Бизнес

БизнесПохожие презентации:

")

First Novartis Press Conference

1.

First Novartis Press Conference:Presentations given by

Daniel Vasella

(The Birth of Novartis)

and

Raymund Breu

(Financial Overview)

press1

2.

The Birth of Novartis:A Frontier of

Promises and Challenges

press2

3.

Novartis Aspirations - “Beat theBest”

To capture and hold worldwide leadership positions with a

strong, sustainable performance based on continuous

innovation

To create a fast, focused, flexible company with a passion for

competitiveness and implementation

press3

4.

Novartis: Global Leadershippress4

#1

in Life Sciences

#2

in Healthcare

#1

in Agribusiness

#2

in Medical Nutrition

5.

Advantages of Global LeadershipAchieve critical competitive mass

Reach scope and depth in our franchises

Hire, retain the best associates

Be our customers’ source of reference

Preferred partner for alliances and licensing cooperations

press5

6.

Integration:Rapid Pace, Decisive

Actions

press6

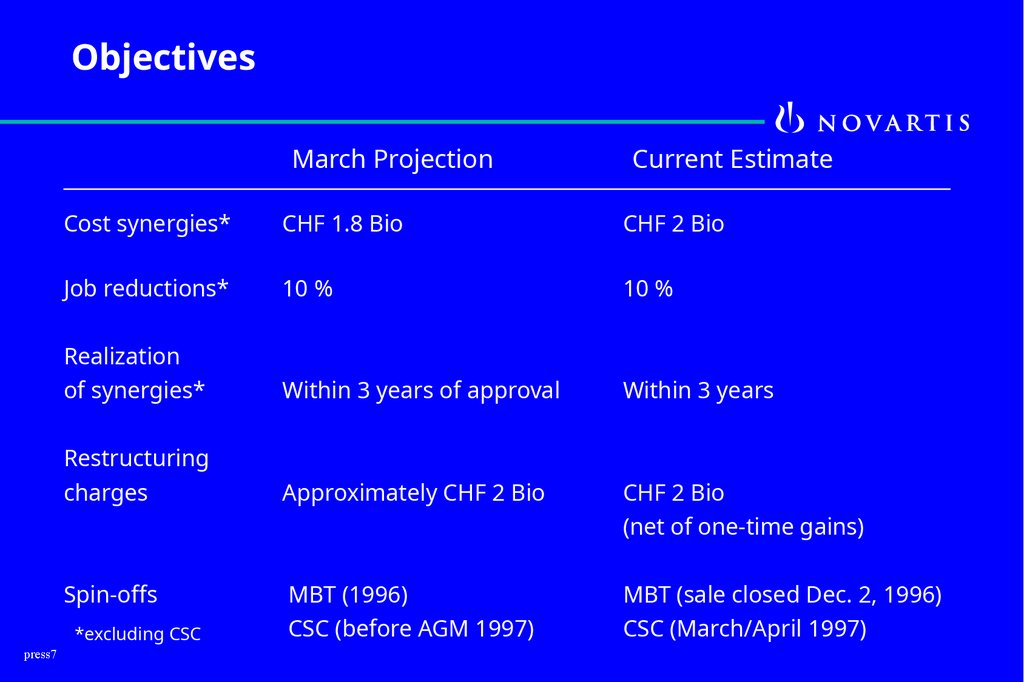

7.

ObjectivesMarch Projection

Current Estimate

Cost synergies*

CHF 1.8 Bio

CHF 2 Bio

Job reductions*

10 %

10 %

Realization

of synergies*

Within 3 years of approval

Within 3 years

Restructuring

charges

Approximately CHF 2 Bio

CHF 2 Bio

(net of one-time gains)

MBT (1996)

CSC (before AGM 1997)

MBT (sale closed Dec. 2, 1996)

CSC (March/April 1997)

Spin-offs

*excluding CSC

press7

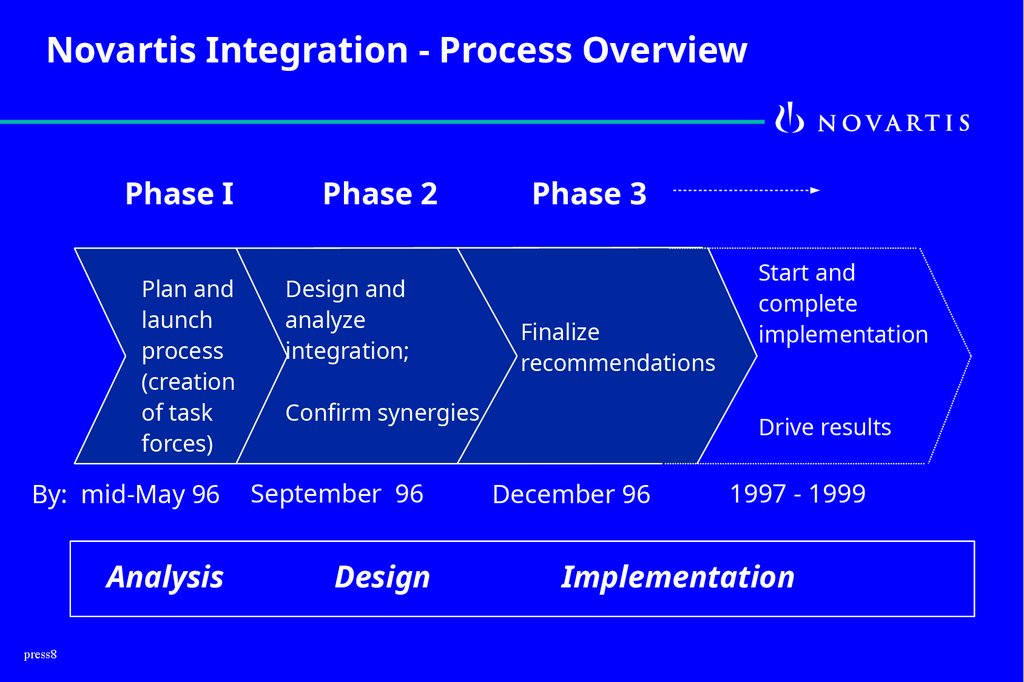

8.

Novartis Integration - Process OverviewPhase I

Phase 2

Plan and

launch

process

(creation

of task

forces)

Design and

analyze

integration;

By: mid-May 96

September 96

Analysis

Design

press8

Phase 3

Finalize

recommendations

Confirm synergies

Start and

complete

implementation

Drive results

December 96

1997 - 1999

Implementation

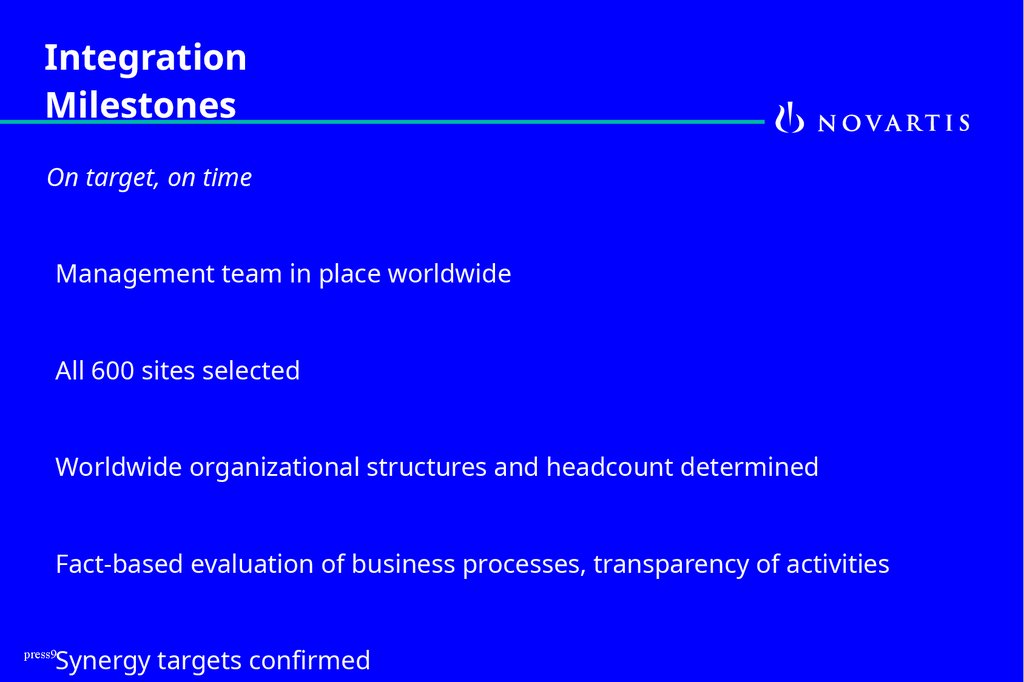

9.

