухгалтерский

стандарт

отклонение

Exercise 7.

Read the dialogue, sum the its content using the phrases given below and act it out:

The dialogue is about ...;

According to the dialogue ...;

The experts make it clear that... (stress the point that...; draw the attention of...

to the fact that...; suggest, remind, promise);

Finally, the experts come to the conclusion that... (agree about...).

6. ACCOUNTING METHODS

American: Accounting is a kind of data processing and recording. In my country

it's usually the accountant who decides on the form which this recording shall take

and on the methods to be used.

Russian: Do you mean that in writing financial statements for stockholders and

lenders accountants can make the firm look strong and healthy and when preparing

tax returns, on the other hand, they can make the firm look poor and weak?

Am.: Accountants prepare financial statements according to rules set by law and

15

16.

by the accounting profession itself. Often the rules allow more than one way of reporting information.R.: Accounts can be kept on an accrual or a cash basis. How do the two methods

differ in real life?

Am.: Firms that keep their accounts on an accrual basis report costs and revenues

in the year in which sales are made even if the customers do not pay until later. Those

that keep their accounts on a cash basis report costs and revenues in the year in which

payment is made.

R.: I know that each method has its pros and cons. But how does each method affect the way the outside users of the income statement and the balance sheet see

the image of the company?

Am.: The accrual basis matches the income statement more closely to the balance sheet and accrual basis accounts show rapidly rising income. But little

of the income is cash!

R.: What is more, the accrual basis assumes that all accounts receivable will be

collected, but in reality some may not.

Am.: For these reasons, some people think the cash. basis is a more prudent way

to draw up an income statement. Accountants have also to decide how to determine

the monetary value of an item included in a financial statement.

R.: What problems can arise here?

Am.: Assets can be recorded at the amount of cash paid to acquire them at me

time of their acquisition.

R.: At the historical cost, in other words.

Am.: Yes. In addition, current, replacement cost and net realizable value can be used.

R.: Are goods held in inventory another problem area?

Am.: Yes, there are two ways of dealing with inventories. One is FIFO,

theother is LIFO.

R.: Theoretically, I believe, we can argue in favour of both methods. Whichworks

better in real life?

Am.: In recent years many firms have switched from FIFO to LIFO.

R.: Do you have an explanation?

Am.: Yes. During periods of inflation, LIFO results in a higher cost of goods and,

hence, a lower reported income. As a result a firm that uses LIFO pays less income tax.

Words you may need:

accounting method

cash basis monetary

value of an item

current replacement cost

net realizable cost

inventories

FIFO

LIFO

16

метод учета

метод записи доходов и издержек на счетах

только при их поступлении и выплате; кассовая база

стоимость операции {статьи в балансе)

в денежном выражении

чистая (потенциальная) стоимость реализации

товарно-материальные запасы

«первая партия в приход – первая в расход»

«последняя партия в приход – первая в расход»

17.

Exercise 8.Give extensive answers to these discussion questions:

1. What is the role of accountancy in a free-market economy?

2. What is managerial accounting?

3. Who needs the information provided in financial statements?

4. How are accountants classified in Russia?

5. What services do public accountants offer their clients?

6. What is done in this country to create a strong and respected professional

body of accountants?

7. What accounting system is most widely practised in the world?

8. In what way does cash basis accounting differ from accounting on accrual basis?

9. What do you think of the problem of harmonizing national accounting standards?

Exercise 9.

Write a short paragraph, explaining:

a) What accounting is and what role it plays in a free-market economy.

b) What sort of statement the balance sheet is.

c) What sort of statement the income statement is.

d) The difference between the two branches of accounting.

e) Accounting principles.

f) The functions of the Chart of Accounts.

Exercise 10

Prepare a short talk on the following:

a) The work of public accountants, private accountants, and accountants who

work for units of the government and non-for-profit firms firms.

b) Why do all firms need both fixed and working capital?

c) How is Russian accounting developing? Do any of the Big Eight have offices

in Russia?

d) What are your own sources of funds? Earnings from employment? Contributions from parents or others?

e) If you are a student, describe the fixed capital and working capital of your university. List some fixed assets that it owns.

Exercise 11.

A company needs the chief accountant, who will:

– maintain accounts payable ledger;

– supervise banking and cash activities, supply contracts, reconciliation of bank

statements;

– deal with local tax authorities;

– work directly with the CFO (chief financial officer – старшее должностное

лицо по финансовым вопросам, главный сотрудник по финансовым вопросам);

– supervise the accounting department;

– cooperate with internal and external auditors.

17

18.

The requirements include:– excellent English;

– degree in accounting;

– knowledge of the Russian accounting system;

– familiarity with GAAP (generally accepted accounting principles – общепринятые принципы бухгалтерского учета);

– proper computer skills;

– ability to work independently.

Do many applicants stand a good chance?

Reading practice

Exercise 11.

