Финансы

ФинансыПохожие презентации:

Account of taxes and mandatory payments in banks

1. ACCOUNT OF TAXES AND MANDATORY PAYMENTS IN BANKS

2.

21. Types of budget and extra-budgetary payments of the bank

and their calculation.

2. The procedure for calculating and accounting for income tax,

value added tax, environmental tax, property tax in banks.

3. Reflection of operations on extra-budgetary payments in bank

accounting.

3. Commercial banks, as legal entities, pay the following taxes and make deductions to the state budget. Namely: - profit tax from

1. Types of budget and extrabudgetary payments ofthe bank and their calculation.

COMMERCIAL BANKS, AS LEGAL ENTITIES, PAY THE FOLLOWING TAXES

AND MAKE DEDUCTIONS TO THE STATE BUDGET. NAMELY:

- PROFIT TAX FROM LEGAL ENTITIES;

- PROPERTY TAX;

- LAND TAX;

- TAX FOR THE USE OF WATER RESOURCES;

- VALUE ADDED TAX;

- PERSONAL INCOME TAX;

- INSURANCE CONTRIBUTIONS TO THE EXTRA-BUDGETARY PENSION

FUND OF CITIZENS (TRANSFERRED TO THE RELEVANT DEPARTMENTS

OF THE PEOPLE'S BANK);

- MANDATORY DEDUCTIONS TO STATE TRUST FUNDS

SINGLE SOCIAL PAYMENT.

4.

The tax on improvement and developmentof social infrastructure has been combined

with the profit tax. When paying this tax,

banks provide information to the state tax

inspectorates at the beginning of the next

quarter, predicting the amount of profit

received during the quarter in monthly

terms. The forecasted tax amount is

transferred to the appropriate account of the

state budget at the beginning of the month,

and in this case,

Debit 19931 - "Deferred taxes",

Credit 23402 - "Funds of the republican

budget" account.

5.

The amount of profit tax paid during the month is transferred to the appropriate5

expense account of the bank at the end of each quarter.

a). If the estimated amount of profit tax for the quarter corresponds to reality,

Debit 56902 – “Estimation of income tax”,

Credit –19931-“Deferred taxes” account.

b). If the amount of profit tax paid in advance for the quarter is less than the

actual amount of profit tax of the bank, the underpaid part is transferred to the

bank’s account 22502 and transferred from this account to the state budget.

- for the underpaid amount,

Debit 56902 – “Estimation of income tax”,

Credit 22502 – “Accrued income (profit) taxes” account.

- when the underpaid amount is transferred to the state budget account,

Debit 22502 – “Accrued income (profit) taxes”,

Credit 23402 – “Funds of the republican budget” account.

6.

Property tax calculation. Commercial banks pay property 6tax, like all legal entities, at present this tax rate is 5 percent

of the total amount of property (in accordance with the

Resolution of the President of the Republic of Uzbekistan

dated 29.12.2017 No. PP-3454, Appendix 17). The tax period

for property tax is a calendar year. When determining the

taxable base for property tax in banks, the balances on

accounts 16509+16535+16529+16541, 16549 are taken (there

is a tax exemption for terminals in the lease, recorded in

account 16549, and they are deducted from the tax base).

There is also an exemption for intangible assets reflected in

account 16601, and they are also not included in the tax base.

Banks submit advance reports to tax authorities for all

quarters of the year. The monthly property tax paid by the

bank is calculated and accumulated in account 22504, and the

following accounting entry is made:

7.

Debit 56714–“Taxes (except for income tax) andlicenses”,

Credit 22504 –“Accrued other taxes (on a separate

analytical account)” account.

At the end of the reporting period, the actually accrued

annual property tax is paid and a report on the amount of

tax paid is submitted by January 25. When property tax is

paid, the following accounting entry is made.

Debit 22504 –“Accrued other taxes (on a separate

analytical account)”

Credit 23402 –“Funds of the republican budget”

account.

After property tax is paid, a report on the amount of tax

paid is submitted by January 25.

7

8.

Land tax calculation. Legal entities that own land plotson the basis of property rights, ownership rights, right of

use or lease rights, including banks, are considered payers

of land tax (in accordance with the Resolution of the

President of the Republic of Uzbekistan No. PP-3454

dated 30.12.2019, Appendix 19). In the event that real

estate is leased by a bank, the lessor, that is, the bank, is

the payer of land tax. In the event that several legal entities

jointly use a land plot, each legal entity pays land tax for

its share of the used area of the land plot. Land tax is

calculated based on the situation as of January 1 of each

tax period, and the land tax calculation is submitted to the

state tax service body at the location of the land plot by

February 15 of the reporting year. Payment of land tax is

made by banks in equal installments every quarter of the

year, by the 15th day of the second month of the quarter.

