Менеджмент

Менеджмент Бизнес

БизнесПохожие презентации:

des entreprises")

An Investigation of Financial Determinants of Corporate Dividend Policy

1.

NATIONAL RESEARCH UNIVERSITYHIGHER SCHOOL OF ECONOMICS

Saint Petersburg School of Economics and Management

Prepared by

Academic supervisor

Dmitrishin Stepan

A.Sidorko Senior Lecturer

Mileshnikov Nikita

Ermolaeva Daria

An Investigation of Financial

Determinants of Corporate Dividend

Policy

Bachelor’s thesis in article format

in the field 38.03.02 ‘Management’

“International Business and Management Studies”

Saint Petersburg, 2023

2.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

2

Outline

Research Background and Motivation

3

Research Problem

4

Underlying Theories

5

Main Concepts

6

Hypotheses formulation

7

Methods & Data

9

Results

12

Discussion

14

Conclusion

15

References

17

Appendices

20

3.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

Research Background and

Motivation

1. Dividend policy has been a subject of considerable debate in corporate finance, with

numerous studies examining its determinants and consequences (Sanchit, 2022).

2. Analysis of dividend policies in the U.S. utility, energy, and oil and gas industry can provide

valuable insights for Russian companies to optimize the policies in terms of dividends.

3. The U.S. has a great banking system, relatively flexible taxing policies, one of the greatest

markets in the world with huge perspectives of future development (Schweitzer, 2022).

That is why it is important to investigate what are the determinants of dividend policy in

those sectors in the United States.

3

4.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

4

Research Problem

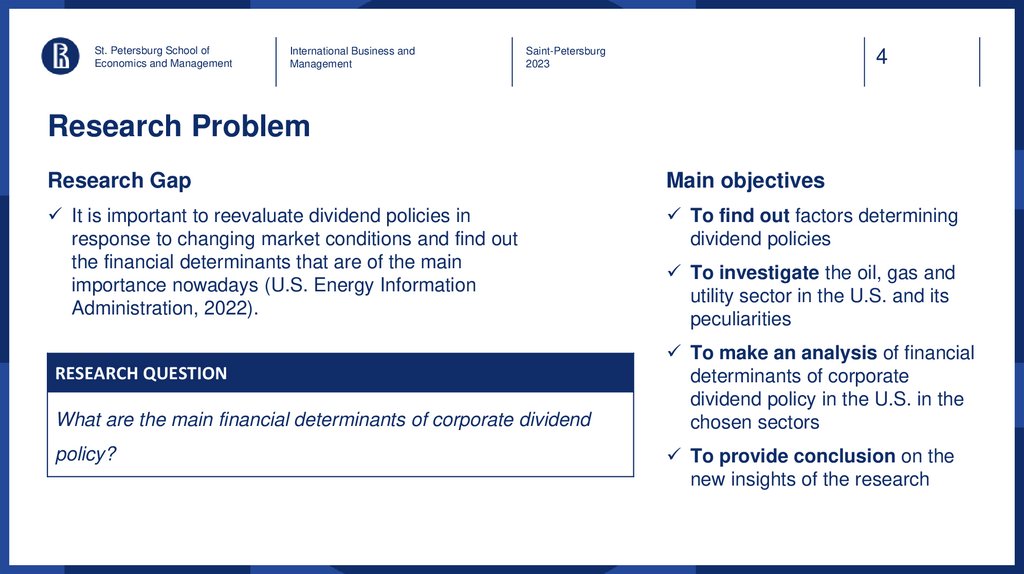

Research Gap

Main objectives

It is important to reevaluate dividend policies in

response to changing market conditions and find out

the financial determinants that are of the main

importance nowadays (U.S. Energy Information

Administration, 2022).

To find out factors determining

dividend policies

RESEARCH QUESTION

What are the main financial determinants of corporate dividend

policy?

To investigate the oil, gas and

utility sector in the U.S. and its

peculiarities

To make an analysis of financial

determinants of corporate

dividend policy in the U.S. in the

chosen sectors

To provide conclusion on the

new insights of the research

5.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

5

Underlying Theories

The Dividend Valuation model

The more dividends a company pays, the higher the value of its stock (Hu et al., 2023).

Gordon growth model (Dividend Discount model)

Method used to value a company's stock based on the assumption that the company will continue to pay

dividends at a constant growth rate indefinitely (Kazi, 2020).

Modigliani and Miller’s dividend irrelevancy theory

The way a company distributes its profits to shareholders should not have an impact on the company's

overall value (Modigliani & Miller, 1961).

