")

Английский язык

Английский языкПохожие презентации:

")

Macroeconomic environment and perspectives in Colombia

1. Macroeconomic environment and perspectives in Colombia

Hernando José GómezMoscow, Oct 11 2016

2.

Table of contents1

International context

2

Where are we coming from – a long term view

3

Macroeconomic, fiscal situation, and perspectives

4

Colombia in the regional context

3.

International Context4.

The United States has consolidated its economic recovery…USA Annual Growth

5

4,1

3,8

4

3,4

2,8

3

2,5

2,7

2,4

2,2

2,4 2,4

2,5

1,8

2

1,8

% 1

1,6

1,5

0,9

0

-0,3

-1

-2

2017

2016

2015

2014

2013

2012

2011

2010

2008

2007

2006

2005

2004

2003

2002

2001

2000

Source: Bureau of Economic Analysis y WEO abril de 2016.

2009

-2,8

-3

5.

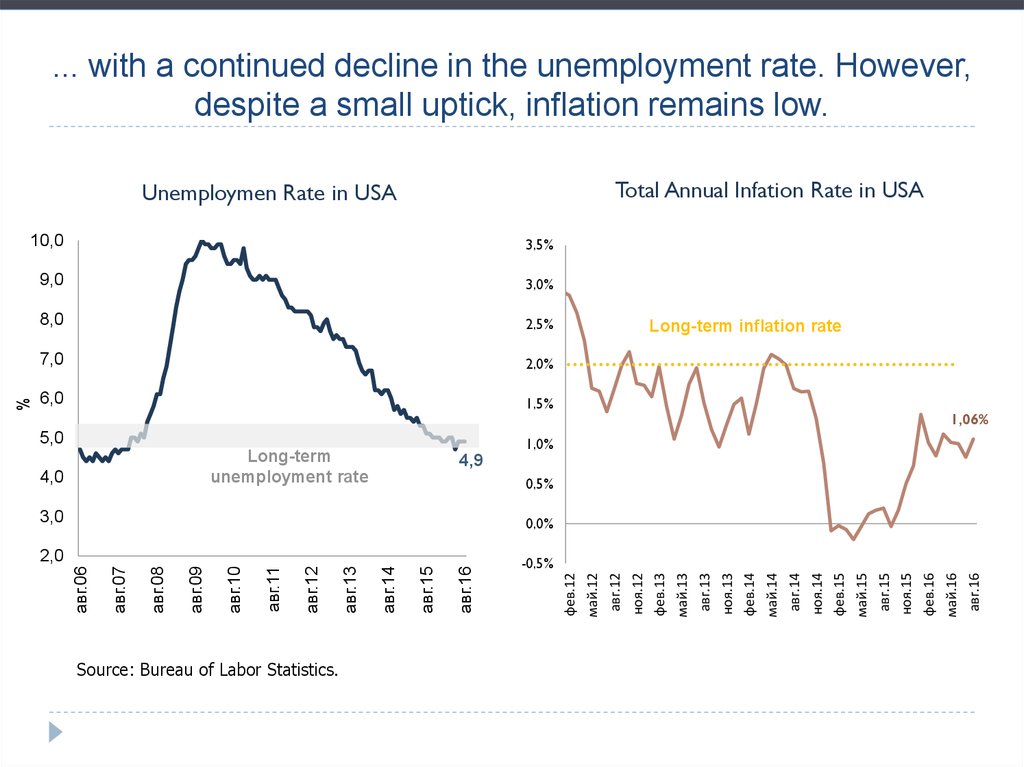

... with a continued decline in the unemployment rate. However,despite a small uptick, inflation remains low.

Total Annual Infation Rate in USA

Unemploymen Rate in USA

3,5%

9,0

3,0%

8,0

2,5%

7,0

2,0%

6,0

1,5%

5,0

4,9

0,5%

авг.16

авг.15

авг.14

авг.13

авг.12

авг.11

авг.10

-0,5%

авг.09

2,0

авг.08

0,0%

авг.07

3,0

Source: Bureau of Labor Statistics.

1,06%

фев.12

май.12

авг.12

ноя.12

фев.13

май.13

авг.13

ноя.13

фев.14

май.14

авг.14

ноя.14

фев.15

май.15

авг.15

ноя.15

фев.16

май.16

авг.16

4,0

Inflación deinflation

Long-term

largo plazo

rate

1,0%

Long-term

unemployment rate

авг.06

%

10,0

6.

