Экономика

ЭкономикаПохожие презентации:

Malaysia Distribution Strategy Report

1.

Malaysia Distribution Strategy Report2023. 04

Global Distribution Strategy PJT

2.

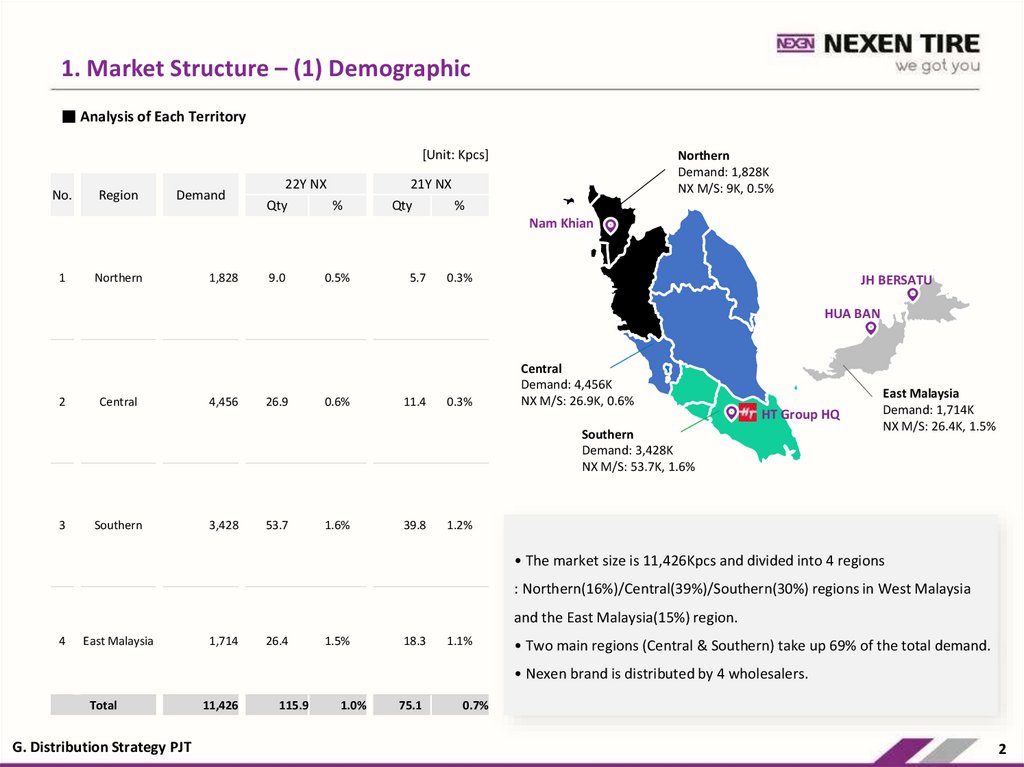

1. Market Structure – (1) Demographic■ Analysis of Each Territory

[Unit: Kpcs]

No.

Region

Demand

22Y NX

Qty

Northern

Demand: 1,828K

NX M/S: 9K, 0.5%

21Y NX

%

Qty

%

Nam Khian

1

Northern

1,828

9.0

0.5%

5.7

0.3%

JH BERSATU

HUA BAN

2

Central

4,456

26.9

0.6%

11.4

0.3%

Central

Demand: 4,456K

NX M/S: 26.9K, 0.6%

HT Group HQ

Southern

Demand: 3,428K

NX M/S: 53.7K, 1.6%

3

Southern

3,428

53.7

1.6%

39.8

East Malaysia

Demand: 1,714K

NX M/S: 26.4K, 1.5%

1.2%

• The market size is 11,426Kpcs and divided into 4 regions

: Northern(16%)/Central(39%)/Southern(30%) regions in West Malaysia

and the East Malaysia(15%) region.

4

East Malaysia

1,714

26.4

1.5%

18.3

1.1%

• Two main regions (Central & Southern) take up 69% of the total demand.

• Nexen brand is distributed by 4 wholesalers.

Total

G. Distribution Strategy PJT

11,426

115.9

1.0%

75.1

0.7%

2

3.