Read the text that follows to find the answers to the following questions:

– What financial document presents the position of the enterprise?

– What can assets include?

– What can liabilities include?

– What is equity?

– What financial document measures the performance of the enterprise?

7. FINANCIAL STATEMENTS AND THEIR ELEMENTS

A. Balance sheet

The position of the enterprise is presented in the balance sheet. That statement

shows resources and the claims to or interests in them and provides an indication of

the financial strength of the enterprise.

The balance sheet includes the following elements:

Assets

Assets include property, plant and equipment, financial leases, investments in subsidiaries and other enterprises; long-term receivables; purchased goodwill, patents,

trade marks and similar intangibles; marketable securities;

current receivables (or trade debts); inventories; cash and bank balances; and prepaid expenses.

Assets arise from past events, which may be cash or non-cash transactions. Assets

may be purchased, exchanged for other assets, self-generated or received as grants or

donations.

An asset is recognized when it is reasonably certain that the future economic benefit embodied in it will flow to the enterprise.

In a number of countries, intangible assets such concessions, patents, licenses,

trade marks and similar rights and assets may be recognized in the balance sheet only

if they were acquired for a valuable consideration. A number of countries allow assets

to be carried on the balance sheet only if the reporting enterprise is the legal owner.

18

19.

LiabilitiesLiabilities include long-term loans and debentures, short-term loans, and bank

overdrafts, payables, pension plans and similar financial obligations. The scope of definition of liabilities covers obligations whose financial amounts can or cannot be established precisely. It therefore covers what is usually described as provisions in some

countries. Provisions are liabilities, the amount of which cannot be established precisely, or the occurrence of which is uncertain. In some countries, provisions may not

be used to adjust the value of assets. In those countries, value adjustments on debtors

are referred to as write-downs. In other countries, write-downs on debtors are commonly referred to as provisions. Provisions should be distinguished from .reserves,

which are amounts set aside under equity for future use with respect to obligations

which may arise from probable or possible events.

A liability is recognized when it is reasonably certain that a future reduction in

economic benefit will result from the settlement of the obligation.

Equity

Paid-in capital is treated differently in many countries, in some of which all

amounts paid in by equity shareholders are classified as paid-in and are not further categorized. In other countries, paid-in capital is divisible into two types: that relating to

the par value of the shares offered for sale and that relating to share premium or additional capital. In consolidated balance sheets, the amount of equity should be given separately for the shareholders of the parent enterprise and for other shareholders.

Equity is a residual arising from the deduction of liabilities from the assets of the

reporting enterprise. Equity arises from two sources: that provided by shareholders

(for example, paid-in capital) and that generated by the activities of the enterprise (for

example, earnings less distributions to shareholders, unrealized surpluses).

B. Income statement/ profit and loss statement

The income statement, or profit and loss statement measures performance of an

enterprise. The bottom line of this statement is the net result of the operations of the

enterprise in the reporting period. It reveals the change during the period in the equity

of the enterprise resulting from its operations.

Revenues

Revenues are inflows or enhancements of assets (or reductions of liabilities) that

arise in the course of the normal activities of the enterprise.

The events that result in revenues and revenues themselves are referred to by a variety of names: including sales, fees, interest, dividends, royalties and rent.

Expenses

Expenses are outflows or depletions of assets (or additions to liabilities) that arise

in the course of the enterprise's normal activities.

The events from which expenses arise and expenses themselves are referred to by

a variety of names, including cost of sales, wages and depreciation.

An expense is recognized when it is realized that an expenditure does not produce

future economic benefits. It is also recognized when a liability is incurred without the

recognition of an asset. When it is possible to do so, expenses are recognized in the

income statement on the basis of direct association between expenses incurred and the

19

20.

earning of specific items of income. The process is commonly referred to as matchingof expenses with revenues.

Gains and losses

Gains are increases in equity that result from transactions that are incidental to the

enterprise's activities and from other transactions, events or circumstances affecting

the enterprise during a period, except those that result in revenues or equity contributions.

Losses are decreases in equity that result from transactions that are incidental to

the enterprise's activities and from other transactions, events or circumstances affecting the enterprise during a period, except those that result in expenses or distributions

of equity.

Gains are normally recognized when realized. Losses are normally recognized

when realized or when it becomes evident that there is an impairment in the value of

the assets, or an increase in the liabilities, to which the losses relate.

Exercise 12.

Read the text quickly and explain what "green accounting" is:

C. Green Accounting

"Green accounting" is accounting for the environment. It is a major issue of public

concern currently being addressed by the Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting. In its first report, presented in March 1990, ISAR considered some preliminary research of the nature, benefits and costs of environmental disclosures together with some tentative

recommendations. In its second report, a year later, ISAR reviewed the response of

governments and industries to its initiative in this area. On the basis of the results

ISAR made some recommendations concerning monitoring information disclosures

and accounting practices in this area.