6.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

6

Main Concepts

1. Stability of dividends:

Companies should maintain a stable dividend payout over time to avoid large fluctuations in

dividend payouts (Chen, 2020).

2. Dividend payout ratio:

Companies should consider their financial needs, growth prospects, and other factors when

determining their dividend payout ratio (Gill et al., 2010).

3. Retention of earnings:

Companies should retain a portion of their earnings for reinvestment in the business (Baumol et

al., 1970).

4. Investor preferences:

Companies should consider the preferences of their shareholders when determining their

dividend policy (Hu et al., 2023).

7.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

Hypotheses formulation

Quick Ratio shows company’s liquidity position in short-term perspective (Seth, 2022).

According to Dupius (2019), higher liquidity helps companies to perform better and pay higher

dividends.

H1: Increase of quick ratio has significantly positive relationship with

dividend payouts.

Debt-to-Equity ratio is a good proxy for risk. A high debt-to-equity ratio indicates that a

company has more debt than equity financing, which can increase its risk (Collins et al.,

1996).

H2: High Debt-to-Equity ratio has significantly negative relationship with dividend

payouts.

7

8.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

Hypotheses formulation

Basse et al. (2021) stated that if the company operates well, the dividends will be higher. The

financial indicator considered as a determinant for dividend payouts is Return on Sales.

H3: High Return on Sales value has significantly positive relationship with dividend payouts.

Companies with high Return on Invested Capital may see better opportunities to reinvest

their profits back into the business, rather than paying out dividends to shareholders (Ali &

Hegazy, 2022).

H4: Increase in Return on Invested Capital ratio has significantly negative relationship with

dividend payouts.

8

9.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

Methods & Data: Data Collection

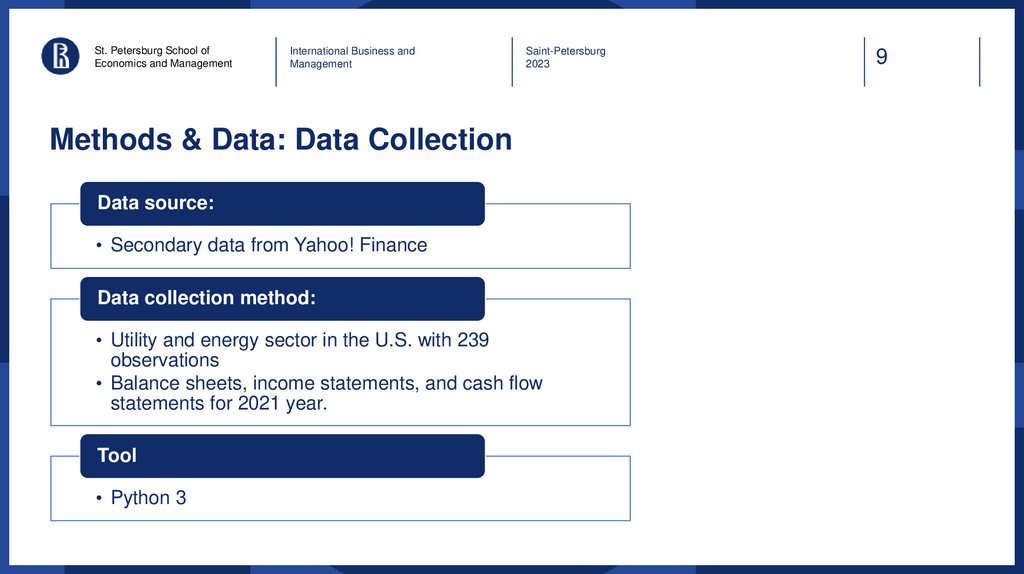

Data source:

• Secondary data from Yahoo! Finance

Data collection method:

• Utility and energy sector in the U.S. with 239

observations

• Balance sheets, income statements, and cash flow

statements for 2021 year.

