Экология

ЭкологияПохожие презентации:

Digital Ecosystem

1.

Digital Ecosystem2.

Storage Area Nonwork Satellite3.

FOLLOWING THE GOALS AND OBJECTIVES,GARUDA BANK INTENDS TO SUPPORT

THE BASIC NEEDS OF HUMAN DEVELOPMENT AIMED AT SOLVING SOCIALLY SIGNIFICANT PROBLEMS IN THE AREAS OF HEALTH,

EDUCATION, CULTURE, SOCIAL POLICY, PHYSICAL CULTURE AND SPORTS, ENVIRONMENTAL PROTECTION,

COMBATING DROUGHT AND WATER SECURITY AND LACK OF DRINKING WATER,

FIGHTING HUNGER AND DISEASE, IGNORANCE AND POVERTY.

DEVELOPING INFRASTRUCTURE, CREATING JOBS,

INVESTING IN THE PRODUCTION OF HIGH-QUALITY

AND ENVIRONMENTALLY FRIENDLY FOOD TO ENSURE FOOD SECURITY,

ESSENTIAL MEDICINES AND IMPROVE THE LIFE OF HUMANITY.

4.

Corporate (full official) name: GARUDA BANK LTDThe business plan drawn up 10.18.2020 from registration in the

PROGRAMS and receiving the status of the Bank license

- DIGITAL BANKING the grant of the following types of banking

operations with funds of local and foreign currency /AED, EURO, US$,

GBP, CNY. BTC/:

➢ attracting funds of individuals, legal persons and funds ' deposits

/demand and time/;opening and maintaining Bank accounts of

individuals and legal entities;

➢ making money transfers on behalf of individuals and legal entities,

including correspondent banks, to their Bank accounts;

➢ purchase and sale of foreign currency in cash and non-cash forms;

➢ attraction of precious metals for individuals and legal entities in

deposits /on demand and for a certain period of time /;opening and

maintaining Bank accounts of individuals and legal entities in

precious metals;

➢ making transfers on behalf of individuals and legal entities, including

correspondent banks, to their Bank accounts in precious metals;

➢ making money transfers without opening Bank accounts, including

electronic money;

➢ Project financing and loan disbursements;

Ensuring the Bank's operations.

The Bank is actually provided with the necessary resources for

sustainable financial activities.

The Bank has sufficient financial, labor, and material resources.

5.

The Bank's main Asset isThis is a Gold Mining Holding with a production base in

Arctic, Siberia & Far East Russia Federation,

established on a production basis

Million tons ore

The average Gold Grade in the ore is 4.5 g/t.

Total Resource Potential

EV/Resources

tons

troy ounces /Au oz.tr./

EV/Inventory

tons

troy ounces /Au oz.tr./

EV/Resources

tons

troy ounces /Ag oz.tr./

Licenses Exploration and Production

6.

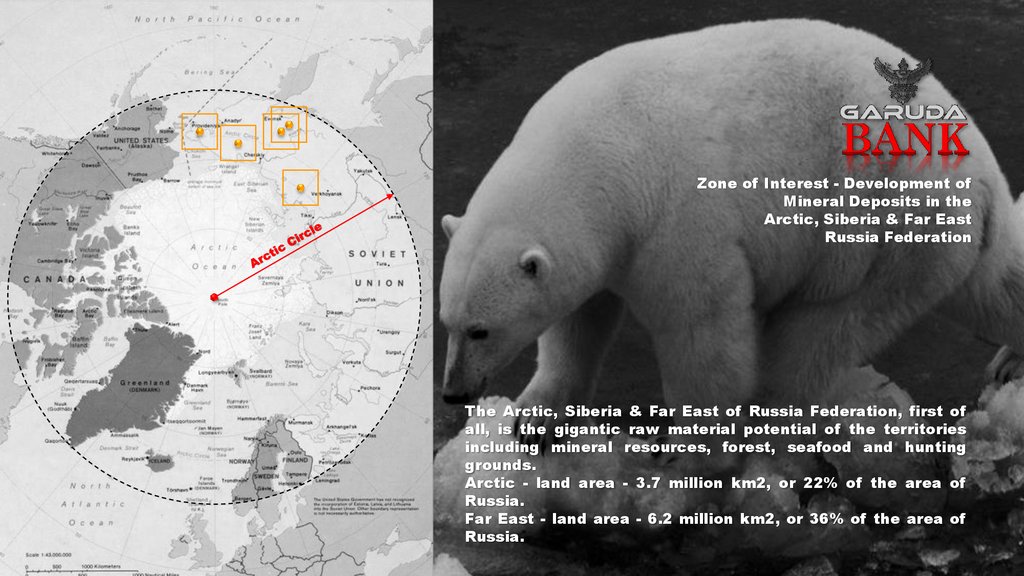

Zone of Interest - Development ofMineral Deposits in the

Arctic, Siberia & Far East

Russia Federation

The Arctic, Siberia & Far East of Russia Federation, first of

all, is the gigantic raw material potential of the territories

including mineral resources, forest, seafood and hunting

grounds.

Arctic - land area - 3.7 million km2, or 22% of the area of

Russia.

Far East - land area - 6.2 million km2, or 36% of the area of

Russia.

7.

DYNAMICS OF GROWTHWith growing uncertainty in the World, investing free money in Gold again attracts investors from different walks of life. Many people

view gold as a defense against capital crisis. The fact is that paper currencies are subject to depreciation, and the stock market is very

manipulative, so physical gold can be a reliable means of investing money to save it for the future. The history of gold as a means of

payment and exchange dates back thousands of years. In addition, the value of gold shows low volatility, which means that in times of

crisis it will be a stable currency and will not depend on banks and governments.

Experts say that gold will never lose its value, since production costs for its extraction are very high, and its amount in nature is no longer

becoming. Therefore, investors are practically not at risk when investing in yellow precious metals. It is recommended that you have up

to 10% of your investment portfolio in Gold. Thus, you can diversify and protect your assets from future crises. Unlike paper currencies,

which can be printed in unlimited quantities if desired, Gold is limited in the earth, which means its value will only grow over time. Since

the beginning of the current 2020, the price of gold has already shown an increase of + 12% in euros. Compared to the same period in

2019, growth was 1/3.

The analytical company S&P Global Market Intelligence reports that the number of new Gold deposits has decreased in the world.