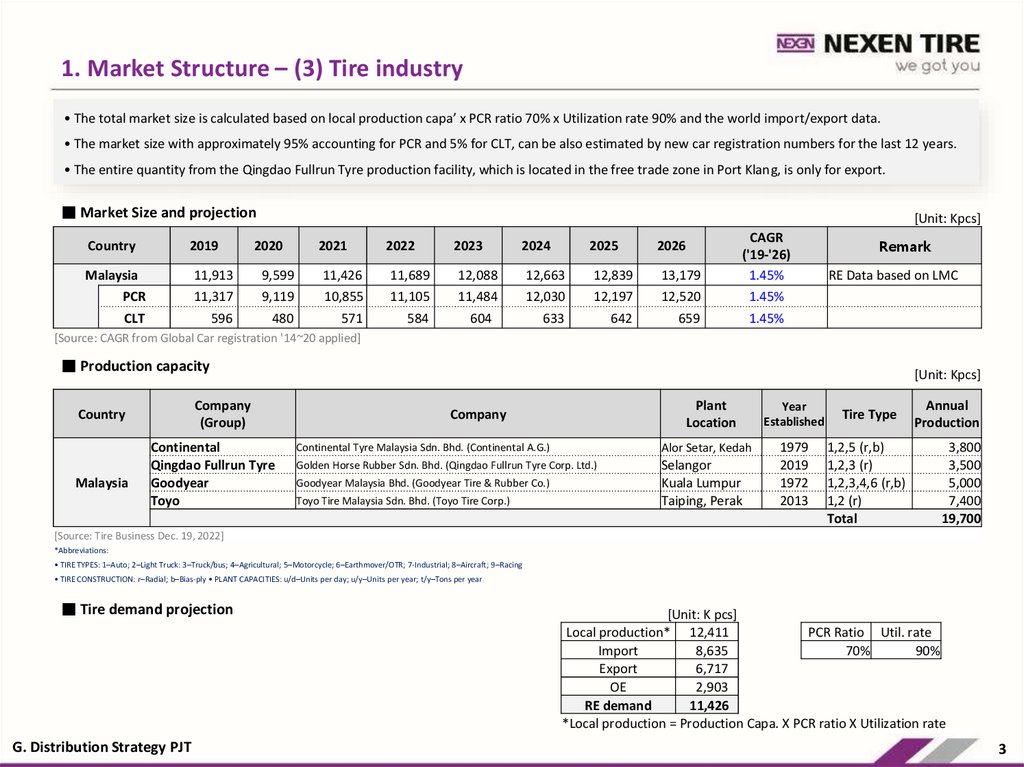

1. Market Structure – (3) Tire industry• The total market size is calculated based on local production capa’ x PCR ratio 70% x Utilization rate 90% and the world import/export data.

• The market size with approximately 95% accounting for PCR and 5% for CLT, can be also estimated by new car registration numbers for the last 12 years.

• The entire quantity from the Qingdao Fullrun Tyre production facility, which is located in the free trade zone in Port Klang, is only for export.

■ Market Size and projection

[Unit: Kpcs]

Country

2019

2020

2021

2022

2023

2024

2025

2026

Malaysia

11,913

9,599

11,426

11,689

12,088

12,663

12,839

13,179

CAGR

('19-'26)

1.45%

PCR

11,317

9,119

10,855

11,105

11,484

12,030

12,197

12,520

1.45%

CLT

596

480

571

584

604

633

642

659

1.45%

Remark

RE Data based on LMC

[Source: CAGR from Global Car registration '14~20 applied]

■ Production capacity

Company

(Group)

Country

Malaysia

Continental

Qingdao Fullrun Tyre

Goodyear

Toyo

[Unit: Kpcs]

Plant

Location

Year

Established

Continental Tyre Malaysia Sdn. Bhd. (Continental A.G.)

Alor Setar, Kedah

Golden Horse Rubber Sdn. Bhd. (Qingdao Fullrun Tyre Corp. Ltd.)

Selangor

Kuala Lumpur

Taiping, Perak

1979

2019

1972

2013

Company

Goodyear Malaysia Bhd. (Goodyear Tire & Rubber Co.)

Toyo Tire Malaysia Sdn. Bhd. (Toyo Tire Corp.)

