Похожие презентации:

KazMunayGas_Economic_Audit_Presentation (1)

1.

Economic Audit of KazMunayGasCorporate & Industry Economic Analysis (Oil & Gas Sector, Kazakhstan)

Team: ____________________ | Date: 09.02.2026

2.

Agenda• 1) Macro context: Kazakhstan oil & gas sector (2024–2025)

• 2) Market structure and external factors (inflation, FX, regulation)

• 3) KazMunayGas: business model, revenues, costs, profitability (2023–2024)

• 4) Problems, economic impact, and recommendations

All figures and claims are sourced in the written report (no new content added).

3.

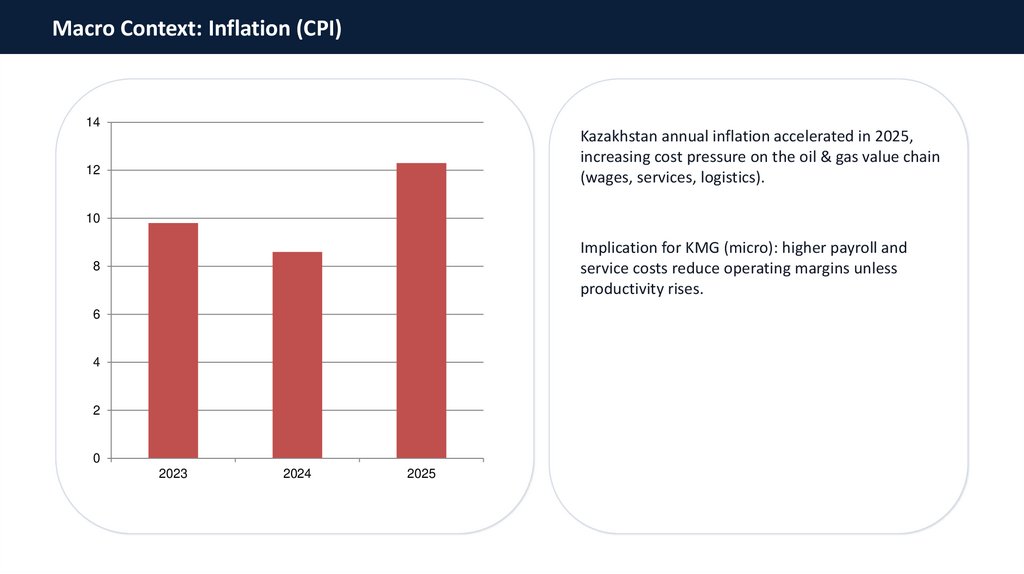

Macro Context: Inflation (CPI)14

Kazakhstan annual inflation accelerated in 2025,

increasing cost pressure on the oil & gas value chain

(wages, services, logistics).

12

10

Implication for KMG (micro): higher payroll and

service costs reduce operating margins unless

productivity rises.

8

6

4

2

0

2023

2024

2025

4.

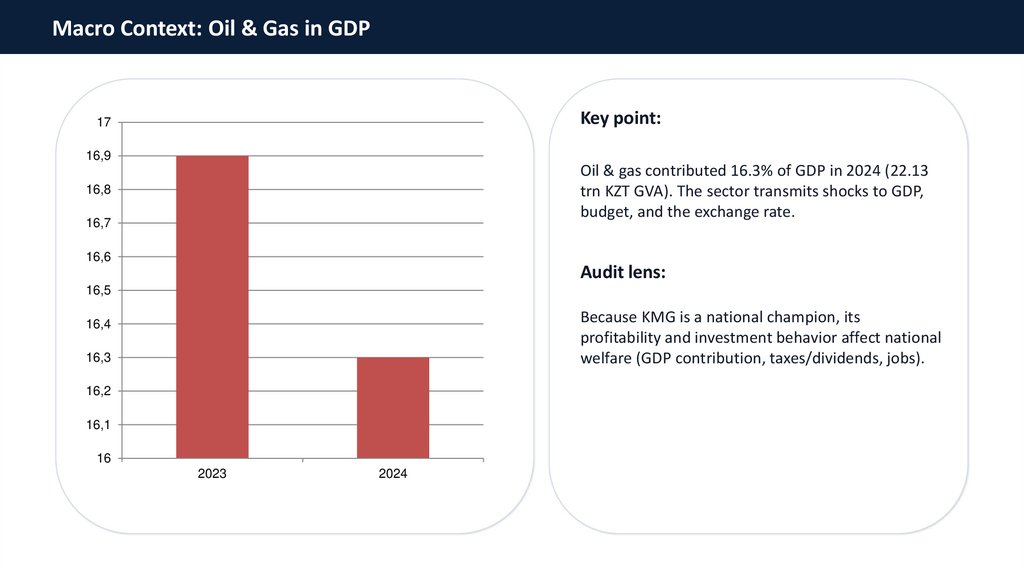

Macro Context: Oil & Gas in GDPKey point:

17

16,9

Oil & gas contributed 16.3% of GDP in 2024 (22.13

trn KZT GVA). The sector transmits shocks to GDP,

budget, and the exchange rate.

