Экономика

Экономика Финансы

ФинансыПохожие презентации:

Financial Evaluation of an IT Project

1.

5В050700-ManagementProject Management

Practice 10: Financial

Evaluation of an IT Project

Duration: 1 study hour

Course no: 13570

Prepared by: Tulekov N

Almaty

2021 г.

2.

5В050700-ManagementContents

Topic

Page

Plan of the practice

3

Sources of Return

4

New Income

8

Income growth

10

Saved income

11

Operational efficiency

12

Development costs

13

Profit Forecast

15

Sprint Burnup Chart

16

Home task

18

Book

19

Questions

20

3.

5В050700-ManagementPlan of the practice

As continue of the last lection we will try today to

build a financial report of effectiveness of an IT

project.

We will observe several sources of income and

costs.

Also we will put all figures in a table for better

visualisation

Let’s go

4.

5В050700-ManagementSources of Return (1/4)

Some projects are implemented to generate income, others to reduce

costs, and others to achieve both. If you can estimate the amount of

money that each topic will bring or save, you can use it for prioritization

purposes. The responsibility for predicting the financial value of the topic

lies with the product owner, but it can be shared with team members programmers, testers, analysts, project managers, etc. In most cases, the

product owner must also rely on business knowledge and sales and

marketing team forecasts.

To determine the financial impact of the topic, I prefer to organize

meetings with the number of people that seems appropriate. The purpose

of such a topic assessment meeting is to complete the form given in the

table for each topic. Depending on the number of topics and participants,

this event may not be limited to a single meeting.

5.

5В050700-ManagementSources of Return (2/4)

Table 10.1 provides a line for each quarter of the next

two years. The time horizon is set at the option of the

command. Sometimes teams prefer to determine the

monthly return for one or two years. In my

experience, a two-year period is suitable for most

projects. This is a kind of middle ground between

divination about the distant future and a reasonable

look forward. Due to the high uncertainty associated

with software development projects, others take this

approach (Bills, 2004a).

Table 10.1 contains columns for different types of recoil, which may be for topics. If you have other return

types in your project, change the headings accordingly. Similarly, use other column headings if you want to

specify them. It is not necessary to have the same set of columns for all topics.

The meeting participants complete the worksheet by estimating the cost in the cells they consider to be

affected by the development of the topic.

6.

5В050700-ManagementSources of Return (3/4)

Where do the numbers come from? Ideally - from a marketing study, which was used in the economic

justification of the feasibility of the project. At a minimum, the person requesting this topic should quantify

the basis for its development. Income from the project can come from various sources. For convenience, we

will designate them as new income, income growth, retained income and operational efficiency.

There can be no doubt that the most common source of income in the project is the generation of new

income. Few companies are content with the existing market share, in most they try to attract new

customers. Even if the product is not sold directly, adding new features can generate new revenue. It is often

useful to distinguish revenue from new customers from additional, incremental income from existing

customers. Income gains can be the result of a new system or product:.

· Provides incentives for existing customers to

purchase additional licenses.

· Contains features that allow you to set a higher

price.

· Contains optional expansion modules that can be

sold separately.

· Provides incentives for the use of consulting

services (for example, integration with a third-party

application).

7.

5В050700-ManagementSources of Return (4/4)

Apart from the new income and income growth is the retained

income. Saved income refers to income that an organization may

lose if it does not implement a project or topic.

No organization can boast of the greatest possible effectiveness.

There is always a task that can be simplified or eliminated. If you

are developing software for use by internal customers, you are

likely well aware of the importance of operational efficiency. At the

same time, even when you are working on a commercial program

that will be sold outside your company, some tasks within the

project can increase operational efficiency. [1. page 77]

8.

5В050700-ManagementNew Income(1/2)

We don't have reliable data. Sales Representative Terry says that based on current sales

forecasts, he will be able to attract 50 new customers per quarter this year, and 100

customers per quarter next year. These values are included in the New Clients column of

Table 10.3. Although the function will appear only in the middle of the 2nd quarter, Terry is

sure that already this quarter will attract 50 new customers.

Now we estimate the revenue per client. This can be done based on existing customer data.

We know, for example, that the average customer pays us $400 a year. However, we believe

that the new service will be most attractive to small customers, those who pay us an

average of $200 per year. In our opinion, you can count on an additional $100 per year from

each such client. The total value of each new customer is thus $300 per year, or $75 per

quarter. Since the service will be available from the 2nd quarter, revenue per customer this

quarter is proportionally reduced. These values are added to the "Revenue per Customer"

column in Table 10.3, which allows you to define "New Revenue."[1. page 78]

9.