IntegrationMilestones

On target, on time

Management team in place worldwide

All 600 sites selected

Worldwide organizational structures and headcount determined

Fact-based evaluation of business processes, transparency of activities

Synergy targets confirmed

press9

10.

Impact of Timing of RegulatoryApprovals

Facilitating factors overcoming approval waiting period:

Focus on ongoing business

Acquisitions (Azupharma) and divestments (MT, MBT)

Interim solutions (e.g. co-marketing agreements)

Focus on Human Resources

Proximity of sites

press10

11.

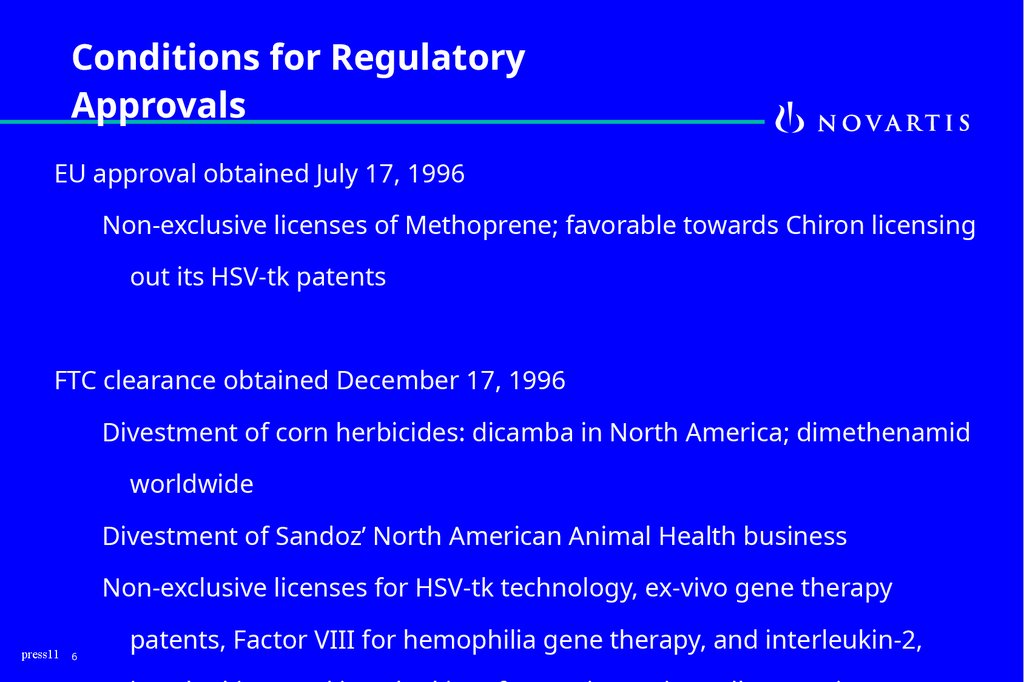

Conditions for RegulatoryApprovals

EU approval obtained July 17, 1996

Non-exclusive licenses of Methoprene; favorable towards Chiron licensing

out its HSV-tk patents

FTC clearance obtained December 17, 1996

Divestment of corn herbicides: dicamba in North America; dimethenamid

worldwide

Divestment of Sandoz’ North American Animal Health business

Non-exclusive licenses for HSV-tk technology, ex-vivo gene therapy

press11

6

patents, Factor VIII for hemophilia gene therapy, and interleukin-2,

12.

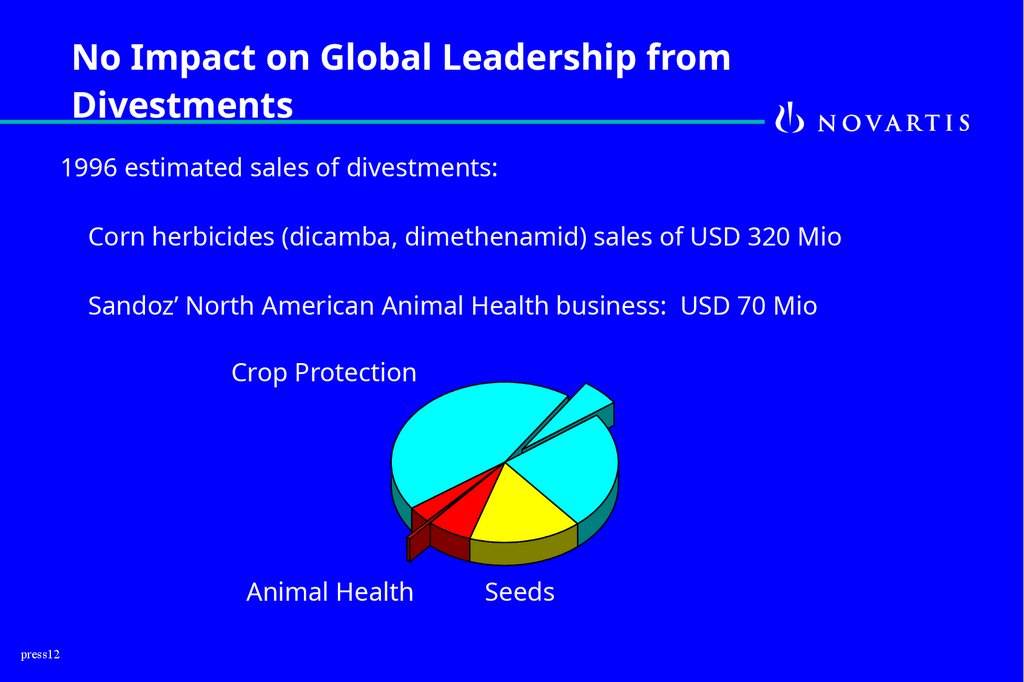

No Impact on Global Leadership fromDivestments

1996 estimated sales of divestments:

Corn herbicides (dicamba, dimethenamid) sales of USD 320 Mio

Sandoz’ North American Animal Health business: USD 70 Mio

Crop Protection

Animal Health

press12

Seeds

13.