Over the past three years, not a single major new field has been discovered, and over the past 10 years, only 25 large deposits have

been discovered. Another supporting factor for the price of Gold is the limited supply of yellow precious metals in the world.

Analysts believe that before the end of this year, she can overcome the mark of $ 2,500 per ounce. It is reported by CNN Business. Now

the precious metal is trading at $2,000 - this is very close to the 8-year high.

According to geological exploration, the world's gold reserves have decreased, and the number of new deposits has decreased

significantly. Gold miners complain of a decrease in gold in ore.

8.

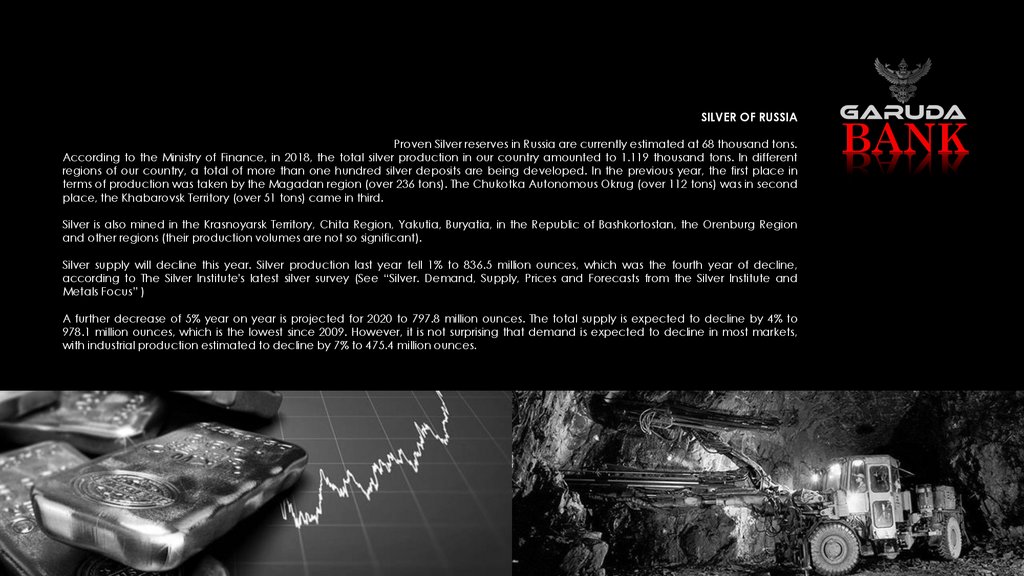

SILVER OF RUSSIAProven Silver reserves in Russia are currently estimated at 68 thousand tons.

According to the Ministry of Finance, in 2018, the total silver production in our country amounted to 1.119 thousand tons. In different

regions of our country, a total of more than one hundred silver deposits are being developed. In the previous year, the first place in

terms of production was taken by the Magadan region (over 236 tons). The Chukotka Autonomous Okrug (over 112 tons) was in second

place, the Khabarovsk Territory (over 51 tons) came in third.

Silver is also mined in the Krasnoyarsk Territory, Chita Region, Yakutia, Buryatia, in the Republic of Bashkortostan, the Orenburg Region

and other regions (their production volumes are not so significant).

Silver supply will decline this year. Silver production last year fell 1% to 836.5 million ounces, which was the fourth year of decline,

according to The Silver Institute's latest silver survey (See “Silver. Demand, Supply, Prices and Forecasts from the Silver Institute and

Metals Focus” )

A further decrease of 5% year on year is projected for 2020 to 797.8 million ounces. The total supply is expected to decline by 4% to

978.1 million ounces, which is the lowest since 2009. However, it is not surprising that demand is expected to decline in most markets,

with industrial production estimated to decline by 7% to 475.4 million ounces.

9.

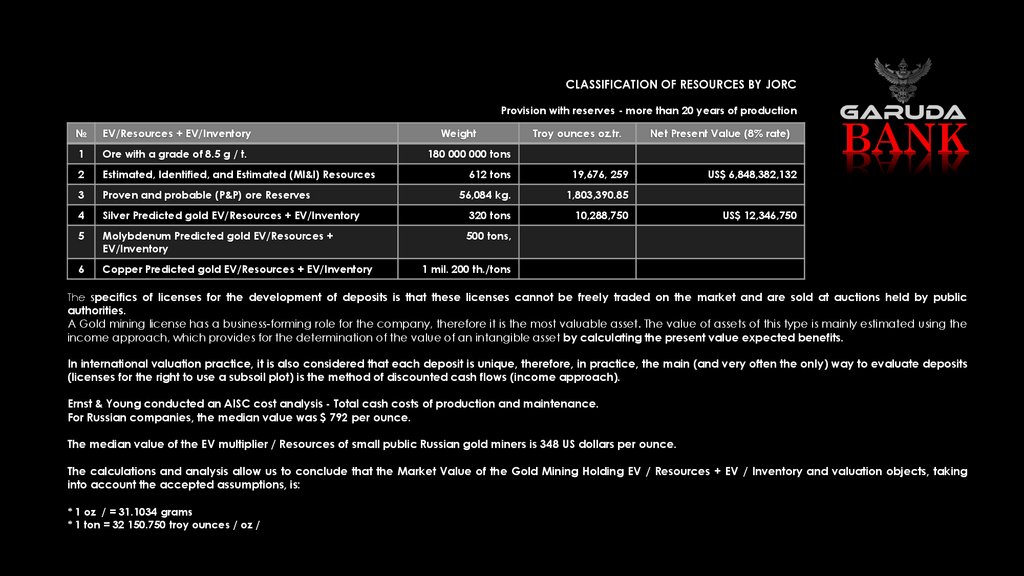

CLASSIFICATION OF RESOURCES BY JORCProvision with reserves - more than 20 years of production

№

EV/Resources + EV/Inventory

1

Оre with a grade of 8.5 g / t.

2

Estimated, Identified, and Estimated (MI&I) Resources

3

Proven and probable (P&P) ore Reserves

4

Weight

Troy ounces oz.tr.

Net Present Value (8% rate)

612 tons

19,676, 259

US$ 6,848,382,132

56,084 kg.

