Экономика

ЭкономикаПохожие презентации:

Stock markets and securities

1.

STOCK MARKETS AND SECURITIES2.

Recommended literature:1.

Сохацька О.М., Роговська-Іщук І.В., Вінницький С.І. Фундаментальний та

технічний аналіз цін товарних та фінансових ринків. Київ: Кондор, 2012.

2.

Shiller R. J. Irrational Exuberance. Princeton: Princeton University Press, 2000.

3.

Mladjenovic P. Stock Investing For Dummies. Indianapolis: Wiley Publishing, Inc.,

2006.

4.

Fisher Ph. A. Common Stocks And Uncommon Profits And Other Writings. New

Jersey: Wiley Publishing, Inc., 2003.

5.

Найман Е. Мала Енциклопедія Трейдера – 3-е вид. – 2003. – 378 С. (Розділ 1, С.

20-34).

6.

Graham В. and Dodd D. Securities Analysis – 6-th Edition. – 2009. – 766 p.

7.

Benjamin Graham. The Intelligent Investor: The Definitive Book on Value Investing.

(або укр. версія) - Грем Б. Розумний інвестор. Стратегія вартісного інвестування.

(із коментарями Джейсона Цвейга) – К.: Наш формат, 2019. – 544 с.

Базилевич В.Д., Шелудько В.М., Ковтун Н.В. Та Ін. Цінні Папери. Київ: Знання,

2011.

8.

3.

TOPIC 1. BASICS OF FUNDAMENTALANALYSIS (part 1)

1. The essence and stages of fundamental analysis.

2. Analysis of the influence of international environment factors.

3. Analysis of macroeconomic indicators.

4. The industry level factors.

4.

1. The essence and stages of fundamental analysisThere are three main methods of analyzing financial markets:

fundamental (FA);

technical (TA);

intuitive.

The need to use fundamental analysis in investment decisions was first theoretically and practically

justified by the American economists Benjamin Graham and David Dodd ("Securities Analysis") (1934).

FA studies the movement of prices at the macroeconomic level and helps to determine the main

market trend.

Trend - the main direction of the dynamics of market prices.

"Fundamental analysts study all the information about the fundamental economic relationship supply and demand, which ultimately determines all prices," said John Marshall, a professor of finance

in the United States.

5.

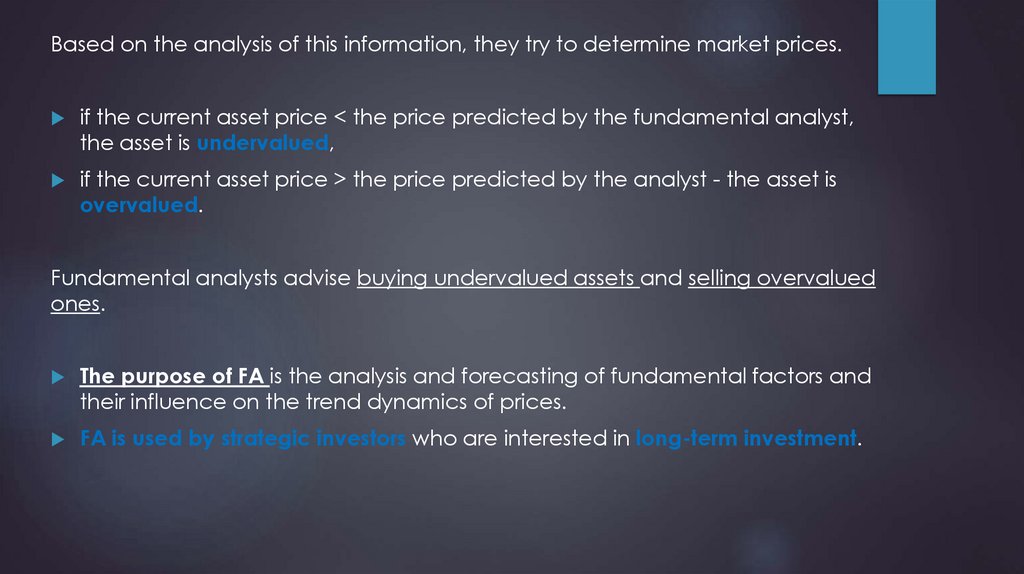

Based on the analysis of this information, they try to determine market prices.if the current asset price < the price predicted by the fundamental analyst,

the asset is undervalued,

if the current asset price > the price predicted by the analyst - the asset is

overvalued.

Fundamental analysts advise buying undervalued assets and selling overvalued

ones.

The purpose of FA is the analysis and forecasting of fundamental factors and

their influence on the trend dynamics of prices.

FA is used by strategic investors who are interested in long-term investment.

6.