16,8

16,7

16,6

Audit lens:

16,5

Because KMG is a national champion, its

profitability and investment behavior affect national

welfare (GDP contribution, taxes/dividends, jobs).

16,4

16,3

16,2

16,1

16

2023

2024

5.

Market Structure & External FactorsMarket structure (Kazakhstan oil & gas): Oligopoly with strong state participation

• High entry barriers: capital intensity, licensing, infrastructure access, geology risk

• Upstream is largely a global price-taker (Brent-linked); transport/refining can have more local market

power

• External factors matter immediately: inflation (costs), USD/KZT (translation + natural hedge), regulation

(taxes, environmental rules)

• Example of regulatory exposure: KMG International faced Romania turnover tax under Law No.

296/2023 (2024)

KMG reported average USD/KZT rising from 456.21 (2023) to 469.31 (2024).

6.

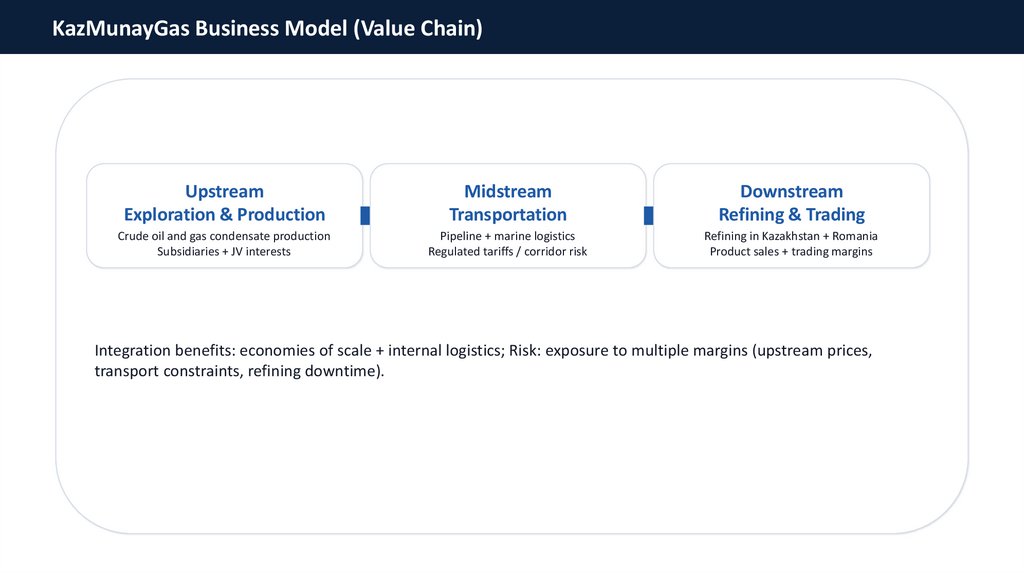

KazMunayGas Business Model (Value Chain)Upstream

Exploration & Production

Midstream

Transportation

Downstream

Refining & Trading

Crude oil and gas condensate production

Subsidiaries + JV interests

Pipeline + marine logistics

Regulated tariffs / corridor risk

Refining in Kazakhstan + Romania

Product sales + trading margins

Integration benefits: economies of scale + internal logistics; Risk: exposure to multiple margins (upstream prices,

transport constraints, refining downtime).

7.