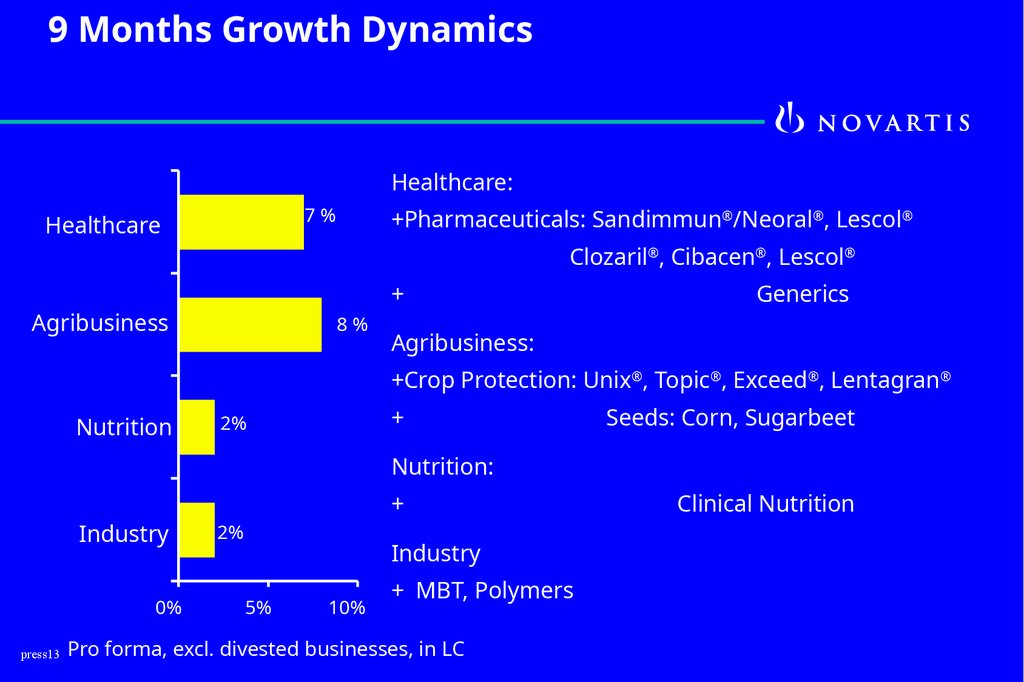

9 Months Growth DynamicsHealthcare:

7%

Healthcare

+Pharmaceuticals: Sandimmun®/Neoral®, Lescol®

Clozaril®, Cibacen®, Lescol®

+

Agribusiness

8%

Generics

Agribusiness:

+Crop Protection: Unix®, Topic®, Exceed®, Lentagran®

Nutrition

+

2%

Seeds: Corn, Sugarbeet

Nutrition:

Industry

0%

+

2%

Industry

5%

10%

+ MBT, Polymers

press13 Pro forma, excl. divested businesses, in LC

Clinical Nutrition

14.

Novartis Core Strategies for FutureGrowth

Innovation, including cutting-edge technologies

Customer focus

Operational excellence with continuing productivity improvements

press14

15.

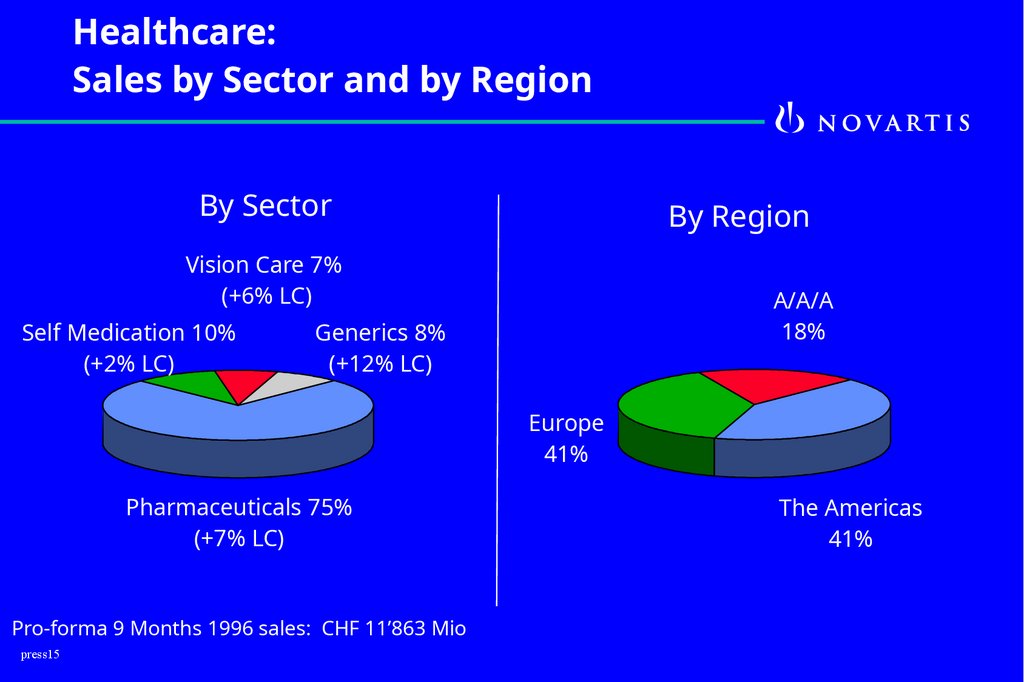

Healthcare:Sales by Sector and by Region

By Sector

By Region

Vision Care 7%

(+6% LC)

Self Medication 10%

(+2% LC)

A/A/A

18%

Generics 8%

(+12% LC)

Europe

41%

Pharmaceuticals 75%

(+7% LC)

Pro-forma 9 Months 1996 sales: CHF 11’863 Mio

press15

The Americas

41%

16.

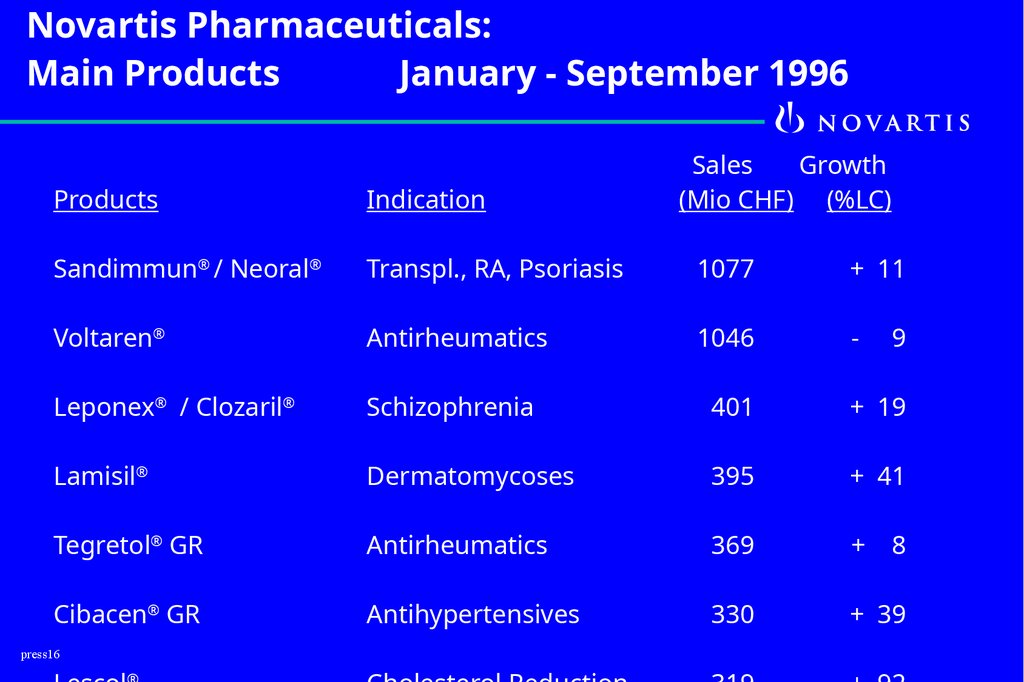

Novartis Pharmaceuticals:Main Products

January - September 1996

Sales

Growth

(Mio CHF) (%LC)

Products

Indication

Sandimmun® / Neoral®

Transpl., RA, Psoriasis

1077

+ 11

Voltaren®

Antirheumatics

1046

-

Leponex® / Clozaril®

Schizophrenia

401

+ 19

Lamisil®

Dermatomycoses

395

+ 41

Tegretol® GR

Antirheumatics

369

+

Cibacen® GR

Antihypertensives

330

+ 39

press16

9

8

17.