Tire Type

Annual

Production

1,2,5 (r,b)

1,2,3 (r)

1,2,3,4,6 (r,b)

1,2 (r)

Total

3,800

3,500

5,000

7,400

19,700

[Source: Tire Business Dec. 19, 2022]

*Abbreviations:

• TIRE TYPES: 1–Auto; 2–Light Truck: 3–Truck/bus; 4–Agricultural; 5–Motorcycle; 6–Earthmover/OTR; 7-Industrial; 8–Aircraft; 9–Racing

• TIRE CONSTRUCTION: r–Radial; b–Bias-ply • PLANT CAPACITIES: u/d–Units per day; u/y–Units per year; t/y–Tons per year

■ Tire demand projection

G. Distribution Strategy PJT

[Unit: K pcs]

Local production* 12,411

PCR Ratio Util. rate

Import

8,635

70%

90%

Export

6,717

OE

2,903

RE demand

11,426

*Local production = Production Capa. X PCR ratio X Utilization rate

3

4.

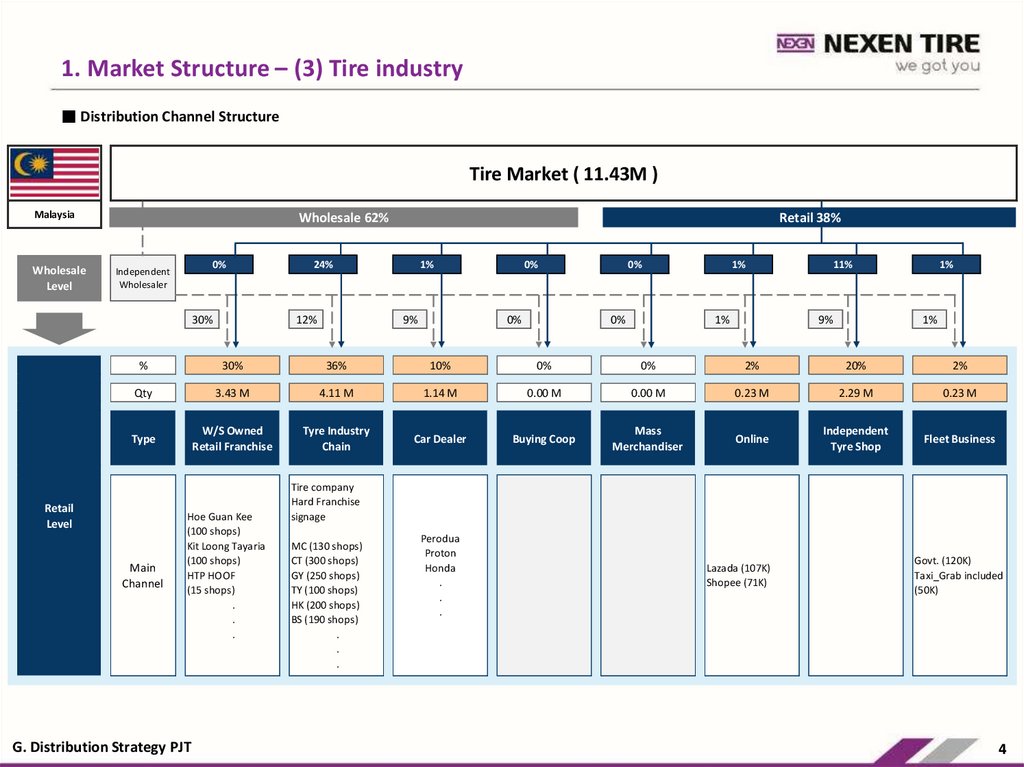

1. Market Structure – (3) Tire industry■ Distribution Channel Structure

Tire Market ( 11.43M )

Malaysia

Wholesale

Level

Wholesale 62%

0%

Independent

Wholesaler

30%

Retail 38%

24%

12%

1%

9%

0%

0%

0%

0%

1%

1%

11%

9%

1%

1%

%

30%

36%

10%

0%

0%

2%

20%

2%

Qty

3.43 M

4.11 M

1.14 M

0.00 M

0.00 M

0.23 M

2.29 M

0.23 M

Type

W/S Owned

Retail Franchise

Tyre Industry

Chain

Car Dealer

Buying Coop

Mass

Merchandiser

Online

Independent

Tyre Shop

Fleet Business

Retail

Level

Main

Channel

Hoe Guan Kee

(100 shops)

Kit Loong Tayaria

(100 shops)

HTP HOOF

(15 shops)

.