5В050700-ManagementNew Income(2/2)

10.

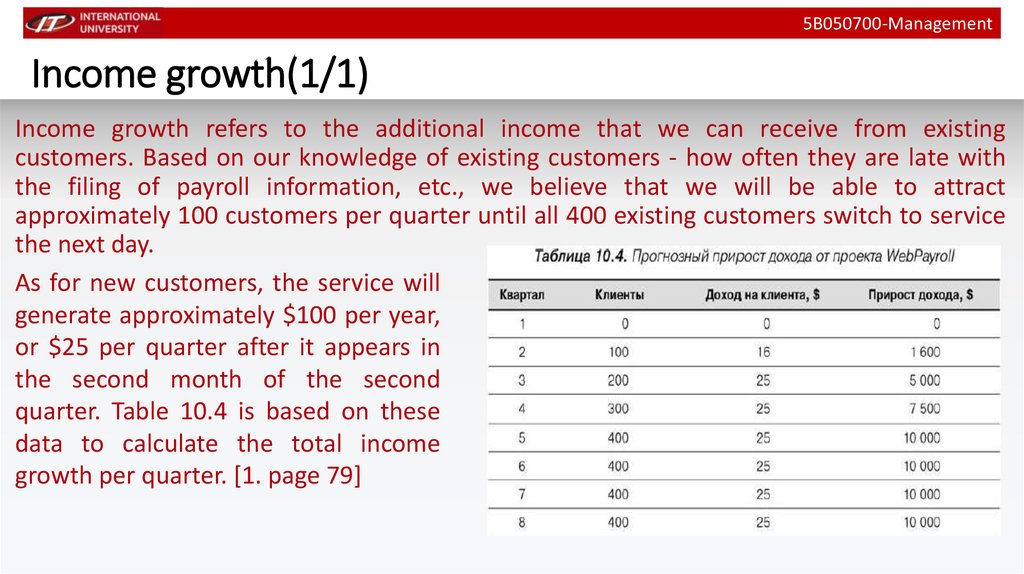

5В050700-ManagementIncome growth(1/1)

Income growth refers to the additional income that we can receive from existing

customers. Based on our knowledge of existing customers - how often they are late with

the filing of payroll information, etc., we believe that we will be able to attract

approximately 100 customers per quarter until all 400 existing customers switch to service

the next day.

As for new customers, the service will

generate approximately $100 per year,

or $25 per quarter after it appears in

the second month of the second

quarter. Table 10.4 is based on these

data to calculate the total income

growth per quarter. [1. page 79]

11.

5В050700-ManagementSaved income(1/1)

Saved income is something that we will not lose due to customer dissatisfaction with our

product, growing needs or other reasons for refusing to WebPayroll. The company currently

does not have a good indicator to track this factor. We only know that it is beginning to turn

into a problem and will become much more

serious over the next few years. According to our

estimates, the transition to the next day service

will prevent the departure of 20 customers per

quarter in the first year and 40 customers per

quarter in the second year. It is especially

important that these customers continue to use

WebPayroll, despite the lack of this functionality

until the second quarter. Knowing that each

existing customer generates $400 per year, i.e.

$100 per quarter, we can calculate the saved

revenue as shown in Table 10.5. [1. page 80]

12.

5В050700-ManagementOperational efficiency(1/1)

For the next day's maintenance project to be successful, we need to almost completely

eliminate manual interference with the system that exists today. Without automating this

operation, we will have to include two additional accountants in the middle of this year and

two more in the middle of next year.

As a result of the planned efficiency improvement in the

next day's maintenance project, we expect to reduce one of

these positions each year. Accountants cost an average of

$20 000 a year. Each of them is also provided with office

space, certain equipment, software and compensation

payments. In total, these additional hidden expenses

amount to about another 50% of the employee's salary. In

other words, the real cost of an accountant is closer to $30

000 a year. It's called full pay. The number of accountants

who have not been hired and the full salary give when

multiplying the operating efficiency for each quarter.[1.

page 81]

13.

5В050700-ManagementDevelopment costs (1/2)

In order to complete the development of the investment profile of the service WebPayroll project

the next day, we need to estimate the expected costs of developing the topic. To do this, look at the

wages of all project participants (Table 10.7).

The full salary in table 10.7 is calculated by

increasing the salary of each employee by 50%.