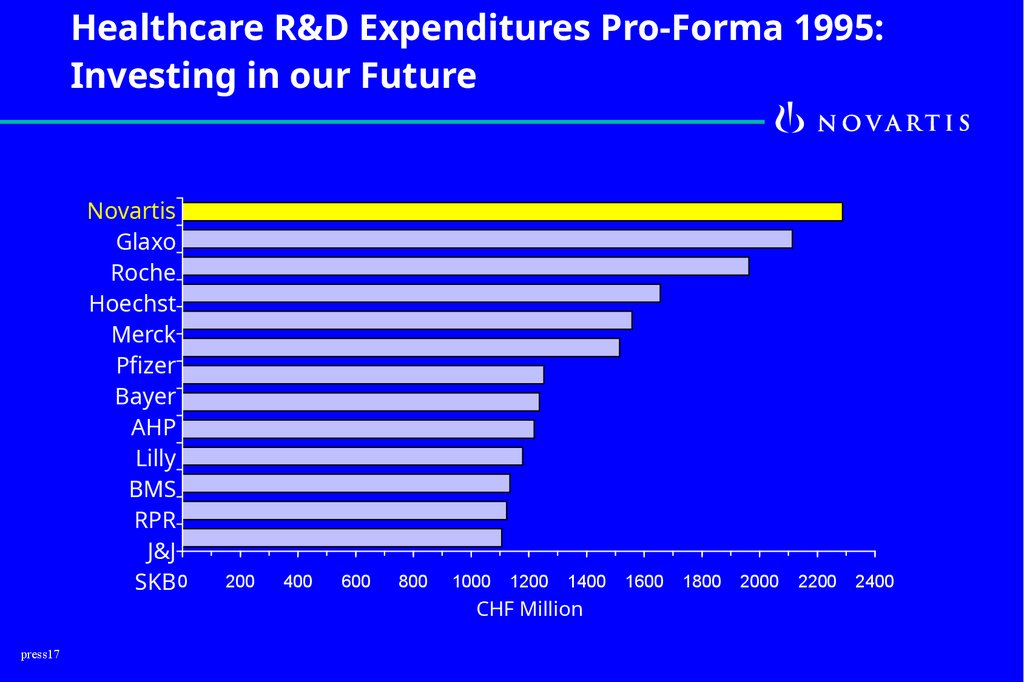

Healthcare R&D Expenditures Pro-Forma 1995:Investing in our Future

Novartis

Glaxo

Roche

Hoechst

Merck

Pfizer

Bayer

AHP

Lilly

BMS

RPR

J&J

SKB 0

press17

200

400

600

800

1000

1200

1400

CHF Million

1600

1800

2000

2200

2400

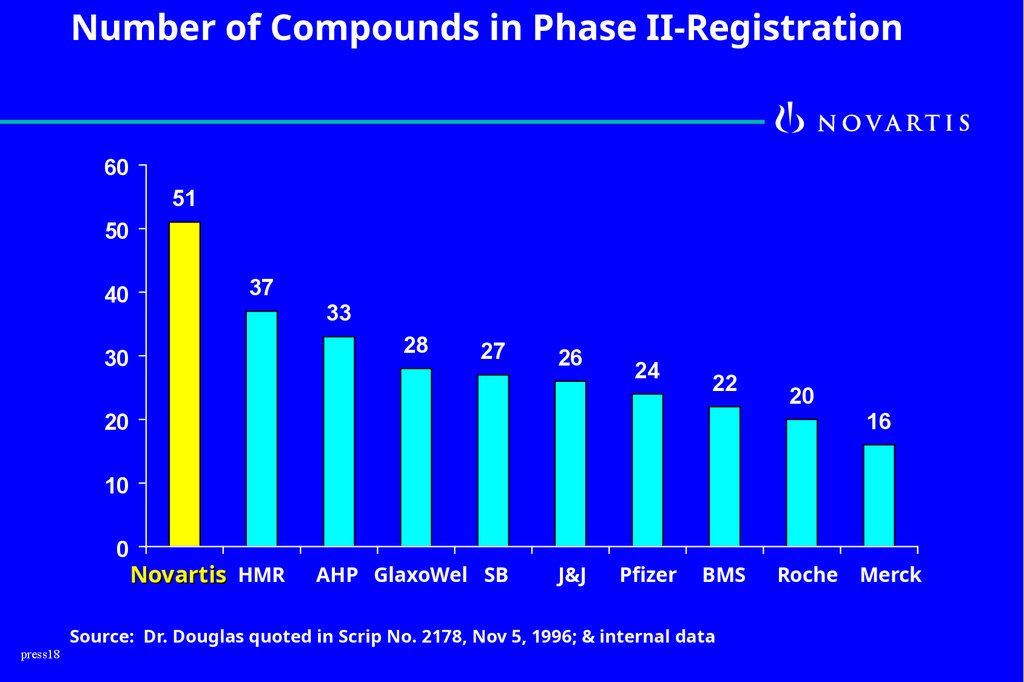

18.

Number of Compounds in Phase II-Registration60

51

50

40

37

33

28

30

27

26

24

22

20

16

20

10

0

press18

Novartis HMR

AHP GlaxoWel SB

J&J

Pfizer

BMS

Source: Dr. Douglas quoted in Scrip No. 2178, Nov 5, 1996; & internal data

Roche

Merck

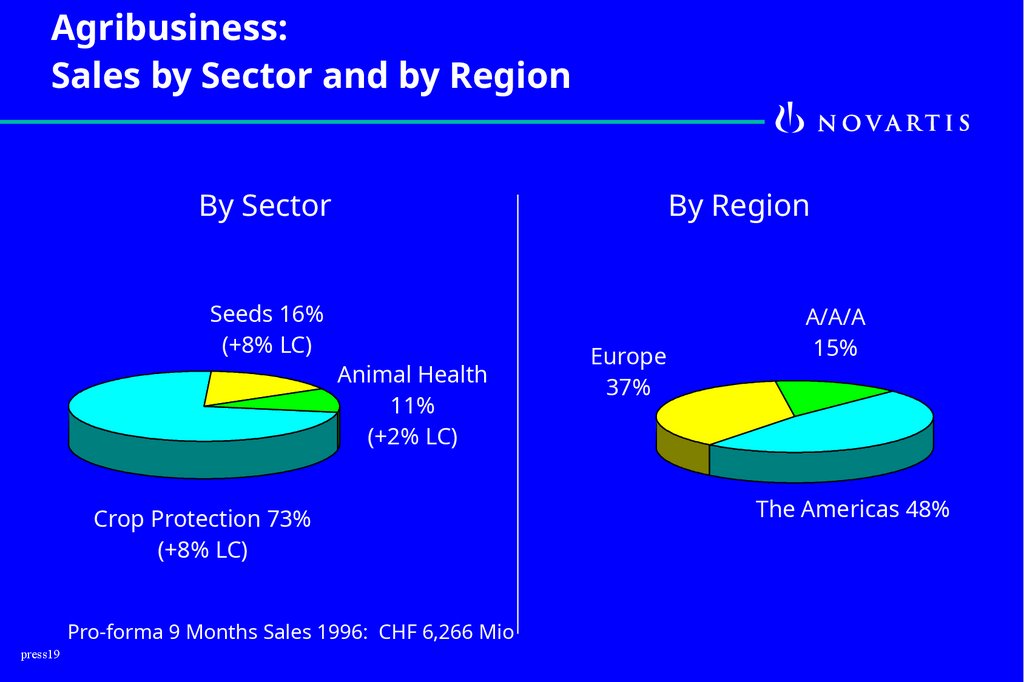

19.

