Маркетинг

МаркетингПохожие презентации:

")

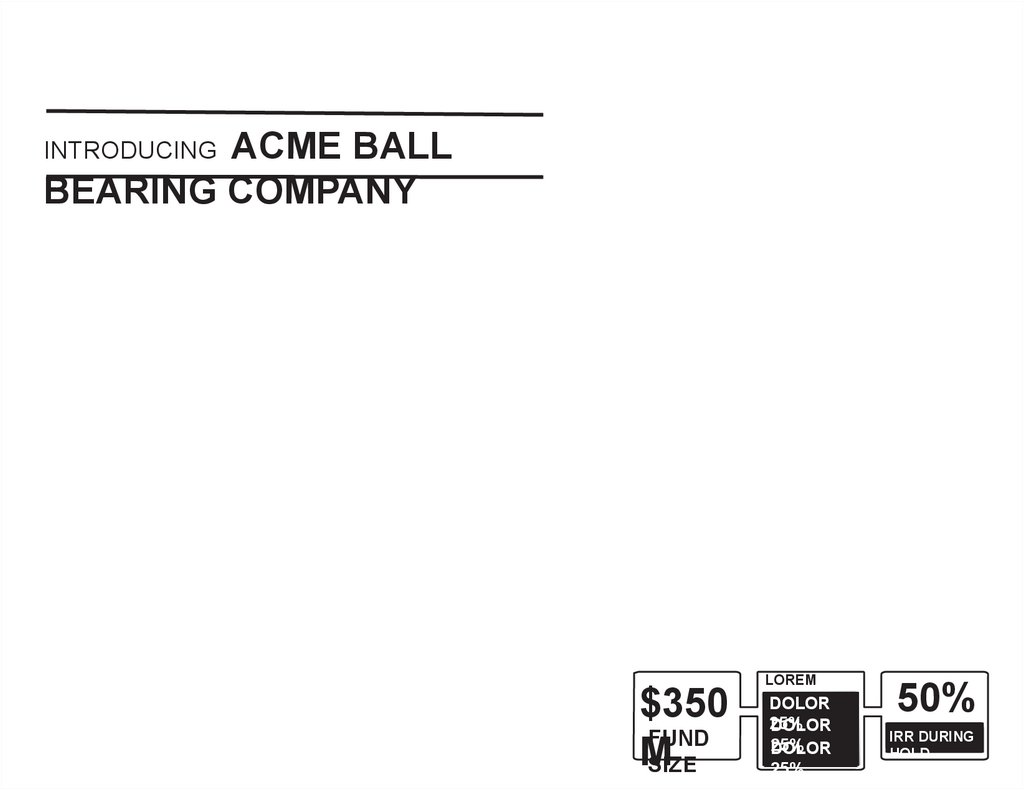

Introducing Acme Ball. Bearing сompany

1.

INTRODUCING ACME BALLBEARING COMPANY

$350

FUND

M

SIZE

LOREM

IPSUM

DOLOR

25%

DOLOR

25%

DOLOR

25%

50%

IRR DURING

HOLD

2.

THIS MEMORANDUM MAY NOT BE READ, CIRCULATED, DISTRIBUTED, REPRODUCED, OR OTHERWISE USED FORANY PURPOSE OTHER THAN THE PURPOSE DESCRIBED HEREIN.

WE DO NOT MAKE ANY REPRESENTATIONS OR WARRANTIES, EXPRESS OR IMPLIED, AS TO THE ACCURACY

OR COMPLETENESS OF THE INFORMATION PROVIDED INTHIS MEMORANDUM. WE RESERVETHE RIGHTTO AMEND,

REPLACE AND/OR SUPPLEMENTTHIS MEMORANDUM AT ANY TIME AND UNDERTAKE NO OBLIGATION TO PROVIDE

THE RECIPIENT WITH ACCESS TO ADDITIONAL INFORMATION. NOTHING IN THIS MEMORANDUM IS, OR SHOULD BE

RELIED UPON AS, A PROMISE OR REPRESENTATION AS TO THE FUTURE. THE INFORMATION CONTAINED IN THIS

MEMORANDUM DOES NOT PURPORT TO BE ALL- INCLUSIVE OR TO CONTAIN ALL THE INFORMATION AVAILABLE.

THIS MEMORANDUM DOES NOT CONSTITUTE AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY

SECURITIES. SUCH AN OFFER OR SOLICITATION, IF MADE, WOULD BE SOLELY BY WAY OF THE CONFIDENTIAL

PRIVATE PLACEMENT MEMORANDUM RELATING TO THE OPPORTUNITIES CONTEMPLATED IN THIS MEMORANDUM.