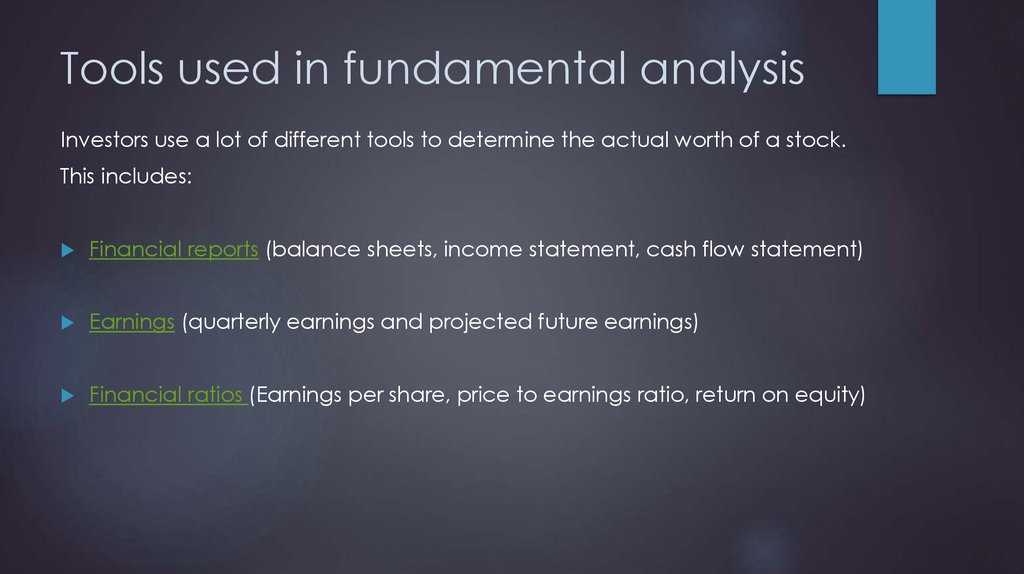

Tools used in fundamental analysisInvestors use a lot of different tools to determine the actual worth of a stock.

This includes:

Financial reports (balance sheets, income statement, cash flow statement)

Earnings (quarterly earnings and projected future earnings)

Financial ratios (Earnings per share, price to earnings ratio, return on equity)

7.

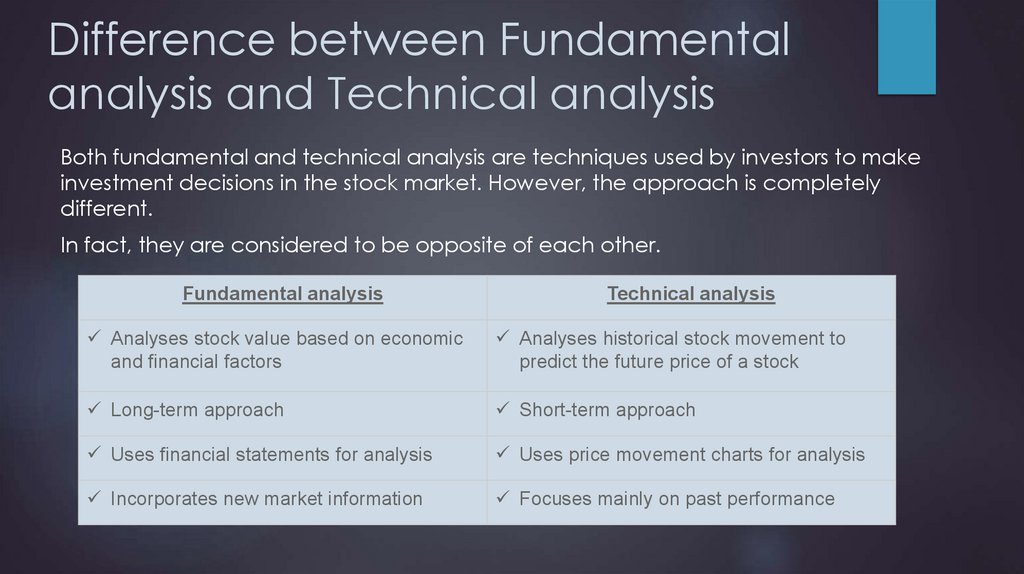

Difference between Fundamentalanalysis and Technical analysis

Both fundamental and technical analysis are techniques used by investors to make

investment decisions in the stock market. However, the approach is completely

different.

In fact, they are considered to be opposite of each other.

Fundamental analysis

Technical analysis

Analyses stock value based on economic

and financial factors

Analyses historical stock movement to

predict the future price of a stock

Long-term approach

Short-term approach

Uses financial statements for analysis

Uses price movement charts for analysis

Incorporates new market information

Focuses mainly on past performance

8.

News and life cycles of fundamental factorsNews:

accidental and unexpected (political and natural, such as wars,

earthquakes, sometimes economic)

planned and expected (economic, rarely political)

Life cycles of fundamental factors:

short cycle (usually by unexpected events, not more than 1 day)

long cycle (from a few weeks to several years) (all factors related to the

general state of the national and world economy, such as interest rates,

inflation, unemployment, etc.)

9.

Options for the impact of market expectations:I.

when expectations come true - the dynamics of prices

will not change much;

II.

when expectations are not met due to only one factor

that was not taken into account - the price continues

the current dynamics with acceleration at the time of

the message;

III.

when expectations are completely wrong - the price

becomes a strong change of course in the opposite

direction.