Since the iteration takes two weeks, the total salary

per iteration is 1/26 of the total salary. The Time in

Project column indicates the proportion of time

that each team member in the project has. All are

fully occupied except for one programmer. The

column "Adjusted iteration costs" shows the project

costs for each participant, taking into account the

full salary and the time of participation in the

project. In general, the team's iteration costs are

$13 550. Round this value to $13 500. [1. page 81]

14.

5В050700-ManagementDevelopment costs (2/2)

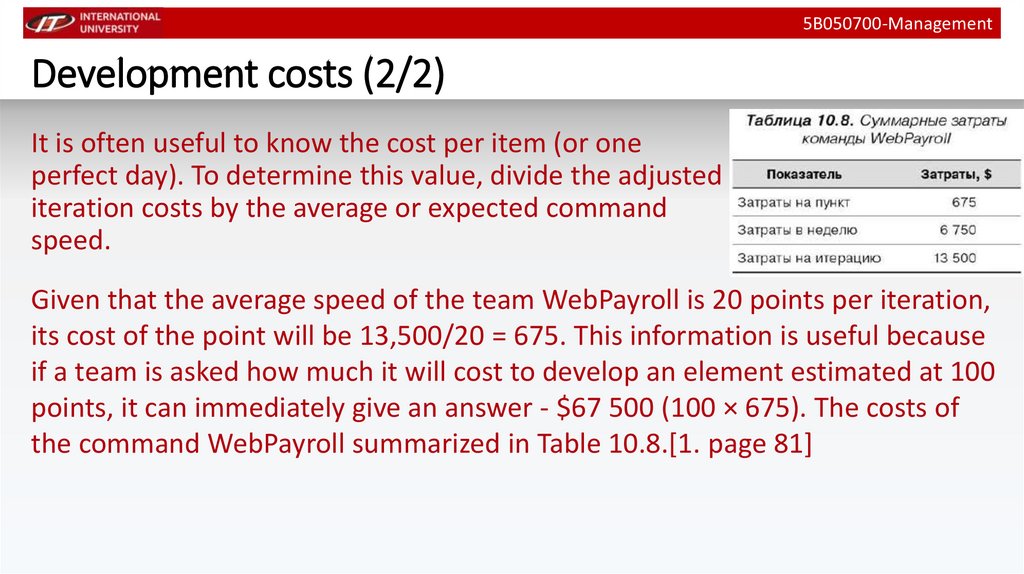

It is often useful to know the cost per item (or one

perfect day). To determine this value, divide the adjusted

iteration costs by the average or expected command

speed.

Given that the average speed of the team WebPayroll is 20 points per iteration,

its cost of the point will be 13,500/20 = 675. This information is useful because

if a team is asked how much it will cost to develop an element estimated at 100

points, it can immediately give an answer - $67 500 (100 × 675). The costs of

the command WebPayroll summarized in Table 10.8.[1. page 81]

15.

5В050700-ManagementProfit Forecast (1/1)

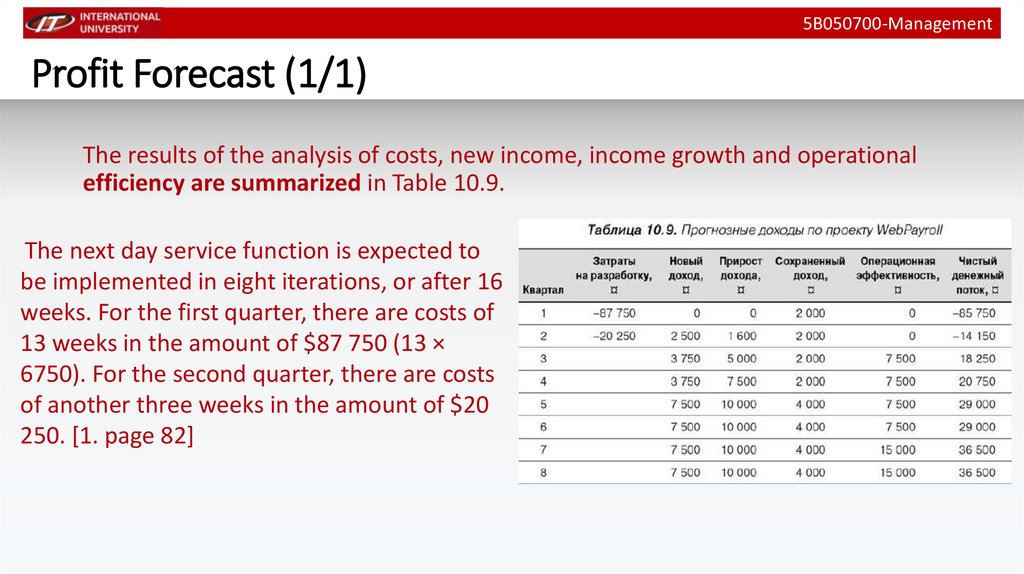

The results of the analysis of costs, new income, income growth and operational

efficiency are summarized in Table 10.9.