.

.

G. Distribution Strategy PJT

Tire company

Hard Franchise

signage

MC (130 shops)

CT (300 shops)

GY (250 shops)

TY (100 shops)

HK (200 shops)

BS (190 shops)

.

.

.

Perodua

Proton

Honda

.

.

.

Lazada (107K)

Shopee (71K)

Govt. (120K)

Taxi_Grab included

(50K)

4

5.

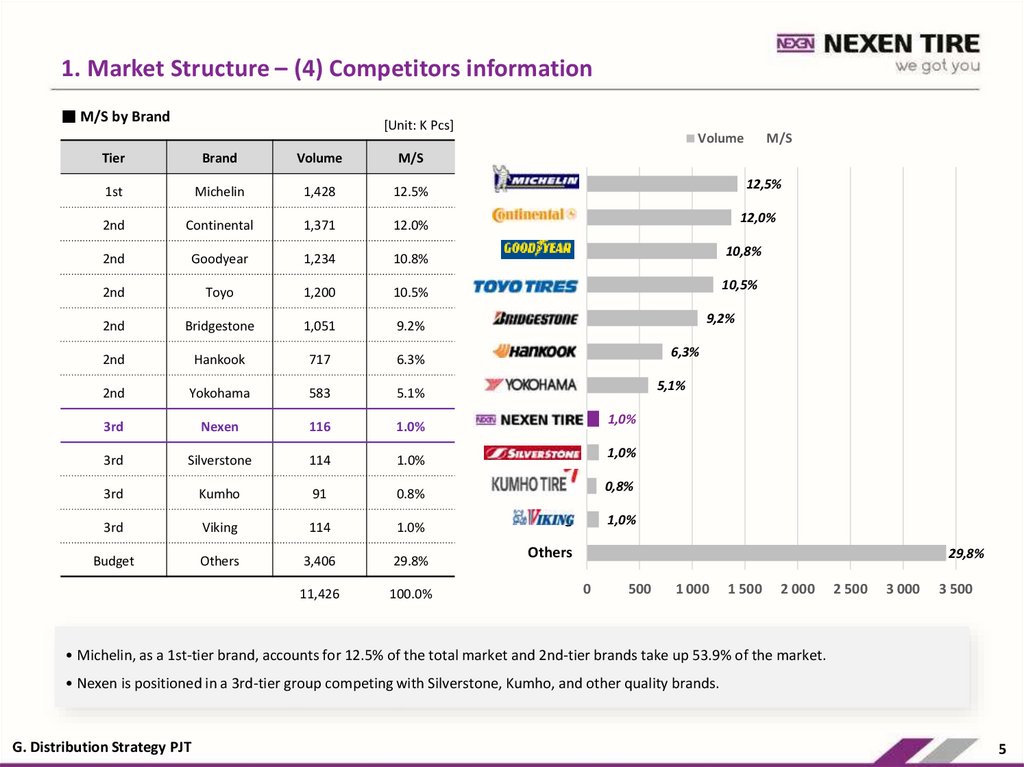

1. Market Structure – (4) Competitors information■ M/S by Brand

[Unit: K Pcs]

Tier

Brand

Volume

M/S

1st

Michelin

1,428

12.5%

2nd

Continental

1,371

12.0%

2nd

Goodyear

1,234

10.8%

2nd

Toyo

1,200

10.5%

2nd

Bridgestone

1,051

9.2%

2nd

Hankook

717

6.3%

2nd

Yokohama

583

5.1%

3rd

Nexen

116

1.0%

3rd

Silverstone

114

1.0%

3rd

Kumho

91

0.8%

3rd

Viking

114

1.0%

Budget

Others

3,406

29.8%

11,426

100.0%

Volume

M/S

Michelin

12,5%

Continental

12,0%

Goodyear

10,8%

Toyo

10,5%

Bridgestone

9,2%

Hankook

6,3%

Yokohama

5,1%

Nexen

1,0%

Silverstone

1,0%

Kumho

0,8%

Viking

1,0%

Others

29,8%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

• Michelin, as a 1st-tier brand, accounts for 12.5% of the total market and 2nd-tier brands take up 53.9% of the market.