10.

If the fundamental news contradicts the existing trend -then the time of its influence on the market dynamics

is limited to an hour or several hours;

if ... confirms the trend - there is some acceleration of

the trend followed by a certain pullback.

11.

All fundamental factors are evaluatedfrom two points of view:

How will this news affect the discount rate?

What is the state of the national economy?

12.

Discount rateThe most common rumor in the stock and currency market

is the expectation of a change in the discount rate.

If the interest rate is expected to rise:

stock market – will decrease,

currency market – the national currency will growth.

13.

Discount rate is expected to ↑stock market will decrease

"Fed model" - relationship between 10-year interest rate and stock market level.

Price to earnings

ratio (P/E)

Long-term interest rate

Long-term interest rate

Price to earnings ratio (P/E)

This model was fashionable to use in the 1990s and early 2000s to explain the market

situation.

14.

Scheme of carrying out fundamentalanalysis "from top to bottom"

analysis of the economy and the market as a whole;

industry analysis;

regional analysis;

analysis of investment attractiveness of the objects of

investment;

formation of investment strategy;

formation of investment portfolio.

15.

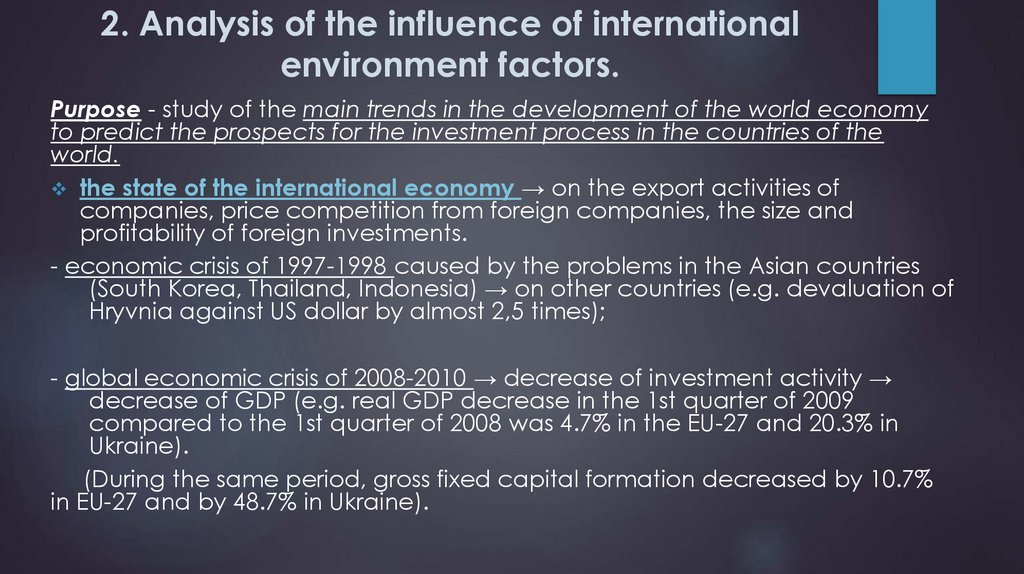

2. Analysis of the influence of internationalenvironment factors.

Purpose - study of the main trends in the development of the world economy

to predict the prospects for the investment process in the countries of the

world.

the state of the international economy → on the export activities of

companies, price competition from foreign companies, the size and

profitability of foreign investments.

- economic crisis of 1997-1998 caused by the problems in the Asian countries

(South Korea, Thailand, Indonesia) → on other countries (e.g. devaluation of

Hryvnia against US dollar by almost 2,5 times);

- global economic crisis of 2008-2010 → decrease of investment activity →

decrease of GDP (e.g. real GDP decrease in the 1st quarter of 2009

compared to the 1st quarter of 2008 was 4.7% in the EU-27 and 20.3% in

Ukraine).

(During the same period, gross fixed capital formation decreased by 10.7%

in EU-27 and by 48.7% in Ukraine).

16.

international political events:- in the late 1990s in Hong Kong, due to its subordination to China, significant

price fluctuations were observed in the stock market;

- election of 2008 Obama as president of the USA → liberalization of trade and

economic relations of the USA with many countries - a positive factor in the

economic development of these countries.

demand on the international markets:

-

2008-2009 ↓ demand in international markets → ↓ both export production and

related production in different countries → ↓ GDP → ↓ investment;

prices of imported fuel and energy commodities:

-

affect production capacity and production costs;

-

↑ prices of these goods → ↑ inflation rates → ↓ returns on securities and ↓ stock

indices.

international sports and cultural events → attract foreign investment →

develop infrastructure, ↑ competitiveness in international markets, improve the

investment climate at ↑ the value of securities.

17.