Six major global industries (chemicals, forestry products, metals, motors, petroleum and petrochemicals, and pharmaceuticals) have been chosen as the basis of this

survey. The grounds for this selection were that such industries are particularly likely

to have environmental information to report as they are industries that tend to have

a significant impact on the environment because of the types of raw materials consumed, the production processes employed, or the nature of the end product.

The industries were asked to disclose information relevant to the following major

areas of concern:

– policies and programmes about environment,

– major environmental improvements achieved,

– emission levels,

– impact on governmental legislation,

– legal proceedings,

– financial impacts.

The survey revealed that there is a high level of interest in environmental matters.

86 % of the surveyed enterprises provided at least some information. Besides, the level of disclosure has increased greatly in comparison with the situation a few years

20

21.

ago. However, most corporations complied with only a very small number of theISAR recommendations. The most common disclosures continue to be qualitative

or descriptive in nature, but not quantitative. It is difficult to gain an objective view

of a corporation's performance in this area.

A significant minority of corporations disclose information about the actual emission

levels and contingent environmental liabilities. One major problem concerning environmental actions that few corporations have yet taken is the question of how to report

the achieved results. For example, while the initiation of major environmental programmes, the achievement of large percentage reductions of emissions and the making

of large financial expenditures may indicate that a corporation is improving its performance, it may also indicate that the corporation has major environmental problems.

In contrast, the existence of no new programmes, stable emission levels and little

financial expenditures may indicate that a corporation is either ignoring the problem

or that the corporation has done extremely well in the past and that there is little room

for further improvements. There is an encouraging sign, however, that a small number

of corporations started to provide fairly detailed and objective information on the extent to which they are meeting the industry norms and governmental requirements.

II. AUDITING

1. PERFORMING AN AUDIT

Vocabulary list

Auditing

Auditor

Examine

Accounting records

financial statements

to offer an opinion

audit

build up

account(s) audit

auditor's opinion

supervisory board

government agency

in-depth audit report

audit process

аудит

аудитор

проверять, проводить ревизию

документы учета

финансовая отчетность

сделать заключение (по результатам

аудиторской проверки)

аудит, аудиторская проверка, ревизия,

проводить аудиторскую проверку

наращивать, накапливать

аудит счетов, ревизия счетов

аудиторское заключение

наблюдательный совет

ведомство, правительственная

организация

детальный аудиторский отчет

процесс проведения аудиторской

проверки

21

22.

audit proceduresjudgement

audited company

preliminary analytical review

assumption

figures

legal position

misstatement

to complete test audit

evaluation

substantive test(ing)

tests in totals

materiality

audit risk

inherent risk

control risk

detection risk

approval of the financial statements

deviation

unqualified opinion

to qualify the opinion

integrity

certify

to conduct ai* audit

generally accepted auditing standards

методика проведения ревизии /

аудиторской проверки

суждение, оценка

проверяемая компания

предварительный анализ финансовохозяйственной деятельности

допущение, предпосылка, предположение

данные

юридическое положение, юридический

статус

сообщение неверных (неправильных)

сведений, искажение сведений

завершить аудиторскую проверку

оценка

независимая проверка

проверка итоговых чисел

«существенность» (искажения)

риск некачественного контроля

присущий (виду деятельности) риск

риск контроля

риск (не)обнаружения

подтверждение финансовой отчетности

отклонение

безусловное мнение (оценка, заключение)

дать аудиторское заключение

с оговорками

добросовестность, профессиональная

честность

выдавать свидетельство

проводить аудиторскую проверку

общепринятые стандарты аудита

TEXT

Auditing is a process in which an independent accountant-auditor examines

a firm's accounting records and financial statements and offers an opinion on their accuracy and reliability.

There are different types of audits, for example, financial statements audits,

income tax audits, "value for money" audits, environmental audits, administrative audits, financial management audits, etc.

The accountancy profession has built up a significant amount of expertise in performing financial statements audits.

Accounts audits \ vere established as an instrument to protect third parties, the users

of accounts, since the auditor's opinion helps establish credibility of financial statements.

22

23.

Special bodies of users, such as supervisory boards, employee representatives,government agencies may sometimes need an in-depth audit report, which is

usually confidential.

It should be stressed that auditors do not monitor, they offer an opinion, and the

audit process and audit procedures are complicated and manifold. The auditor's opinion is gradually being built up from a mass of detailed work to the final judgement

through the planning and testing stages. The auditor normally starts with a study

of the business environment the audited company is working in and performs a preliminary analytical review.

Then he should direct his attention to the financial statements. Interestingly enough,

however, the auditor's attention is not directed towards the financial statements' elements as such. But towards the correctness of various assumptions made by the management for their preparation. For instance, the auditor needs to know if figures are

complete and accurate and reflect what they should reflect, if income and expenses are

recorded in the proper periods and if the legal position is reflected adequately.