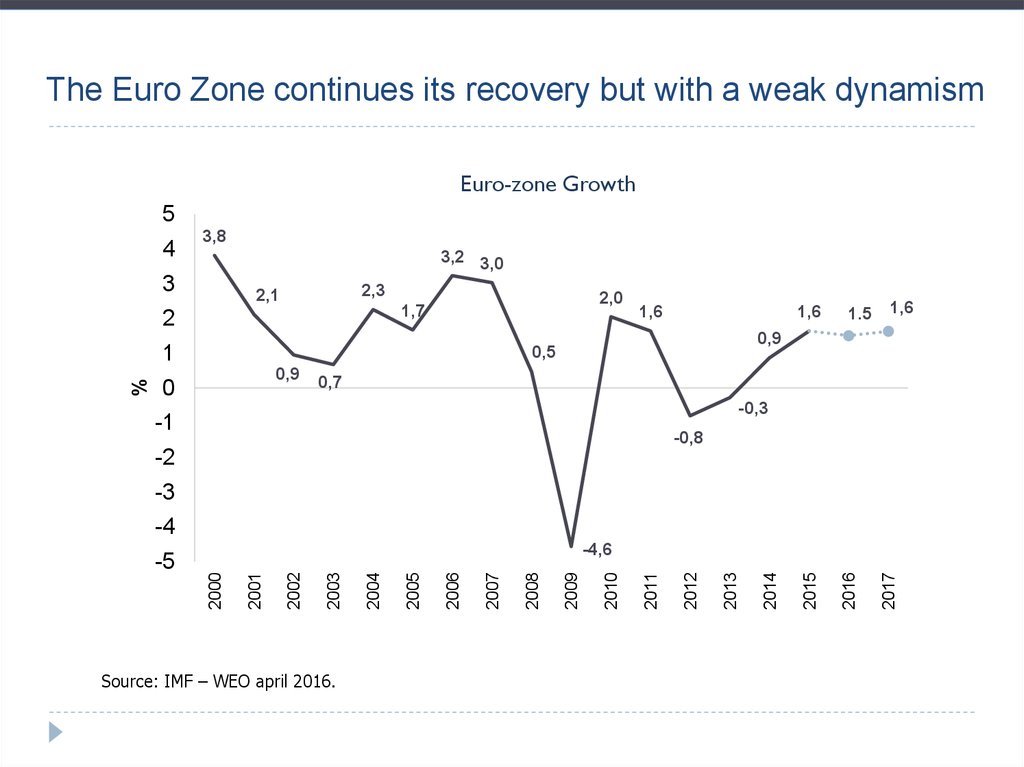

The Euro Zone continues its recovery but with a weak dynamismEuro-zone Growth

5

4

3,8

3,2 3,0

3

2,3

2,1

2,0

1,7

2

%

1

1,6

1,6

0,9

1,6

0,9

0,5

0

1.5

0,7

-0,3

-1

-0,8

-2

-3

-4

Source: IMF – WEO april 2016.

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

-4,6

2000

-5

7.