This summary, which contains brief, selected information pertaining to the anticipated business and affairs of the Fund, has been

prepared by the Fund Manager to provide general information about the Fund. This is not an offer to sell, or a solicitation of an

offer to buy securities, as such an offer or solicitation can only come through the offering’s PPM. This material cannot, and does

not, replace the PPM, and the PPM supersedes this material in all respects. This investment involves various degrees of risk,

including the speculative market and financing risks associated with fluctuations in the BALL BEARING market including tax

status, liquidity, and fees, expenses, and other risk factors. Please refer to the “Risk Factors” section of the PPM.

contact: somebody@acmeballs.com

3. FUND SUMMARY

FUNDSUMMAR

ACME

BALL

BEARING

C0MPAN

Y

KEY

INVESTMENT

IRR

DURING

METRICS

HOLD PERIOD

HOLD

9.12%

(PROJECTED)

5 Years

DIVIDEND HURDLE - CURRENT PAY

8%

PERFORMANCE SPLIT

(INVESTOR/MANAGER)

90/10

MANAGEMENT

FEE

1.75% on Asset Value

FIRST

YEAR

YIELD

(PROJECTED)

7.55%

LOCATION

Cayman Islands

FUND MANAGER

Somebody Services Ltd

•The Projected IRR is net of all carried interest,

managementBEARING

Somebody BALL BEARING

Services Ltd andAGENT

BALL

LEASING

the BALL BEARING Leasing AgentSomebody

is Somebody BALL

Leasing Pte

BEARING Leasing Pte Ltd (together “The Managers”)

Ltd

•The Managers handle all monetary issues and

Themanagement

projected decisions

yield over

the

hold

period

is based on

relating

to the

Fund.

The Managers

select, manage

and liquidatein

interests

specific

assumptions

thein selected

PrivateBALL

Placement

BEARING

Memorandom of the Fund

(the “ PPM ” ) including the

on behalf of the Fund.

projected exit scenarios.

4.

THE BIG IDEA IN 126WORDS:

Economists will tell you the world is “flat”. However, when you need to

go somewhere, you’ll find it’s actually big, round and you need an

airplane ticket to get there, and you won’t be flying alone.

In 2013, for the first time in history, 3 billion passengers will fly on

commercial airlines.

Where’s the opportunity in this? Today, there is tremendous upside from investing in

commercial air. They have long service lives, well understood value-curves and trade in a liquid

market. Planes are mobile, allowing quick movement of the asset from low demand to high

demand areas. It reasons then, if you know how to buy, sell and manage planes in today’s

market, you can make a high return on capital and accordingly manage risk.

This presentation is about our business in the acquisition, management and leasing of

commercial PLANES.

5.