Agribusiness:Sales by Sector and by Region

By Sector

Seeds 16%

(+8% LC)

By Region

Animal Health

11%

(+2% LC)

Crop Protection 73%

(+8% LC)

Pro-forma 9 Months Sales 1996: CHF 6,266 Mio

press19

Europe

37%

A/A/A

15%

The Americas 48%

20.

Crop Protection OutlookMaintain leadership position with profitability above industry average

Derive competitive advantage from innovation

Focus on core business areas, profitable markets and high value adding

products

Achieve continuous productivity improvements

press20

21.

Animal Health OutlookContinued dynamic growth with Program® in the companion animal

business

Tiamutin® (against bacterial infections in pig & poultry) brings growth

opportunities with worldwide Novartis organization

Flexible and lean infrastructure

Increasing market share both in companion and farm animals

press21

22.

Seeds:Outlook

Focus on high value-added products and markets in corn, sugarbeet,

vegetables, flowers and oilseeds

Forceful global #2 position in corn

Strengthened competitive advantage through leadership in relevant applied

technologies

Above industry-average profitability and growth

press22

23.

Novartis Top Rankings in Nutrition# 1 brand in jarred baby food

# 1 health food marketer in Europe

# 2 worldwide in clinical nutrition

press23

24.

Nutrition - OutlookFocus on high growth, high value-added areas

Health-oriented products

Above industry-average volume growth

press24

25.

Building NovartisGlobal leadership in core areas with broad and deep market penetration

Top-ranked position in R&D investment creates innovation powerhouse

Commitment to stay in the forefront with accelerated growth

Dynamic earnings potential

Demerger unlocks shareholder value with enhanced focus on life sciences

Strong balance sheet

Fulfill the powerful logic of Novartis

press25

26.

The Promise of NovartisTo accomplish great things, we must not

only act but also believe

Anatole France

press26

27.

Financial Overviewpress27

28.

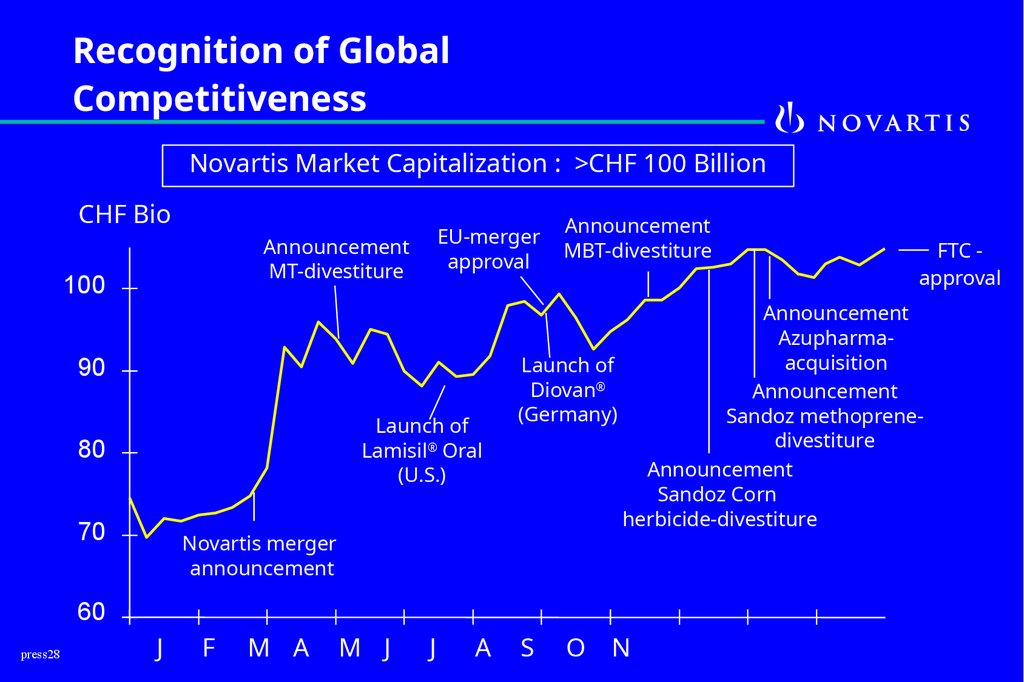

Recognition of GlobalCompetitiveness

Novartis Market Capitalization : >CHF 100 Billion

CHF Bio

EU-merger

approval

Announcement

MT-divestiture

100

90

Launch of

Lamisil® Oral

(U.S.)

80

70

Novartis merger

announcement

Announcement

MBT-divestiture

Announcement

Azupharmaacquisition

Launch of

Diovan®

Announcement

(Germany)

Sandoz methoprenedivestiture

Announcement

Sandoz Corn

herbicide-divestiture

60

press28

J

F

M A

M J

J

A

FTC approval

S

O

N

29.

