Похожие презентации:

")

Land_Tax_Presentation_Professional_EN_Uzbekistan

1.

Title• Land Tax in Uzbekistan

• Detailed & Professional Overview

2.

Plan• 1. Tax Period

• 2. Calculation & Reporting Rules

• 3. Payment Procedure

• 4. Special Regulations

• 5. Key Compliance Requirements

3.

Tax Period• • The land tax period is the calendar year.

• • Tax is calculated based on the situation as of

January 1.

• • Applies to both agricultural and nonagricultural land users.

4.

Tax Calculation Principles• • Taxpayers calculate the tax independently.

• • Calculation is based on:

• – Tax base determined under Article 427.

• – Land category and usage type.

• – Applicable tax rates approved annually.

• • Each legal entity is responsible for correct

calculation.

5.

Reporting Deadlines• • Non-agricultural land:

• – Report submitted by January 20.

• • Agricultural land:

• – Report submitted by May 1.

• • Reports must be submitted to the tax

authority of the land’s location.

6.

Changes in Tax Base• • If the land area or tax base changes during

the year:

• – Legal entities must submit an updated tax

report within 1 month.

• • Agricultural land changes:

• – Updated report due by December 1.

• • Ensures tax is aligned with actual land usage.

7.

Non-Taxable Land Notice• • Legal entities that own non-taxable land

must submit a special notice.

• • Deadline: January 20 of each tax year.

• • Notice submitted in an approved form

issued by the State Tax Committee.

8.

Multi-Storey Property Rule• • For non-residential premises in multi-storey

buildings:

• – Taxable land area = total land area ÷

number of floors.

• • Ensures fair distribution of land tax among

multiple property owners.

9.

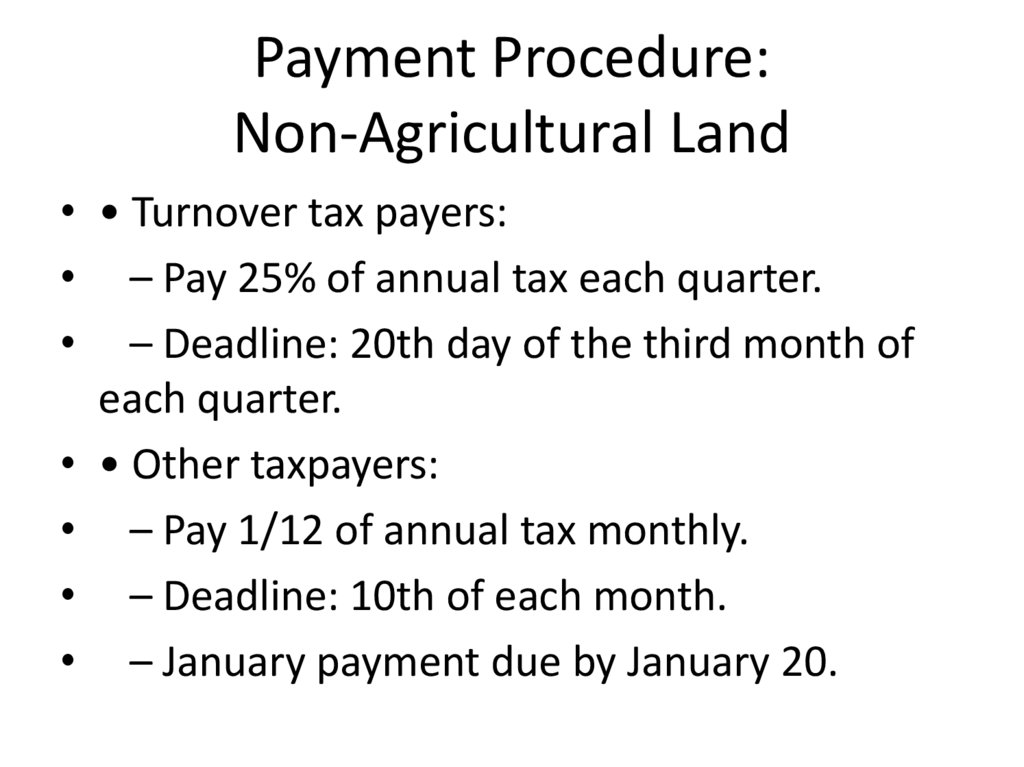

Payment Procedure:Non-Agricultural Land

• • Turnover tax payers:

• – Pay 25% of annual tax each quarter.

• – Deadline: 20th day of the third month of

each quarter.