8

9.

After the tax base is determined, the area of the territory where the bankbuildings are located is determined and the tax amount is determined based on

the established rates. The determined amount of land tax is paid to the relevant

accounts of the state budget in the established manner and within the

established periods. The amount of the calculated land tax is credited to the

account

Debit 56714 – “Taxes (except for income tax) and licenses”,

Credit 22504 – “Other taxes calculated (in a separate analytical account)”.

When the land tax is paid,

Debit 22504 – “Other taxes calculated (in a separate analytical account)”,

Credit 23402 – Funds of the republican budget”.

In the event of a change in the tax base during the tax period, banks shall

submit a revised calculation of the land tax to the state tax service body within

one month.

9

10.

For transactions subject to VAT, the amount of payment isdetermined at the end of each month, and then the payment is

made.

For example, a bank received 500 thousand soums in income from

renting a fixed asset (truck) to a client for 120 days. When VAT is

calculated on the income received in the following manner,

a). When the client transfers the rental payment for using the truck

to the bank,

Debit 20208-“Client's term deposit account”- 500 thousand

soums,

Credit 29802 –“Payments for goods and materials and services

provided” -500 thousand soums.

b). The VAT amount (83333.33 = 500000 / 120 x 20) was

calculated:

Debit 29802–“Payments for goods and services rendered” 83333.33 soums,

Credit 22504 –“Other accrued taxes” - 83333.33 soums.

10

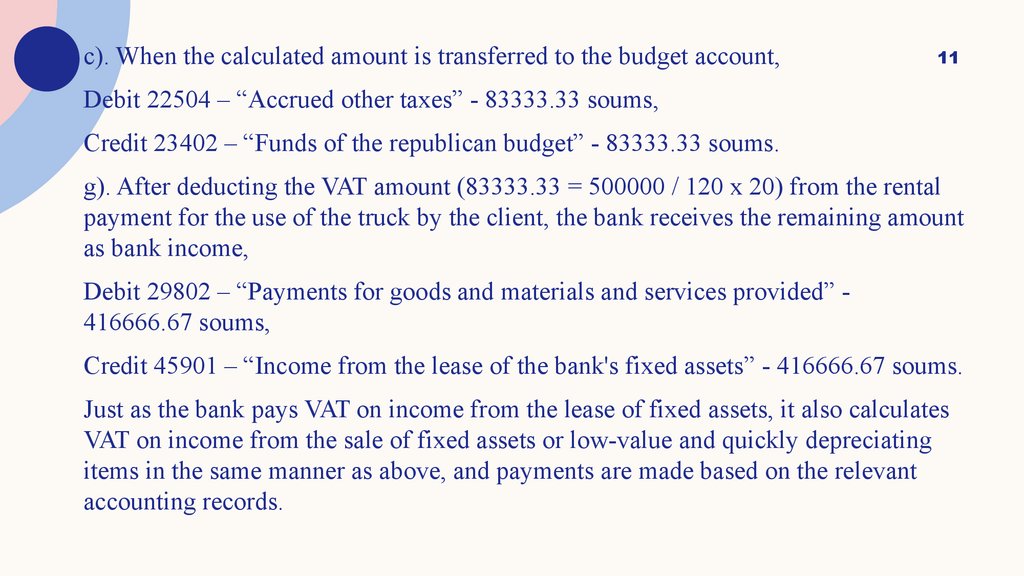

11.

c). When the calculated amount is transferred to the budget account,11

Debit 22504 – “Accrued other taxes” - 83333.33 soums,

Credit 23402 – “Funds of the republican budget” - 83333.33 soums.

g). After deducting the VAT amount (83333.33 = 500000 / 120 x 20) from the rental

payment for the use of the truck by the client, the bank receives the remaining amount

as bank income,

Debit 29802 – “Payments for goods and materials and services provided” 416666.67 soums,

Credit 45901 – “Income from the lease of the bank's fixed assets” - 416666.67 soums.

Just as the bank pays VAT on income from the lease of fixed assets, it also calculates

VAT on income from the sale of fixed assets or low-value and quickly depreciating

items in the same manner as above, and payments are made based on the relevant

accounting records.

12.