• Nexen is positioned in a 3rd-tier group competing with Silverstone, Kumho, and other quality brands.

G. Distribution Strategy PJT

5

6.

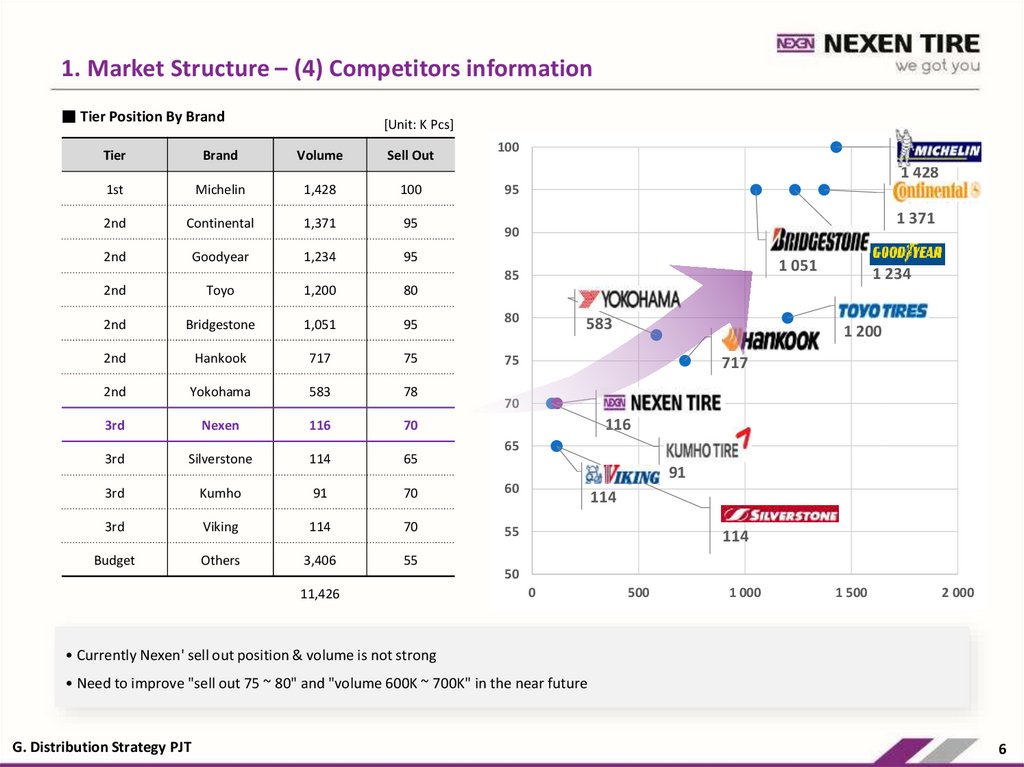

1. Market Structure – (4) Competitors information■ Tier Position By Brand

[Unit: K Pcs]

100

Tier

Brand

Volume

Sell Out

1st

Michelin

1,428

100

2nd

Continental

1,371

95

2nd

Goodyear

1,234

95

2nd

Toyo

1,200

80

2nd

Bridgestone

1,051

95

80

2nd

Hankook

717

75

75

2nd

Yokohama

583

78

3rd

Nexen

116

70

3rd

Silverstone

114

65

3rd

Kumho

91

70

60

3rd

Viking

114

70

55

Budget

Others

3,406

55

Michelin

1 428

Continental

1 371

95

90

Bridgestone

Goodyear

1 051

1 234

85

11,426

Yokohama

583

Hankook

717

Toyo

1 200

Nexen

116

70

65

Viking

114

Kumho

91

Silverstone

114

50

0

500

1 000

1 500

2 000

• Currently Nexen' sell out position & volume is not strong

• Need to improve "sell out 75 ~ 80" and "volume 600K ~ 700K" in the near future

G. Distribution Strategy PJT

6

7.