• • Other taxpayers:

• – Pay 1/12 of annual tax monthly.

• – Deadline: 10th of each month.

• – January payment due by January 20.

10.

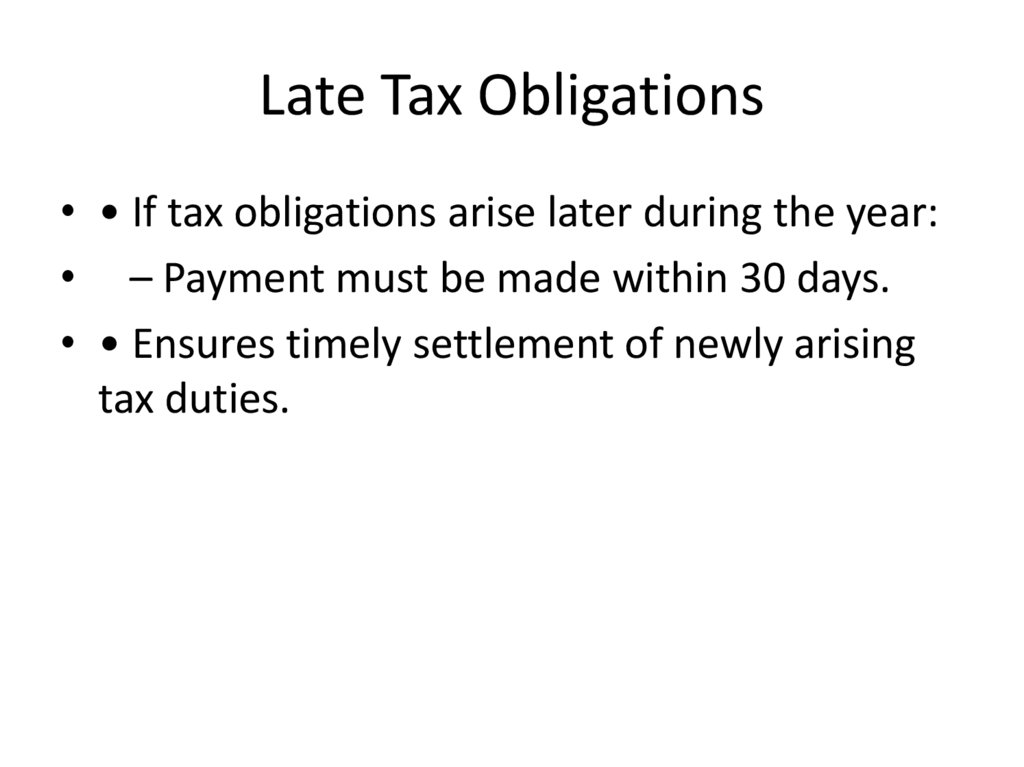

Late Tax Obligations• • If tax obligations arise later during the year:

• – Payment must be made within 30 days.

• • Ensures timely settlement of newly arising

tax duties.

11.