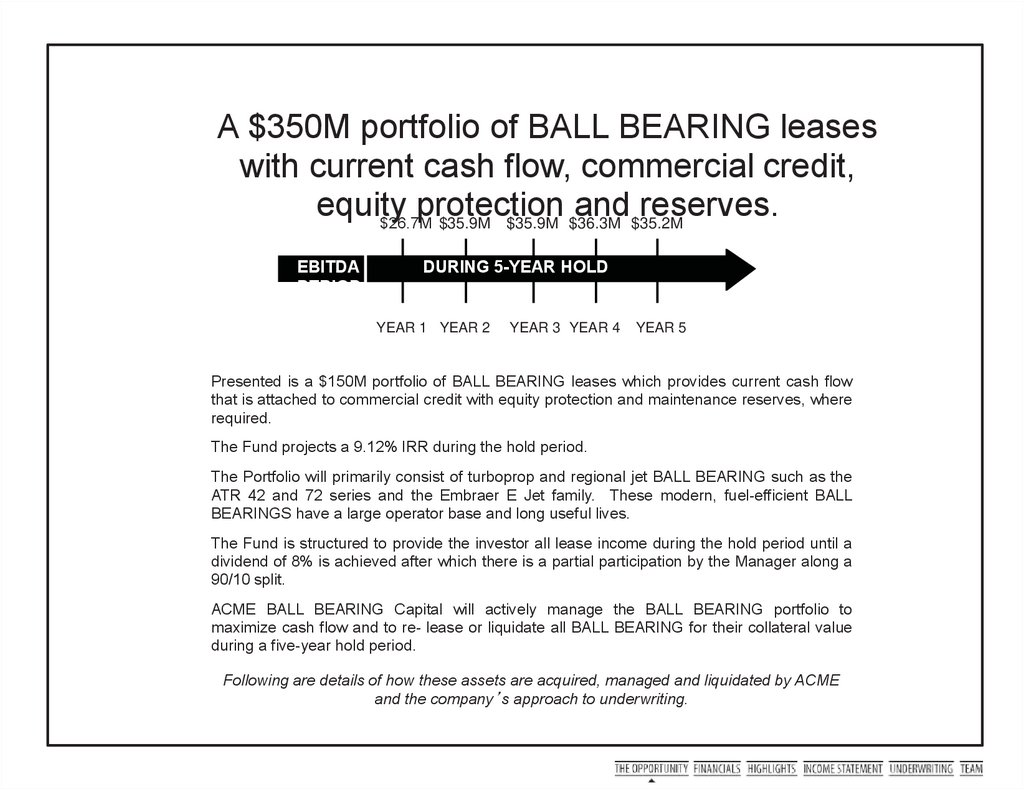

A $350M portfolio of BALL BEARING leaseswith current cash flow, commercial credit,

equity

protection and reserves.

$26.7M $35.9M $35.9M $36.3M $35.2M

EBITDA

PERIOD

DURING 5-YEAR HOLD

YEAR 1 YEAR 2

YEAR 3 YEAR 4

YEAR 5

Presented is a $150M portfolio of BALL BEARING leases which provides current cash flow

that is attached to commercial credit with equity protection and maintenance reserves, where

required.

The Fund projects a 9.12% IRR during the hold period.

The Portfolio will primarily consist of turboprop and regional jet BALL BEARING such as the

ATR 42 and 72 series and the Embraer E Jet family. These modern, fuel-efficient BALL

BEARINGS have a large operator base and long useful lives.

The Fund is structured to provide the investor all lease income during the hold period until a

dividend of 8% is achieved after which there is a partial participation by the Manager along a

90/10 split.

ACME BALL BEARING Capital will actively manage the BALL BEARING portfolio to

maximize cash flow and to re- lease or liquidate all BALL BEARING for their collateral value

during a five-year hold period.

Following are details of how these assets are acquired, managed and liquidated by ACME

and the company’s approach to underwriting.

6. PROFORMA

and INCOMEPROJECTIONS

BRIEFING. The proforma reflects a 5-year fund model in which, at the end of the hold

period, the value of all the funds assets are reconciled at their depreciated value, and investors

are repatriated with capital up to the 8% dividend return and split 90/10 with the Manager

thereafter. The Fund has a projected IRR of 9.12%. Depreciation is calculated on a straight line

basis over the term of each given lease. The starting value of the asset at the beginning of the

lease is the recorded purchase price, and depreciation continues evenly until the asset is valued

at its residual value at lease end.

SUMMARY INCOME

STATEMENT

YEAR 1

YEAR 2 YEAR 3 YEAR 4 YEAR 5

Revenue from BALL

BEARING Lease

$26.9 M

$36.1 M

$36.1 M

$36.5 M

$35.4 M

Operational Expenses

$0.24M

$0.24M

$0.24M

$0.24M

$0.24M

EBITDA

$26.7 M

$35.9 M

$35.9 M

$36.3 M

$35.2 M

NET INCOME

$11.3M

$13.8M

$14.5M

$16.8M

$18.5M

7.55

%

11.24

12.34

9.67

9.24

%

%

%

%

NET INCOME ON

$150M FUND

Y5

Y2

Y4

Y3

note: the income statement provided in PPM

supersedes this document

Net Income as

a % of

Investor Funds

Y1

7. FUND HIGHLIGHTS

BALL BEARING LEASES IN AN ACTIVE BUYER/SELLERBRIEFING:

The management team has purchased, leased and managed more than 360 BALL BEARING over a period of more

MARKET

than 40 years. The Fund is organized to lease regional turboprop and jet BALL BEARING in service of high growth markets to include

Asia and Latin America.