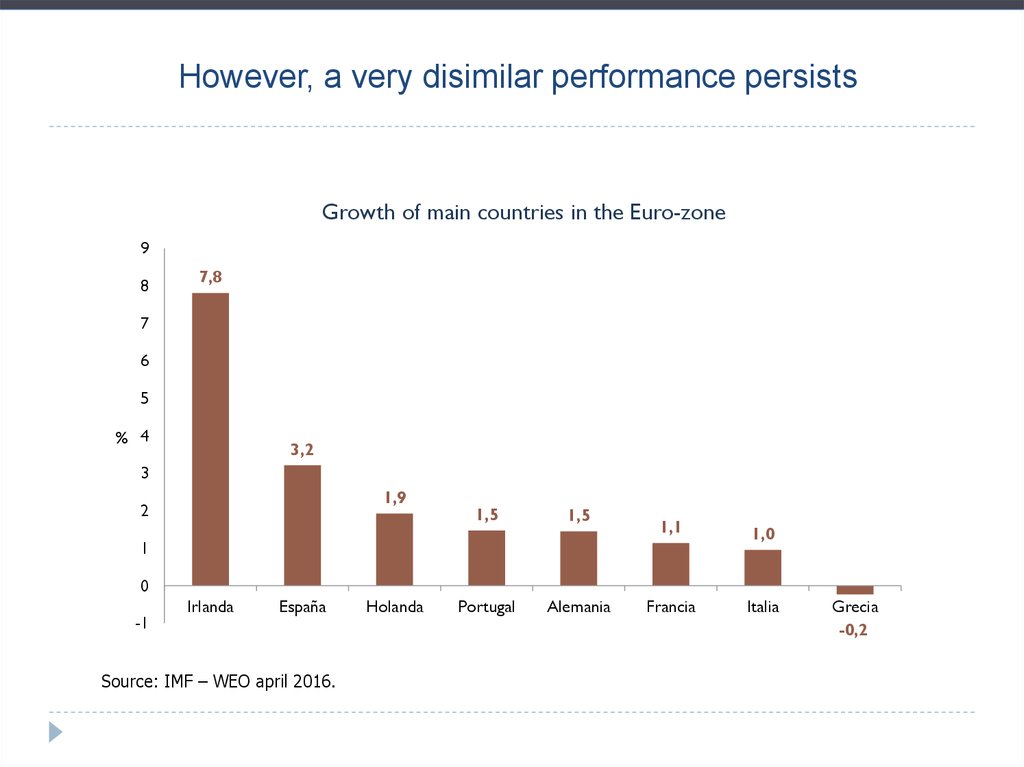

However, a very disimilar performance persistsGrowth of main countries in the Euro-zone

9

8

7,8

7

6

5

% 4

3,2

3

1,9

2

1,5

1,5

Portugal

Alemania

1,1

1,0

Francia

Italia

1

0

-1

Irlanda

España

Source: IMF – WEO april 2016.

Holanda

Grecia

-0,2

8. The measures taken by the ECB have reduced, but not eliminated, the risk of deflation

Annual Inflation on the Euro-zone2,5

2,0

1,5

0,5

0,4

0,2

0,0

-0,1

-0,1

-0,5

-1,0

Euro-zone

Germany

Source: European Central Bank. Official data.

France

Italy

Spain

авг.16

июн.16

апр.16

фев.16

дек.15

окт.15

авг.15

июн.15

апр.15

фев.15

дек.14

окт.14

авг.14

июн.14

апр.14

фев.14

дек.13

окт.13

авг.13

июн.13

-1,5

апр.13

%

1,0

9. As for the emerging world, the fall in commodity prices has been widespread but there has been a slight rebound

Commodities Price Index(Base = 100 Jun 2011)

110

Energy

100

90

Agriculture

80

Precious metals

70

60

Other minerals

50

40

Source: World Bank Commodity Price Data (Pink Sheet).

авг.16

июн.16

апр.16

фев.16

дек.15

окт.15

авг.15

июн.15

апр.15

фев.15

дек.14

окт.14

авг.14

июн.14

апр.14

фев.14

дек.13

окт.13

авг.13

июн.13

апр.13

фев.13

дек.12

окт.12

авг.12

июн.12

апр.12

30

10. ... with an increase in risk perception, despite an important declining from the peak of 506 to 358. In part thanks to the

recovery in developed economiesEmerging Markets Bonds Index –EMBI506,8

Jun-2014

500,0

Basis Points

450,0

400,0

350,0

358,6

300,0

Source: Bloomberg

сен.16

май.16

янв.16

сен.15

май.15

янв.15

сен.14

май.14

янв.14

сен.13

май.13

янв.13

сен.12

май.12

250,0

11. That in turn led to a depreciation of major currencies, with the Colombian peso and Brazilian real the most volatile

Exchange Rate Index (Base 100 = june 2014)180

Jun-2014

160

140

120

100

Source: Bloomberg.

Perú

sep.-16

jul.-16

mar.-16

ene.-16

nov.-15

sep.-15

jul.-15

Brasil

Brazil

may.-16

Chile

mar.-15

ene.-15

nov.-14

sep.-14

jul.-14

México

may.-15

Colombia

may.-14

mar.-14

ene.-14

nov.-13

sep.-13

jul.-13

may.-13

mar.-13

80

12.