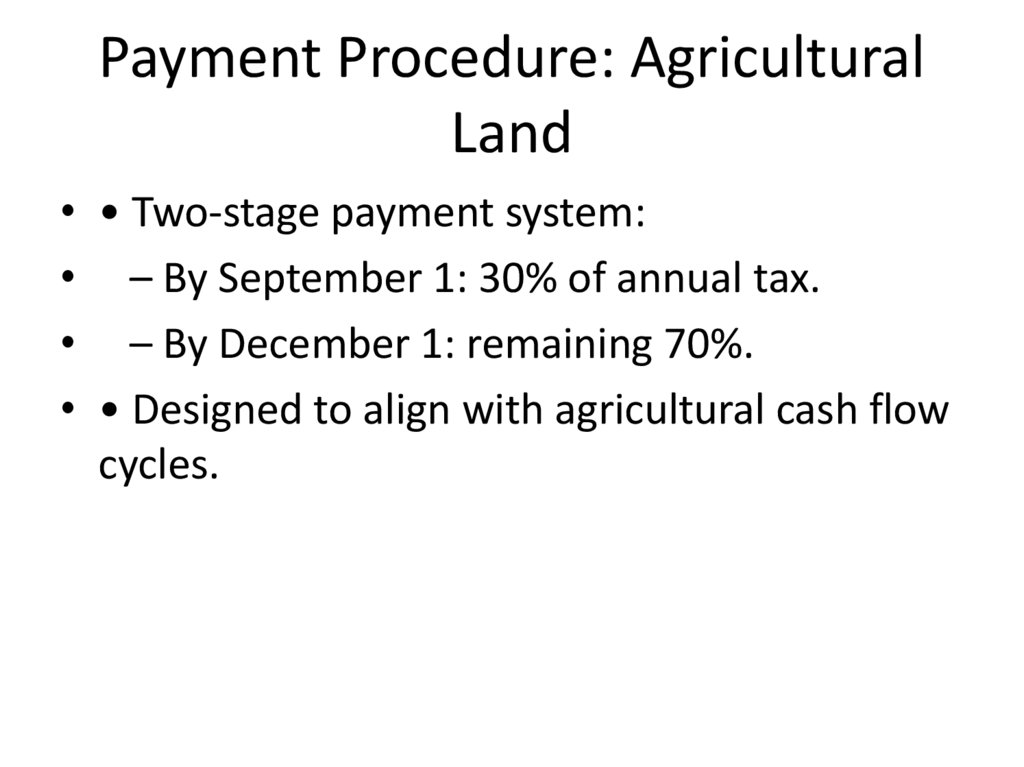

Payment Procedure: AgriculturalLand

• • Two-stage payment system:

• – By September 1: 30% of annual tax.

• – By December 1: remaining 70%.

• • Designed to align with agricultural cash flow

cycles.

12.

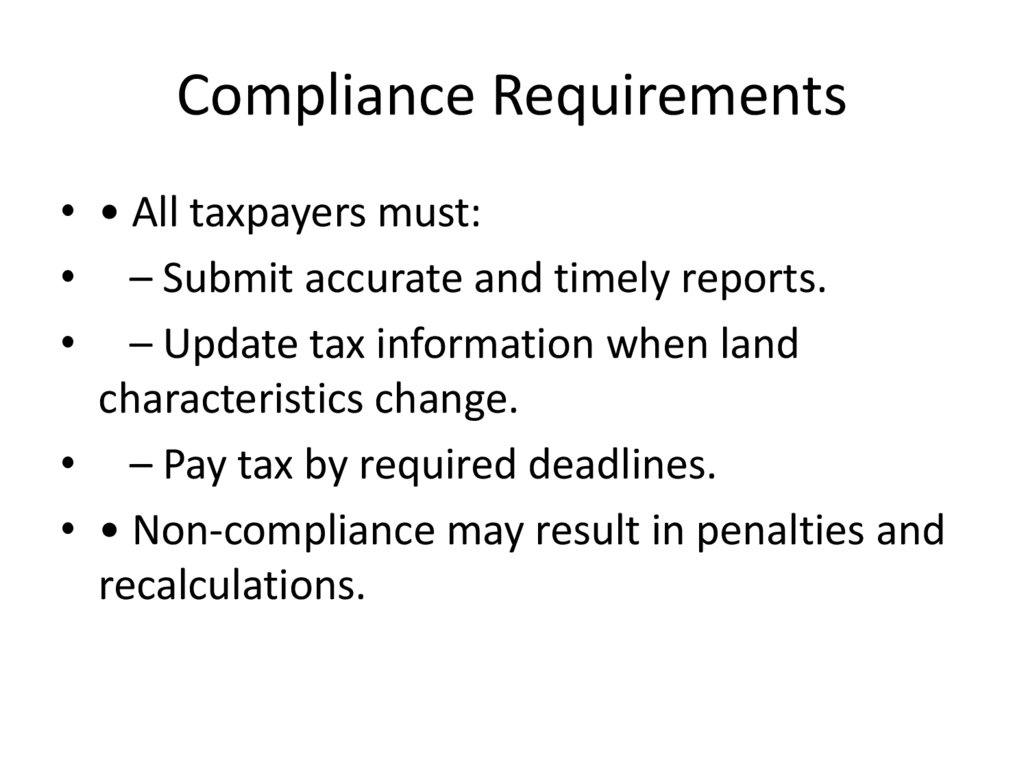

Compliance Requirements• • All taxpayers must:

• – Submit accurate and timely reports.

• – Update tax information when land

characteristics change.

• – Pay tax by required deadlines.

• • Non-compliance may result in penalties and

recalculations.

13.

Conclusion• • Land tax administration in Uzbekistan is

structured and deadline-driven.

• • Reporting and payment rules differ for

agricultural and non-agricultural land.

• • Accurate reporting ensures correct taxation

and avoids penalties.

• • Understanding the regulations helps legal

entities maintain full compliance.