Финансы

ФинансыПохожие презентации:

Introduction to Accounting

1. Introduction to Accounting

Bibigul Zhakupova1

2.

• What is Accounting?– What Accounting is about?

– Why Accounting is needed?

– Where Accounting takes place?

– What accountants are doing at work?

2

3.

What is Accounting?3

4.

Financial AccountingManagerial Accounting

Tax Accounting

4

5.

Accounting is ….a language

of business

5

6. Accounting is a language of business….

Cash InflowCash Outflow

Revenue

Costs

Profit

Income

Gains

Earnings

Expenses

Losses

6

7.

The Company / Business EntityCoca Cola

Proctor and Gamble

Exxon Mobil

IKEA

KPMG

7

8.

Financial Accounting8

9.

What are the main functionsof Financial Accounting?

To collect information about company’s

business transactions;

To prepare Financial Reports from this

information.

9

10. Functions of Accounting

To Collect Information……..What Kind of Information?

10

11. Information regarding

business transactionsof the Company

11

12.

What kind of transactions arecalled “business transactions” ?

12

13.

What kind of transactions arecalled “business transactions” ?

Examples:

Purchase of raw materials

Purchase of equipment

Construction of plant, administrative building

Payment of salaries

Payment for electricity and utilities

Sale of furniture

13

14.

How information regarding“business transactions” is

collected ?

14

15.

How information regarding “businesstransactions” is collected ?

By collecting source documents

about business transactions

15

16.

The collected information isrecorded.

How it is recorded?

16

17.

The collected information isrecorded.

How it is recorded?

By journal entries, using debits

and credits

17

18.

Financial Statements areprepared from those records

through the process called

Accounting Cycle

18

19.

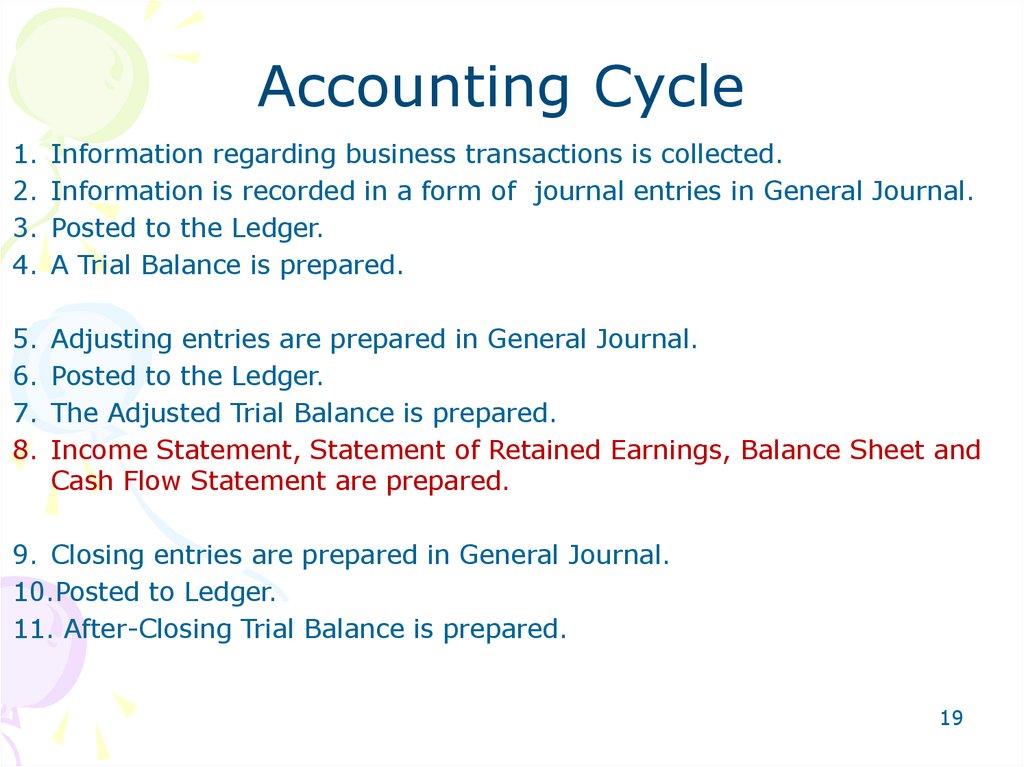

Accounting Cycle1. Information regarding business transactions is collected.