1,803,390.85

Silver Predicted gold EV/Resources + EV/Inventory

320 tons

10,288,750

5

Molybdenum Predicted gold EV/Resources +

EV/Inventory

500 tons,

6

Copper Predicted gold EV/Resources + EV/Inventory

180 000 000 tons

US$ 12,346,750

1 mil. 200 th./tons

The specifics of licenses for the development of deposits is that these licenses cannot be freely traded on the market and are sold at auctions held by public

authorities.

A Gold mining license has a business-forming role for the company, therefore it is the most valuable asset. The value of assets of this type is mainly estimated using the

income approach, which provides for the determination of the value of an intangible asset by calculating the present value expected benefits.

In international valuation practice, it is also considered that each deposit is unique, therefore, in practice, the main (and very often the only) way to evaluate deposits

(licenses for the right to use a subsoil plot) is the method of discounted cash flows (income approach).

Ernst & Young conducted an AISC cost analysis - Total cash costs of production and maintenance.

For Russian companies, the median value was $ 792 per ounce.

The median value of the EV multiplier / Resources of small public Russian gold miners is 348 US dollars per ounce.

The calculations and analysis allow us to conclude that the Market Value of the Gold Mining Holding EV / Resources + EV / Inventory and valuation objects, taking

into account the accepted assumptions, is:

* 1 oz / = 31.1034 grams

* 1 ton = 32 150.750 troy ounces / oz /

10.

POTENCIIAL MARKETEMIRATES is an important world center for gold trading.

Trading volumes are estimated in thousands of tons.

According to the report, 4,086 companies are active in the Dubai Gold market. Dubai imported 2018 gold totaling 65 billion Euros.

The structure of companies in the EMIRATES Gold market is as follows

➢ 2.498 firms are licensed to trade Gold and silver jewelry;

➢ 184 companies are registered to trade in gold and other precious metals;

➢ 392 jewelry companies;

➢ 7 firms are engaged in the production of Gold products;

➢ 5 companies are in the category "Gold refining and processing".

The UAE accounts for about 14% of the World Gold Trade.

EMIRATES, in particular, is constantly rising in the ranking in terms of purchases and investments.

Gold trading in the UAE is one of the most important sectors of the economy, accounting for 20% of the country's total exports, excluding oil.

11.

GARUDA BANK to Raise Capital, plans to issue GLOBAL DEPOSITARY RECIEPT / GDR /The Depository GARUDA BANK and the custodian Bank play a key role in the implementation of the issue project.

GDR / GLOBAL DEPOSITARY RECIEPT is a secondary security issued in the form of a certificate and certifying the right of its owner to possess

a certain amount of the underlying asset (stock or bond) of a foreign issuer.

The custody receipt is based on an agreement between the Issuer of shares and the Depository Bank. It stipulates the rights and obligations

of the parties, including with respect to investors. The provisions of such an agreement provide for terms, assets that are placed in the bank,

distribution of expenses, describe the process of issue and the transfer of receipts.

A separate depository bank holds shares of companies that are the subject of a receipt (GDR). The bank buys these shares and then issues

receipts that confirm that the bank owns the shares.

One of the advantages of GDR is that the investor buys receipts and has almost the same rights as the investor who purchases shares

directly in the stock market.

GDR / GLOBAL DEPOSITARY RECIEPT - fully equivalent in terms of ownership of the most basic asset - shares. According to them, the owner

will also receive dividends, and a change in the exchange rate of any type of depositary receipts will repeat the change in the exchange

rate of the underlying shares.

The implementation of the project will be closely linked with the use of digital technologies in the development of Gold deposits, which

provide the investment community with new tools for investing in a wide variety of projects, and for the initiators of such projects - additional

opportunities to attract the capital necessary for their implementation.

Feature of the project - This is a modern technology for investing and generating income, coupled with real reliable collateral. Using

blockchain technology, we plan to create a new economic model of relationships in the mining industry, in particular in Gold mining.

12.

Prospects for the Bank’s Development.Goals, objectives and market policy of the Bank.

The main priorities in the Bank's development are to ensure competitive advantages, increase assets,

profit and capitalization through the use of modern banking and information technologies.

Based on the expected scenario conditions for economic development, the Bank has identified the

main priorities of its activities for the forecast period:

➢ maintaining a high business reputation and maintaining the Bank's stability;

➢ the increase in the volume of transactions, expanding and improving the range of services in the

face of growing competition on financial markets;

➢ increasing the capital base, adequate growth of active operations of the Bank;

➢ ensuring the investment attractiveness of the Bank, increase profits;

➢ minimizing the risks of banking activities, primarily credit risk;

➢ the proper balance between liquidity and profitability of banking operations;

➢ expanding the client base in terms of population and enterprises of small and medium business;

➢ retail business development:

➢ the introduction of credit programmes (including through the promotion of the product "credit

card");the promotion of a common project of payment cards and customer service on remote

technologies (Internet);

➢ implementation of the program of increasing fee income through comprehensive customer service;

➢ the formation of the modern Bank, adequate to the scale and complexity of the business

management system:

➢ the adoption of flexible interest and tariff policy;

➢ use of effective internal control and risk management procedures for banking activities;

➢ optimization of costs within banking activities;

➢ minimization of the cost of attracted resources;

➢ formation of a team of professional and highly qualified employees, improvement of the personnel

motivation system;

➢ optimization of the asset structure in order to reduce the potential risk of losses. This implies an optimal

distribution of proportions between the four main areas of activity:

➢ corporate business;

➢ private banking;

➢ working in the securities market;

➢ interbank transactions;

➢ increase the efficiency of banking operations;

➢ optimize costs to ensure break-even operations.

13.

The Bank's strategic management includes the following stages:Formulation of the Bank's long-term goal.

➢ Formulation of long-term General principles for achieving the Bank's

goal.

➢ Based on the Goals and Principles - setting medium-term goals

(objectives) for the Bank's development in the selected areas of activity.

➢ Creating optimal conditions for achieving the Bank's medium-term goals

(objectives).Organization of effective operational management and

control over the achievement of medium-term goals (objectives).

➢ Setting new medium-term goals (objectives) in case of positive results in

achieving previously set medium-term goals /objectives/The main

strategic objectives for the planning period are:

➢ in terms of asset management:

➢ the establishment of a quality and profitable:

➢ portfolio of securities included in quotation lists of the first (highest) level

of the organizer of trading, and other securities that comply with the

basic license operations and transactions;

➢ loan portfolio based on minimization and diversification of credit risks;

➢ the increase in lending to small business and population, development,

and implementation

14.