Passenger numbers are growing, reaching 3 billion in 2013, this figure is expected to double again by 2030. Much of this growth is

in regional airports and is dominated by Asian and Latin American passengers traveling to and from main service hubs. To service

this market you need the right BALL BEARING that are desired by regional operators. In support of this customer base, the Fund

buys high demand, fuel efficient, turbo prop and jet BALL BEARING and leases those BALL BEARING to regional airlines that are

servicing this high-growth travel market

THE FUND IS MANAGED BY EXPERTS IN REGIONAL BALL BEARING LEASING

ACME BALL BEARING Capitals’ management aims to proved high, single digit yields, based on the experience of having purchased and

remarketed commercial BALL BEARING throughout the world, including transactions completed in North America, Latin America, Europe and

Asia.The BALL BEARING Leasing Agent has an excellent worldwide reputation among airlines as a commercial BALL BEARING marketers that is

technically proficient with substantial aviation knowledge. Finally, the learning curve for the establishment of relationships within the industry,

technical expertise and experience managing operating leases and purchasing technicalities is steep. This provides a high barrier to entry into the

niche aviation finance industry and will limit serious competitors in the immediate future.

MODERN, HIGH-UTILITY BALL BEARING FLEET

The portfolio will primarily consist of turboprop and small regional jet BALL BEARING, such as the ATR 42 and 72 series and the Embraer E Jet

family. IN DEMAND: ATR has a backlog that stands at 221 BALL BEARING worth more then $5 billion at the end of 2012. These BALL BEARING

have a wide operator base.

OPERATIONAL LEASES TO AIRLINES HAVE BECOME THE MOST PROFITABLE

SEGMENT WITHIN THE COMMERCIAL AVIATION INDUSTRY

Strong growth in the global aviation market, especially in the Asian and Latin American regions, provide the Fund with numerous attractive leasing

opportunities. The Manager intends to acquire regional turboprop and jet BALL BEARING that are accretive to distributable cash flow per share,

while maintaining desirable portfolio characteristics in terms of BALL BEARING type, fleet age, lease term and geographic concentration.

In comparison to other alternative asset classes, aviation leasing assets provide current lease income and have clear, ascertainable market and

residual values. These types of cash generating assets provide stable returns in turbulent times.

8. PROFORMA INCOME STATEMENT WITH DETAIL

The proforma results are based on an initial equity investment of $150M by the investor group, which is to be invested in BALLBEARING such as the ATR 42 and 72 series and the Embraer PPM. The Fund will distribute to investors, quarterly, all

distributable free cash flow pro rata in accordance with their percentage interests. Distributable free cash flow distributions will be

made as follows: (i) First, 100% to the investor until 8% return is met;

(ii) Second, 90% to the Investor and 10% to the Manager in accordance with the PPM.

60months

CASH FLOW

PROJECTIONS

Revenue from BALL BEARING Leases

YEAR 1

$

26,974,000

YEAR 2

$

36,180,000

YEAR 3

$

36,180,000

YEAR 4

$

YEAR 5

36,599,000

$

35,000

- $

35,493,000

Less Fund Operating Expenses:

Audit

Fees (Fixed Fee

Annually)

Performance

Legal Fees (Fixed Monthly)

Director Salaries (Fixed Monthly)

Valuation Fees (Fixed Quarterly)

Travel Expenses (Fixed Monthly)

Total Operating Expenses

EBITDA

$ $

35,000 48,000

96,000

40,000

24,000

243,000

26,731,000

$

$

OTHER EXPENSES:

Interest Paid During Year

Asset Mgt Fees (Paid Quarterly)

Depreciation

Taxable Income

Income Tax Expense

Net Income - Accounting Purposes

$ $

-

35,000 -

$

48,000

96,000

40,000

24,000

24,000

243,000

35,937,000

$

35,000 - $

$

48,000

96,000

40,000

24,000

243,000

$

35,937,000

$

48,000

96,000

40,000

36,356,000

-

48,000

96,000

40,000

24,000

243,000

243,000

$

35,000

$

35,250,000

3,663,368

5,234,466

4,813,243

3,432,047

1,976,698

2,795,197

8,940,893

3,935,614

12,903,811

3,717,460

12,903,811

3,496,737

12,562,025

3,270,698

11,492,459

11,331,541

13,863,109

14,502,486

16,865,190

18,510,145

-

-

-

-

11,331,541

13,863,109

14,502,486

16,865,190

18,510,145

9. Underwriting FUNDAMENTALS

UnderwritingCOMMERCIAL

FUNDAMENTALS

BALL BEARING

THE MANAGER PROJECTS it will review as many as 20 lease opportunities in a month.

To efficiently underwrite this volume, we’ve developed screens and an underwriting

process:

ACME: FIRST LEVEL OF

UNDERWRITING SCREENS

1

2

3

4

5

6

LESSEE

STRONG

PROBABILI

OPERATO

LEAS

IS AN BALL

FINANCIA

LS

COLLATER

AL

TY OF

DEFAULT

RS

HISTORY

Does the

potential lessee

have the

necessary

financial

Whatcredibility?

is the lessee’s

net asset value?