2. Information is recorded in a form of journal entries in General Journal.

3. Posted to the Ledger.

4. A Trial Balance is prepared.

5. Adjusting entries are prepared in General Journal.

6. Posted to the Ledger.

7. The Adjusted Trial Balance is prepared.

8. Income Statement, Statement of Retained Earnings, Balance Sheet and

Cash Flow Statement are prepared.

9. Closing entries are prepared in General Journal.

10.Posted to Ledger.

11. After-Closing Trial Balance is prepared.

19

20.

Financial Reports are preparedin accordance with rules

similar to all business entities

20

21.

Accounting standards:• IFRS (МСФО) - European

standards;

• GAAP – US standards;

21

22.

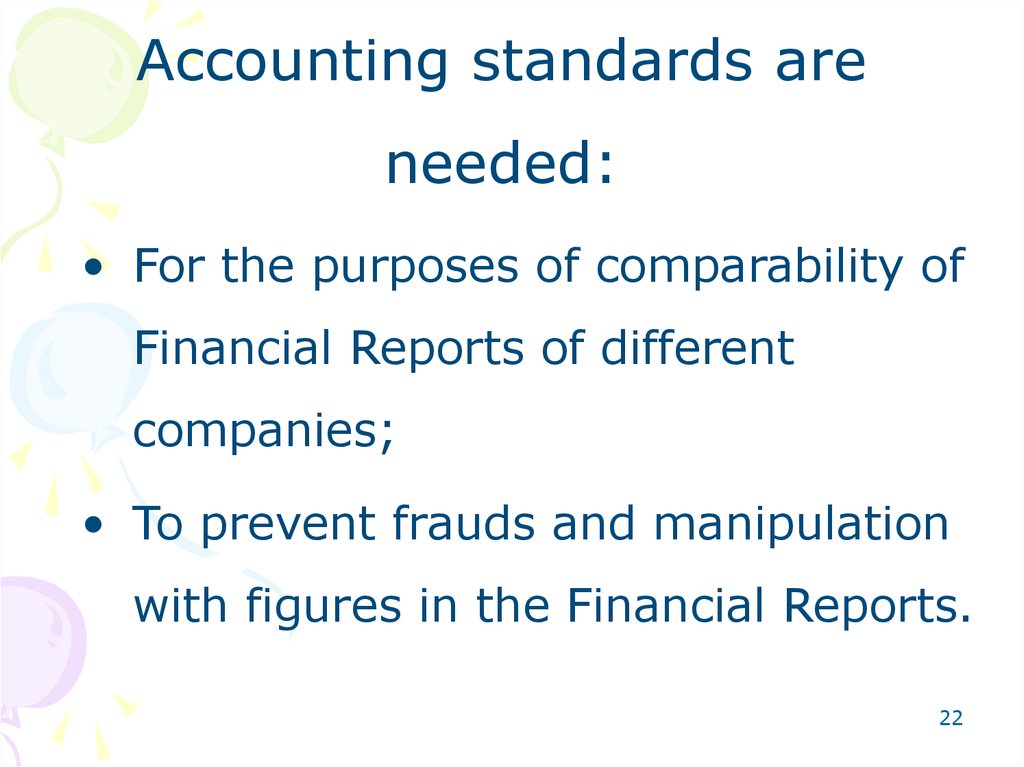

Accounting standards areneeded:

• For the purposes of comparability of

Financial Reports of different

companies;

• To prevent frauds and manipulation

with figures in the Financial Reports.

22

23.