An important goal for the Bank is to use favorable factors to strengthenitsposition in the banking sector.

In this regard, the Bank will take measures todevelop and implement a new

approach to customer service, business development, creationand

implementation of new banking activities and services.

The above-mentioned activities of the Bank include the following maintasks:

➢ implementation of an effective marketing policy in order to expand the

range ofbanking services, development and implementation of new

banking products;

➢ improvement of information technologies; optimization of the Bank's

organizational structure;

➢ optimizing the structure of active operations, increasing their profitability

whileminimizing financial risks;

➢ building a system to support operational decision-making inresource and

risk management.Based on the strategic aspects, the following directions

of strategicdevelopment are outlined:

➢ increase in profitable assets based on the principle of caution and

adequatedevelopment of the resource base;

➢ regulating the volume of the loan portfolio and securities portfolio in

order tomaintain high asset quality and liquidity;

➢ capital growth, taking into account the need to ensure a sufficient level

ofprofit for shareholders and the development of operations, subject to

compliance with the economicstandards established by the;

➢ strict control and minimization of investments in low-yield assets;

development and improvement of the internal Bank tax planning system;

➢ growth of Commission income due to traditional banking services and

introduction ofnew banking products; work in traditional segments of

the currency and money markets,ensuring revenue growth from resource

allocation operations and from the use ofnew financial instruments;

➢ carrying out activities in strict accordance with the requirements of the

currentlegislation and regulations of the Central Bank Tocounteract the

legalization (laundering) of proceeds from crime and thefinancing of

terrorism.

15.

The Bank's principles regarding the formation of banking technologies: theBank's Shareholders pay special attention to the introduction of advanced

technologies for banking operations, considering technology as the main

source of acquiring competitive advantages in the long term. So, as of

today, with the assistance of the main shareholders, a program is being

developed to create a ground and space segment of the Storage Area

Nonwork Satellite infrastructure, transfer and protect information based on

new physical principles (Quantum communication), developed

technologies and launching into earth orbit its own processing data center

that fully serves the created Ecosystem and the Issue of Bank payment

cards.

Own and intermediary operations in the money and financial markets:

performing operations to attract and place resources on various financial

markets in rubles and foreign currency on their own behalf and at their own

expense in strict accordance with the current banking legislation and

subject to the restrictions established for banks with a basic license. The

introduction of new product programs will increase the Bank's

attractiveness in working with awide range of clients. Attracting funds to a

Bank depends on the stability of its financial position and leads to an

increase in working capital.

The Bank's work on raising funds is based on the following main areas:

➢ attracting large corporate clients for servicing,

➢ gradual transition from short-term to long-term resources,

➢ organization of individual customer service,

➢ development of special products aimed at working with individuals,

including the development of Bank cards,

➢ expanding the network of partner banks in the interbank market.

➢ The placement of funds is based on the Bank's experience in lending as a

legal entity(including correspondent banks) and individuals.

16.

The main result of the Bank's activity should be the achievement of a stablefinancial result while maintaining a moderate investment risk. In its activities,

the Bank is guided by the principles of commercial activity, which increases

the efficiency of its work, strengthens its image, and promotes the

development of business relations with customers, partners, and other

banks.

Each Employee of the Bank is responsible for ensuring that their relations

with clients, correspondent banks, and colleagues contribute to the

effective operation of the Bank, its development, and improvement of the

quality of services provided.

The driving motive of the Bank's activity is to make a profit, in which all

participants in the economic process are interested, but the Bank does not

care what price the profit is achieved.

The Bank operates within the actual available resources. The Bank's

activities are carried outtalking into account the quantitative

correspondence between resources and credit investments, and the

correspondence of the nature of Bank assets to the specifics of the

attracted resources. First of all, this applies to the timing of both. Economic

independence in work implies freedom of disposal own funds and

attracted resources, income management, free choice of clients and

depositors. At the same time, economic independence also implies

economic responsibility for the results of its activities.

The Bank is liable for its obligations with all funds and property belonging to

it, taking all the risk from its operations on itself.

The Bank indicates its commitment to the principles of fair competition and

countering the legalization (laundering) of proceeds from crime and the

financing of terrorism.

The Bank's business reputation in the interbank market, among its clients

and partners, Is characterized by reliability and stability, which adds

confidence to the Bank's management in the correctness of the chosen

development strategy.

17.

Providing a full range of corporate banking services is the core of the Bank'sbusiness.

➢ Customer service will be provided with extensive use of electronic

banking tools;

➢ Attracting clients, improving the Bank's services and introducing new

banking products will be based on the development and

implementation of a program of marketing activities;

➢ The increase in the securities portfolio will be carried out in the part of

business with state and corporate securities included in the highest

quotation list;

➢ Loan volumes will be determined taking into account the adequate

development of the resource base, maintaining the proper quality of the

loan portfolio, and expanding the range of credit products. It will provide

for systematic monitoring of credit activities, first of all, a comprehensive

assessment of credit risks and the quality of the loan portfolio on an

ongoing basis. To this end, an appropriate mechanism for monitoring

financial and credit risks and managing problem loans is being formed;

➢ It occupies a special place in the Bank's activities and will continue to do

so in the future Bank lending. Interbank loans are a fairly reliable way to

place temporarily available funds of clients. The Bank will impose strict

requirements on its counterparties for interbank transactions, which will

be carried out on the basis of regularly reviewed limits;

➢ The Bank will provide standard loans and various forms of credit

lines(including overdrafts to the current accounts of corporate clients,

credit cards for individuals, etc.), which will allow customers to use credit

cards resources as needed with a significant reduction in their cost.

➢ The main conditions for granting loans are the solvency of customers, the

quality of the collateral offered, and the credit history of borrowers. The

set of financial instruments that the Bank will accept as collateral will

change in accordance with their actual market value;

18.