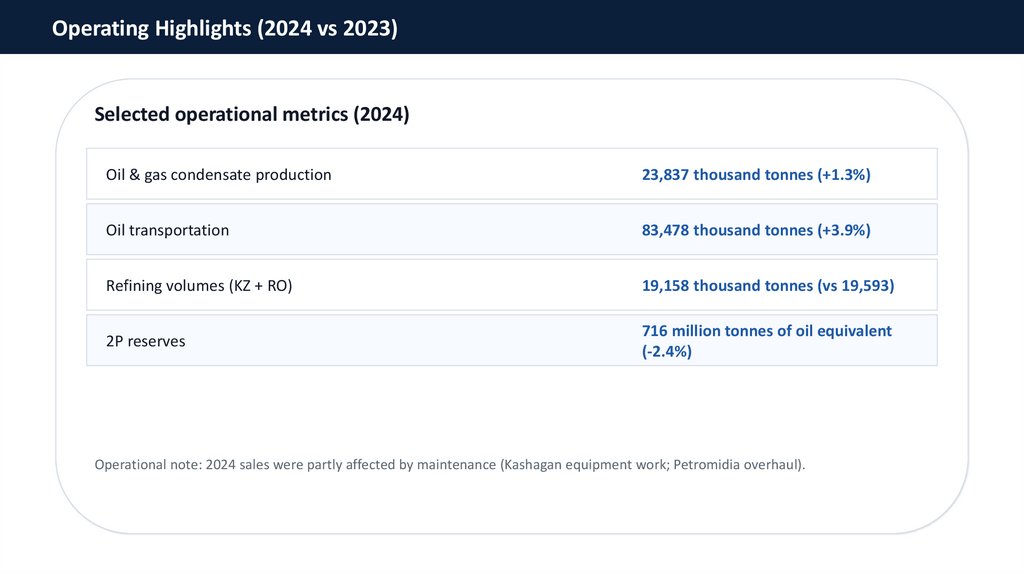

Operating Highlights (2024 vs 2023)Selected operational metrics (2024)

Oil & gas condensate production

23,837 thousand tonnes (+1.3%)

Oil transportation

83,478 thousand tonnes (+3.9%)

Refining volumes (KZ + RO)

19,158 thousand tonnes (vs 19,593)

2P reserves

716 million tonnes of oil equivalent

(-2.4%)

Operational note: 2024 sales were partly affected by maintenance (Kashagan equipment work; Petromidia overhaul).

8.

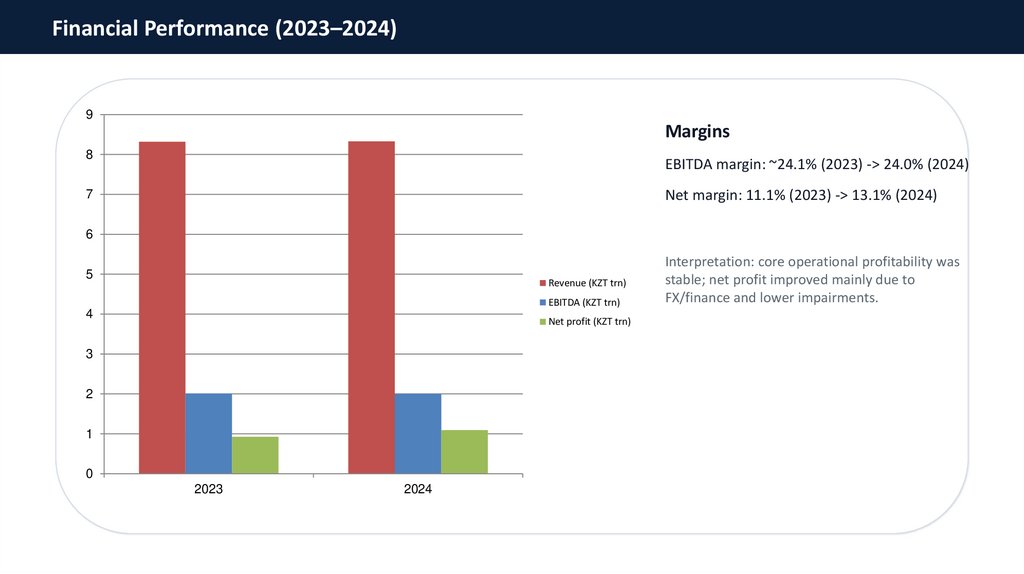

Financial Performance (2023–2024)9

Margins

8

EBITDA margin: ~24.1% (2023) -> 24.0% (2024)

Net margin: 11.1% (2023) -> 13.1% (2024)

7

6

5

Revenue (KZT trn)

EBITDA (KZT trn)

4

Net profit (KZT trn)

3

2

1

0

2023

2024

Interpretation: core operational profitability was

stable; net profit improved mainly due to

FX/finance and lower impairments.

9.