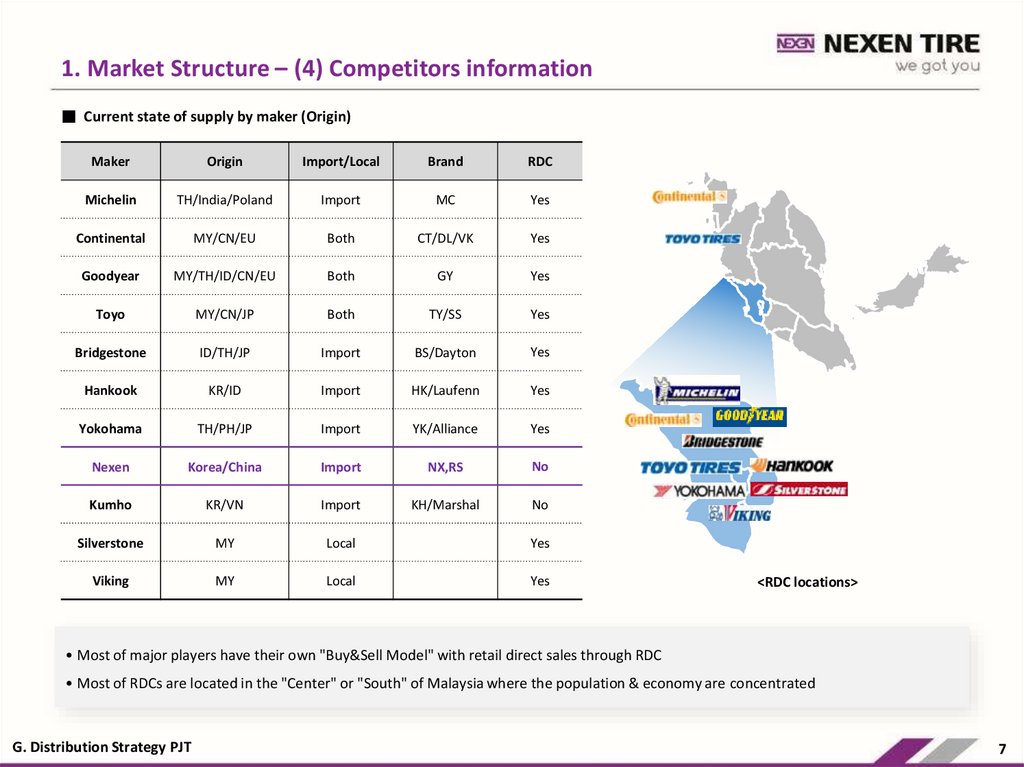

1. Market Structure – (4) Competitors information■ Current state of supply by maker (Origin)

Maker

Origin

Import/Local

Brand

RDC

Michelin

TH/India/Poland

Import

MC

Yes

Continental

MY/CN/EU

Both

CT/DL/VK

Yes

Goodyear

MY/TH/ID/CN/EU

Both

GY

Yes

Toyo

MY/CN/JP

Both

TY/SS

Yes

Bridgestone

ID/TH/JP

Import

BS/Dayton

Yes

Hankook

KR/ID

Import

HK/Laufenn

Yes

Yokohama

TH/PH/JP

Import

YK/Alliance

Yes

Nexen

Korea/China

Import

NX,RS

No

Kumho

KR/VN

Import

KH/Marshal

No

Silverstone

MY

Local

Yes

Viking

MY

Local

Yes

<RDC locations>

• Most of major players have their own "Buy&Sell Model" with retail direct sales through RDC

• Most of RDCs are located in the "Center" or "South" of Malaysia where the population & economy are concentrated

G. Distribution Strategy PJT

7

8.