Tool

• Python 3

9

10.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

10

Methods & Data: Variables definition

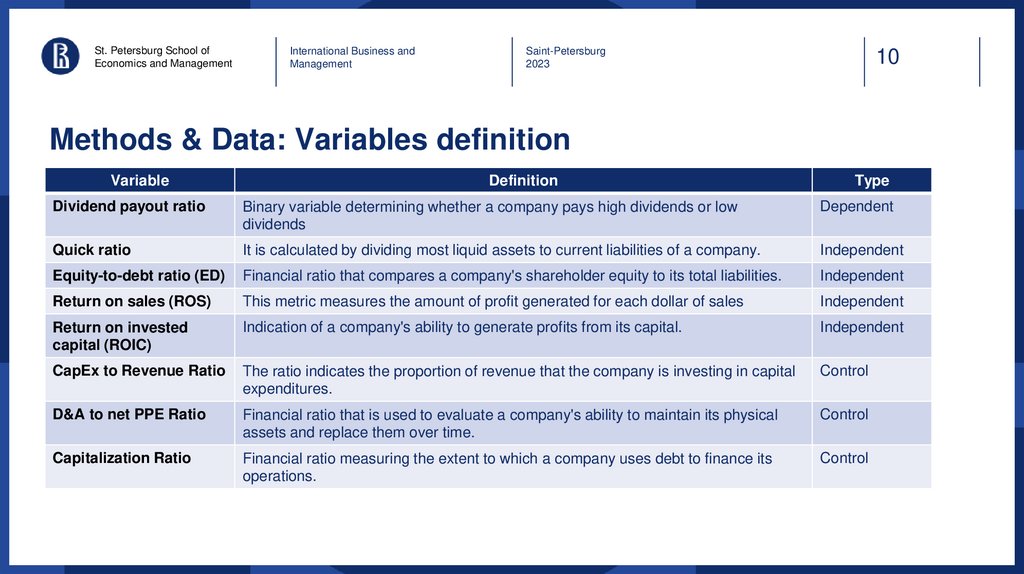

Variable

Definition

Type

Dividend payout ratio

Binary variable determining whether a company pays high dividends or low

dividends

Dependent

Quick ratio

It is calculated by dividing most liquid assets to current liabilities of a company.

Independent

Equity-to-debt ratio (ED)

Financial ratio that compares a company's shareholder equity to its total liabilities.

Independent

Return on sales (ROS)

This metric measures the amount of profit generated for each dollar of sales

Independent

Return on invested

capital (ROIC)

Indication of a company's ability to generate profits from its capital.

Independent

CapEx to Revenue Ratio

The ratio indicates the proportion of revenue that the company is investing in capital

expenditures.

Control

D&A to net PPE Ratio

Financial ratio that is used to evaluate a company's ability to maintain its physical

assets and replace them over time.

Control

Capitalization Ratio

Financial ratio measuring the extent to which a company uses debt to finance its

operations.

Control

11.

St. Petersburg School ofEconomics and Management

International Business and

Management

Methods & Data:

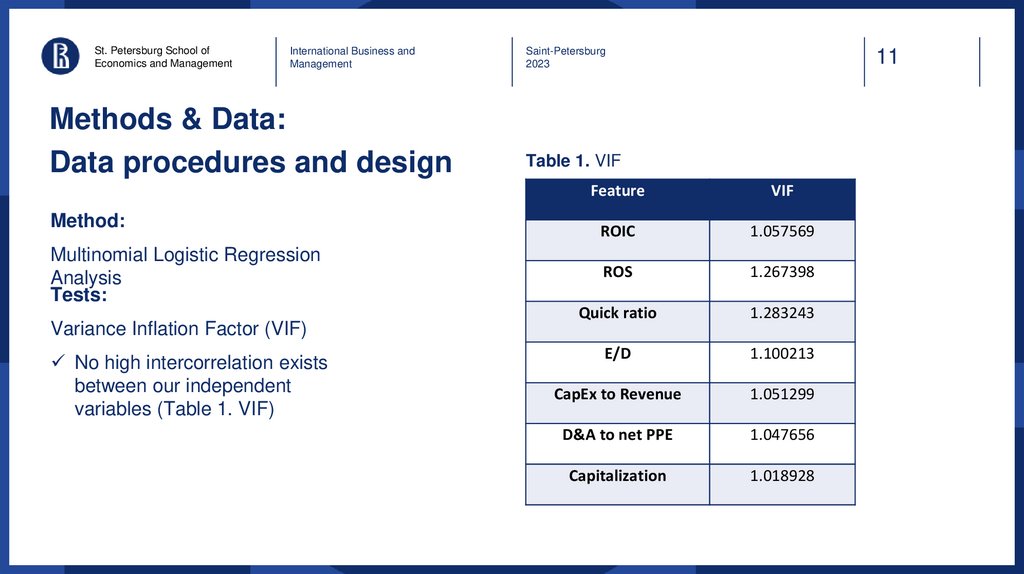

Data procedures and design

Method:

Multinomial Logistic Regression

Analysis

Tests:

Variance Inflation Factor (VIF)

No high intercorrelation exists

between our independent

variables (Table 1. VIF)

Saint-Petersburg

2023

11

Table 1. VIF

Feature

VIF

ROIC

1.057569

ROS

1.267398

Quick ratio

1.283243

E/D

1.100213

CapEx to Revenue

1.051299

D&A to net PPE

1.047656

Capitalization

1.018928

12.

