")

")

Бизнес

БизнесПохожие презентации:

Operational Management of Insurance Business 5FNCE006C

1. Operational Management of Insurance Business 5FNCE006C

Hasan UmarovFinance Department

2. Teaching Calendar

3. Assessment methods and weightings

Assessmentname

Weighting

Qualifying Mark

Topics

covered

Assessment

type

Mid-term exam

40%

30%

Lecture 1-5

In-class Test

Final exam

60%

30%

Lecture 6-9

End-of-module

Final Exam

Finance Department

3

4. Sources:

Birds’ modern insurance law. Author: John BirdsFinance Department

4

5. Lecture 1 Introduction to Operational Management of Insurance Business

Finance Department6. The Chartered Insurance Institute (CII)

The CII is the largest professional body for the Insurance and Financial Planningprofessions, with more than 125,000 members in over 150 countries.

It was founded in Y1912.

Success in CII qualifications is universally

recognized as evidence of knowledge and

technical expertise.

CII offers a range of globally recognized

qualification and certification from entry level to

advanced professional designations, including:

1. Certificate in Insurance

2. Diploma in Insurance

3. Advanced Diploma in Insurance

Finance Department

6

7. The Chartered Insurance Institute (CII)

Finance Department7

8. Certificate in Insurance

This is an introductory level qualification designed for individualswho are new to the insurance industry or those in support or

administrative roles who wish to build a strong foundation in

insurance principles and practices.

To be awarded the Certificate in insurance, candidates must

complete three units (modules) to accumulate at least 40 credits.

For non-UK members, there are 3 units recommended to pass:

1. W01 – General Insurance Level 4 (Introduction to

Insurance Business)

2. WUE – Insurance Underwriting Level 5 (Operational

Management of Insurance Business)

3. WCE – Insurance Claims Handling Level 6 (Advanced

Study of Insurance Business)

Finance Department

8

9. Diploma in Insurance

It is an intermediate level qualification aimed at insurance professionalswho have foundational knowledge and are looking to deepen their technical

expertise, gain recognition and progress in their careers.

This intermediate level qualification provides a comprehensive

understanding of insurance principles, products, and practices, equipping

students with the knowledge and technical expertise required to operate

effectively within a dynamic and regulated financial services environment.

A minimum of 120 CII credits must be obtained for successful completion,

4 units recommended to pass:

1. M05 – Insurance Law core

2. M92 – Insurance Business and Finance core

3-4. There are 12 optional units (Insurance broking practice / personal

insurances / aviation and space insurance / reinsurance / others)

Finance Department

9

10. Advanced Diploma in Insurance

The Advanced Diploma in Insurance is a prestigious and globally respected qualification.It is designed for insurance professionals who wish to deepen their technical knowledge,

enhance their strategic thinking, and demonstrate leadership potential in the insurance

and risk management industry.

The Advanced Diploma comprises 3 core units and 2 option units from the CII

Insurance qualifications framework, providing a total of 290 CII credits on successful

completion.

1. 530 – Economics and Business core

2. 820 – Advanced claims core

3. 903 – Advanced insurance broking core

4-5. There are 9 optional units (Insurance corporate management / strategic

underwriting / advanced risk financing and transfer / others).

This qualification is widely recognized by employers and industry regulators and is a key

step toward achieving Chartered Insurer status – the industry’s gold standard for

professionalism and competence.

Finance Department

10

11. What is Risk ?

There is no single definition of risk.Finance Department

- Pure risk (loss or no

- Speculative risk (loss,

loss)

break-even or gain)

- Financial risk

- Non-financial risk

(measurable in monetary

terms)

(non-measurable in

monetary terms)

- Particular (or

diversifiable) risk

- Fundamental (nondiversifiable) risk

(affects only individuals or

communities)

(affects the entire economy

or large numbers of persons

or communities)

11

12. What is Insurance?

According to “American Risk and Insurance Association”:Insurance is the pooling of fortuitous losses by transfer of such risks to insurers, who

agree to indemnify insureds for such losses, to provide other pecuniary benefits on

their occurrence, or to render services connected with the risk.

Basic characteristics of Insurance:

1. Pooling of losses

2. Fortuitous event

3. Risk transfer

4. Indemnification

Finance Department

12

13. Ideal requirements of an insurable risk

1. A large number of exposure units (ideally, homogeneous)2. Accidental and unintentional loss

3. Loss must be determinable and measurable (e.g. emotional loss, reputational

damage, political instability cannot be measured)

4. Loss should not be catastrophic (reinsurance helps to cover a catastrophic loss)

5. The chance of loss must be calculated (insurer must be able to calculate both the

average frequency and the average severity of future losses with some accuracy)

6. The premium must be economically feasible

Finance Department

13

14. Insurance to society: costs and benefits

#Costs

#

Benefits

1

The cost of doing business increases

1

Peace of mind

2

Fraudulent claims

2

Indemnification for loss

3

Inflated claims

3

Improved cash flow

4

Reduction of fear and anxiety

5

Source of investments

6

Loss prevention & loss control

7

Enhancement of credits

8

Business continuity and expansion

9

Keep people in employment

Finance Department

14

15. Types of risk

Market risk• Arising from market movements (interest rates, FX,

equity prices, etc.)