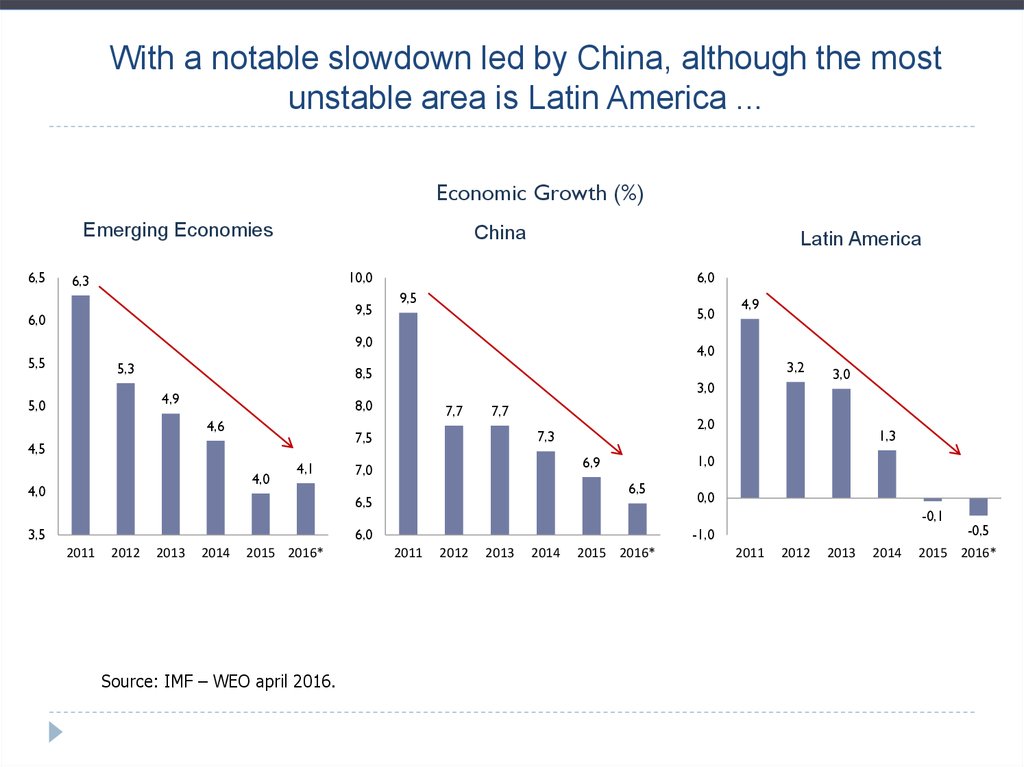

With a notable slowdown led by China, although the mostunstable area is Latin America ...

Economic Growth (%)

Emerging Economies

6,5

China

Latin America

10,0

6,3

9,5

6,0

6,0

9,5

5,0

9,0

5,5

5,3

4,0

3,2

8,5

4,9

5,0

3,0

8,0

4,6

4,0

4,0

7,7

7,7

4,1

6,5

6,5

3,5

2012

2013

2014

2015 2016*

Source: IMF – WEO april 2016.

0,0

-0,1

6,0

2011

1,3

1,0

6,9

7,0

3,0

2,0

7,3

7,5

4,5

4,9

-1,0

2011

2012

2013

2014

2015 2016*

2011

2012

2013

2014

-0,5

2015 2016*

13.

... Where the most affected countries were Venezuela, Brazil andEcuador ...

Economic Growth 2015 (%)

4

3,1

2,5

2,4

2,3

2,3

2

0,4

0

-0,6

%

-2

-3,0

-4

-6

-8

-10

-10,0

Source: FMI.

Venezuela

Brazil

Ecuador

Argentina

Chile

Mexico

Peru

Uruguay

Colombia

-12

14. A major change in growth leadership with India’s service economy in first place instead of China, will keep down the price of

raw materialsEconomic Growth on China and India

14

China

India

%

12

10

7,3

7,5

8

6,9

6

6,5

4

2005

2006

2007

2008

Source: World Bank and WEO

2009

2010

2011

2012

2013

2014

2015 2016*

15.