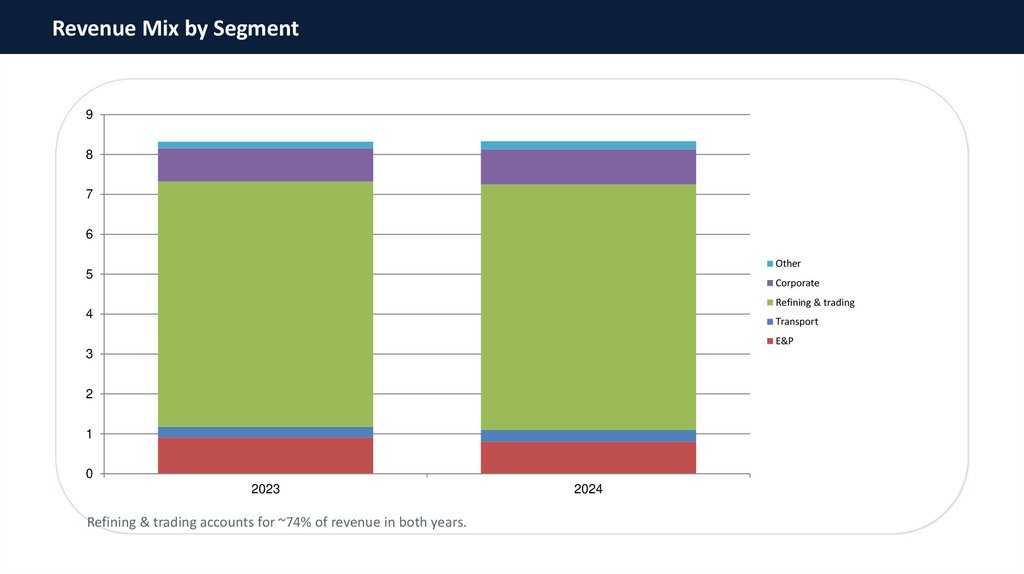

Revenue Mix by Segment9

8

7

6

Other

5

Corporate

Refining & trading

4

Transport

E&P

3

2

1

0

2023

Refining & trading accounts for ~74% of revenue in both years.

2024

10.

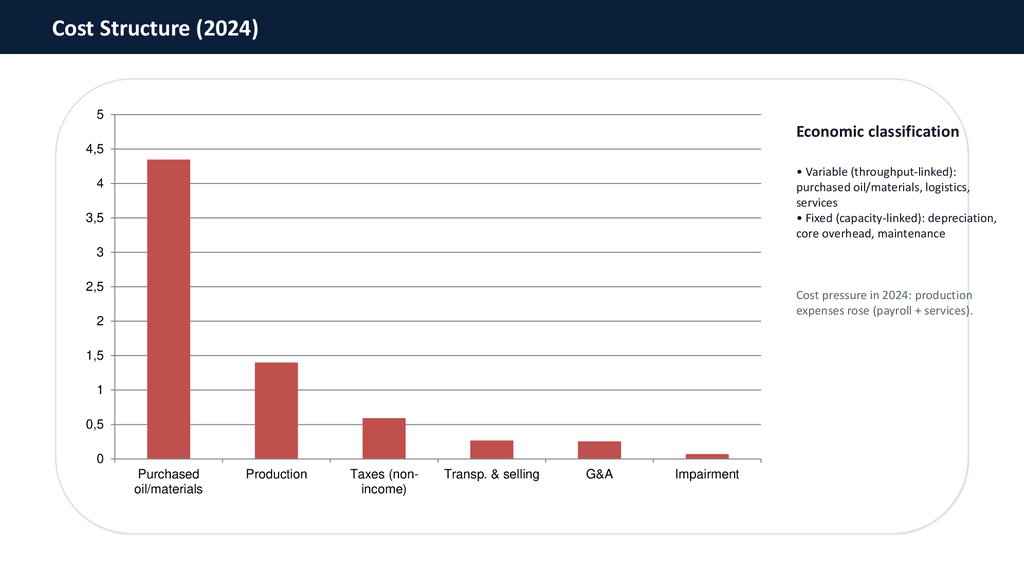

Cost Structure (2024)5

Economic classification

4,5

• Variable (throughput-linked):

purchased oil/materials, logistics,

services

• Fixed (capacity-linked): depreciation,

core overhead, maintenance

4

3,5

3

2,5

Cost pressure in 2024: production

expenses rose (payroll + services).

2

1,5

1

0,5

0

Purchased

oil/materials

Production

Taxes (nonincome)

Transp. & selling

G&A

Impairment

11.