What are their

revenues and

profitability?

Do we know

them?

Do they have a

history with other

lessors?

Is the potential

lessee able to

establish bank

guarantees for the

lease?

Is the potential

lessee able to

provide corporate

guarantees from a

parent or related

company with better

financials?

Based on due

diligence information

gathered, collateral

available and

financials, what is the

lessee’s probability

of default?

Is the probability of

default acceptable

and able to be

protected via

available guarantees

etc?

Has the potential

lessee operated

such BALL

BEARING

previously?

Does

the potential

lessee have

maintenance

facilities or do they

outsource?

Is the lessee able

to pay

maintenance

reserves?

E

TERM

S

BEARING

AVAILABLE

?

Are the lease

terms within our

standard terms?

Do we need to

move

off-target

from our desired

lease rate?

Is the period of

lease in line

with our

underwriting

requirements?

Is the correct BALL

BEARING

Is the available?

BALL

BEARING available

at a suitable target

cost and structure?

Are we able to

complete in an

acceptable

time period?

ACME BALL BEARING Leasing Pte Ltd’s management has over 40 years of BALL BEARING purchasing, selling and leasing management

experience covering in excess of 360 BALL BEARING in this time. In addition, ACME BALL BEARING Leasing’s long history as a well-known

part of the world-wide BALL BEARING industry provides the Fund with extensive relationships with airlines, BALL BEARING manufacturers,

BALL BEARING lessors, financial institutions and other participants in the industry, which will enhance the ability to source BALL BEARING and

lessees.

10.

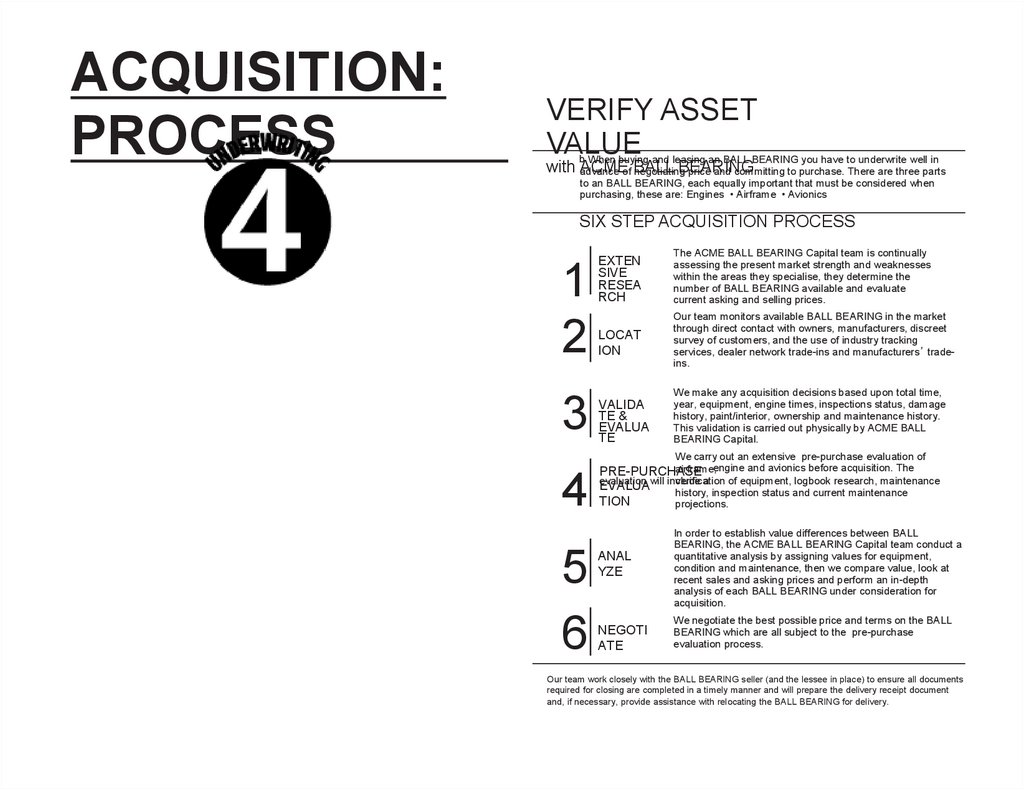

ACQUISITION:PROCESS

VERIFY ASSET

VALUE

b When buying and leasing an BALL BEARING you have to underwrite well in

with ACME

BEARING

advance of BALL

negotiating

price and committing to purchase. There are three parts

to an BALL BEARING, each equally important that must be considered when

purchasing, these are: Engines • Airframe • Avionics

SIX STEP ACQUISITION PROCESS

1

2

3

EXTEN

SIVE

RESEA

RCH

The ACME BALL BEARING Capital team is continually

assessing the present market strength and weaknesses

within the areas they specialise, they determine the

number of BALL BEARING available and evaluate

current asking and selling prices.

