Менеджмент

МенеджментПохожие презентации:

Department for Audit and IFRS HR Audit

1.

Department for Audit and IFRSHR Audit

2.

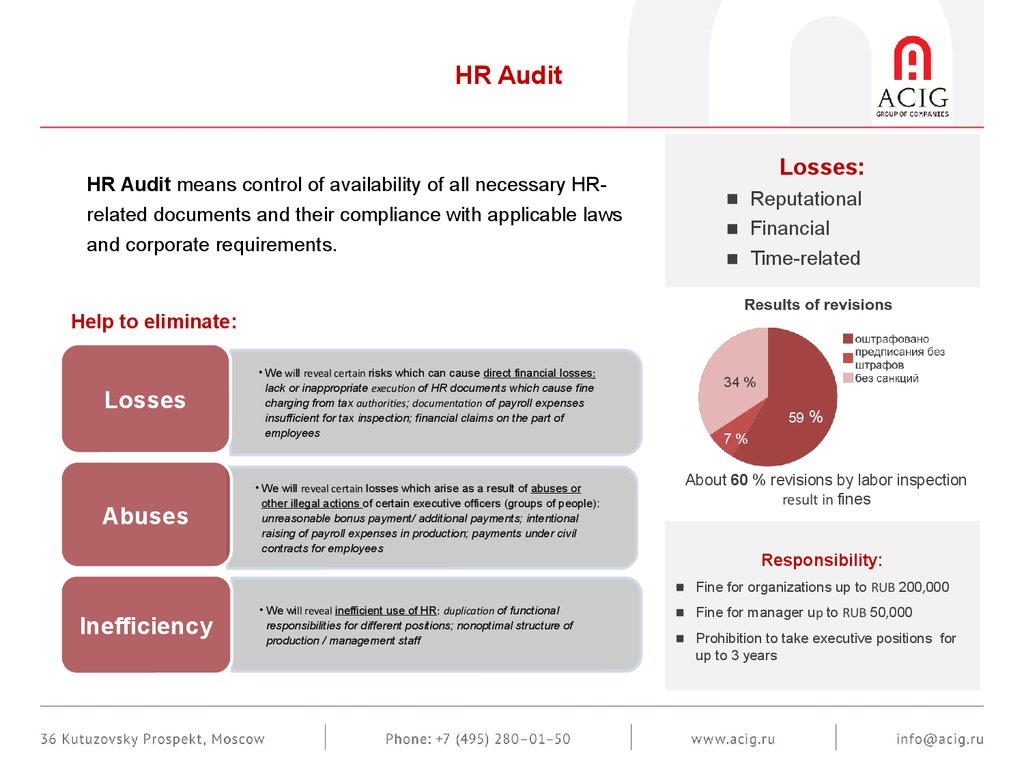

HR AuditHR Audit means control of availability of all necessary HRrelated documents and their compliance with applicable laws

and corporate requirements.

Losses:

▪ Reputational

▪ Financial

▪ Time-related

Help to eliminate:

Losses

Abuses

• We will reveal certain risks which can cause direct financial losses:

lack or inappropriate execution of HR documents which cause fine

charging from tax authorities; documentation of payroll expenses

insufficient for tax inspection; financial claims on the part of

employees

• We will reveal certain losses which arise as a result of abuses or

other illegal actions of certain executive officers (groups of people):

unreasonable bonus payment/ additional payments; intentional

raising of payroll expenses in production; payments under civil

contracts for employees

34 %

59

%

7%

About 60 % revisions by labor inspection

result in fines

Responsibility:

▪ Fine for organizations up to RUB 200,000

Inefficiency

• We will reveal inefficient use of HR: duplication of functional

responsibilities for different positions; nonoptimal structure of

production / management staff

▪ Fine for manager up to RUB 50,000

▪ Prohibition to take executive positions for

up to 3 years

3.

ProjectsCase

Payroll control during audit of financial and business activities

• Goal – assurance of payroll expenses

• Audit extent– based on aggregates with selective revision of HR documents for certain employees

• Evaluated risks– failure to comply with applicable accounting, tax, and labor laws

Verification of HR documentation in case of changing persons responsible for its maintaining

• Goal – risk elimination during handover of responsibilities

• Audit extent– from selective to total (depending on different groups of staff)

• Evaluated risks– loss of HR documents in the event of handover of responsibilities (or their

execution/ lack thereof), errors in execution of HR documents

Preparation for government audit (labor inspection, tax office)

• Goal – loss minimization after revisions by public authorities

• Audit extent– – from selective to total (depending on different groups of staff)

• Evaluated risks– amount of claims on the part of labor and tax authorities which can arise from

inappropriate HR documenting

Result

1) Detection of system errors in

payroll accounting and HR

documents

2) Evaluation of tax risks (income tax,

fees, corporate tax)

1) Detection of errors in individual

HR documents or failures to

execute those

59 %

2) Development of schedule for

7 %correction of errors

1) Detection of system errors in HR

documents

2) Evaluation of amount of tax claims

on the part of public authorities

(fines, additional tax payments)

3) Development of schedule for

correction of errors