Credit risk

• Risk of counterparty defaulting on obligations

Liquidity risk

• Inability to meet obligations when due

Operational risk

• Failure of internal processes, people, systems, or

external events

Compliance risk

• Regulatory and legal exposure

Reputation risk

• Loss due to negative public perception

Finance Department

15

16. Components of risk

Componentsof risk

Uncertainty

Level of risk

Peril and

hazard

1. Uncertainty doubt about the future, as a result of our incomplete knowledge;

2. Level of risk risk is assessed by insurers in terms of frequency (how often

something might happen) and severity (how costly it would be if it did happen);

3. Peril and hazard if a peril is something which gives rise to a loss, a hazard is

something that influences the operation of the peril.

Finance Department

16

17. Risk management

Risk management is a process that identifies loss exposures faced by anorganization and selects the most appropriate techniques for treating such

exposures.

There are 3 steps in risk management process:

Risk

identification

Risk

analysis

Risk control

Physical risk control

Financial risk control

Finance Department

17

18. Fundamental principles of insurance

Finance Department18

19. Self-insurance, co-insurance and dual insurance

Dual insurance is used whenthere are two or more policies

in force, which cover the same

risk (e.g. the policyholder may

accidentally cover his laptop

under his property insurance

and travel insurance)

Finance Department

19

20. Insurance market

Finance Department20

21. Types of insurance companies in terms of OWNERSHIP:

Insurancecompany

LLC / JSC

Finance Department

Mutual

Captive

21

22. Types of insurance companies in terms of FUNCTION:

Insurancecompany

Composite

Specialist

Direct

Takaful

Finance Department

Telephone, webbased

22

23. Types of intermediaries

Insuranceagents

• Appointed by the insurer

• It has a specific authority to act for

the benefit and on behalf of the

insurer

Insurance

brokers

• Appointed by the client

• Independent entity, engaged in

placing risks with insurance

companies

Finance Department

23

24. Classes of insurance

Personal linesinsurance

Private motor

insurance

Health

insurance

Household

insurance

Travel

insurance

Pet insurance

Personal lines insurance protects a policyholder from loss or damage to personal

property or from damages, for which the policyholder may be held personally

responsible.

Finance Department

24

25. Classes of insurance

Commerciallines

insurance

Property

insurance

Theft

insurance

Pecuniary

insurance

Liability

insurance

Cyber

insurance

Commercial lines insurance protects a business from loss of its business property

or damages, for which the company may be held liable.

Finance Department

25

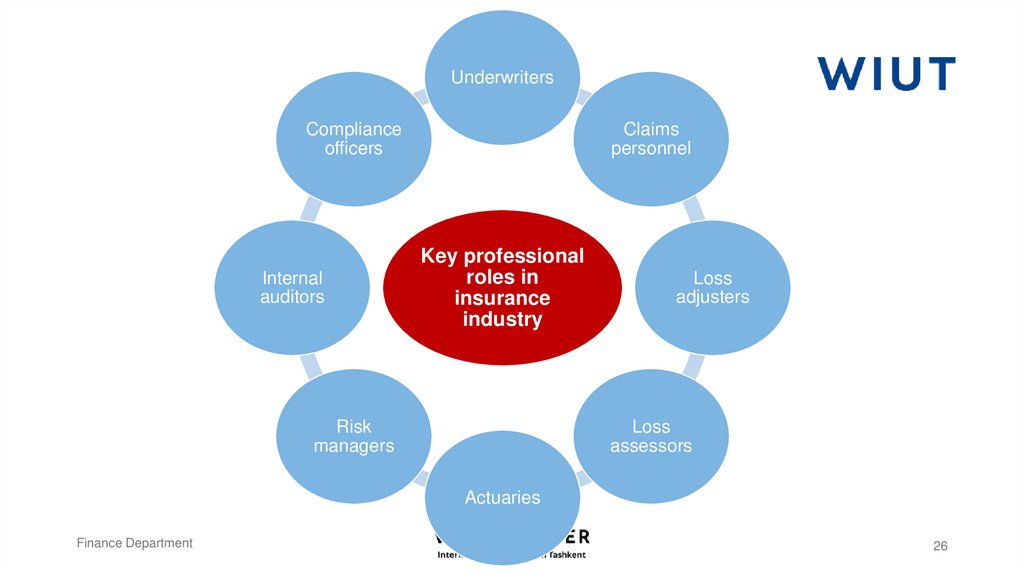

26.

UnderwritersCompliance

officers

Internal

auditors

Claims

personnel

Key professional

roles in

insurance

industry

Risk

managers

Loss

adjusters

Loss

assessors

Actuaries

Finance Department

26

27.

Rate makingOther (IT,

accounting,

legal)

Investments

Underwriting

Key

operations

of an

insurance

company

Reinsurance

Finance Department

Sales &

Marketing

Claims

management

27

28. Thank you

Finance Department28