Where are we comingfrom? – A long term view

16. Colombia has transformed from a low to an upper middle income economy

GDP per capita(International Dollars, PPP)

16000

14000

Upper middle income

12000

USD PPP

10000

Lower middle income

8000

6000

4000

2000

Low Income

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

Source: IMF and World Bank

17. Inflation and unemployment rates have fallen from the two-digit levels from two decades ago

Annual Inflation35

Annual Unemployment Rate

25

32,4

30

20,1

20

25

15

%

%

20

15

10

9,1

9,1

8,4

10

6,8

5

5

Source: Colombian Central Bank. Banco de la República.

2014

2012

2010

2008

2006

2004

2002

2000

1998

1996

1994

1992

1990

1988

1986

1984

0

1982

1,9

1980

0

Source: Colombian National Institute of Statistics. DANE.

18. Security indicators have also drastically improved…

Murders per 100.000 peopleKidnappings

3572

75

69,8

56,2

55

% 45

35,0

32,7

27,8

35

25

Número de personas

65

3500

2500

2000

1500

1000

305

500

288

Source: Colombian Defense Ministry.

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2000

2014

20000

18000

16000

14000

12000

10000

8000

6000

4000

2000

0

17176

15358

16311

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

10972

9128

2002

2013

2012

571

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

471

764

Número de robos

894

2000

2013

2012

2011

2010

2008

2007

2006

2009

Commercial robberies

Terrorist acts

2014

1645

2005

2004

2003

2002

2001

1800

1600

1400

1200

1000

800

600

400

200

0

2001

0

15

Número de ataques

2882

3000

19. …As the levels of poverty and extreme poverty

Monetary Poverty65

Extreme Monetary Poverty

35

61,7

60

33,1

30

55

%

45

20

45,5

40,3

40

18

17,7

%

50

25

49,7

15

12,2

35

10

Total

30

27,8

Urban

25

7,9

Rural

Urban

24,1

20

4,9

Total

5

Rural

Source: Colombian National Institute of Statistics. DANE.

2015

2014

2013

2012

2011

2010

2009

2008

2005

2004

2003

2002

2015

2014

2013

2012

2011

2010

2009

2008

2005

2004

2003

2002

0

20. Inequality, meanwhile, has remained relatively constant

Inequality0,58

0,572

0,567

0,56

0,54

0,542

0,55

0,522

0,52

0,518

0,5

0,489

0,498

0,48

0,46

0,454

Total

0,44

Municipalities

Remainder

Source: Colombian National Institute of Statistics. DANE.

2015

2014

2013

2012

2011

2010

2009

2008

2005

2004

2003

2002

0,42

21. Currently, debt is mainly in local currency, which reduces the external exposure of the country

National Central Government Debt CompositionInternal Debt

External Debt

100%

90%

39%

80%

70%

60%

87%

50%

40%

61%

30%

20%

10%

13%

Source: Colombian Treasury Ministry. MHCP

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

0%

22. The Colombian economy has gone from being purely rural, specializing in coffee, to a service oriented one, albeit strongly

influenced by the energy sectorProductive Structure

30

25

Agri

Agro

Mining

Minas

Industry

Industria

Financial

Serviciosservices

Financieros

25,1

20,7

19,9

20

19,3

19,2

%

16,2

13,8

15

12,8

11,2

11,1

9,3

10

8,4

6,2 6,8

6,5

5

2,0

0

1970

1990

Source: Colombian National Institute of Statistics. DANE.

2010

2015

23. While the amount of exports have grown substantially, it has remained relatively stable as share of GDP

Exports and Imports (% GDP)20

Exports

Exportaciones

18

Imports

Importaciones

16

%

14

12

10

8

Source: Colombian National Planning Department. -DNP

2014

2012

2010

2008

2006

2004

2002

2000

1998

1996

1994

1992

1990

1988

1986

1984

1982

1980

1978

1976

1974

6

24. Exports are still concentrated in traditional products. The top product was coffee in the 70s and is oil today.

Export’s Composition50

70

63,9

60,0

60

50

Traditional exports as share of total exports

45

61,0

41,6

39,9

40

52,2

47,8

35

40,0

40

43,9

%

%

36,1

30

28,8

30

39,0

25

20,9

20

15,1

15

20

10

10

8,1

8,0

4,7

5

0

0

1974

1990

Tradicionales

Traditional

2010

No

Nontradicionales

Traditional

2015

Source: Colombian National Planning Department. -DNP

0,2

1974

Petróleo

Oil

2,2

1990

Café

Coffee

2010

Carbón

Coal

12,8

7,1

2,4

1,2

2015

Ferroníquel

Ferronickel

25. Most imports are still intermediate goods, although consumer goods have gained ground

Import’s Composition70

Consumption

goods

Bienes de Consumo

Intermed.