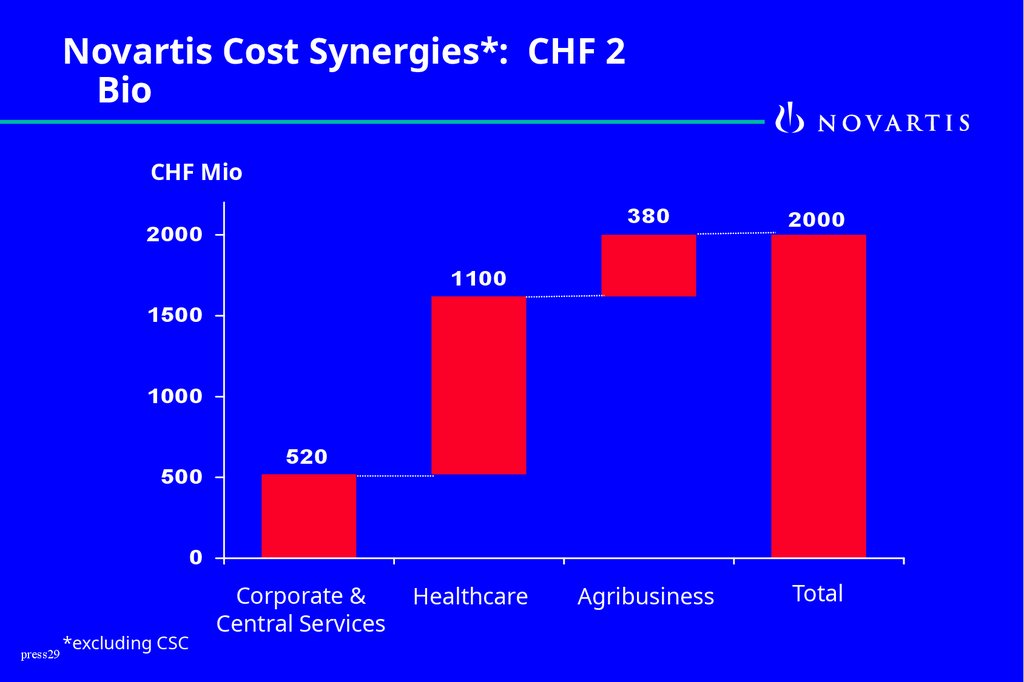

Novartis Cost Synergies*: CHF 2Bio

CHF Mio

2000

380

2000

Agribusiness

Total

1100

1500

1000

500

520

0

press29

*excluding CSC

Corporate &

Central Services

Healthcare

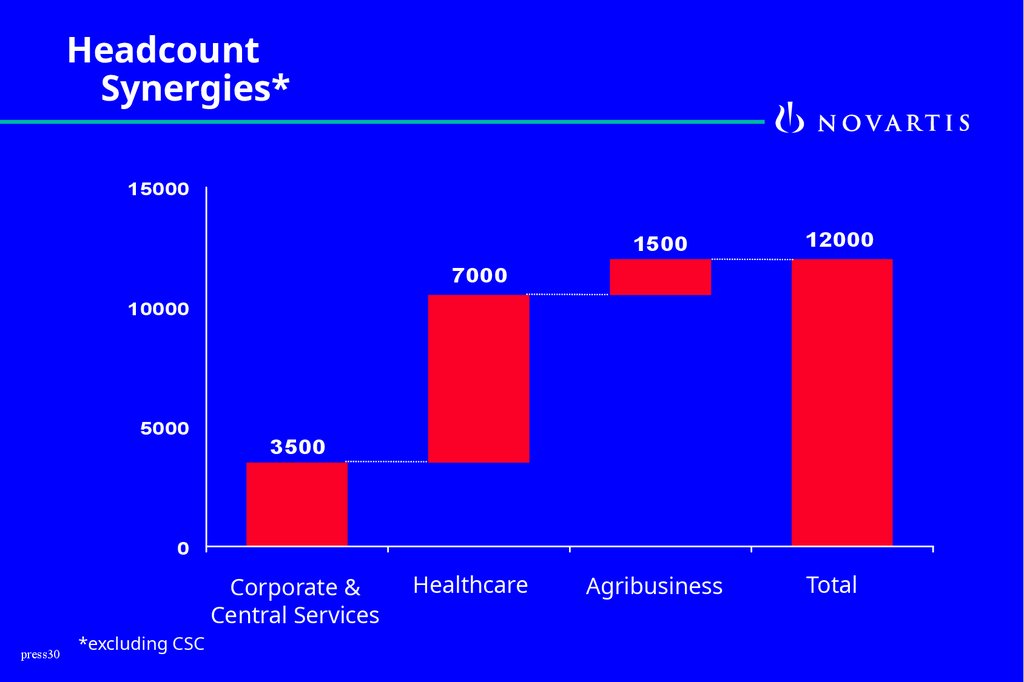

30.

HeadcountSynergies*

15000

1500

12000

Agribusiness

Total

7000

10000

5000

3500

0

Corporate &

Central Services

press30

*excluding CSC

Healthcare

31.

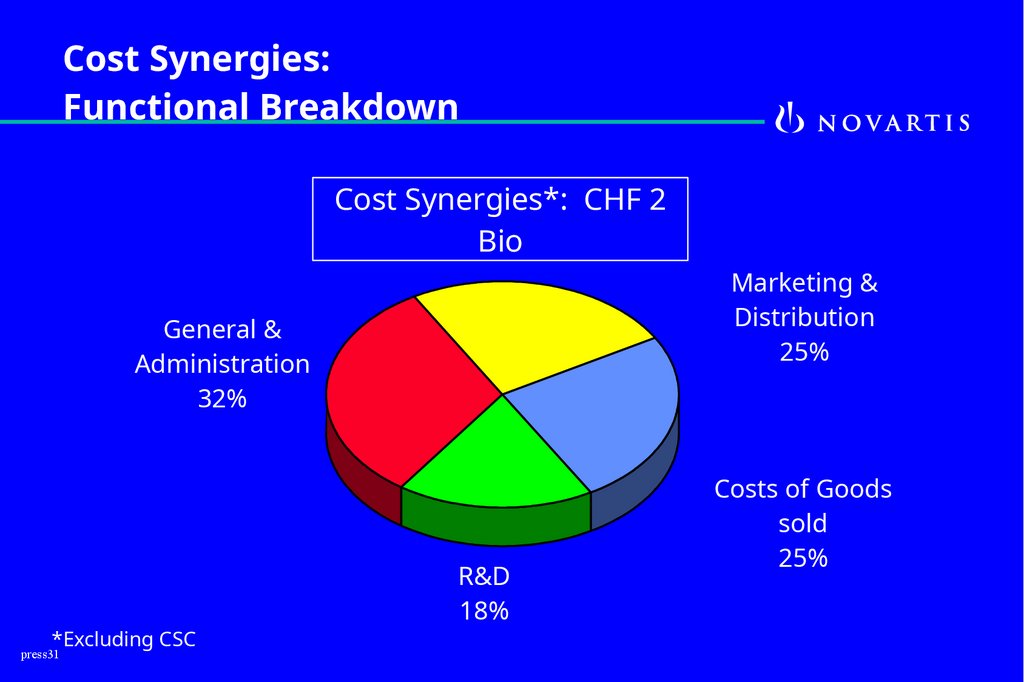

Cost Synergies:Functional Breakdown

Cost Synergies*: CHF 2

Bio

Marketing &

Distribution

25%

General &

Administration

32%

*Excluding CSC

press31

R&D

18%

Costs of Goods

sold

25%

32.

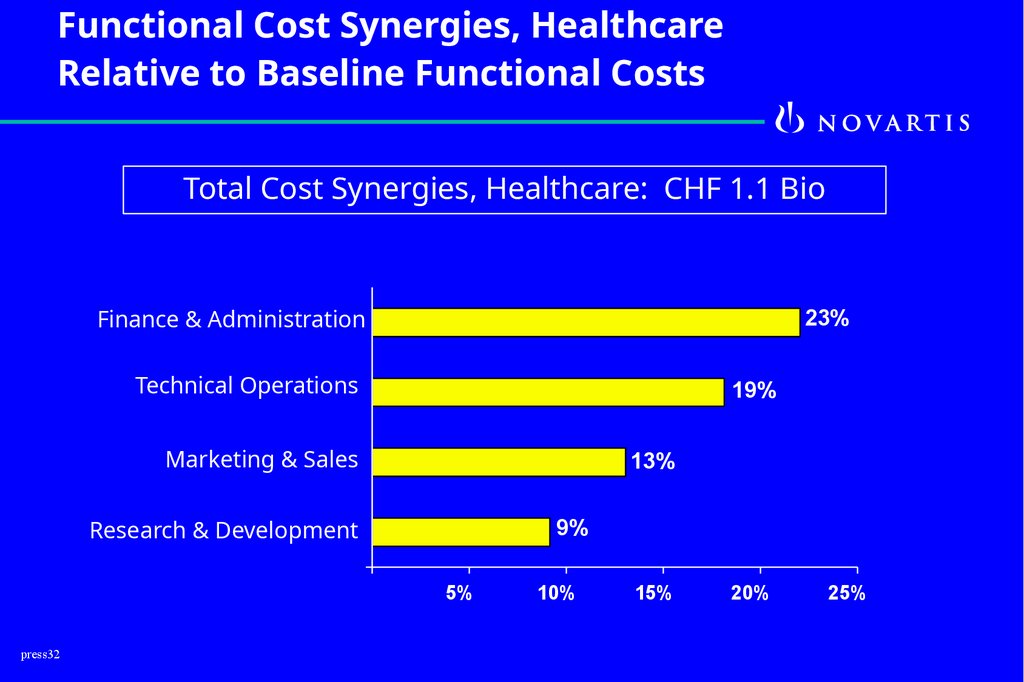

Functional Cost Synergies, HealthcareRelative to Baseline Functional Costs

Total Cost Synergies, Healthcare: CHF 1.1 Bio

Finance & Administration

23%

Technical Operations

19%

Marketing & Sales

13%

Research & Development

9%

5%

press32

10%

15%

20%

25%

33.