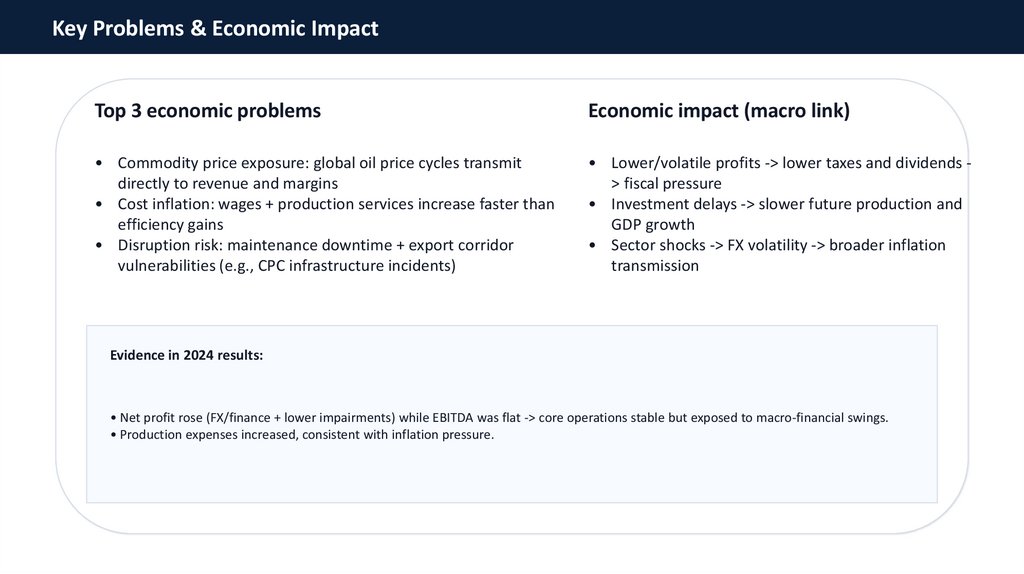

Key Problems & Economic ImpactTop 3 economic problems

Economic impact (macro link)

• Commodity price exposure: global oil price cycles transmit

directly to revenue and margins

• Cost inflation: wages + production services increase faster than

efficiency gains

• Disruption risk: maintenance downtime + export corridor

vulnerabilities (e.g., CPC infrastructure incidents)

• Lower/volatile profits -> lower taxes and dividends > fiscal pressure

• Investment delays -> slower future production and

GDP growth

• Sector shocks -> FX volatility -> broader inflation

transmission

Evidence in 2024 results:

• Net profit rose (FX/finance + lower impairments) while EBITDA was flat -> core operations stable but exposed to macro-financial swings.

• Production expenses increased, consistent with inflation pressure.

12.

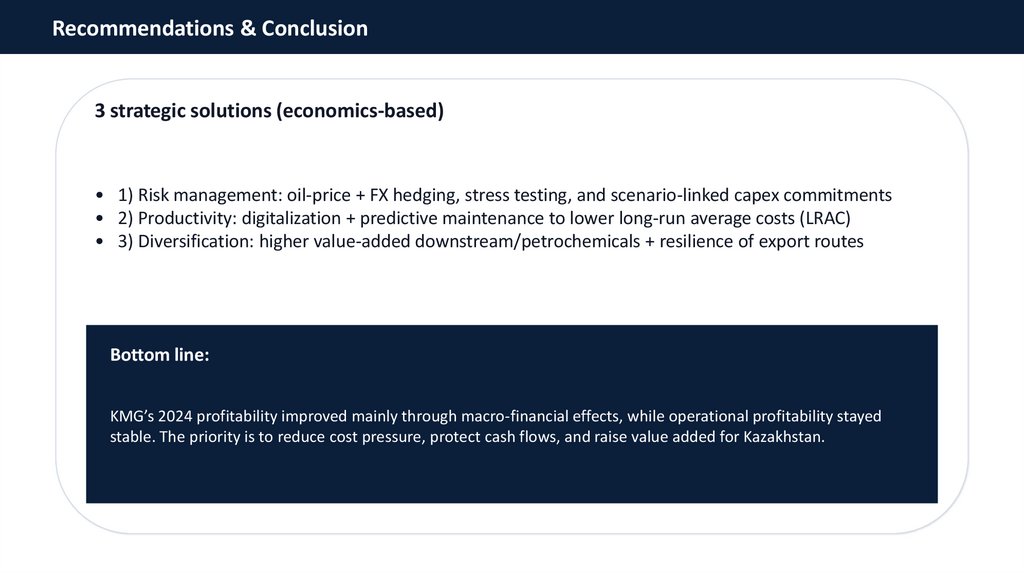

Recommendations & Conclusion3 strategic solutions (economics-based)

• 1) Risk management: oil-price + FX hedging, stress testing, and scenario-linked capex commitments

• 2) Productivity: digitalization + predictive maintenance to lower long-run average costs (LRAC)

• 3) Diversification: higher value-added downstream/petrochemicals + resilience of export routes

Bottom line:

KMG’s 2024 profitability improved mainly through macro-financial effects, while operational profitability stayed

stable. The priority is to reduce cost pressure, protect cash flows, and raise value added for Kazakhstan.