➢ As independent business entities, the Bank's shareholders considerinvesting their own funds in increasing the Bank's capital in the near

future, which will increase the Bank's stability and it will create

economic prerequisites for the Bank's successful development in the

following years of its activity;

➢ Focusing primarily on the provision of banking services (settlements of

legal entities, Bank cards for individuals), the Bank will actively

develop other profitable financial products to meet the needs of its

customers, changing under the influence of economic conditions;

➢ The introduction of new banking services will be accompanied by the

development of appropriate risk assessment procedures and

methodologies. Management experience and knowledge The Bank

and its staff, the up-to-date and accurate information systems, and

the effectiveness of the established risk limits will be key

characteristics of the quality of the risk management process. The risk

management process will be supported by sound accounting

procedures, comprehensive internal controls, and adequate

technology;

➢ The Bank will bet on the use of highly professional, constantly

improving their skills of personnel, guaranteeing competitive

advantages over other banks. Population dynamics of staff will be

determined primarily by the needs of the Bank in the specialists of this

or that direction, the structural composition - nature services provided

by the Bank.

➢ The Bank's personnel policy will beamed at maintaining a stable team

and attracting the best specialists from the labor market. It is planned

to use such a method aperiodic certification of personnel.

19.

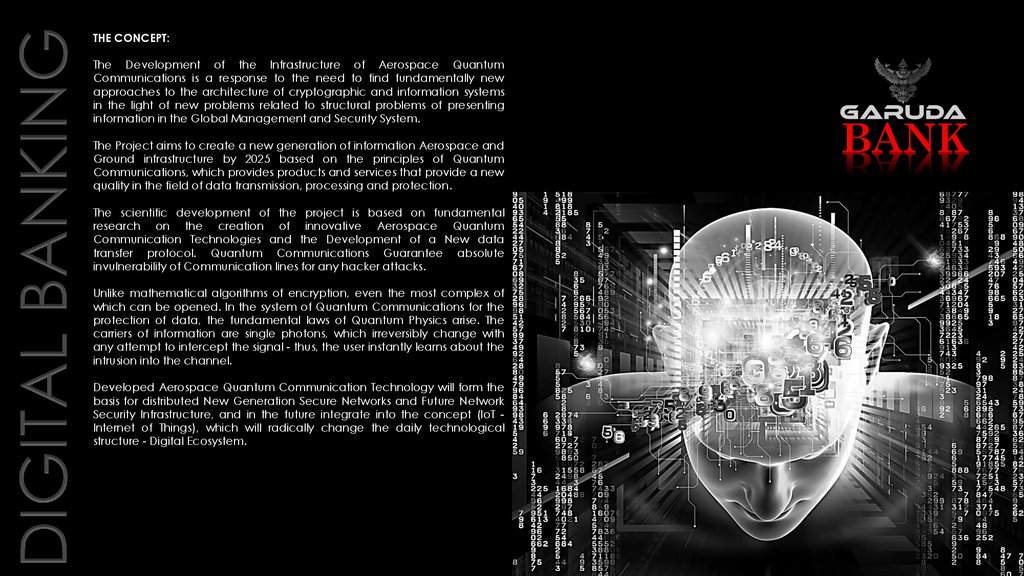

THE CONCEPT:The Development of the Infrastructure of Aerospace Quantum

Communications is a response to the need to find fundamentally new

approaches to the architecture of cryptographic and information systems

in the light of new problems related to structural problems of presenting

information in the Global Management and Security System.

The Project aims to create a new generation of information Aerospace and

Ground infrastructure by 2025 based on the principles of Quantum

Communications, which provides products and services that provide a new

quality in the field of data transmission, processing and protection.

The scientific development of the project is based on fundamental

research on the creation of innovative Aerospace Quantum

Communication Technologies and the Development of a New data

transfer protocol. Quantum Communications Guarantee absolute

invulnerability of Communication lines for any hacker attacks.

Unlike mathematical algorithms of encryption, even the most complex of

which can be opened. In the system of Quantum Communications for the

protection of data, the fundamental laws of Quantum Physics arise. The

carriers of information are single photons, which irreversibly change with

any attempt to intercept the signal - thus, the user instantly learns about the

intrusion into the channel.

Developed Aerospace Quantum Communication Technology will form the

basis for distributed New Generation Secure Networks and Future Network

Security Infrastructure, and in the future integrate into the concept (IoT Internet of Things), which will radically change the daily technological

structure - Digital Ecosystem.

20.

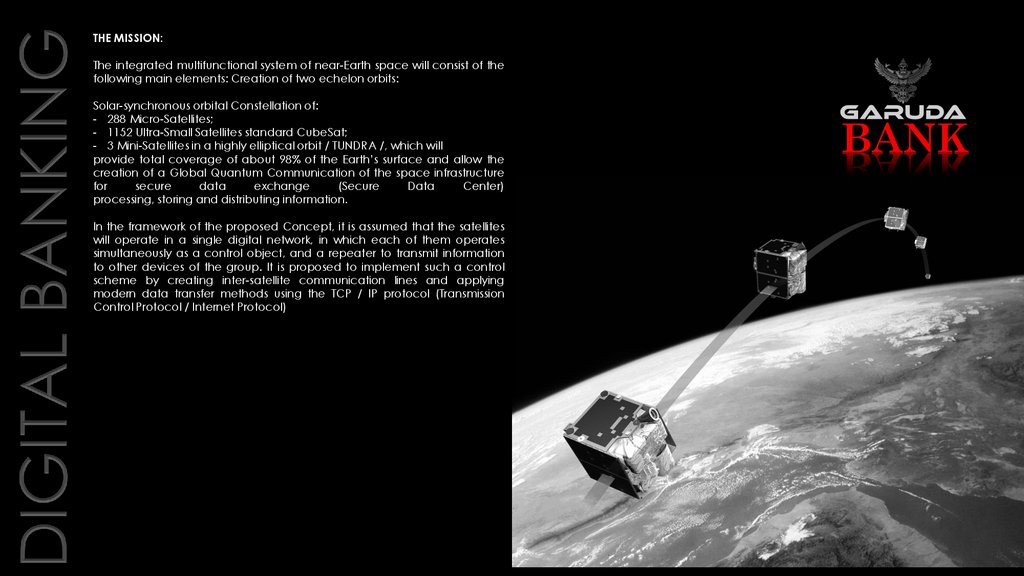

THE MISSION:The integrated multifunctional system of near-Earth space will consist of the

following main elements: Creation of two echelon orbits:

Solar-synchronous orbital Constellation of:

- 288 Micro-Satellites;

- 1152 Ultra-Small Satellites standard CubeSat;

- 3 Mini-Satellites in a highly elliptical orbit / TUNDRA /, which will

provide total coverage of about 98% of the Earth’s surface and allow the

creation of a Global Quantum Communication of the space infrastructure

for

secure

data

exchange

(Secure

Data

Center)

processing, storing and distributing information.