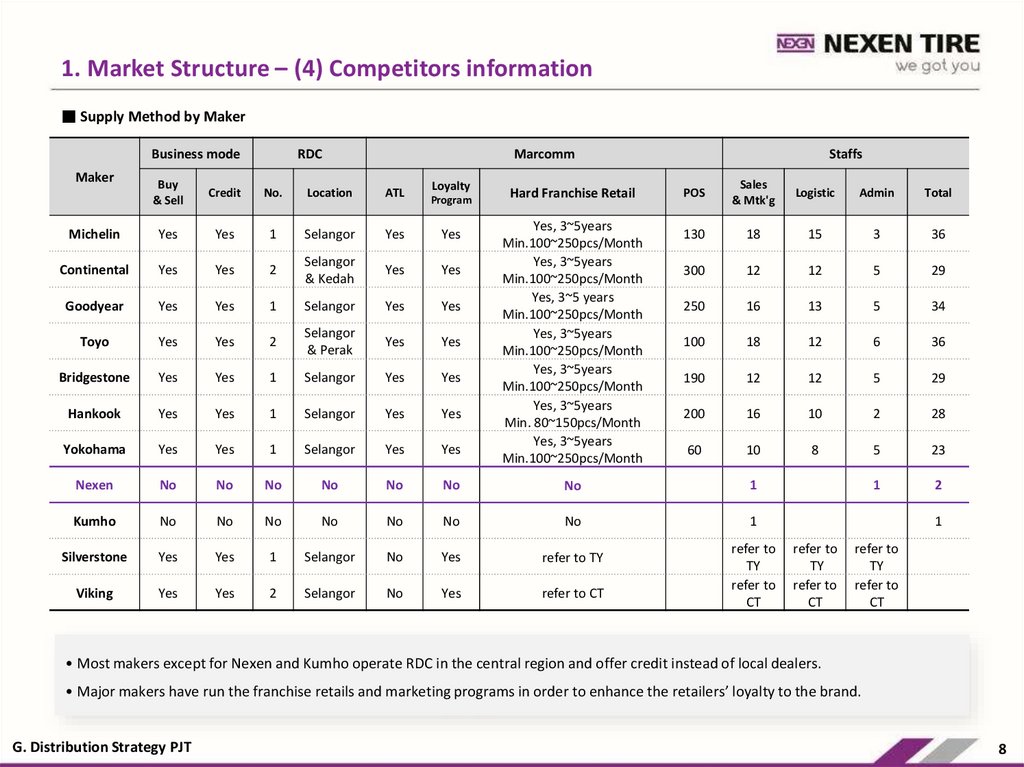

1. Market Structure – (4) Competitors information■ Supply Method by Maker

Business mode

Maker

RDC

Marcomm

Staffs

Buy

& Sell

Credit

No.

Location

ATL

Michelin

Yes

Yes

1

Selangor

Yes

Yes

Continental

Yes

Yes

2

Selangor

& Kedah

Yes

Yes

Goodyear

Yes

Yes

1

Selangor

Yes

Yes

Toyo

Yes

Yes

2

Selangor

& Perak

Yes

Yes

Bridgestone

Yes

Yes

1

Selangor

Yes

Yes

Hankook

Yes

Yes

1

Selangor

Yes

Yes

Yokohama

Yes

Yes

1

Selangor

Yes

Yes

Nexen

No

No

No

No

No

No

No

1

Kumho

No

No

No

No

No

No

No

1

Silverstone

Yes

Yes

1

Selangor

No

Yes

refer to TY

Viking

Yes

Yes

2

Selangor

No

Yes

refer to CT

Loyalty

Program

Hard Franchise Retail

Yes, 3~5years

Min.100~250pcs/Month

Yes, 3~5years

Min.100~250pcs/Month

Yes, 3~5 years

Min.100~250pcs/Month

Yes, 3~5years

Min.100~250pcs/Month

Yes, 3~5years

Min.100~250pcs/Month

Yes, 3~5years

Min. 80~150pcs/Month

Yes, 3~5years

Min.100~250pcs/Month

POS

Sales

& Mtk'g

Logistic

Admin

Total

130

18

15

3

36

300

12

12

5

29

250

16

13

5

34

100

18

12

6

36

190

12

12

5

29

200

16

10

2

28

60

10

8

5

23

1

2

refer to

TY

refer to

CT

1

refer to

TY

refer to

CT

refer to

TY

refer to

CT

• Most makers except for Nexen and Kumho operate RDC in the central region and offer credit instead of local dealers.

• Major makers have run the franchise retails and marketing programs in order to enhance the retailers’ loyalty to the brand.

G. Distribution Strategy PJT

8