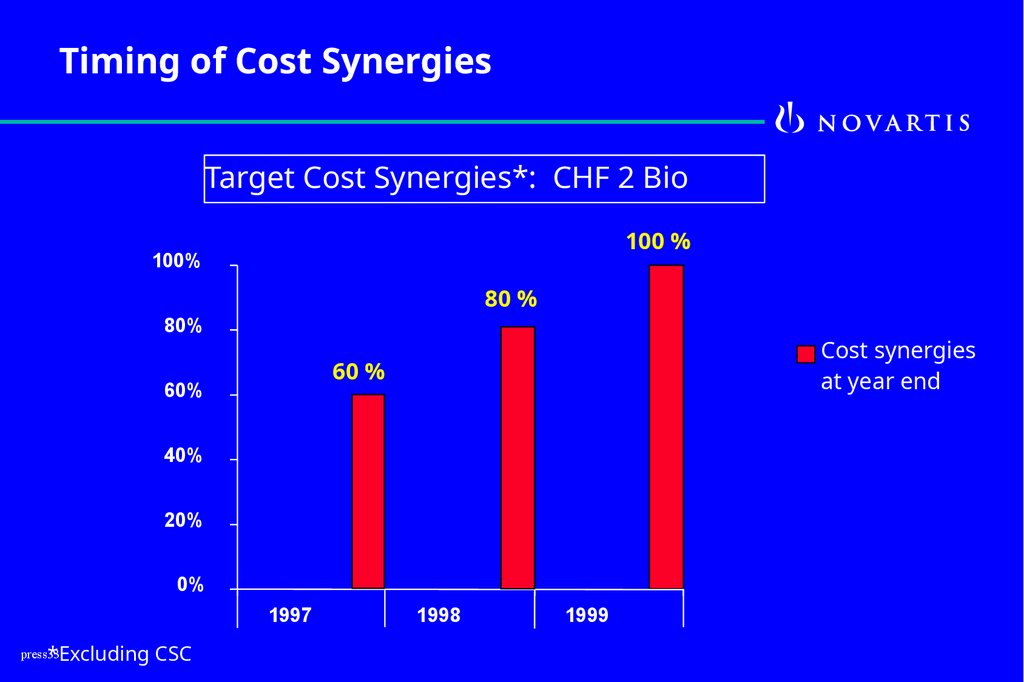

Timing of Cost SynergiesTarget Cost Synergies*: CHF 2 Bio

100 %

100%

80 %

80%

Cost synergies

at year end

60 %

60%

40%

20%

0%

1997

press33

*Excluding CSC

1998

1999

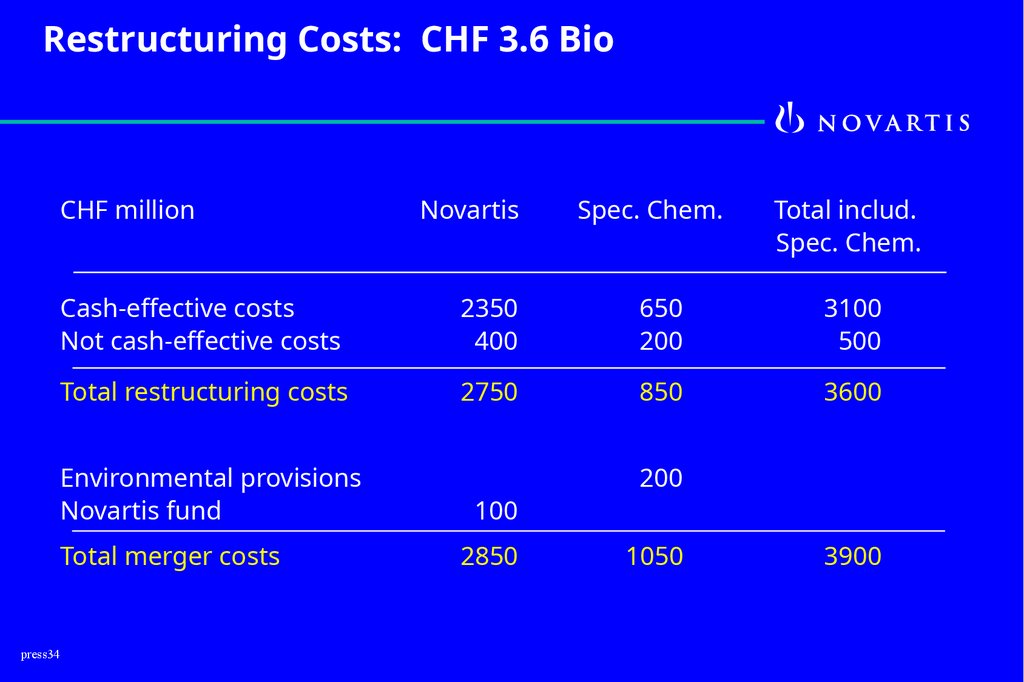

34.

Restructuring Costs: CHF 3.6 BioCHF million

press34

Novartis

Spec. Chem.

Total includ.

Spec. Chem.

Cash-effective costs

Not cash-effective costs

2350

400

650

200

3100

500

Total restructuring costs

2750

850

3600

Environmental provisions

Novartis fund

100

Total merger costs

2850

200

1050

3900

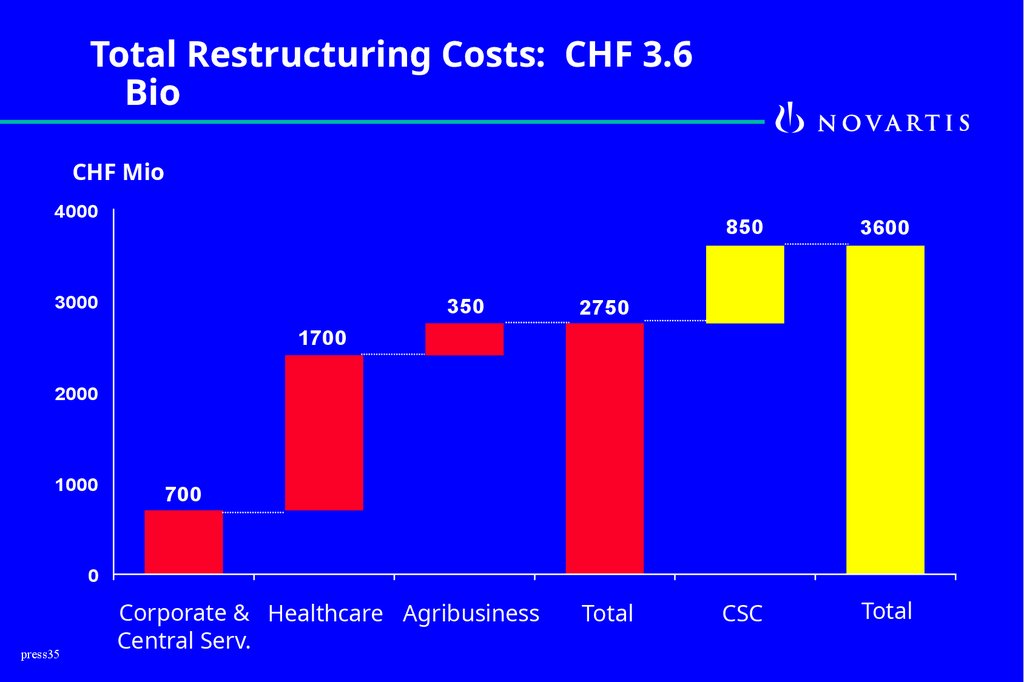

35.

Total Restructuring Costs: CHF 3.6Bio

CHF Mio

4000

3000

350

850

3600

CSC

Total

2750

1700

2000

1000

700

0

press35

Corporate & Healthcare Agribusiness

Central Serv.