In the framework of the proposed Concept, it is assumed that the satellites

will operate in a single digital network, in which each of them operates

simultaneously as a control object, and a repeater to transmit information

to other devices of the group. It is proposed to implement such a control

scheme by creating inter-satellite communication lines and applying

modern data transfer methods using the TCP / IP protocol (Transmission

Control Protocol / Internet Protocol)

21.

MARKET POTENTIAL:Thanks to the trend of the transition of World, producers to the creation

ofsmall-scale Space Technology of the new generation are being opened

all the great opportunities for the development of near-Earth Space and

Earth exploration.

Creation of spacecraft given class capabilities in terms of minimizing costs

and in a short time to launch research satellites with a wide range of tasks.

In the world, large system and infrastructure projects are launched (in the

military sphere, telecommunications, biomedicine, etc.), which require

considerable productivity and security in the processing and transmission of

data.

The main way to solve these problems is the transition from electronics to

optoelectronics and the use of Quantum Technologies.

The market for devices for secure data transmission is currently formed by

crypto routers using classical algorithmic encryption, however the security

of such devices is based on the computational complexity of decryption.

With the growing powers of modern computing devices and the creation

of Quantum Computers, the level of security of classic crypto routers will fall,

and therefore such a class of systems will not be able to Guarantee

Information Security in the future. Recently, as an alternative to classical

cryptographic systems, systems of Quantum Cryptography that have

unconditional security in the transfer of keys are actively developed and

tested.

22.

MARKET SEGMENT:➢ The Market of Devices based on Quantum Principles;

➢ The Operator of Quantum Communication Service;

➢ Banking Security System Platform;

➢ Mobile Telecommunication Platform;

➢ Robotics Platform;

➢ Neuroelectronic Platform;

➢ Transport Platform;

➢ Communications Information Security Platform;

➢ State Institutions Platform;

➢ Military;

➢ E-commercial Platform;

➢ The Internet of Things App

Today in the World there is a request for updating the element base,

application of photonics and Quantum Technologies in high-tech

industries and readiness to change the technological infrastructure. The

project on the creation of the Scientific Satellite Technology Agency, the

production and further launching of Mini Satellites into the near-earth orbit,

will create a constellation of small Spacecraft working in close

cooperation that will unite the participants of the information process into

a unified network infrastructure of the new topology. Providing secure

data exchange with the help of new physical principles.

Quantum protocols for the exchange of information are tools developed

on the basis of Quantum Information theory and have increased

protection from the use of passive surveillance devices for

computer network traffic and in part cryptanalysis.

23.

SUSTAINABILITY:A breakthrough scenario for the development of the Project, involves the

exploitation of the unique properties of Quantum Technologies.

Conducting conceptual studies in the field of analog models, using the

cognitive and bionic approach in the design of ICT systems can lead to

the creation of an alternative architecture of computing systems and

networks, including in favor of the rejection of universal and centralized

devices. This scenario assumes a wide development of autonomous

closed systems, development of IoT (Internet of things) and transformation

into stand-alone smart devices, development of artificial intelligence

systems.

The project is expected to be implemented with a time horizon of 7 years.

The tasks of the project mentioned above can be conditionally divided

into the following interrelated groups:

➢ Harmonization of research and development in the field of Quantum

Informatics within a single road map;

➢ Selection of industrial partners and integrators that will ensure the

production and implementation of technologies;

➢ Construction of infrastructure for the production of components and

assembly of Quantum Communication systems;

➢ Assembly small-scale production of devices of Quantum Cryptography

and Quantum Generators of random numbers of the SPACE Segment;

➢ Approval of a list of critical equipment and components, the

production and / or certification of which is necessary for the

production of equipment for Quantum Communications;

➢ Conducting pilot tests in the part of integrating Quantum

Communications into information networks;

➢ Putting into operation of high-tech productions of components and

assembly of systems of Quantum Communications of the SPACE

Segment; In this regard, the implementation of the project, as the basis

of the Global Information Security, can become a driver for the

development of many high-tech industries.

Such an integral infrastructure has not yet been created in the World

24.

INVESTMENT PROJECT:Ensuring Water and Food Security is one of the priorities of state policy, since it covers a wide range of national, economic, social,

demographic and environmental factors. The stability of domestic production, as well as the availability of necessary reserves and

reserves, is a guarantee of solving this most important state problem.

The main Investments of GARUDA BANK will be directed to the creation of an infrastructure project and a Resident company:

The strategic goal of the project - Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI - is to create a high-tech industrial

and innovative growth zone in the United Arab Emirates based on the sustainable development of year-round cultivation and

integrated processing of environmentally friendly fruit, berry, vegetable, meat and dairy products, as well as the development of

related industries that combine the most advanced technologies with a high level of efficiency and depth of processing.

Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI is the first project of this scale to be implemented in the Middle East. It

will help create conditions for the promotion of modern scientific ideas, as well as early testing of advanced technologies and the

study of economic efficiency, which will create conditions for sustainable long-term socio-economic development through the

formation of a modern platform in the format of the Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI , attractive to

investors aimed at creating competitive high-tech industries, creating an element of investment infrastructure that unites links in the

chain of agro-industrial production, providing access to the Middle East market for agricultural producers.

Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI will represent an organizational Alliance of the government and the

private sector (Public-Private Partnership-PPP) for the purpose of implementing significant and socially important strategic projects

between enterprises of the Republic of Moldova and companies from the United Arab Emirates. It will become a multi-disciplinary

innovation structure for promoting the agricultural sector and will form a system of industries of various specialization based on the

cluster principle, United in a single agro-biotechnological complex with a closed cycle.

25.

The unique concept of Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI will create an international interactive platformfor identifying the most promising areas and effective solutions for the development of the agro-industrial sector in the region. The

core of the project of the Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI will be a scientific and educational cluster,

as the need for qualified personnel in the presence of material and production base sets the task of training local specialists for

various fields of agricultural profile and the formation of the regional labor market.