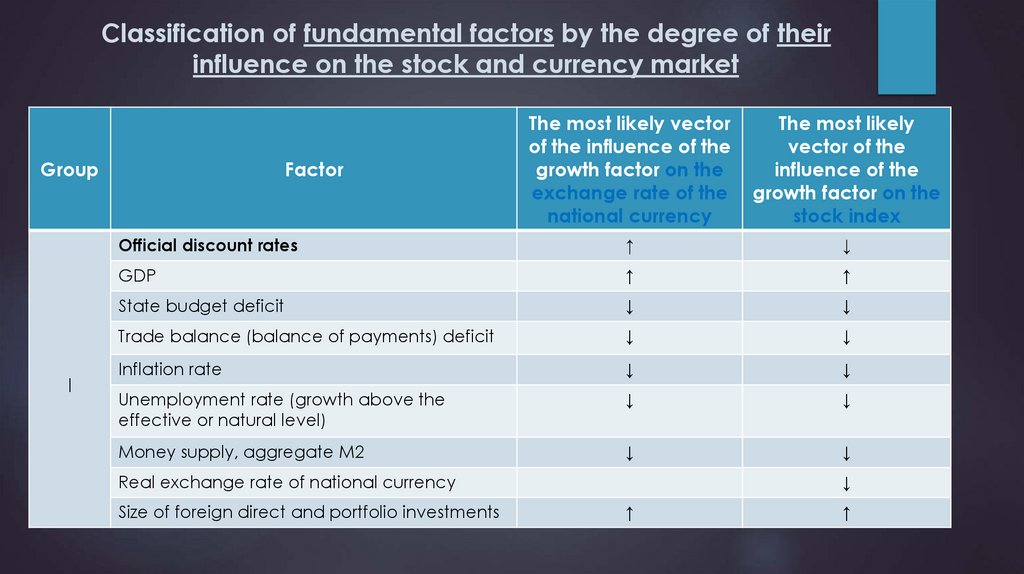

3. Analysis of macroeconomic indicators.Classification of fundamental factors by the degree of

their influence on the stock and currency market

The first group of factors (I) are strong factors, which have a high degree of

independence, that is, they do not have a secondary character. Their

installation in the market is (except for the first indicator) objective in nature,

does not depend on anyone's subjective evaluations and actions.

The factors of the second group (II) are of a similar nature, but their influence

is not as obvious and significant as for the factors of the first group.

Finally, the factors of the third group (III) are the least self-sufficient, subject to

significant influence from the factors of the first group.

18.

Classification of fundamental factors by the degree of theirinfluence on the stock and currency market

The most likely vector

of the influence of the

growth factor on the

exchange rate of the

national currency

The most likely

vector of the

influence of the

growth factor on the

stock index

Official discount rates

↑

↓

GDP

↑

↑

State budget deficit

↓

↓

Trade balance (balance of payments) deficit

↓

↓

Inflation rate

↓

↓

Unemployment rate (growth above the

effective or natural level)

↓

↓

Money supply, aggregate M2

↓

↓

Group

І

Factor

Real exchange rate of national currency

Size of foreign direct and portfolio investments

↓

↑

↑

19.

GroupII

III

The most likely vector

of the influence of the

growth factor on the

exchange rate of the

national currency

The most likely

vector of the

influence of the

growth factor on

the stock index

Size of retail sales

↑

↑

Amount of private income

↑

↑

Volume of orders in industry

↑

↑

Industrial production index

↑

↑

Level of labor productivity in the

economy

↑

↑

The level of world prices for major

export commodities

↑

↑

Production inventory level

↓

↓

Forward rates of national currency

↑

↑

The volume of industrial and ...

construction

↑

↑

The level of deposit rates

↑

↓

Government bond rates

↑

↑

Factor

Note: The table refers to the most likely vector of influence, not the real response of the object under study; the

response prediction is given, all other things being equal

20.

if GDP ↑ - the economy is developing, ↑ sales volumes,company profits are growing, ↑ investment in the stock

market, ↑ demand for securities, ↑ their market prices

(market value), ↑ stock index (the stage of high

conjuncture).

if the unemployment rate ↑ - negative trends in the

economy (↓ GDP, ↓ purchasing power of the

population, ↓ level of demand, ↓ corporate profits) → ↓

investment, supply of securities > demand of securities

and available capital in the stock market → ↓ their

market prices (market value) (stage of low conjuncture).

21.

inflation rate – stock prices (or securities rates/market value) are formed not only under the

influence of supply and demand for securities, but

also taking into account the expected price

increases.

if ↑ inflation rate → ↑ interest rates → ...

if ↑ interest rates → loans become more expensive, ↓

demand for products, ↓ corporate profits, ↓

dividends, ↓ stock market activity.

22.