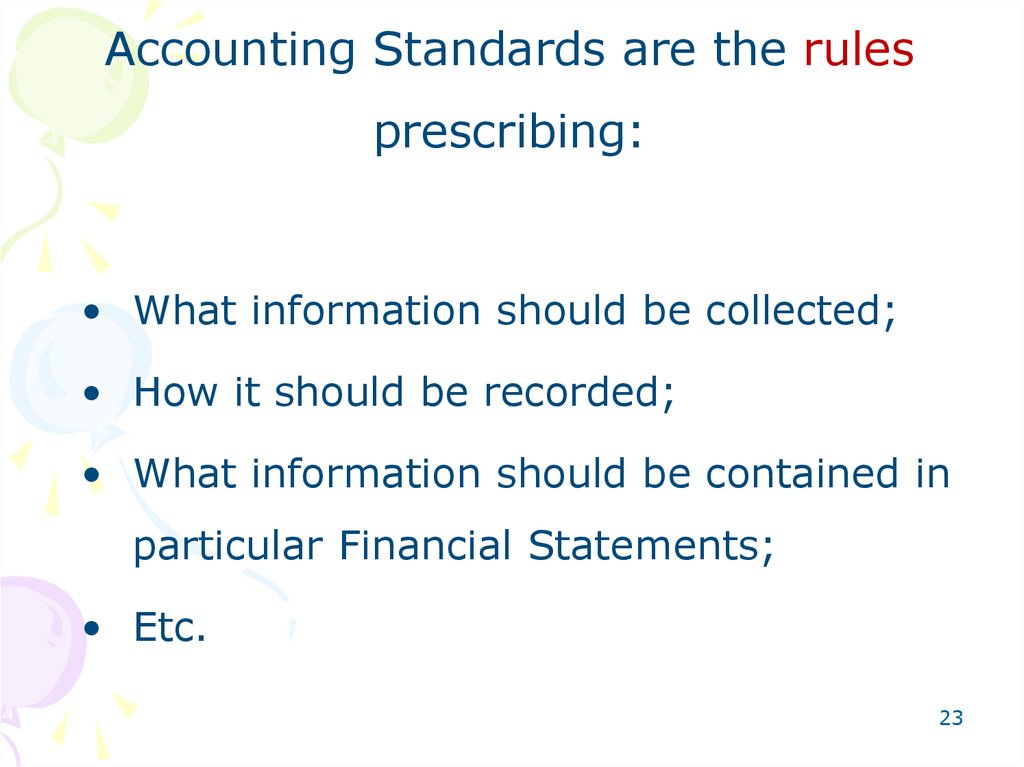

Accounting Standards are the rulesprescribing:

• What information should be collected;

• How it should be recorded;

• What information should be contained in

particular Financial Statements;

• Etc.

23

24.

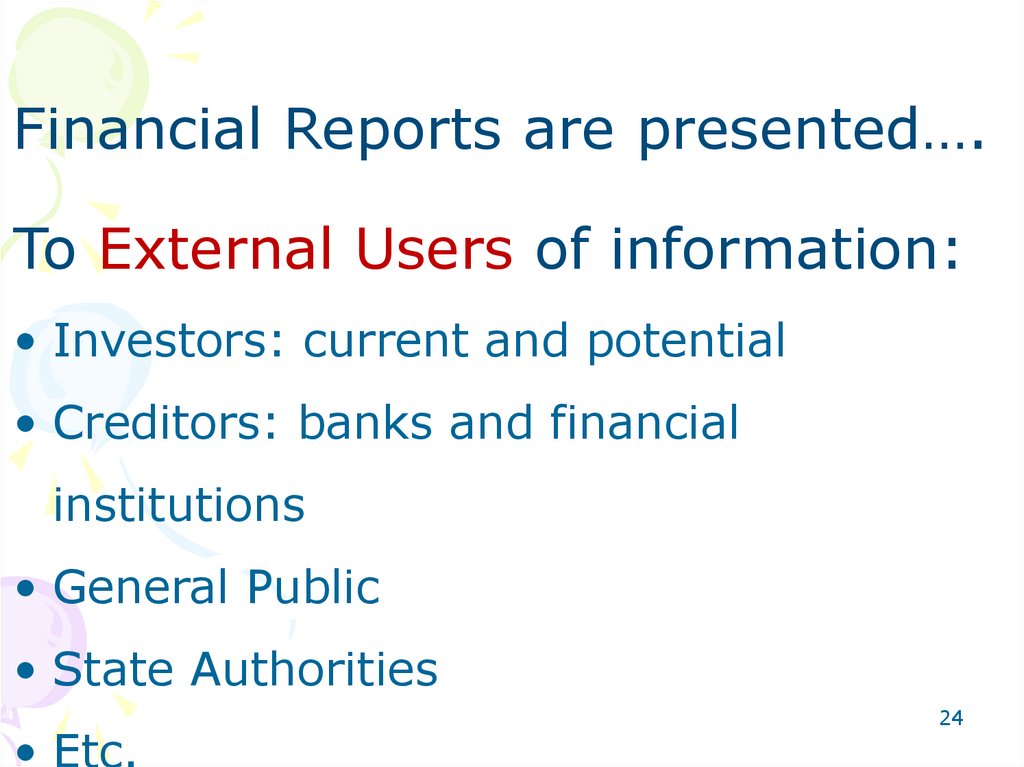

Financial Reports are presented….To External Users of information:

• Investors: current and potential

• Creditors: banks and financial

institutions

• General Public

• State Authorities

• Etc.