The plan includes the construction Research center to enhance ater security, as well as high-tech cluster clean-up and preparation

of biologically active, high-quality water – Deuterium Depleted Water (DDW) for the needs of crop, livestock and poultry; production

and logistics complex consisting of modern greenhouses; animal husbandry, poultry; vegetable stores and warehouses, including

refrigerators and freezers with eco-friendly systems of artificial climate with no refrigerants, ammonia and Freon.

In addition, the Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI will operate production for processing agricultural

products and food, production of highly active biological feed, wholesale and e-Commerce, a service center for modern

agricultural machinery and an Agro-Exhibition Complex with offices and a hotel for the development of agro-tourism.

The project envisages the creation of the Institute of bioresources and mariculture, and the construction of coastal fishing and

commercial AQUA-BIOTECHNOPARKA (Open-ocean) to obtain a physiologically adequate juvenile fish, invertebrates, plants

macrophytes and live feeds via stable and sustainable development of the resource base, including through the creation of hightech knowledge-intensive industries, which will introduce the technology of complex non-waste deep processing and production of

drugs, food products, quality nutritional supplements for animal feed and veterinary drugs in livestock on the basis of biological raw

materials of marine origin.

Products produced by residents of the Special Economic Agro Zone AGRO-TECHNOPARK ABU DHABI will be sold under their own

brand, undergo a thorough check at the product certification center, guaranteeing customers consistently high quality along with

an affordable price. Environmental safety and uninterrupted supply will be one of the key components of the brand.

Attracting international anchor residents at the first stage will give the project of the Special Economic Agro Zone AGROTECHNOPARK ABU DHABI a high status of an International agro-center, and will also help attract the second wave of residents directly

from foreign and local agricultural producers, distribution and trading companies.

26.

Risk Management.Risk – the possibility (probability) of the Bank incurring losses (losses), non-receipt of planned revenues and/or deterioration of

liquidity and/or occurrence of other adverse consequences for the Bank due to various events related to internal and/or external

factors of the Bank's activities that objectively exist in the conditions of uncertainty inherent in banking activities.

The Bank classifies the main banking risks arising in the Bank's activities into two components:

- financial risk;

- non-financial (functional) risks.

Financial risks – risks on operations (transactions) of the Bank that arise due to the movement of financial flows and are manifested

in the financial resources markets.

Financial risks include:

- credit risk;

- market risk;

- interest rate risk;

- isk of loss of liquidity.

non-Financial (functional) risks – banking risks, the occurrence of which is not related to the conduct of any operations

(transactions) and/or the provision of banking services(products’).

These include:

- operational risk- strategic risk,

- regulatory risk (compliance risk).

Concentration risk – the risk that the Bank will incur losses (losses) or not receive planned revenues as a result of concentration of

certain types of risks.

The main strategic goal of risk management, as an integral part of the Bank's management process, is to minimize financial losses

from the implementation of risks, as well as to ensure sustainable development of the Bank and achieve financial reliability of the

Bank.

The main approach to minimizing Bank risks is to determine their quantitative parameters and development of risk management

methods. The Bank's Board of Directors adopted the "risk and capital management Strategy", and the Bank's management Board

approved the" Regulations on risk and capital management", including procedures for managing significant risks.

27.

The purpose of the Bank's risk management policy is to organize a clear process for effective risk management by settingboundaries and limit parameters foreach type of risk. In the context of a downward trend in the profitability of most financial

instruments and, as a result, a decrease in profitability, risk control is one of the most important the main sources of maintaining the

Bank's profitability at the proper level.

An effective way to minimize risks is to regulate them by setting limits.

In accordance with the "risk appetite", the Bank sets the main risk limits, and asset and liability management decisions are analyzed

for possible violations of the established limits.

The main objective of the limit setting system is to ensure that the Bank's assets and liabilities structure is adequate to the nature and

scale of its business.

Within the framework of risk management, the Bank assumes the following main tasks:

- ensuring compliance with regulatory and Supervisory authorities ' requirements for the adequacy of the Bank's risk management

system;

- differentiation of competence and responsibility at different levels of management In the Bank in the field of risk management;

- optimization of the ratio of risk and financial results in all areas of the Bank's activities;

- identification, measurement (assessment) and determination of acceptable level of risks, its limitation and risk control;

- continuous monitoring and control of the risk level;

- ensuring the normal functioning of the Bank in crisis situations;

- avoiding long-term exposure of the Bank to excessive risk;

- achieving correct integration of the Bank's risk management system into the Bank's overall asset and liability management

structure.

Credit Committee.

In order to reduce credit risks, The Bank has established a Credit Committee.

The credit Committee is a permanent collegial body designed to review banking products that have credit, legal and market risks

and make appropriate decisions on them.

The credit Committee is created to resolve issues related to attracting and placing credit resources and other issues within its

competence established by the Credit policy and other internal documents of the Bank on attracting and placing funds.

The credit Committee at its meetings determines the priority types and directions offending, the procedure for reviewing the client's

application and decides on granting and changing the terms of lending, ways to ensure loan repayment, issues related to the

issuance of guarantees, credit conditions

28.

The Bank's Charter will define the system of bodies that exercise internal control in the Bank, the procedure for their formation andpowers, as well as the organizational structure of the Bank in terms of the distribution of powers between the General meeting of

shareholders and the Board of Directors of the Bank,

The Bank's management Board and Chairman of the management Board.

The Charter and internal documents of the Bank define the powers, accountability and responsibility of all structural divisions of the

Bank and its employees in accordance with the nature and scale of operations performed and the level and combination of risks

assumed.

Internal control in the Bank is carried out in accordance with the powers defined by the Bank's constituent and internal documents

by the following bodies

➢ management Bodies – the General meeting of shareholders,

➢ Board of Directors, the Bank's Management Board,

➢ Chairman Of The Bank's Management Board;

➢ The Bank’s Audit Commission;

➢ Chief Accountant of the Bank;

➢ Internal Audit Service of the Bank;

➢ Internal Control Service of the Bank;

➢ Risk Management Service;

➢ Responsible officer (structural division) on counteraction to legalization(laundering) of incomes obtained in a criminal way,

The Bank's internal control system includes the following areas:

➢ control by the management Bodies over the organization of the Bank's activities;

➢ control over the functioning of the banking risk management system and evaluation banking risk;

➢ control over the distribution of powers when performing banking operations and other transactions;

➢ control over the management of information flows (receiving and transmitting information) and ensuring information security;

➢ continuous monitoring of the operation of the system internal control in order to assess its compliance with the objectives of the

Bank's activities, identify shortcomings, develop proposals and monitor the implementation of decisions to improve the Bank's

internal control system (hereinafter referred to as monitoring the internal control system).