goods

Bienes

Intermedios

Capitaldegoods

Bienes

Capital

Notclasificados

classified

No

58,3

60

53,1

50

43,1

42,3

40

%

36,1

35,4

34,4

29,8

30

22,4

22,2

20

11,8

9,8

10

1,0

0,2

0

1974

Source: Colombian National Planning Department. -DNP

1990

0,1

2010

0,0

2015

26.

Macroeconomic, fiscalcontext, and perspectives

27.

Macroeconomic and fiscalcontext

Perspectives

28.

Macroeconomic and fiscalcontext

Perspectives

29.

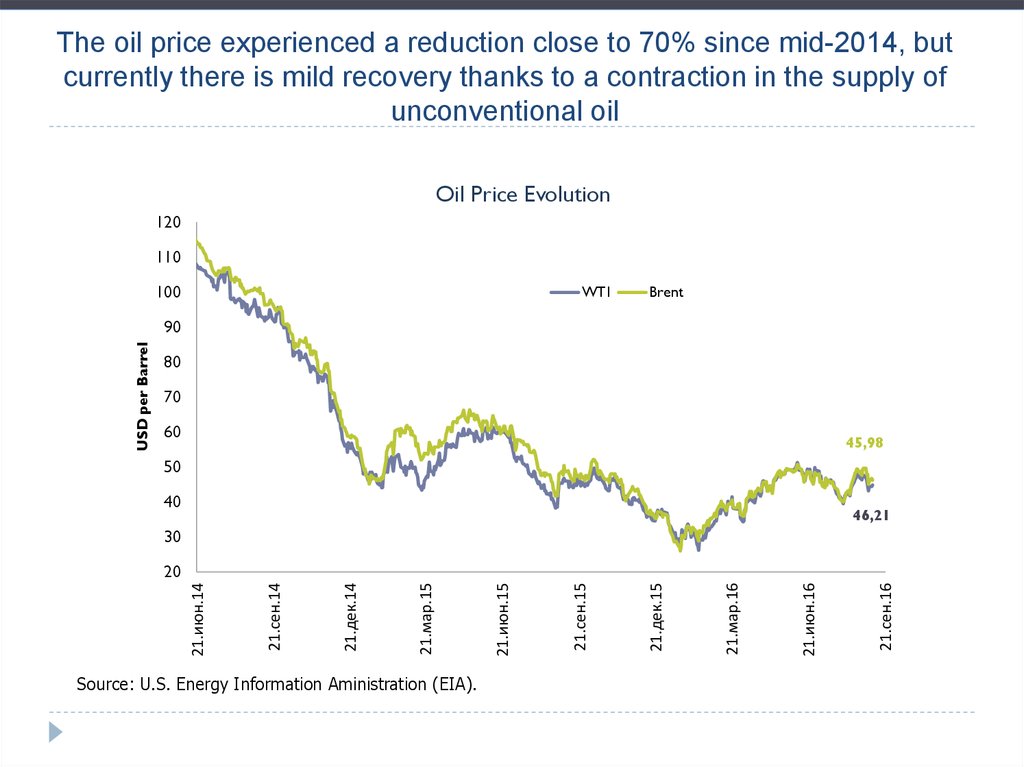

The oil price experienced a reduction close to 70% since mid-2014, butcurrently there is mild recovery thanks to a contraction in the supply of

unconventional oil

Oil Price Evolution

120

110

100

WTI

Brent

USD per Barrel

90

80

70

60

45,98

50

40

46,21

30

Source: U.S. Energy Information Aministration (EIA).

21.сен.16

21.июн.16

21.мар.16

21.дек.15

21.сен.15

21.июн.15

21.мар.15

21.дек.14

21.сен.14

21.июн.14

20

30. This has had an impact on the risk perception of Colombia ...

Emerging Markets Bonds Index –EMBI- Colombia400

Jun-14

350

Basis Points

300

250

234,1

200

150

100

Source: Bloomberg.