St. Petersburg School ofEconomics and Management

International Business and

Management

Results

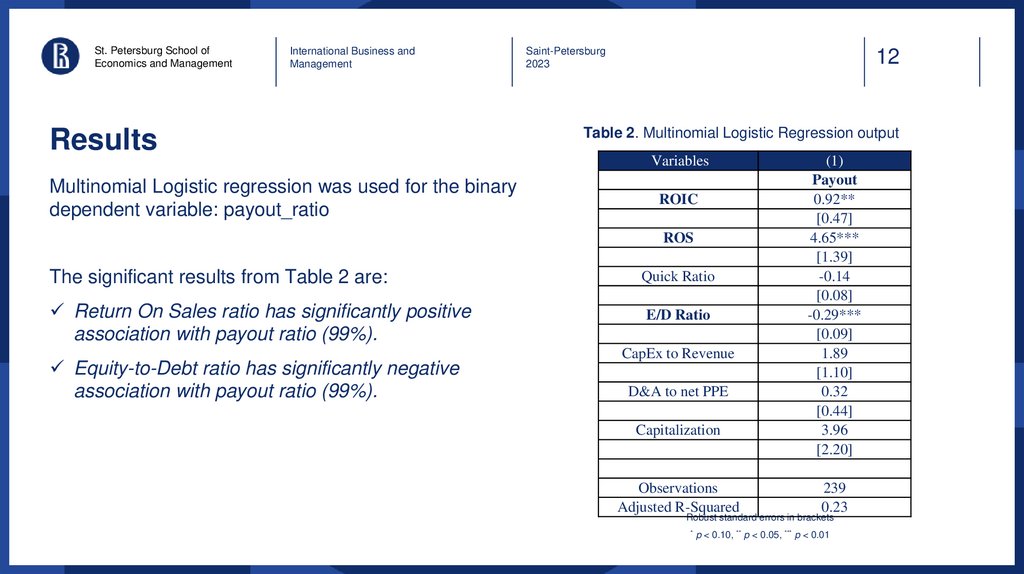

Multinomial Logistic regression was used for the binary

dependent variable: payout_ratio

Saint-Petersburg

2023

12

Table 2. Multinomial Logistic Regression output

Variables

ROIC

ROS

The significant results from Table 2 are:

Quick Ratio

Return On Sales ratio has significantly positive

association with payout ratio (99%).

E/D Ratio

Equity-to-Debt ratio has significantly negative

association with payout ratio (99%).

CapEx to Revenue

D&A to net PPE

Capitalization

Observations

Adjusted R-Squared

(1)

Payout

0.92**

[0.47]

4.65***

[1.39]

-0.14

[0.08]

-0.29***

[0.09]

1.89

[1.10]

0.32

[0.44]

3.96

[2.20]