29.

Internal documents regulating banking operationsAll divisions of the Bank act on the basis of the relevant internal Bank Regulations, which establish, among other things, the direct

subordination (control) of the division, and within the limits of the powers granted by these Provisions.

The activities of the Bank's employees are regulated by the relevant job descriptions.

Development of internal regulations, regulations, procedures, methods, instructions and other documents regulating the Bank's

activities (hereinafter referred to as internal documents), as well as their updating, editing, making changes and additions is carried

out in the following cases:

➢ changes in the current legislation of the Emirates;

➢ introduction of new business processes, business lines, transactions and operations;

➢ changes in the Bank's organizational structure, including the formation of new structural divisions, collegial bodies, and the

introduction of additional positions in the staffing table;

➢ the need to optimize current business processes, business lines, transactions and operations, and the Bank's overall operations;

➢ in other cases that require the development, updating, editing, or ordering of internal documents. Internal documents are

approved by the Bank's management bodies in accordance with their competence:

➢ the General meeting of the Bank's participants;

➢ By the Bank's Board of Directors;

➢ board of bank;

➢ Chairman Of The Bank's Management Board.

The development of internal documents, as well as their updating, editing, making changes and additions, may initiate:

➢ The Bank's management bodies;

➢ The internal audit service;

➢ The internal control service

➢ Risk management service

➢ Legal department;

➢ Heads of structural divisions (persons who replace them, persons acting as heads of structural divisions, responsible employees).

30.

When forming the staff, the Bank sets qualification requirements for employees.The qualification requirements include: requirements for the level of professional education, work experience in the specialty,

training direction, professional knowledge and skills necessary for the performance of official duties.

To the sole Executive body, its deputies, members of collegiate Executive body, chief accountant,

Deputy chief accountant, head and chief accountant of the branch, to the persons exercising the functions of the heads of the risk

management Department, internal control Service, internal audit Service of persons appointed to these positions (candidates for

these positions) the Bank shall notify the qualifying requirements and requirements to business reputation in accordance with the

regulatory requirements of the Bank EMIRATES.

Implementation of the principle of professionalism and personal competencies is carried out through amulti-stage selection and

admission procedure on a competitive basis. At the same time, the assessment of the candidate's professional competencies is

carried out by the direct supervisor. Employee (first stage) and supervising Deputy Chairman of the management Board (second

stage). The personal and socio-psychological qualities of the candidate are evaluated by the direct Manager of the future

employee, and the conclusion on the compliance of these qualities with the Bank's requirements and the candidate's compliance

with the Bank's corporate culture is brought to the attention of the Bank's management.

Creating an effective labor motivation system

The goal of creating and developing an effective motivation system is to ensure that each employee of the Bank is directly and

consistently interested in achieving the planned performance of their personal work, and, if possible, in improving the results in

comparison with the planned ones. The main component of the Bank's employee motivation system is the mechanism of monetary

remuneration for work. The main principle in the system of monetary remuneration is equal pay for equal work, which means the

same level of wages for employees who occupy the same complexity and importance of positions (jobs)and show equal levels of

performance. Monetary remuneration in the Bank consists of: a permanent guaranteed part, acting as an official salary, a personal

allowance, and a bonus.

All payments provided for by the labor remuneration system are made at the expense of funds Remuneration Fund, the amount of

which is approved annually by the Board of Directors.

The remuneration Fund includes any accruals to employees in cash and in kind, compensation accruals related to working hours or

working conditions, incentive accruals and allowances, bonuses and one-time incentive accruals for production results and other

expenses related to the maintenance of Bank employees in the performance of their work functions.

31.

Maintaining organizational order in the BankThe most important condition for achieving the Bank's strategic goals is the unconditional fulfillment by all employees of the Bank of

their official duties, strict compliance with labor and production discipline, demanding managers to their subordinates, and the

unconditional fulfillment by subordinates of orders, instructions and work tasks set by managers.

The basis of performance is the organizational order in the Bank, when employees they know and perform their job responsibilities

as set out in the job descriptions, managers are responsible for decisions made within their area of responsibility, planning, reporting

and monitoring the implementation of decisions made is carried out in accordance with the adopted and approved rules,

methods and instructions.

Corporate culture of the Bank.

Corporate culture is a system of beliefs, norms of behavior, attitudes and values that are the rules that determine how employees

should work and behave Bank.

The Bank pays great attention to understanding the role and significance of corporate culture for success in implementing not only

short-term but also long-term strategic goals, and the ability to form the required level of culture, as this is an essential condition for

successful organizational changes and is designed to create a sense of involvement in common goals among Bank employees.

Corporate culture is strengthened through company-wide activities aimed at fostering a sense of community, belonging to the

Bank, loyalty and reliability in the work of the Bank's employees. Creating a positive image both outside and inside the Bank

contributes to the education and promotion of corporate identity and a positive social and psychological atmosphere in the Bank's

team.

The determining factor for the Bank's success in the market will be its ability to offer high-quality service and convenient access to

services, while maintaining competitive prices. The Bank will use alternative sales channels, packaging technologies, and crossselling tools. Working in all market segments and strengthening mutual trust, the Bank will encourage customer loyalty and provide

existing and potential customers with the opportunity to acquire the necessary knowledge in the field of financial services.

The Bank builds its long-term strategy taking into account objective patterns of economic development and the nature of the tasks

set by the course of economic processes in the country. Currently, the Bank's shareholders Express their interest in expanding the

Bank's activities in the financial services market. Active participation of its main shareholders in the Bank's work, constant joint work

of the Bank's Board of Directors and the Bank's Management Bourdon expanding the range of banking services, allows the Bank to

plan activities that involve the support of all the Bank's shareholders.

An important task of the Bank is to create a balanced low-riskportfolio of securities and loan portfolio. The Bank's management has

approved a credit policy that imposes strict requirements on the quality of borrowers ' collateral, guarantees of loan repayment,

and more carefully checks the creditworthiness of organizations.

32.

GLOBAL PLATFORM FOR GLOBAL MARKETWe create a set of payment services around a person that are necessary

for their life. In the same way, we create a set of payment services for

businesses that are necessary for their daily work