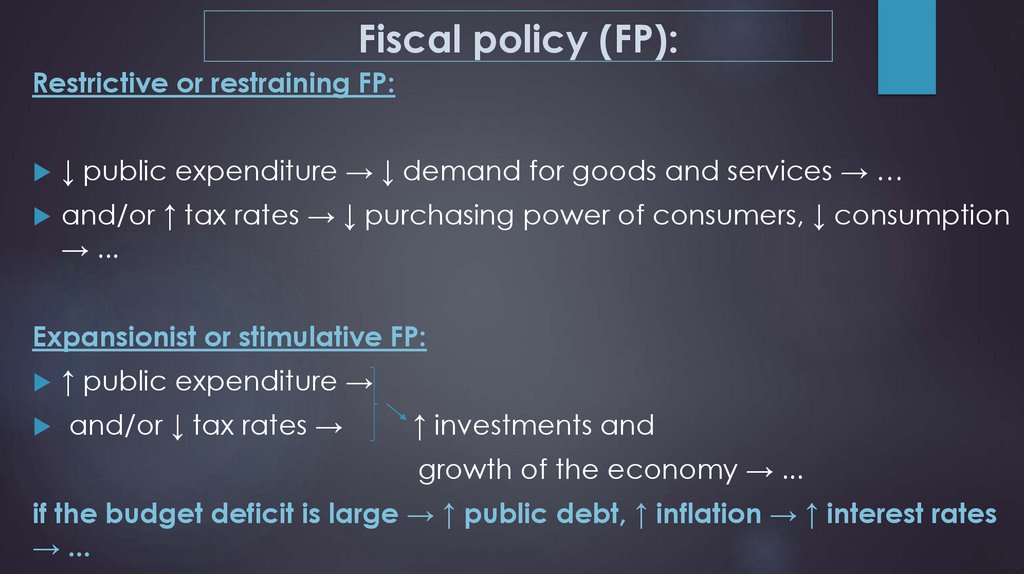

Fiscal policy (FP):Restrictive or restraining FP:

↓ public expenditure → ↓ demand for goods and services → …

and/or ↑ tax rates → ↓ purchasing power of consumers, ↓ consumption

→ ...

Expansionist or stimulative FP:

↑ public expenditure →

and/or ↓ tax rates →

↑ investments and

growth of the economy → ...

if the budget deficit is large → ↑ public debt, ↑ inflation → ↑ interest rates

→ ...

23.

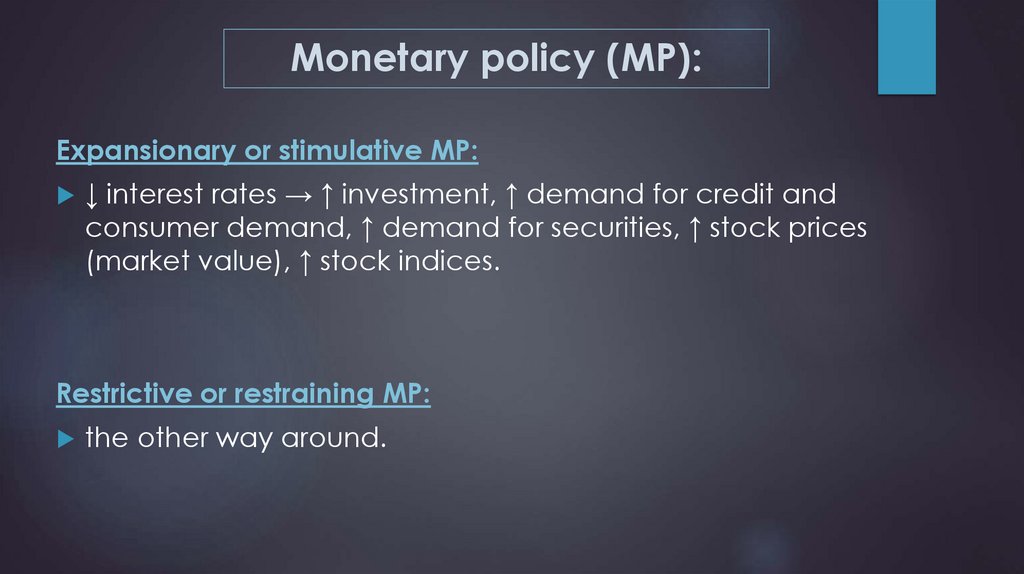

Monetary policy (MP):Expansionary or stimulative MP:

↓ interest rates → ↑ investment, ↑ demand for credit and

consumer demand, ↑ demand for securities, ↑ stock prices

(market value), ↑ stock indices.

Restrictive or restraining MP:

the other way around.

24.

4. The industry level factors.The economy has a cyclical nature of development:

-

recession,

-

bottom,

-

rise,

-

top.

When investing, it is important to identify which sectors of

the economy will be investment-attractive and most

affected in a particular macroeconomic situation.

25.

Comparative characteristics of stock pricesdepending on the state of the industry

26.