The auditor should focus on any misstatement whether it is intentional or unintentional. The management is responsible for the reliability of financial position. If the

management is not prepared to take the responsibility it may be hard to complete the

audit. In such situations the auditor should seek his own evidence by means of independent audit procedures.

Although the financial statements are the ultimate objectives of an audit, normally

such audits cannot be completed without a proper study and evaluation of the accounting system and assessment of the internal accounting controls.

Defining the audit strategy the auditor has to decide whether to rely on internal

controls or to resort to substantive testing applying analytical review procedures, such

as tests in totals, comparison with budgets or even statistical analysis of figures.

In the planning stage as well as during the performance of audit procedures and,

finally, in forming conclusions, "materiality" and "audit risk" are critical elements

in the auditor's judgement. "Materiality" refers to the magnitude or nature of a misstatement (including an omission) of financial information.

"Audit risk" (including three different components - inherent risk, control risk, detection risk) is the risk that an auditor may give an appropriate opinion on financial

information that is materially misstated.

The natural fmalization of the audit process is the auditor's report, reflecting the

auditor's opinion on the financial statements. Unfortunately, audits do not always end

up in an approval of the financial statements. Any deviation from the unqualified opinion should be explained in the auditor's report, including the uncertainty or the disagreement that caused the auditor to qualify his opinion.

In order to protect the public interests and the profession's integrity an individual

must be sufficiently educated and adequately trained before being certified to act as an

auditor.

23

24.

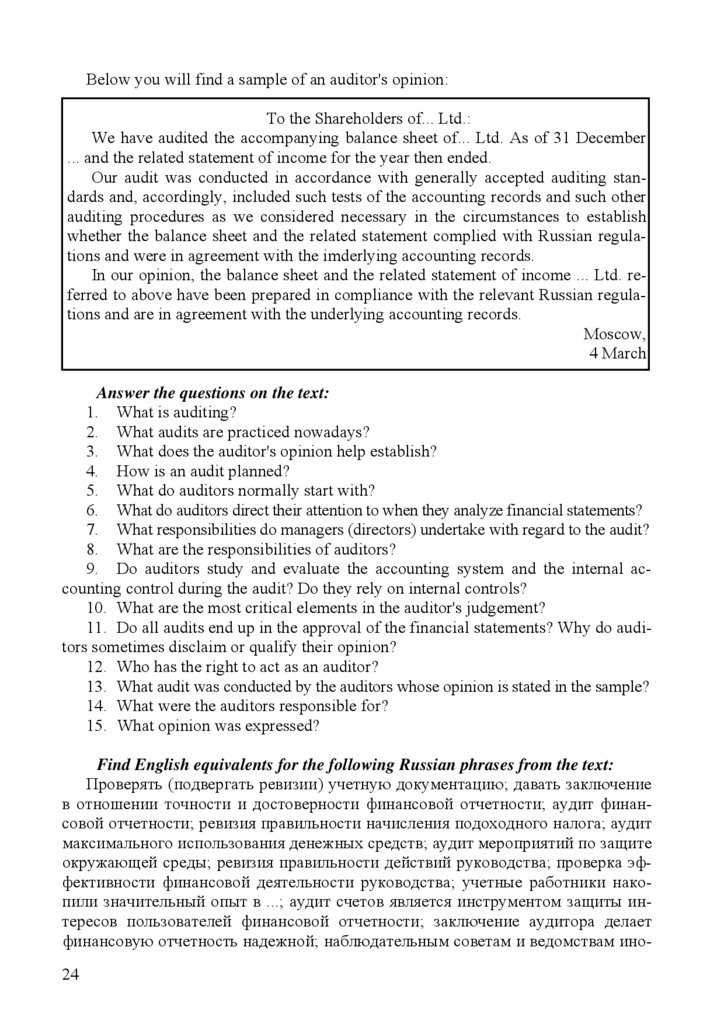

Below you will find a sample of an auditor's opinion:To the Shareholders of... Ltd.:

We have audited the accompanying balance sheet of... Ltd. As of 31 December

... and the related statement of income for the year then ended.

Our audit was conducted in accordance with generally accepted auditing standards and, accordingly, included such tests of the accounting records and such other

auditing procedures as we considered necessary in the circumstances to establish

whether the balance sheet and the related statement complied with Russian regulations and were in agreement with the imderlying accounting records.

In our opinion, the balance sheet and the related statement of income ... Ltd. referred to above have been prepared in compliance with the relevant Russian regulations and are in agreement with the underlying accounting records.

Moscow,

4 March

Answer the questions on the text:

1. What is auditing?

2. What audits are practiced nowadays?

3. What does the auditor's opinion help establish?

4. How is an audit planned?

5. What do auditors normally start with?

6. What do auditors direct their attention to when they analyze financial statements?

7. What responsibilities do managers (directors) undertake with regard to the audit?

8. What are the responsibilities of auditors?

9. Do auditors study and evaluate the accounting system and the internal accounting control during the audit? Do they rely on internal controls?