239

0.23

Robust standard errors in brackets

* p < 0.10, ** p < 0.05, *** p < 0.01

13.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

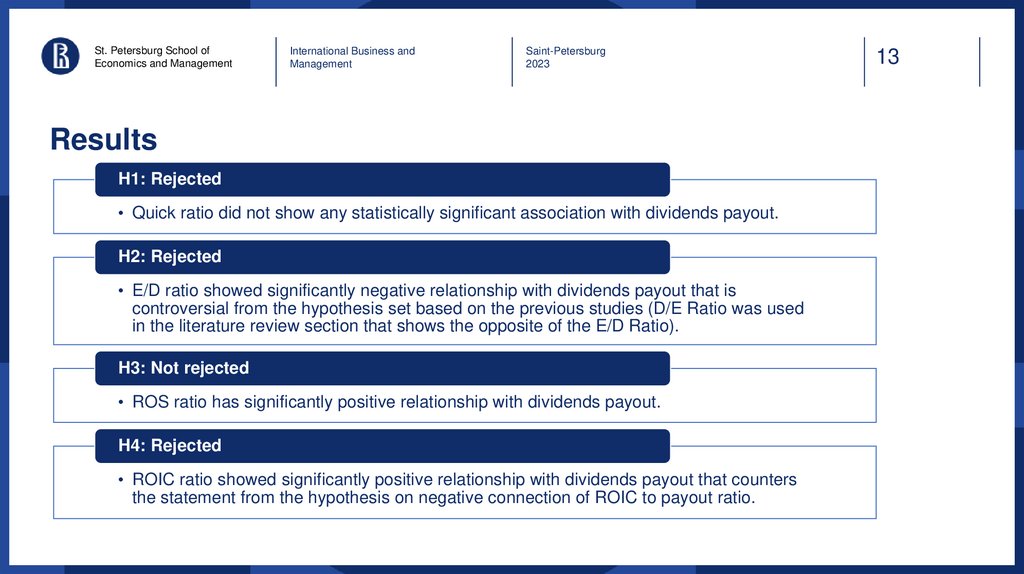

Results

H1: Rejected

• Quick ratio did not show any statistically significant association with dividends payout.

H2: Rejected

• E/D ratio showed significantly negative relationship with dividends payout that is

controversial from the hypothesis set based on the previous studies (D/E Ratio was used

in the literature review section that shows the opposite of the E/D Ratio).

H3: Not rejected

• ROS ratio has significantly positive relationship with dividends payout.

H4: Rejected

• ROIC ratio showed significantly positive relationship with dividends payout that counters

the statement from the hypothesis on negative connection of ROIC to payout ratio.

13

14.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

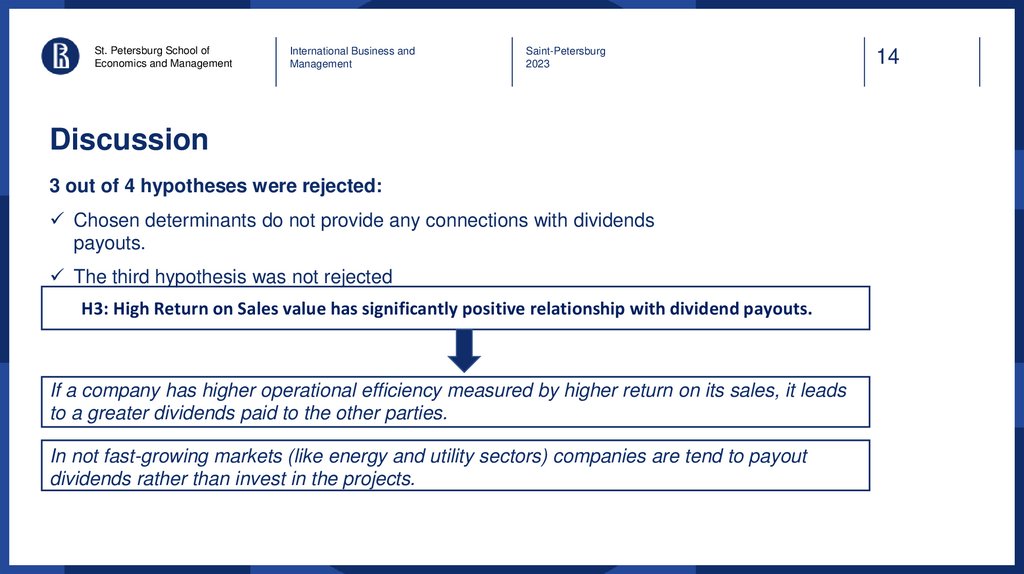

Discussion

3 out of 4 hypotheses were rejected:

Chosen determinants do not provide any connections with dividends

payouts.

The third hypothesis was not rejected

H3: High Return on Sales value has significantly positive relationship with dividend payouts.

If a company has higher operational efficiency measured by higher return on its sales, it leads

to a greater dividends paid to the other parties.

In not fast-growing markets (like energy and utility sectors) companies are tend to payout

dividends rather than invest in the projects.