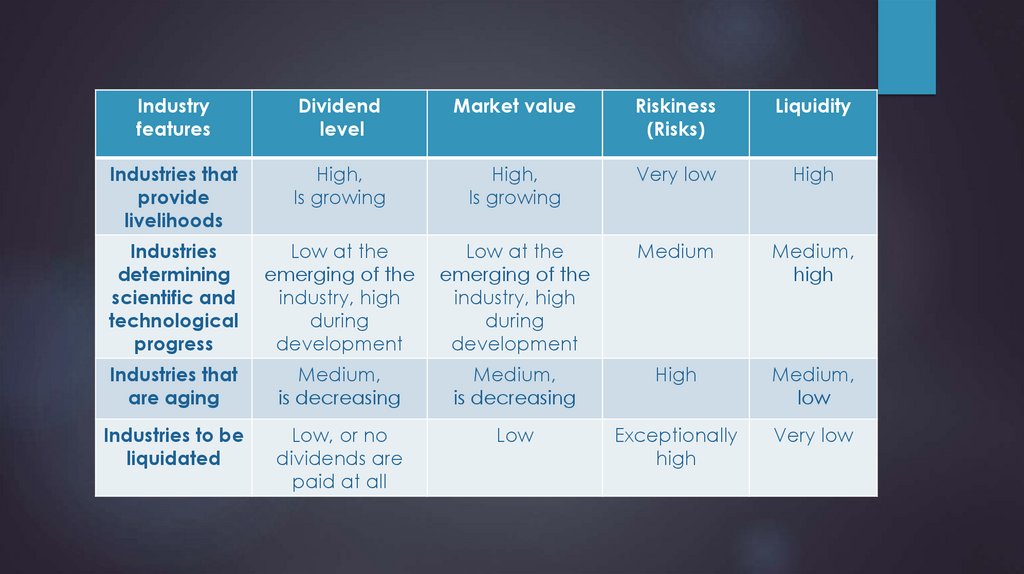

The main characteristics of shares depending onthe industry affiliation of the company

Industry

features

Dividend

level

Market value

Riskiness

(Risks)

Liquidity

Emerging

industries

Low

Low

Very high,

high

Low

Growth

industries

Is growing

Medium, is

growing

Medium,

low

Medium,

high

Cyclical

industries

Stable

industries

It fluctuates

It fluctuates

High when

according to according to

business

the stages of

the stages of activity drops,

the economic the economic very low when

cycle

cycle

the industry

picks up

High,

stable

Medium,

high,

permanent

Low

Medium,

high

High

27.

Industryfeatures

Dividend

level

Market value

Riskiness

(Risks)

Liquidity

Industries that

provide

livelihoods

High,

Is growing

High,

Is growing

Very low

High

Industries

determining

scientific and

technological

progress

Low at the

emerging of the

industry, high

during

development

Low at the

emerging of the

industry, high

during

development

Medium

Medium,

high

Industries that

are aging

Medium,

is decreasing

Medium,

is decreasing

High

Medium,

low

Industries to be

liquidated

Low, or no

dividends are

paid at all

Low

Exceptionally

high

Very low

28.

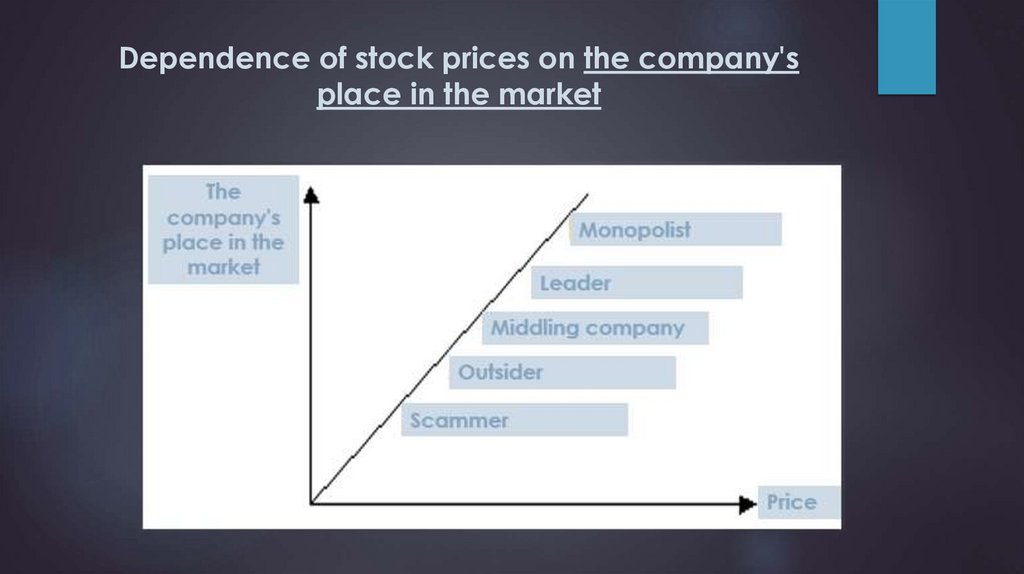

Dependence of stock prices on the company'splace in the market

29.

The main characteristics of shares dependingon the company's place in the market

Company's

place in the

market

Dividend

level

Market

value

Riskiness

(Risks)

Liquidity

Orientation

investors

Monopolist

High,

medium

Stable

Very low

High

On high dividends, stable market

value, minimal risk

Leader

High,

medium

Stable or is

growing

Low

High

On high dividends, stable market

value, low risk

Middling

company

Medium,

low

Stable or is

decreasing

Medium

High,

medium

On the expectation of possible

high dividends and growth of the

market value of the shares, which

gives us hope for an increase in

the market share of the company

in the near future

30.