LOCAT

ION

Our team monitors available BALL BEARING in the market

through direct contact with owners, manufacturers, discreet

survey of customers, and the use of industry tracking

services, dealer network trade-ins and manufacturers’ tradeins.

VALIDA

TE &

EVALUA

TE

We make any acquisition decisions based upon total time,

year, equipment, engine times, inspections status, damage

history, paint/interior, ownership and maintenance history.

This validation is carried out physically by ACME BALL

BEARING Capital.

We carry out an extensive pre-purchase evaluation of

4

5

6

airframe,engine and avionics before acquisition. The

PRE-PURCHASE

verification

of equipment, logbook research, maintenance

evaluation will include

a

EVALUA

history, inspection status and current maintenance

TION

projections.

ANAL

YZE

NEGOTI

ATE

In order to establish value differences between BALL

BEARING, the ACME BALL BEARING Capital team conduct a

quantitative analysis by assigning values for equipment,

condition and maintenance, then we compare value, look at

recent sales and asking prices and perform an in-depth

analysis of each BALL BEARING under consideration for

acquisition.

We negotiate the best possible price and terms on the BALL

BEARING which are all subject to the pre-purchase

evaluation process.

Our team work closely with the BALL BEARING seller (and the lessee in place) to ensure all documents

required for closing are completed in a timely manner and will prepare the delivery receipt document

and, if necessary, provide assistance with relocating the BALL BEARING for delivery.

11.

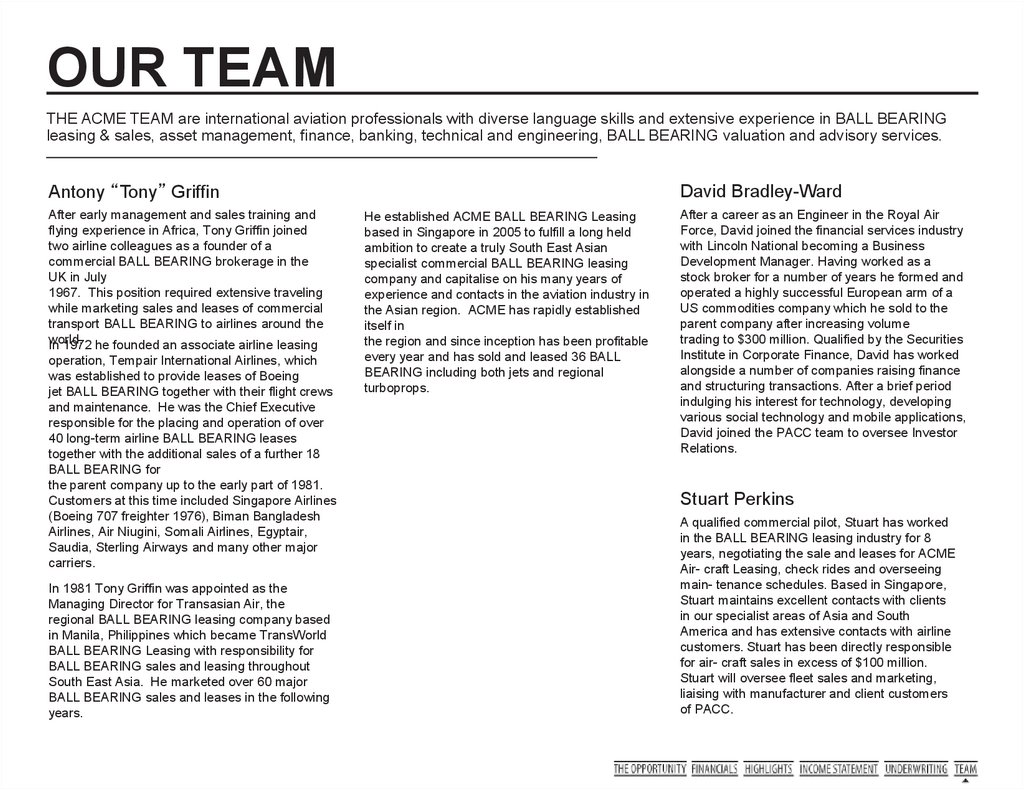

OUR TEAMTHE ACME TEAM are international aviation professionals with diverse language skills and extensive experience in BALL BEARING

leasing & sales, asset management, finance, banking, technical and engineering, BALL BEARING valuation and advisory services.