14

15.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

15

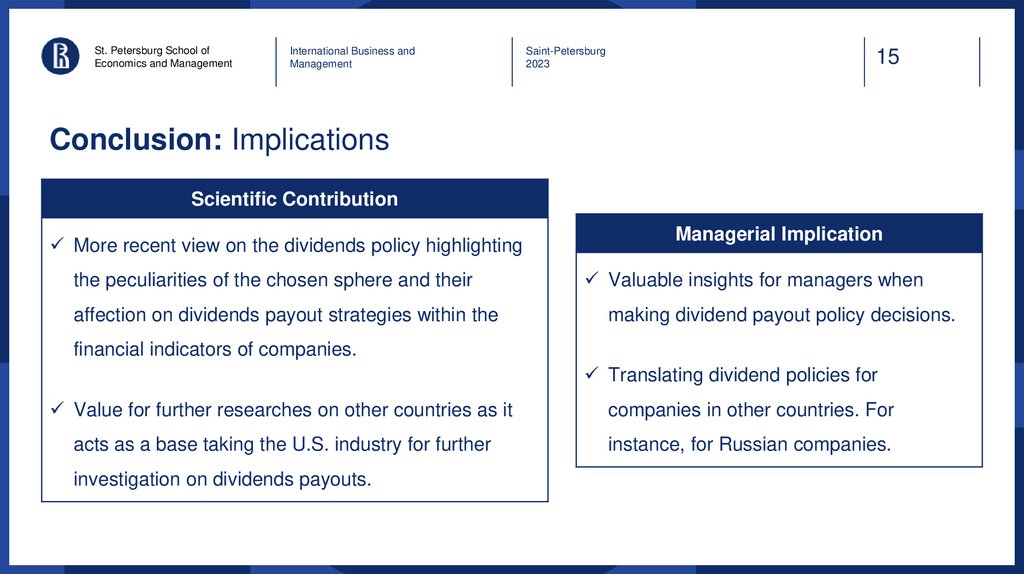

Conclusion: Implications

Scientific Contribution

More recent view on the dividends policy highlighting

the peculiarities of the chosen sphere and their

affection on dividends payout strategies within the

Managerial Implication

Valuable insights for managers when

making dividend payout policy decisions.

financial indicators of companies.

Translating dividend policies for

Value for further researches on other countries as it

companies in other countries. For

acts as a base taking the U.S. industry for further

instance, for Russian companies.

investigation on dividends payouts.

16.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

16

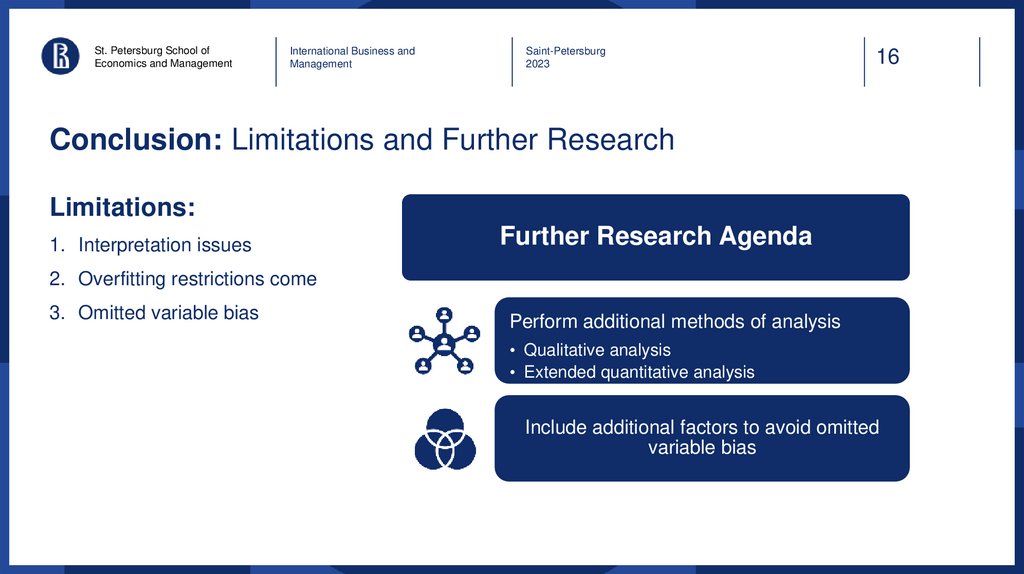

Conclusion: Limitations and Further Research

Limitations:

1. Interpretation issues

Further Research Agenda

2. Overfitting restrictions come

3. Omitted variable bias

Perform additional methods of analysis

• Qualitative analysis

• Extended quantitative analysis

Include additional factors to avoid omitted

variable bias

17.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

17

References

1. Ali, H., & Hegazy, A. Y. (2022). Dividend policy, risk and the cross-section of stock returns: Evidence from India. International

Review of Economics & Finance, 79, 169-192. https://doi.org/10.1016/j.iref.2022.02.002

2. Baumol, W. J., Heim, P., Malkiel, B. G., & Quandt, R. E. (1970). Earnings retention, new capital and the growth of the

firm. The Review of Economics and Statistics, 345-355. https://doi.org/10.2307/1926311