10. What are the most critical elements in the auditor's judgement?

11. Do all audits end up in the approval of the financial statements? Why do auditors sometimes disclaim or qualify their opinion?

12. Who has the right to act as an auditor?

13. What audit was conducted by the auditors whose opinion is stated in the sample?

14. What were the auditors responsible for?

15. What opinion was expressed?

Find English equivalents for the following Russian phrases from the text:

Проверять (подвергать ревизии) учетную документацию; давать заключение

в отношении точности и достоверности финансовой отчетности; аудит финансовой отчетности; ревизия правильности начисления подоходного налога; аудит

максимального использования денежных средств; аудит мероприятий по защите

окружающей среды; ревизия правильности действий руководства; проверка эффективности финансовой деятельности руководства; учетные работники накопили значительный опыт в ...; аудит счетов является инструментом защиты интересов пользователей финансовой отчетности; заключение аудитора делает

финансовую отчетность надежной; наблюдательным советам и ведомствам ино24

25.

гда нужны глубокие аудиторские отчеты, которые являются, как правило, конфиденциальными; аудиторы не контролируют, они дают заключение в отношении точности и достоверности финансовой отчетности; деловая среда, в которойработает проверяемая компания;

аудиторы обращают свое внимание на правильность предположений руководства; преднамеренное или непреднамеренное искажение данных; брать на

себя ответственность за ...; процедура проведения аудиторской проверки; оценка системы внутреннего контроля; прибегать к независимым проверкам; анализ

финансово-хозяйственной деятельности; «материальность» и «риск некачественного контроля» являются исключительно важными факторами при формировании заключения аудитора; подтвердить финансовую отчетность; безусловное заключение; аудиторская проверка была проведена в соответствии с

общепринятыми стандартами аудита; балансовый отчет соответствует российскому законодательству.

Say in a few words what the text is about. Use the opening phrases.

2. AUDITING IN RUSSIA

Vocabulary list

statutory requirement

in force

"true and fair" view

to find faults

chartered public accountant

consultancy

to render a wide range of services

tax return

maintenance of accounting

institutional infrastructure

audit chamber

statutory audit

practising certificate

consolidated accounts

cost and management accounting

insolvency

civil and commercial law

employment law

установленное законом требование

действующий

точное отражение

находить недочеты

дипломированный частнопрактикующий

бухгалтер

предоставление консультационных услуг

предоставить широкий перечень услуг

налоговая декларация

ведение системы бухучета

институциональная инфраструктура

аудиторская палата

аудит, предписанный законом

свидетельство, дающее право заниматься

аудиторской деятельностью

сводная отчетность

производственный и управленческий

учет

неплатежеспособность

гражданское и коммерческое право

закон о занятости

25

26.

TEXTIn most industrialized countries audit is a statutory requirement applying to limited

companies. The transition to a market economy has led to the establishment

of new market mechanisms and creation of new institutions. Under the legislation

in force, joint ventures are required to submit their annual financial statements, audited by an auditing organization, to the local financial authority.

Russia didn't use to have auditing firms in the past, but this profession is developing very fast. There are hundreds of auditing firms in every big city now.

As in many other countries the auditor is responsible for ensuring that the accounts

show a "true and fair" view of the business's financial position and performance. Auditing in our country is a process in which an independent accountant examines a

firm's records, analyses financial statements and offers an opinion on their accuracy

and reliability. If the auditor doesn't find faults he confirms the Balance Sheet and the

Profit and Loss Account Due to the specific business environment, auditors in Russia

render a very wide range of consultancy services. They help their clients to prepare

tax returns and give advice on the maintenance of accounting and organization of internal control. They also give advice on how to set up businesses, how to improve an

enterprise management, explain their clients rules for performing foreign trade transactions and foreign currency operations.

In order to play their proper part in the national economic development, auditors

must be independent of pressures not simply from clients but also from government

or state agencies. Moreover, an independent, effective and efficient profession requires a strong institutional infrastructure. That's why audit chambers have been set

up throughout the country.

The strength and prestige of a professional body depends on the professional competence. To be entitled to carry out statutory audits of accounting documents in Russia, an auditor must have a license.

As for the professional qualifications for auditors in the UK, they are really very

high. Every chartered accountant undergoes several years of intensive professional

training culminating in examinations of a very high standard. Even then, further experience and study are required to obtain a practicing certificate. The examinations cover such subjects as auditing, analysis and critical assessment of annual accounts, general accounting, consolidated accounts, cost and management accounting, internal

audit, legal and professional standards relating to the statutory auditing, company law,

the law on insolvency, tax law, civil and commercial law, employment law, basic

principles of financial management, etc. That is why, the UK accountants and auditors

are respected over the world.