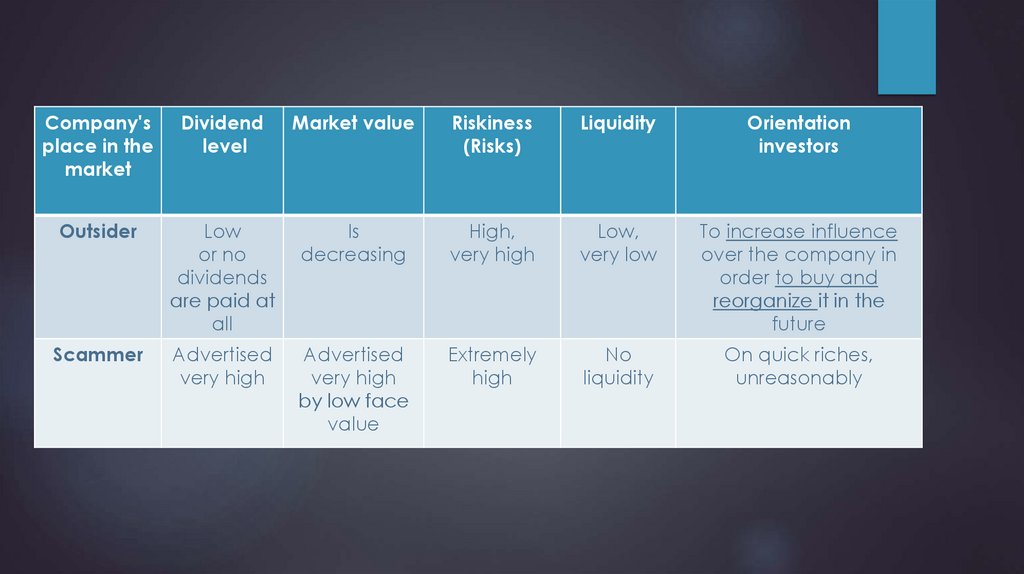

Company'splace in the

market

Dividend

level

Market value

Riskiness

(Risks)

Liquidity

Orientation

investors

Outsider

Low

or no

dividends

are paid at

all

Is

decreasing

High,

very high

Low,

very low

To increase influence

over the company in

order to buy and

reorganize it in the

future

Scammer

Advertised

very high

Advertised

very high

by low face

value

Extremely

high

No

liquidity

On quick riches,

unreasonably

31.

Dependence of stock prices on the stages of the lifecycle of an enterprise

32.

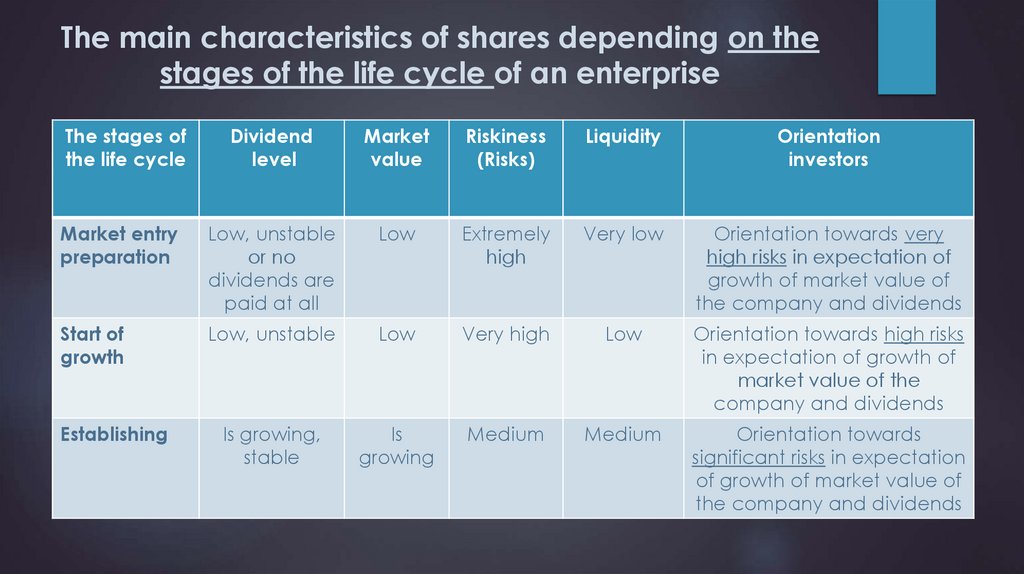

The main characteristics of shares depending on thestages of the life cycle of an enterprise

The stages of

the life cycle

Dividend

level

Market

value

Riskiness

(Risks)

Liquidity

Orientation

investors

Market entry

preparation

Low, unstable

or no

dividends are

paid at all

Low

Extremely

high

Very low

Orientation towards very

high risks in expectation of

growth of market value of

the company and dividends

Start of

growth

Low, unstable

Low

Very high

Low

Orientation towards high risks

in expectation of growth of

market value of the

company and dividends

Is growing,

stable

Is

growing

Medium

Medium

Orientation towards

significant risks in expectation

of growth of market value of

the company and dividends

Establishing

33.