3. Basse, T., Klein, T., Vigne, S. A., & Wegener, C. (2021). US stock prices and the dot. com-bubble: Can dividend

policy rescue the efficient market hypothesis?. Journal of Corporate Finance, 67, 101892.

https://doi.org/10.1016/j.jcorpfin.2021.101892

4. Chen, J., Song, W., & Goergen, M. (2020). Passing the dividend baton: The impact of dividend policy on new CEOs'

initial compensation. Journal of Corporate Finance, 56, 458-481. https://doi.org/10.1016/j.jcorpfin.2019.04.004

5. Collins, M. C., Saxena, A. K., & Wansley, J. W. (1996). The role of insiders and dividend policy: a comparison of regulated and

unregulated firms. Journal of Financial and Strategic Decisions, 9(2), 1-9. Retrieved from:

[https://www.researchgate.net/profile/M-Collins3/publication/237692072_The_role_of_insiders_and_dividend_policy_A_comparison_of_regulated_and_unregulated_firms/lin

ks/56f912f408ae95e8b6d3f65f/The-role-of-insiders-and-dividend-policy-A-comparison-of-regulated-and-unregulated-firms.pdf].

6. Dupuis, D. (2019). Ex-dividend day price behavior and liquidity in a tax-free emerging market. Emerging Markets Review, 38,

239-250. https://doi.org/10.1016/j.ememar.2019.02.001

7. Gill, A., Biger, N., & Tibrewala, R. (2010). Determinants of dividend payout ratios: evidence from United States. The Open

Business Journal, 3(1). http://dx.doi.org/10.2174/1874915101003010008

18.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

18

References

8. Hu, X., Chen, Y., Ren, L., & Xu, Z. (2023). Investor Preference Analysis: An Online Optimization Approach with

Missing Information. Information Sciences. https://doi.org/10.1016/j.ins.2023.03.066

9. Kazi, M. (2020). Gordon Growth Model (GGM). FinancialEdge. Retrieved from: [https://www.fe.training/freeresources/valuation/gordon-growth-model-ggd/#:~:text=The Gordon Growth Model].

10. Miller, M. H., & Modigliani, F. (1961). Dividend Policy, Growth, and the Valuation of Shares. The Journal of Business,

34(4), 411–433. Retrieved from: [http://www.jstor.org/stable/2351143].

11. Sanchit, G. (2022). Dividend Policy. Economics Discussion. Retrieved from:

[https://www.economicsdiscussion.net/financial-management/dividend-policy/33373].

12. Schweitzer, K. (2022). The 9 Benefits of a setting up a US Company for a Foreigner (Non-Residents). StartFleet.

Retrieved from: [https://startfleet.io/guide/9-benefits-of-us-company-for-non-residents].

13. Seth, S. (2022). Quick Ratio Formula With Examples, Pros and Cons. Investopedia. Retrieved from:

[https://www.investopedia.com/terms/q/quickratio.asp].

14. U.S. Energy Information Administration. (2022). Gasoline explained. Gasoline price fluctuations. EIA. Retrieved from:

[https://www.eia.gov/energyexplained/gasoline/price-fluctuations.php#:~:text=Gasoline].

19.

NATIONAL RESEARCH UNIVERSITYHIGHER SCHOOL OF ECONOMICS

Prepared by

Academic supervisor

Saint Petersburg School of Economics and Management

«Сюда вставим наши фото с контактной

информацией»

Thank you

for your attention!