Total

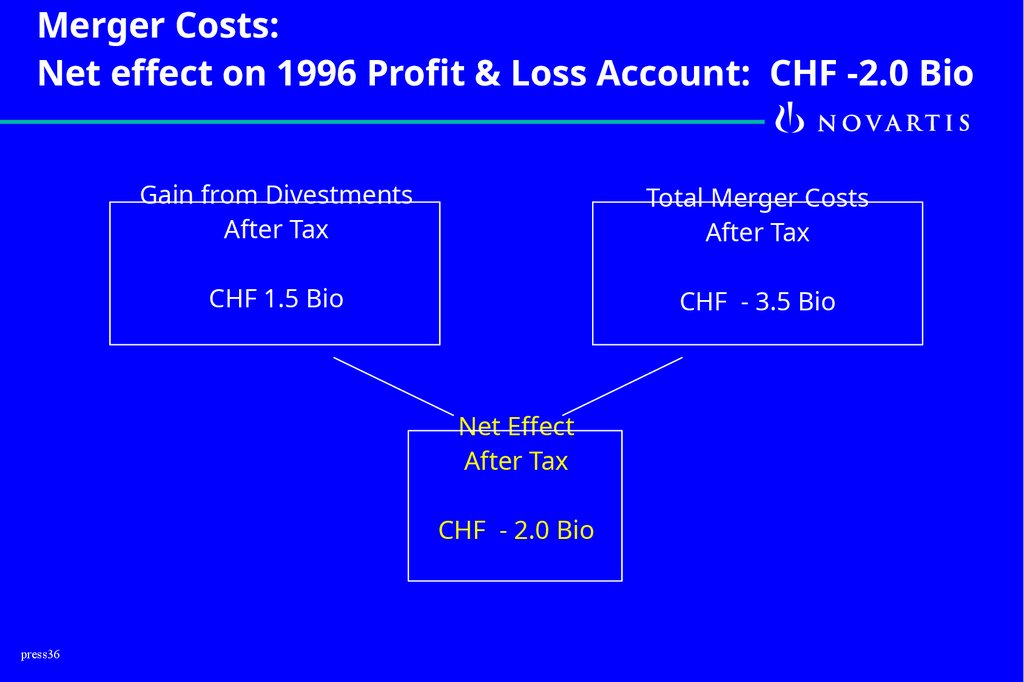

36.

Merger Costs:Net effect on 1996 Profit & Loss Account: CHF -2.0 Bio

Gain from Divestments

After Tax

Total Merger Costs

After Tax

CHF 1.5 Bio

CHF - 3.5 Bio

Net Effect

After Tax

CHF - 2.0 Bio

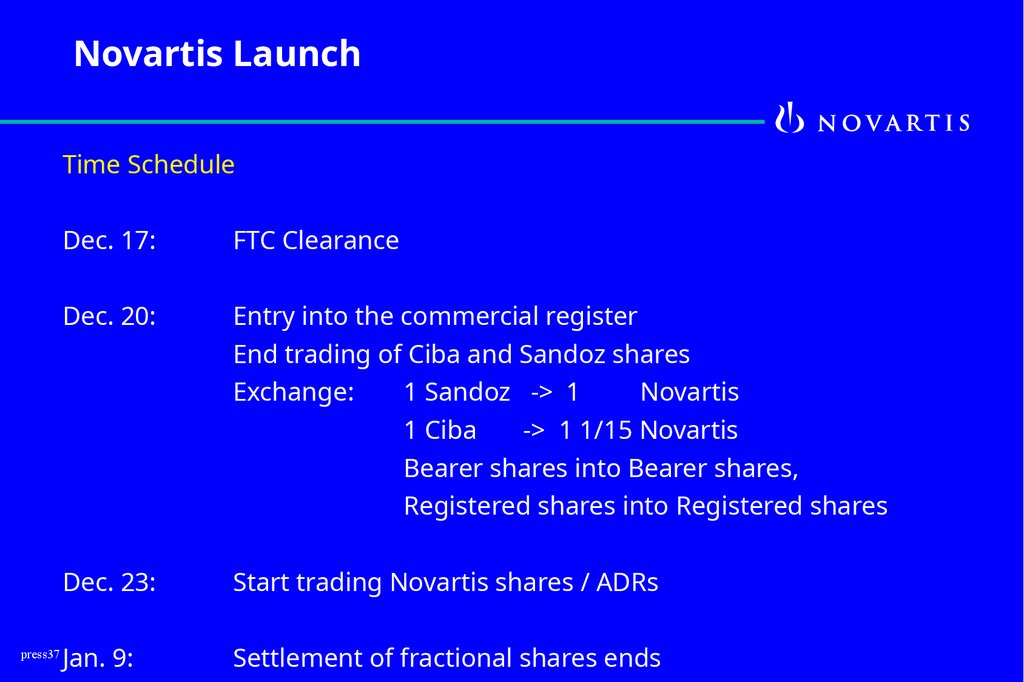

press36

37.

Novartis LaunchTime Schedule

Dec. 17:

FTC Clearance

Dec. 20:

Entry into the commercial register

End trading of Ciba and Sandoz shares

Exchange:

1 Sandoz -> 1

1 Ciba

Novartis

-> 1 1/15 Novartis

Bearer shares into Bearer shares,

Registered shares into Registered shares

press37

Dec. 23:

Start trading Novartis shares / ADRs

Jan. 9:

Settlement of fractional shares ends

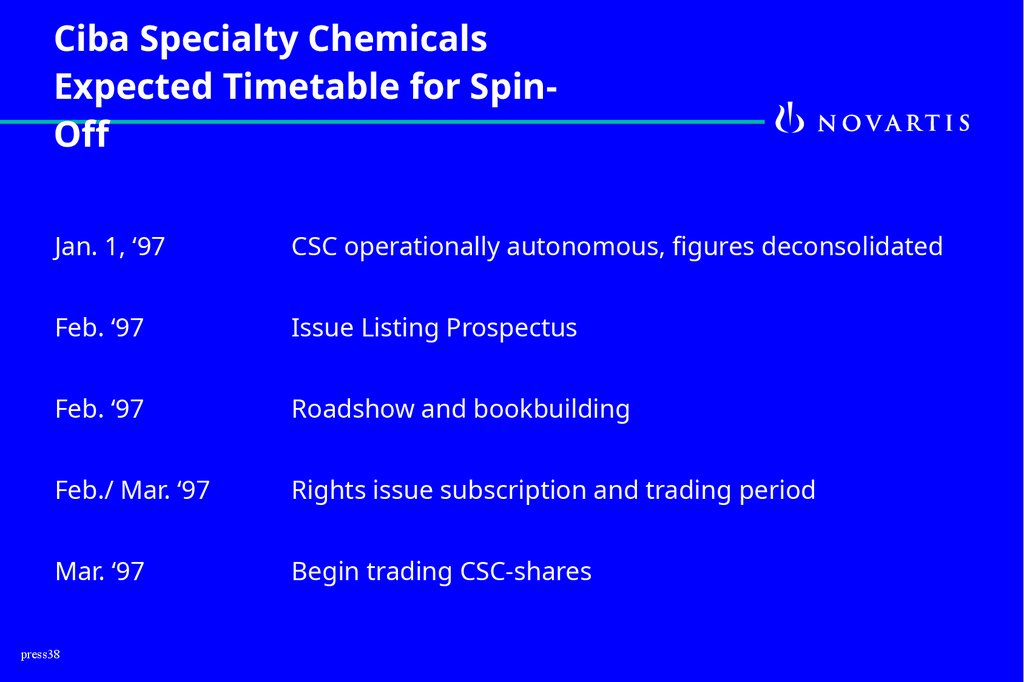

38.

Ciba Specialty ChemicalsExpected Timetable for SpinOff

Jan. 1, ‘97

CSC operationally autonomous, figures deconsolidated

Feb. ‘97

Issue Listing Prospectus

Feb. ‘97

Roadshow and bookbuilding

Feb./ Mar. ‘97

Rights issue subscription and trading period

Mar. ‘97

Begin trading CSC-shares

press38