Answer the questions on the text:

1. What forms of business organization are audited in Russia?

2. Why is the auditing profession developing fast in Russia now?

3. What responsibilities do Russian auditors take?

4. Why is it that Russian auditors offer a wide range of services?

26

27.

5. What conditions can ensure existence of an independent, effective and efficientauditing profession?

6. What professional qualifications exist for auditors in the UK?

7. What examinations do the UK auditors take?

Find English equivalents for the following Russian phrases from the text:

Проведение аудиторской проверки является требованием, установленным

законом; в соответствии с существующим законодательством; финансовая отчетность, проверенная аудиторской фирмой;

аудит быстро развивается; финансовая отчетность дает истинную картину

финансового состояния; обнаружить недочеты; подтвердить счет прибылей и

убытков; правила осуществления внешнеторговых сделок и операций с твердой

валютой; организовать аудиторскую палату; иметь лицензию; пройти интенсивную профессиональную подготовку; получить свидетельство практикующего

аудитора.

Say in a few words what the text is about. Use the opening phrases.

3. EXERCISES

Work on vocabulary and grammar

Exercise 1.

a) Study the key words in the dictionary:

Audit (ing), auditor, auditor's opinion, auditor's report, records.

b) Match the verbs from (1) with the nouns from (2) below:

1)

to share

2)

certificate

to take

assumption

to foster

responsibility

to seek

faults

to submit

services

to give

advice

to make

point of view

to obtain

financial statements

to find

evidence

to render

standards

Exercise 2.

a) Supply the articles where necessary;

b) Write down 3-5 questions about the text;

c) Say what you have learned form the text about government auditing in Sweden;

The Swedish National Audit Office (SNAO) is ... independent institution for central government auditing and accounting in ... Sweden. The main task of... organiza27

28.

tion is to audit the effective fulfilmen of central government goals and commitments.In line with this, the organization analyses revenues and expenditures of ... central

government, audits central government activities, examines accounts and performance

of all government agencies and ... public organizations. The SNAO selects independently ... agencies and activities to be audited, ... auditing methods

to be used, ... content of the audit reports, as well as the audit statements. All audits

are carried out in accordance with generally accepted auditing standards. The audits

principally have ... control functions, but substantial efforts are also made to ensure

that the results of the audit can be used as ... basis for improving efficiency and effectiveness. The SNAO also has ... task of improving financial management at all levels

of ... central government, of fostering high standards of financial management leading

to the efficient use of central government funds, efficient cash flows and security of

the payment system.

The government and ... Parliament use the information of the SNAO as a basis for

their decisions on ... development and transformation of the Swedish public administration. Besides, ... government often turns to the SNOA for ... comments on measures

proposed by different public commissions.

In addition, ... SNAO establishes ... norms, develops auditing methods, and offers

training, and advice on issues related to auditing and financial management.

The staff are recruited on ... basis of educational qualifications and ... professional

ability. Almost 95 per cent of the professional staff hold high professional qualifications.

Central government appropriations finance some fifty per cent of ... organization's activity and the remaining activities are fee-financed. The SNAO is ... active member of

INTOSAI (the International Organization for Supreme Audit Institutions) and its European equivalent EUROSAI (the European Organization for Supreme Audit Institutions).

Words you may need:

Swedish National Audit Office

foster v

cash How

public administration

appropriation n

fee-financed

INTOSAI

EUROSAI

Государственная ревизионная служба Швеции

поощрять, благоприятствовать

поток наличных средств

управление на государственном

и местном уровнях

ассигнование

на хозрасчете

Международная организация высших

контрольных органов

Европейская организация высших

контрольных органов

Exercise 3.

a) Supply the prepositions where necessary.

b) Say what the auditors checked during the audit in accordance with the instructions given to them.

28

29.

Auditors’ ReportWe have examined the books, accounts and vouchers relating ... the six months

ended 30th September ... (year) which were presented ... us. We have made extensive

enquiries ... the system of internal check ... force and are satisfied that it is working

efficiently. Particular attention was paid to the methods in force for the authorization

of accounts for payment and the handling ... cash. The cash balances ...the 30th September ... (year) were counted and found to be in accordance ... the cashier's books.

All bank payments have been verified with the bank statements and certificates of the

balances on the accounts obtained ... the bankers.

We have checked all cash and bank payments ... the receipts and have to report that

a number of small payments are unsupported ... vouchers. It has been possible, however, to obtain other evidence to show that these disbursements were properly made. The

cash books have been cast and all postings ... the various ledgers checked ... detail.

All invoices ... respect of goods purchased and expenses incurred have been examined with the appropriate analysis of books, the totals of which have been

checked. Several minor errors were detected which have not been rectified. The

postings to the Creditors' Ledgers have been test-checked, being far too numerous to

do in detail. The balances ... the individual Creditors' accounts have been compared

with special audit statement obtained from them and found to be ... order. Our instructions did not require us to examine the Sales Ledgers and Day Books: we therefore report that in such work as we have performed we found no evidence or opportunity ... defalcation or fraud.