20.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

20

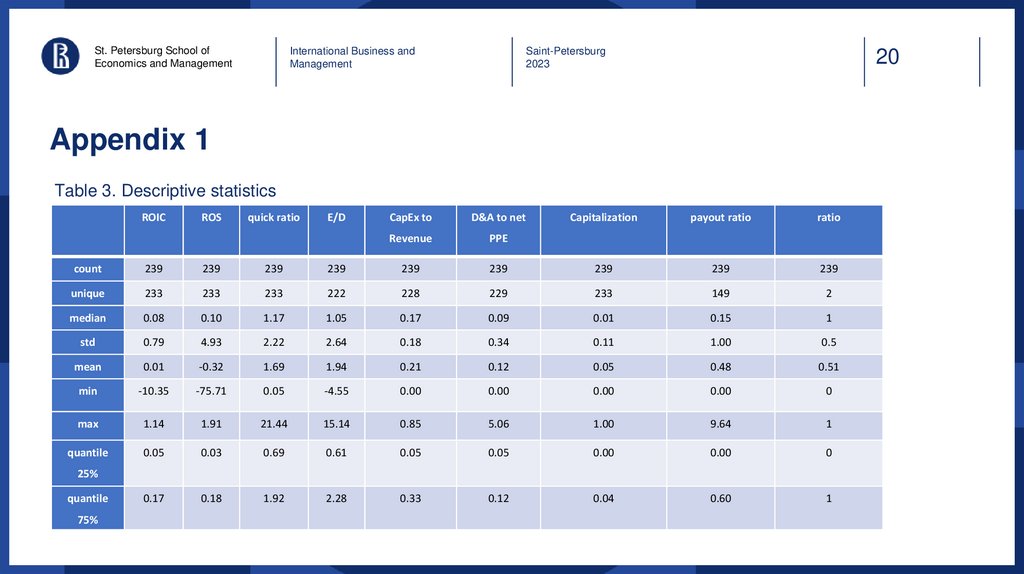

Appendix 1

Table 3. Descriptive statistics

ROIC

ROS

quick ratio

E/D

CapEx to

D&A to net

Revenue

PPE

Capitalization

payout ratio

ratio

count

239

239

239

239

239

239

239

239

239

unique

233

233

233

222

228

229

233

149

2

median

0.08

0.10

1.17

1.05

0.17

0.09

0.01

0.15

1

std

0.79

4.93

2.22

2.64

0.18

0.34

0.11

1.00

0.5

mean

0.01

-0.32

1.69

1.94

0.21

0.12

0.05

0.48

0.51

min

-10.35

-75.71

0.05

-4.55

0.00

0.00

0.00

0.00

0

max

1.14

1.91

21.44

15.14

0.85

5.06

1.00

9.64

1

quantile

0.05

0.03

0.69

0.61

0.05

0.05

0.00

0.00

0

0.17

0.18

1.92

2.28

0.33

0.12

0.04

0.60

1

25%

quantile

75%

21.

St. Petersburg School ofEconomics and Management

International Business and

Management

Saint-Petersburg

2023

21

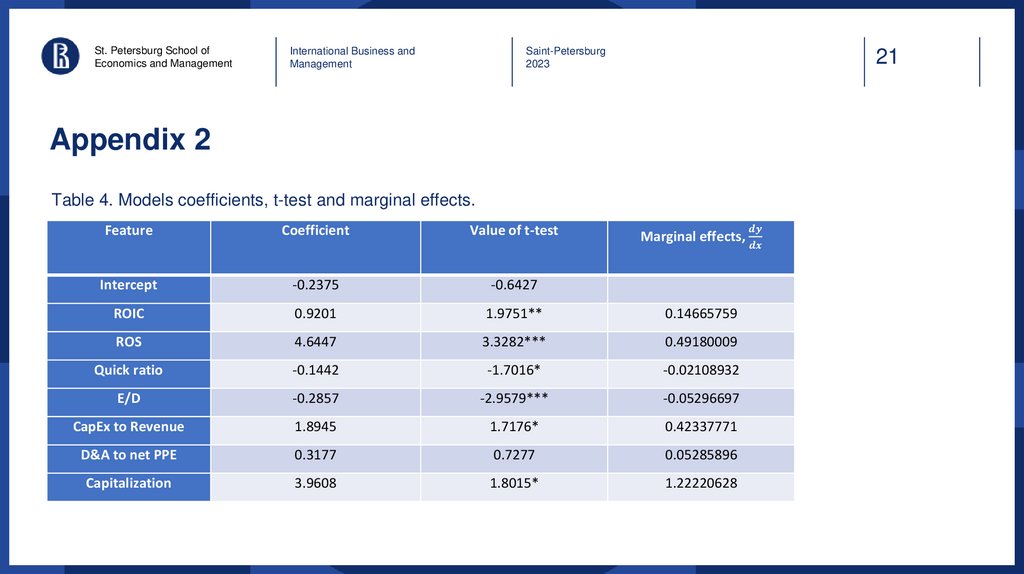

Appendix 2

Table 4. Models coefficients, t-test and marginal effects.

Feature

Coefficient

Value of t-test

Marginal effects,

Intercept

-0.2375

-0.6427

ROIC

0.9201

1.9751**

0.14665759

ROS

4.6447

3.3282***

0.49180009

Quick ratio

-0.1442

-1.7016*

-0.02108932

E/D

-0.2857

-2.9579***

-0.05296697

CapEx to Revenue

1.8945

1.7176*

0.42337771

D&A to net PPE

0.3177

0.7277

0.05285896

Capitalization

3.9608

1.8015*

1.22220628