Antony “Tony” Griffin

After early management and sales training and

flying experience in Africa, Tony Griffin joined

two airline colleagues as a founder of a

commercial BALL BEARING brokerage in the

UK in July

1967. This position required extensive traveling

while marketing sales and leases of commercial

transport BALL BEARING to airlines around the

world.

In 1972 he founded an associate airline leasing

operation, Tempair International Airlines, which

was established to provide leases of Boeing

jet BALL BEARING together with their flight crews

and maintenance. He was the Chief Executive

responsible for the placing and operation of over

40 long-term airline BALL BEARING leases

together with the additional sales of a further 18

BALL BEARING for

the parent company up to the early part of 1981.

Customers at this time included Singapore Airlines

(Boeing 707 freighter 1976), Biman Bangladesh

Airlines, Air Niugini, Somali Airlines, Egyptair,

Saudia, Sterling Airways and many other major

carriers.

In 1981 Tony Griffin was appointed as the

Managing Director for Transasian Air, the

regional BALL BEARING leasing company based

in Manila, Philippines which became TransWorld

BALL BEARING Leasing with responsibility for

BALL BEARING sales and leasing throughout

South East Asia. He marketed over 60 major

BALL BEARING sales and leases in the following

years.

David Bradley-Ward

He established ACME BALL BEARING Leasing

based in Singapore in 2005 to fulfill a long held

ambition to create a truly South East Asian

specialist commercial BALL BEARING leasing

company and capitalise on his many years of

experience and contacts in the aviation industry in

the Asian region. ACME has rapidly established

itself in

the region and since inception has been profitable

every year and has sold and leased 36 BALL

BEARING including both jets and regional

turboprops.

After a career as an Engineer in the Royal Air

Force, David joined the financial services industry

with Lincoln National becoming a Business

Development Manager. Having worked as a

stock broker for a number of years he formed and

operated a highly successful European arm of a

US commodities company which he sold to the

parent company after increasing volume

trading to $300 million. Qualified by the Securities

Institute in Corporate Finance, David has worked

alongside a number of companies raising finance

and structuring transactions. After a brief period

indulging his interest for technology, developing

various social technology and mobile applications,

David joined the PACC team to oversee Investor

Relations.

Stuart Perkins

A qualified commercial pilot, Stuart has worked

in the BALL BEARING leasing industry for 8

years, negotiating the sale and leases for ACME

Air- craft Leasing, check rides and overseeing

main- tenance schedules. Based in Singapore,

Stuart maintains excellent contacts with clients

in our specialist areas of Asia and South

America and has extensive contacts with airline

customers. Stuart has been directly responsible

for air- craft sales in excess of $100 million.

Stuart will oversee fleet sales and marketing,

liaising with manufacturer and client customers

of PACC.

12.