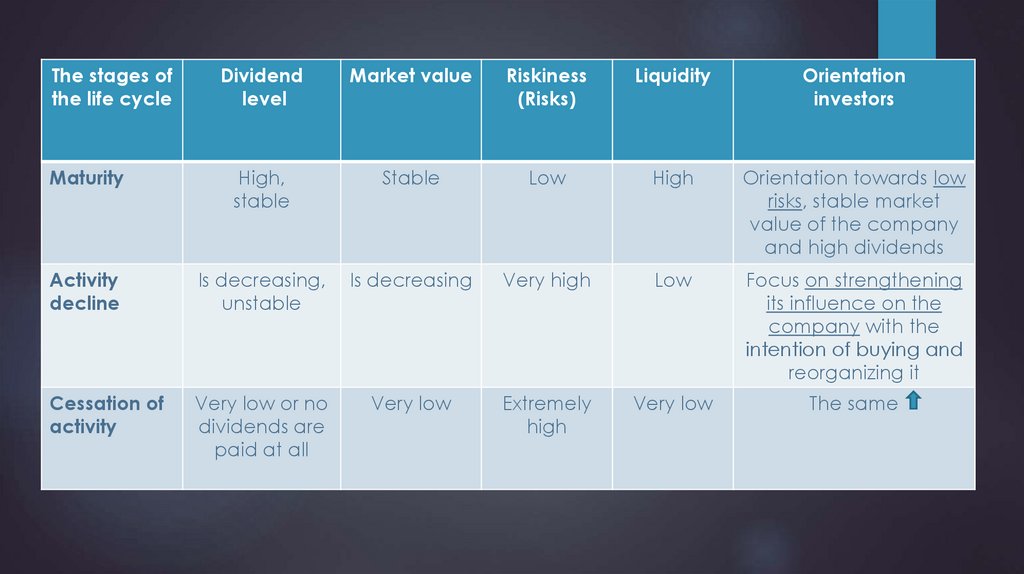

The stages ofthe life cycle

Dividend

level

Market value

Riskiness

(Risks)

Liquidity

Orientation

investors

Maturity

High,

stable

Stable

Low

High

Orientation towards low

risks, stable market

value of the company

and high dividends

Activity

decline

Is decreasing,

unstable

Is decreasing

Very high

Low

Focus on strengthening

its influence on the

company with the

intention of buying and

reorganizing it

Cessation of

activity

Very low or no

dividends are

paid at all

Very low

Extremely

high

Very low

The same

34.

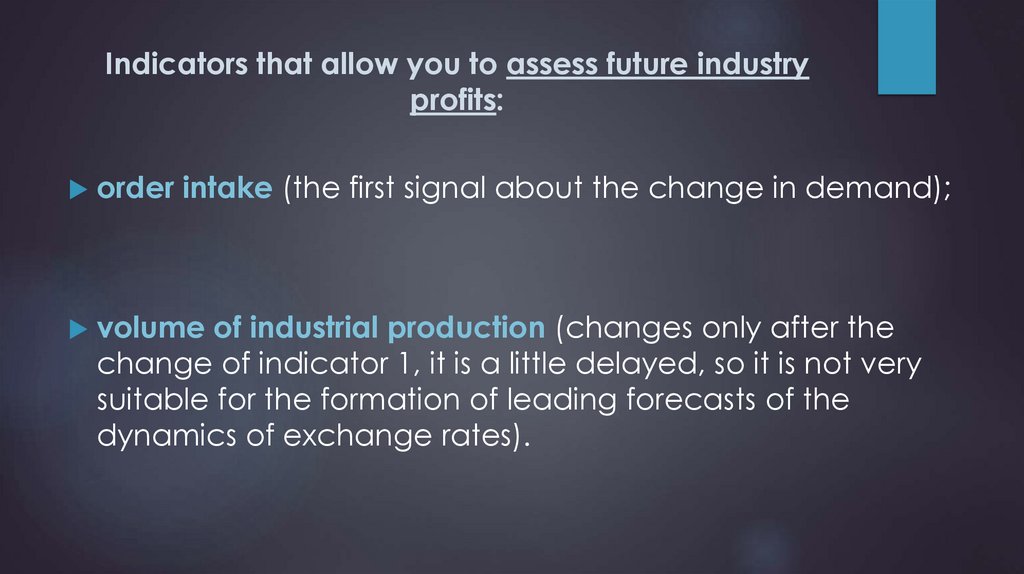

Indicators that allow you to assess future industryprofits:

order intake (the first signal about the change in demand);

volume of industrial production (changes only after the

change of indicator 1, it is a little delayed, so it is not very

suitable for the formation of leading forecasts of the

dynamics of exchange rates).