Words you may need:

Voucher

authorization of accountsfor payment

handling of cash

cash balance

cashier's book

bank statement

receipt

disbursements

cash book

cast

posting

ledger

expenses incurred

detect

оправдательный денежный документ

разрешение на осуществление

платежей со счетов

использование наличности

остаток кассовой наличности

журнал кассовых операций

выписка из счета

квитанция

выплаты

кассовая книга, журнал кассовых

операций

подсчитывать, исчислять, подводить

итоги

проводка

бухгалтерская книга, бухгалтерский

регистр

понесенные расходы

обнаруживать

29

30.

rectifyCreditors' Ledger

test-check

audit statement

Sales Ledger

Day Book

Defalcation

Fraud

исправлять

книга кредиторов

проверять с помощью теста

аудиторский отчет

книга учета продаж

книга операций рабочего дня

присвоение чужих денег

мошенничество, обман

Exercise 4.

a) Open the brackets putting the verbs in the correct form. b) Discuss the content

of the article.

Misuse of Public Funds

It is a universally accepted truth in Russia that the heads of many public funds habitually (to divert) trillions of rubles away from the stated purpose into lucrative deals

for personal gain.

Over the first 10 months of this year, the Accounts Chamber, a watchdog of the

State Duma, (to reveal) that nearly 1.8 trillion rubles, were not used for their designated purposes.

The auditors (to find) that nearly every fund was not using its money as it was supposed to. For instance, the Moscow branch of Russia's Pension Fund (to buy) a building

for about 2 billion rubles, (to spend) 11.5 billion rubles on its renovation and repair,

and (to pay) another 6 billion rubles to an intermediary for "selecting the building",

preparing the necessary documents, and obtaining the consent of the parties concerned." The Pension Fund (to misuse) more than 660 billion rubles despite the fact that

people in some regions were left without pension payments for up to three months.

Many public funds (to set) up their own banks with charter capital running into

hundreds of billions of rubles.

In spite of the obvious violations of regulations, all these operations cannot be put

down as embezzlement without court rulings, and the violators are unlikely to be sued.

Misappropriations from extrabudgetary funds (to encourage) not only by people

with a particular mentality and by a lack of adequate actions on the part of lawenforcement agencies, but also by the very system through which financial resources

(to flow) from top to bottom. State extrabudgetary funds (to act) as an intermediary

that collects payments and remits them to the recipients. Thus, they (to tempt) to "invest" the money in lucrative fast-yielding deals.

There would probably have been fewer cases of embezzlement and misuse of assets if public funds had initially been granted legal rights to earn money by, for example, transacting in securities and foreign-exchange valuables, and making short-term

deposits in banks. So far the funds only (to have) a list of operations barred to them.

30

31.

Words you may need:Misuse

Divert

Lucrative

personal gain

Accounts Chamber

designated purposes

embezzlement

court ruling

sue

misappropriation

remit

recipient

fast-yielding deals

valuables

bar

злоупотребление

отвлекать, отводить

прибыльный, выгодный, доходный

личная выгода

Счетная палата

указанные (запланированные) цели

растрата

постановление суда

преследовать в судебном порядке

незаконное присвоение, растрата

переводить (средства)

получатель

сделки, быстро приносящие прибыль

ценности

запрещать

Exercise 5.

Fill each gap with a suitable word from the box. Sum up the text in 5-7 sentences

and present your summary in class.

free opinion (2)

statements

Proper preparing

responsibilities

standards performed

audit (2)

