Финансы

ФинансыПохожие презентации:

Decision tree. Risk planning and value

1.

Decision tree2.

2A decision tree is a graphical method that shows the

sequence of strategic decisions and proposed

sequence in every possible unit of circumstances

3.

3Building the decision tree begins with the

earliest decisions and moves forward in time

through the successive events and decisions

4.

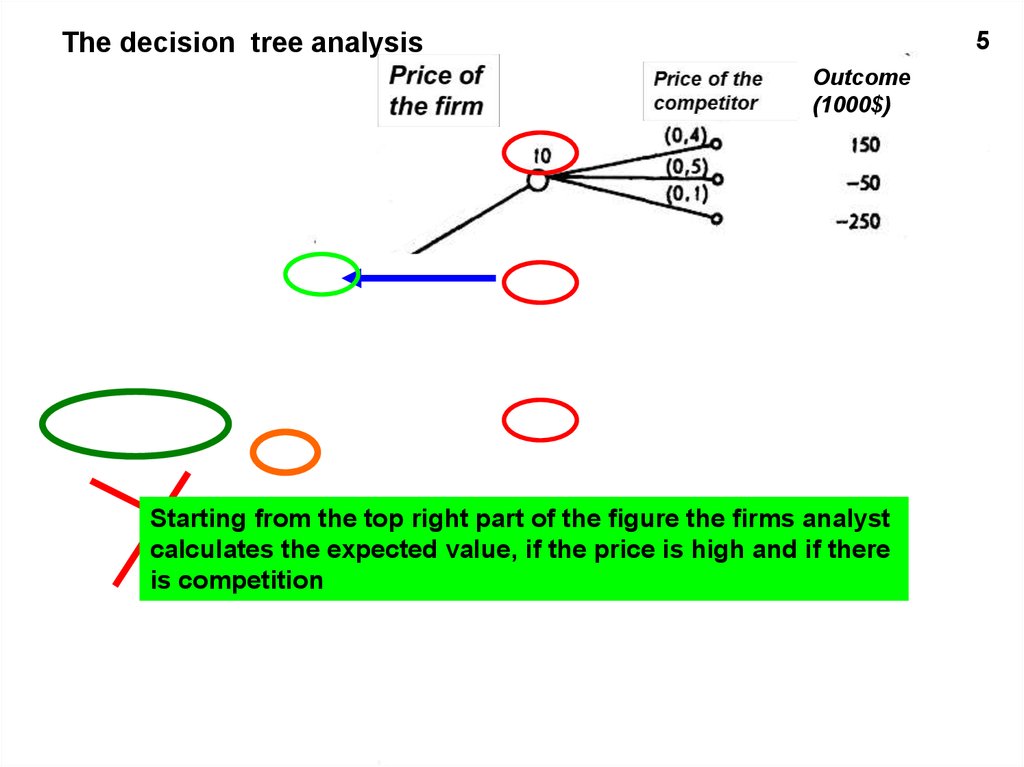

Outcome(1000$)

Price of the firm

5.

4Because of every decision

depends on the assessment of

the events that will occur later,

the tree decision analysis begins

at the end of the sequence and

moves back

6.

5The decision tree analysis

Outcome

(1000$)

Starting from the top right part of the figure the

Pricefirms

of the analyst

firm

calculates the expected value, if the price is high and if there

is competition

7.

Risk planning and price of risk8.

9For the risk it is characteristic that the probability of

outcomes can be evaluated statistically

Potential profit and loss can be included in the cost

structure of the firm

9.

10In-house risk

Concerns possible losses that firms prefer to include in the cost

structure in advance instead of buying insurance against such

losses

10.

11If the number of accidents within the firm is large

enough so that they can be predicted,

the management may determine the

probability of loss and add it to the

other costs

Ех:

If the average estimated losses of the company can be

predicted for the current period, then they can be

insured in the company, regarding them as the cost of

doing business

11.

Determination of the possibility of such damagescan be part of the planning of the company under

condition of allocation of reserve in case of damage

or unforeseen circumstances

12.

Therefore, banks regularly write off bad loans, andthe usual practice in accounting is unpaid invoices

for any business that has a receivables

13.

Intercompany riskOccurs if the number of

observations within one company

is not large enough so that the

management can predict the

damages with reasonable

accuracy

14.

When considering a lot of firms, the number of observationsbecomes large enough to be able to demonstrate the necessary

stability of predictions

15.

Examples of such risks are fire,16.

floods,17.

storms and other natural disasters18.

Since the heads of companies are not able to predict suchdamage to their firms

The burden of forecasting passed on

insurance companies

The insurance companies

have large base of certain

cases

19.

The likelihood of loss cannot be set for a particularfirm, but the likelihood of loss, covering many

businesses can be predicted with a minimum error

Р

20.

Insurance company predicts cumulative risk of allfirms that she secures and distributes the total

cost of the anticipated losses by charging each

firm fee, called a premium

21.

Insurance premium becomes part of the cost structure ofthe insured company

22.

The insurance company must decide what premium tocharge based on estimated losses + administrative

costs and profit

23.

The manager, trying to avoid risk, should decide whether tobuy or not to buy insurance, based on the estimated cost of

operations of the company and its utility functions

24.

Ех:Функция полезности