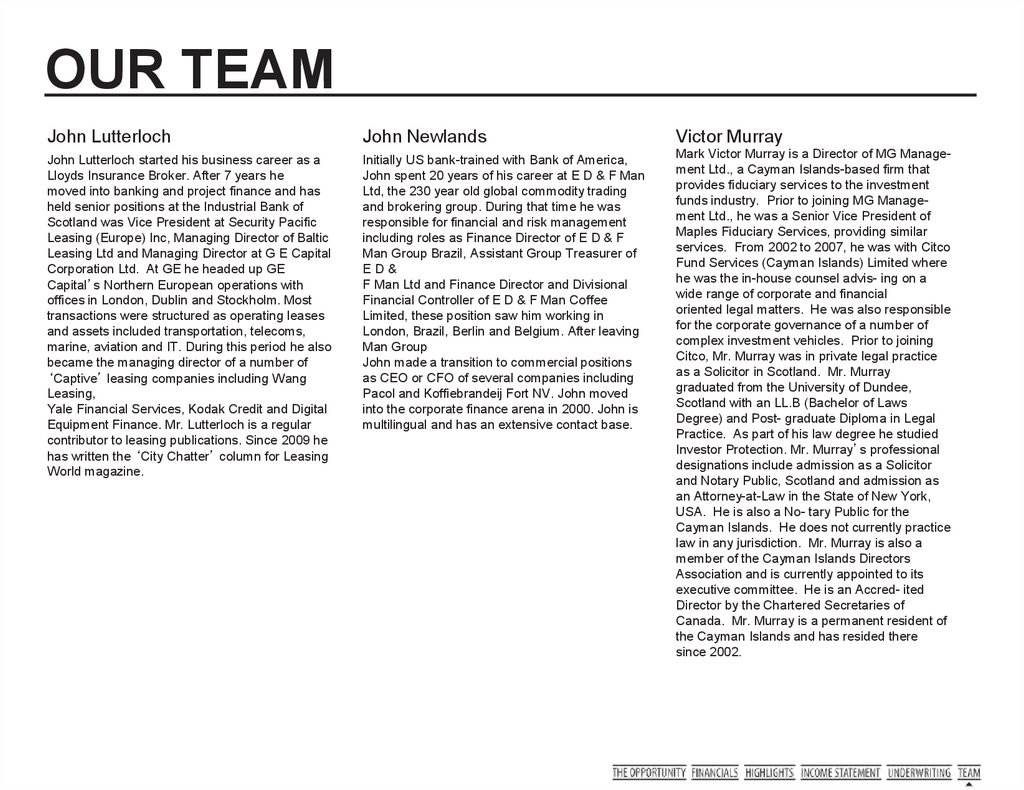

OUR TEAMJohn Lutterloch

John Newlands

Victor Murray

John Lutterloch started his business career as a

Lloyds Insurance Broker. After 7 years he

moved into banking and project finance and has

held senior positions at the Industrial Bank of

Scotland was Vice President at Security Pacific

Leasing (Europe) Inc, Managing Director of Baltic

Leasing Ltd and Managing Director at G E Capital

Corporation Ltd. At GE he headed up GE

Capital’s Northern European operations with

offices in London, Dublin and Stockholm. Most

transactions were structured as operating leases

and assets included transportation, telecoms,

marine, aviation and IT. During this period he also

became the managing director of a number of

‘Captive’ leasing companies including Wang

Leasing,

Yale Financial Services, Kodak Credit and Digital

Equipment Finance. Mr. Lutterloch is a regular

contributor to leasing publications. Since 2009 he

has written the ‘City Chatter’ column for Leasing

World magazine.

Initially US bank-trained with Bank of America,

John spent 20 years of his career at E D & F Man

Ltd, the 230 year old global commodity trading

and brokering group. During that time he was

responsible for financial and risk management

including roles as Finance Director of E D & F

Man Group Brazil, Assistant Group Treasurer of

ED&

F Man Ltd and Finance Director and Divisional

Financial Controller of E D & F Man Coffee

Limited, these position saw him working in

London, Brazil, Berlin and Belgium. After leaving

Man Group

John made a transition to commercial positions

as CEO or CFO of several companies including

Pacol and Koffiebrandeij Fort NV. John moved

into the corporate finance arena in 2000. John is

multilingual and has an extensive contact base.

Mark Victor Murray is a Director of MG Management Ltd., a Cayman Islands-based firm that

provides fiduciary services to the investment

funds industry. Prior to joining MG Management Ltd., he was a Senior Vice President of

Maples Fiduciary Services, providing similar

services. From 2002 to 2007, he was with Citco

Fund Services (Cayman Islands) Limited where

he was the in-house counsel advis- ing on a

wide range of corporate and financial

oriented legal matters. He was also responsible

for the corporate governance of a number of

complex investment vehicles. Prior to joining

Citco, Mr. Murray was in private legal practice

as a Solicitor in Scotland. Mr. Murray

graduated from the University of Dundee,

Scotland with an LL.B (Bachelor of Laws

Degree) and Post- graduate Diploma in Legal

Practice. As part of his law degree he studied

Investor Protection. Mr. Murray’s professional

designations include admission as a Solicitor

and Notary Public, Scotland and admission as

an Attorney-at-Law in the State of New York,

USA. He is also a No- tary Public for the

Cayman Islands. He does not currently practice

law in any jurisdiction. Mr. Murray is also a

member of the Cayman Islands Directors

Association and is currently appointed to its

executive committee. He is an Accred- ited

Director by the Chartered Secretaries of

Canada. Mr. Murray is a permanent resident of

the Cayman Islands and has resided there

since 2002.