accordance

management view

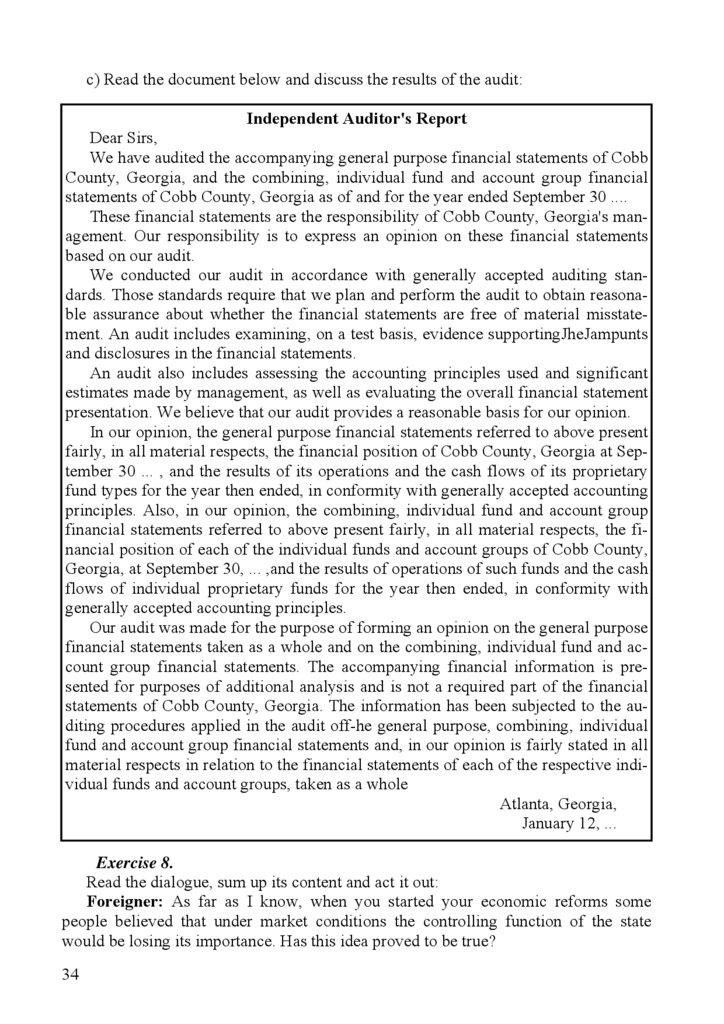

Independent Auditors' Report to the Board of Directors and

Stockholders of ___ Company

We have audited the consolidated balance sheet of __ Company and Subsidiaries

at December 31, ... and ... (years) and the related consolidated statements of income,

stockholders' equity and cash Hows for each of the years in the period ended December 31, ... (year).

Respective __ of directors and auditors are as follows: the company directors are

responsible for the preparation of financial __; our responsibility is to form an independent __ based on our audit of these statements and to report our opinion to you.

Basis of opinion. We conducted our __ in accordance with generally accepted auditing __. Our audit includes examination, on a test basis, of evidence relevant to the

amounts and disclosures in the financial statements. It also includes an assessment of

the significant estimates and judgements made by the ___ in the preparation of the financial statements, and of whether the accounting policies are appropriate to the company's circumstances, consistently applied and adequately disclosed.

We planned and __ our audit so as to obtain all the information and explanations

which we considered ___ in order to provide us with sufficient evidence to give reasonable assurance that the financial statements are __ from material misstatements,

31

32.

whether caused by fraud or other irregularity or error. In __ our opinion we also evaluated the overall adequacy of the presentation of information in the financial statements. We believe that our ___ provides a reasonable basis for our opinion.Opinion. In our __ the financial statements referred to above give a true and fair

of the consolidated financial position of __ Company and Subsidiaries at December 31,

... (year) and have been properly prepared in ___ with generally accepted accounting

principles and the Company Act 1985.

Words you may need:

Disclosure

Fraud

отражение (информации в финансовой отчетности)

обман, мошенничество

Exercise 6.

Read the dialogue, translate the Russian remarks into English and act the dialogue out:

Foreigner: As far as we know, you are Russia's leading provider of accounting

and consulting services. The history of your firm mirrors the changes that have taken

place in Russia over the recent years.

Russian: Да, вы правы. Наша фирма была основана еще в 1989 году. Все эти

годы нам пришлось упорно работать, так как мы начинали практически с нуля.

А сейчас мы активно сотрудничаем с Большой Шестеркой, крупнейшие представители нашего бизнеса обращаются к нам за помощью и советом.

F.: What services do you provide?

R.: Мы предоставляем широкий перечень услуг: от услуг в области бухучета

и аудита до услуг в области финансового менеджмента и налогообложения.

Главным является проведение аудиторских проверок и подтверждение финансовой отчетности.

F.: Who are your clients?

R.: Нашими клиентами являются компании всех форм организации бизнеса,

работающие во всех секторах нашей экономики, включая транспорт, торговлю и

банковскую деятельность.

F.: We in the UK believe that if auditors are to play their role in economy they

must be independent. What are your fundamental principles?

R.: Мы полностью разделяем вашу точку зрения в отношении независимости

аудиторов, кроме того, мы уделяем большое внимание повышению их профессионального уровня.

F.: Are there any professional organizations of auditors in Russia?

R.: Да, у нас существуют различные профессиональные организации, помогающие аудиторским фирмам решать различные вопросы, включая повышение

квалификации, лицензирование и т.п.

F.: Thank you for the opportunity to learn something about auditing in Russia.

32

33.

4. DISCUSSIONExercise 7.

a) Read the texts and do the tasks that follow.

b) Describe the two main functions of auditing. Discuss how public accountants

(auditors) and government auditors perform these functions. Explain the importance

of internal auditing.

Audit is an examination of the records and reports of an enterprise by accounting

specialists other than those responsible for their preparation. Public auditing by independent accountants has acquired professional status and become increasingly common with the rise of large business units and the separation of ownership from control. The public accountant performs tests to determine whether the management's