24

25. Financial Accounting

Why to present informationregarding the company’s

financial performance and

financial position to the

external users?

25

26. Financial Accounting

Investors and Creditors should makea crucial decision:

How to allocate their (limited)

resources in the most optimal way?

26

27. Financial Accounting

Information regarding business transactions of the company is collectedInformation is recorded

Financial Reports are prepared:

• Income Statement

• Balance Sheet

• Statement of Cash

Flows

• Disclosure Notes

Accounting

Standards:

e.g. IFRS, GAAP

Financial

Statements

External Independent Audit

External Users:

•Investors

•Creditors

•General Public

•State Authorities

•Etc.

27

28. Disclosure Notes

Mainly provide:1.

Description of the main Accounting Policies;

2.

Explanation to some items/figures shown in

Financial Statements;

3.

Some information which is not present in the

Financial Statements (because does not belong to

the reporting period), however crucial for investors

to make decisions.

28

29. The company’s Accounting Policy

• Prepared by the Chief Financial Officer and ChiefAccountant;

• Approved by the Board of Directors and Board of

Shareholders;

• Based on Accounting Standards;

• Describes how accounting is conducted for

specific transactions;

29

30. Financial Accounting

Informationregarding

business

transactions is

collected

Accounting

Cycle

Financial Report:

• Financial Statements:

1. Balance Sheet;

2. Income

Statement;

3. Cash Flow

Statement;

4. Statement of

Retained

Earnings

• Disclosure Notes

30

31. Financial Accounting

1. Information regarding business transactions is collected;2. Financial Report is prepared;

3. Financial Report should be prepared in accordance with

accounting standards;

4. Financial Report should contain information only about

past transactions which really occurred;

5. Financial Report should be audited by an independent

auditor;

6. Financial Report is presented to external users (mainly to

Investors and Creditors) for analysis;

7. Based on the results of the analysis Investors and

Creditors will make an investment/loan decision.

31

32. Managerial Accounting

Collect information for internal users:1. Management of different levels;

2. Employees.

32

33. Managerial Accounting

What kind of information?Information which helps managers to run

the company in the most efficient way.

33

34. Functions of Management:

PlanningDirecting and

Motivating

Controlling

35. Planning and Control Cycle

Formulating longand short-term plans(Planning)

Comparing actual

to planned

performance

(Controlling)

Decision

Making

Measuring

performance

(Controlling)

Begin

Implementing

plans (Directing

and Motivating)

36. Managerial Accounting

Information which helps managers to run the companyInformation is collected and recorded

No Standard Reports

• What information to collect?

• How often?

• In what form to record and

present?

• What tools of analysis to use?

No rules such as

Accounting Standards

Discretion of the

managers

Internal Users:

•Management of different levels

•Employees

36

37. Comparison of Financial and Managerial Accounting

Financial AccountingManagerial Accounting

External persons who

make financial decisions

Managers who plan for

and control an organization

Historical perspective

Future emphasis

3. Verifiability

versus relevance

Emphasis on

verifiability

Emphasis on relevance

for planning and control

4. Precision versus

timeliness

Emphasis on

precision

Emphasis on

timeliness

5. Subject

Primary focus is on

the whole organization

Focuses on segments

of an organization

6. GAAP/IFRS

Must follow GAAP/IFRS

and prescribed formats

Need not follow GAAP/IFRS

or any prescribed format

7. Requirement

Mandatory for

external reports

Not

Mandatory

1. Users

2. Time focus

37

38. Tax Accounting

Information regarding the company’s tax obligations andpayments is collected and recorded

Tax Reports

Corporate Income Tax Report

Value Added Tax Report

Individual Income Tax Report

Social Tax Report

Etc.

Tax Code

Audit by the Tax

Committee

External Users:

•State Authorities – Tax Committees

•Financial Police

•Other.

38

39.

Thank you!Any questions?

39