The next day service function is expected to

be implemented in eight iterations, or after 16

weeks. For the first quarter, there are costs of

13 weeks in the amount of $87 750 (13 ×

6750). For the second quarter, there are costs

of another three weeks in the amount of $20

250. [1. page 82]

16.

B044-ManagementSprint Burnup Chart (1/2)

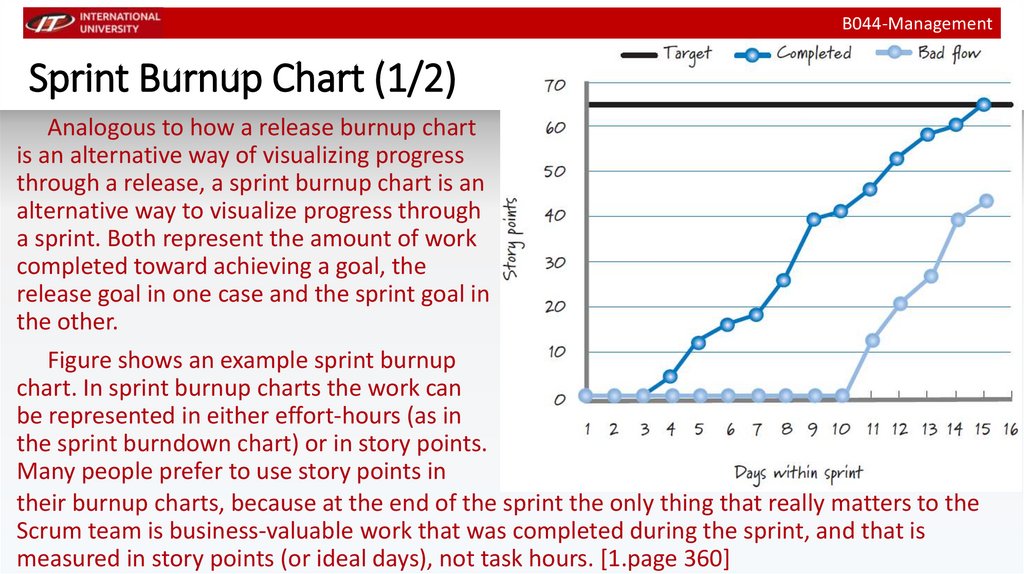

Analogous to how a release burnup chart

is an alternative way of visualizing progress

through a release, a sprint burnup chart is an

alternative way to visualize progress through

a sprint. Both represent the amount of work

completed toward achieving a goal, the

release goal in one case and the sprint goal in

the other.

Figure shows an example sprint burnup

chart. In sprint burnup charts the work can

be represented in either effort-hours (as in

the sprint burndown chart) or in story points.

Many people prefer to use story points in

their burnup charts, because at the end of the sprint the only thing that really matters to the

Scrum team is business-valuable work that was completed during the sprint, and that is

measured in story points (or ideal days), not task hours. [1.page 360]

17.

B044-ManagementSprint Burnup Chart (2/2)

Also, if we measure story points of completed

product backlog items, at a glance we can get a

good feel for how the work is flowing and how the

team is completing product backlog items through

the sprint. To illustrate this point a third line

(labeled “Bad flow”) is included on the sprint

burnup chart in Figure (normally this line would

not be on the chart; it is added in this example for

comparison purposes). The “Bad flow” line

illustrates what the burnup chart might look like if

the team starts too many product backlog items at

the same time, delays completion of items until

later in the sprint, fails to meet the sprint target because of the reduced velocity of doing too

much work in parallel, works on product backlog items that are large and therefore take a long

time to finish, or takes other actions that result in bad flow. [1.page 360]

18.

5В050700-ManagementHome task

By the next practice:

1. to prepare Project Forecast Calculation table

2. to prepare Burnup chart

on your project

19.

B044-ManagementBooks

1. Mike Kohn – Agile estimating and planning. Alpina Publisher, 2018

2. Rubin K- Essential Scrum – A Practical Guide to the Most Popular

Agile Process. Pearson Education, Inc.2012

20.

5В050700-ManagementQuestions