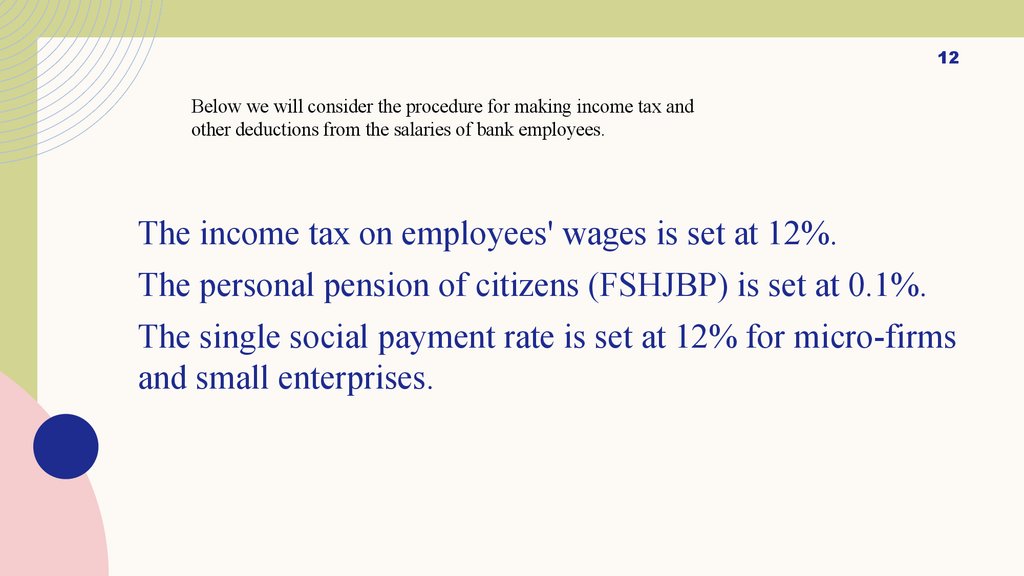

12Below we will consider the procedure for making income tax and

other deductions from the salaries of bank employees.

The income tax on employees' wages is set at 12%.

The personal pension of citizens (FSHJBP) is set at 0.1%.

The single social payment rate is set at 12% for micro-firms

and small enterprises.

13.

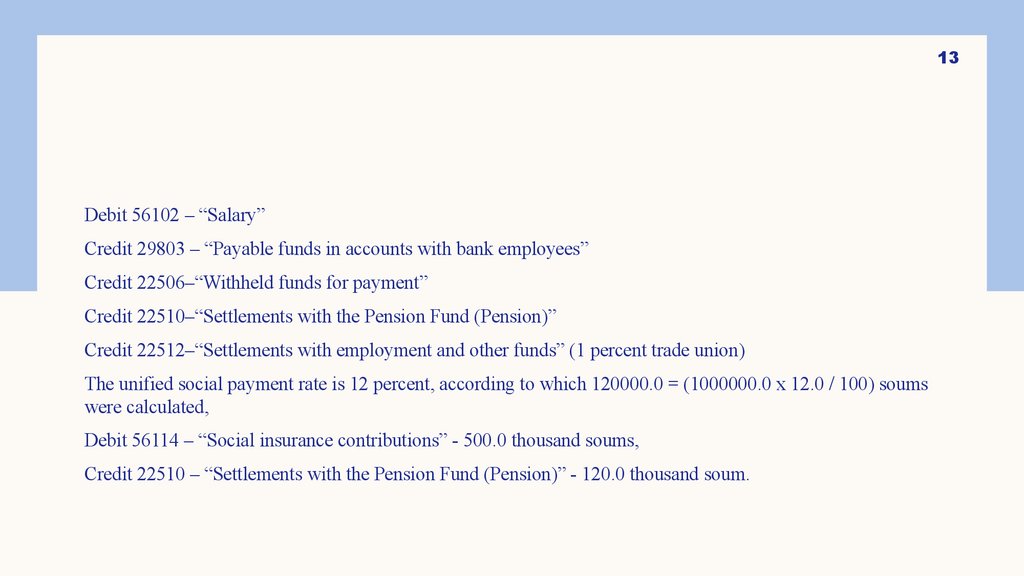

13Debit 56102 – “Salary”

Credit 29803 – “Payable funds in accounts with bank employees”

Credit 22506–“Withheld funds for payment”

Credit 22510–“Settlements with the Pension Fund (Pension)”

Credit 22512–“Settlements with employment and other funds” (1 percent trade union)

The unified social payment rate is 12 percent, according to which 120000.0 = (1000000.0 x 12.0 / 100) soums

were calculated,

Debit 56114 – “Social insurance contributions” - 500.0 thousand soums,

Credit 22510 – “Settlements with the Pension Fund (Pension)” - 120.0 thousand soum.

14. Спасибо

СПАСИБОМарта Артемьева

502-555-0152

brita@firstupconsultants.com

www.firstupconsultants.com