сен.16

май.16

янв.16

сен.15

май.15

янв.15

сен.14

май.14

янв.14

сен.13

май.13

янв.13

сен.12

май.12

янв.12

сен.11

май.11

50

31. And on the sharp depreciation of the peso, reaching historical values and strongly rising currency volatility, but gaining

And on the sharp depreciation of the peso, reaching historicalvalues and strongly rising currency volatility, but gaining value

this year

Nominal Exchange Rate (COP/USD)

$ 3 400

Colombian Pesos per US Dollar

$ 3 200

$ 2.976,16

$ 3 000

$ 2 800

$ 2 600

$ 2 400

$ 2 200

$ 2 000

Source: Colombian Central Bank. Banco de la República.

сен.16

июл.16

май.16

мар.16

янв.16

ноя.15

сен.15

июл.15

май.15

мар.15

янв.15

ноя.14

сен.14

июл.14

май.14

мар.14

янв.14

ноя.13

сен.13

июл.13

$ 1 800

32. Which has fueled an acceleration of inflation thru tradable goods in the economy

Total annual inflation and by group of expense8,97%

9%

8%

Total

7%

Transables

Tradeables

7,87%

Non

Tradeables

No

Transables

6%

5,01%

5%

4%

3%

2%

1%

Source: Colombian National Institute of Statistics. DANE.

авг.16

май.16

фев.16

ноя.15

авг.15

май.15

фев.15

ноя.14

авг.14

май.14

фев.14

ноя.13

авг.13

май.13

фев.13

ноя.12

авг.12

май.12

0%

33. ... El Niño caused an increase on food inflation and pushed general inflation to levels above the target range (2-4%)

Total annual inflation and by group of expense16%

14%

Total

Sin

Alimentos

Without

food

12%

13,06%

Alimentos

Food

10%

8%

8,10%

6%

6,10%

4%

2%

Source: Colombian National Institute of Statistics. DANE.

авг.16

май.16

фев.16

ноя.15

авг.15

май.15

фев.15

ноя.14

авг.14

май.14

фев.14

ноя.13

авг.13

май.13

фев.13

ноя.12

авг.12

май.12

0%

34. Motivating contractionary monetary policy response in order to anchor expectations

фев.12апр.12

июн.12

авг.12

окт.12

дек.12

фев.13

апр.13

июн.13

авг.13

окт.13

дек.13

фев.14

апр.14

июн.14

авг.14

окт.14

дек.14

фев.15

апр.15

июн.15

авг.15

окт.15

дек.15

фев.16

апр.16

июн.16

авг.16

Motivating contractionary monetary policy response in order to

anchor expectations

9

8

Jun 2014

Source: Colombian National Institute of Statistics. DANE.

7,75

7

6

5

%

4

3

2

1

0

35. The oil and monetary shock had an impact on all sectors of the economy

Supply-side annual growth (%)2,0

2,7

PIB

GDP

6,4

2,3

2,4

Social sociales

Services

Servicios

2016-II

4,6

4,8

Servicios

Financieros

Financial

Services

0,1

Transport

Transporte

2,5

1,0

Construction

Construcción

-0,8

Electricidad,

gas ywater

agua

Electricity,

gas and

Industria

Industry

4,5

3,9

6,0

5,2

-7,1

0,3

-0,1

Agro

Agricultural

-10

-5

5,9

14,5

-1,9

Mining

Minas

2014-II

6,1

3,2

2,3

2015-II

5,3

1,4

Comercio

Commerce

8,2

4,2

2,2

0

Source: Colombian National Institute of Statistics. DANE.

5,7

5

%

10

15

20

36. On the demand side, investment has slowed down to negative levels of growth for the second quarter of 2016, while domestic

demand continues to decreaseDemand-side annual growth (%)

EX

Exports

3,6

1,2

0,7

1,2

-11,5

Imports

IM

3,9

1,3

3,3

Final Internal

Demanda

FinalDemand

Interna

-2,3

Investment

Inversión

6,3

1,3

2,0

2,3

Goverment

Gobierno

16,0

5,2

2,7

3,8

3,6

Households

Hogares

2016-II

2015-II

2,53,7

3,9

Total

Consumption

Consumo

Total

2,0

GDP

PIB

-15

-10

-5

Source: Colombian National Institute of Statistics. DANE.

0

3,14,0

5

%

2014-II

10

15

20

37.

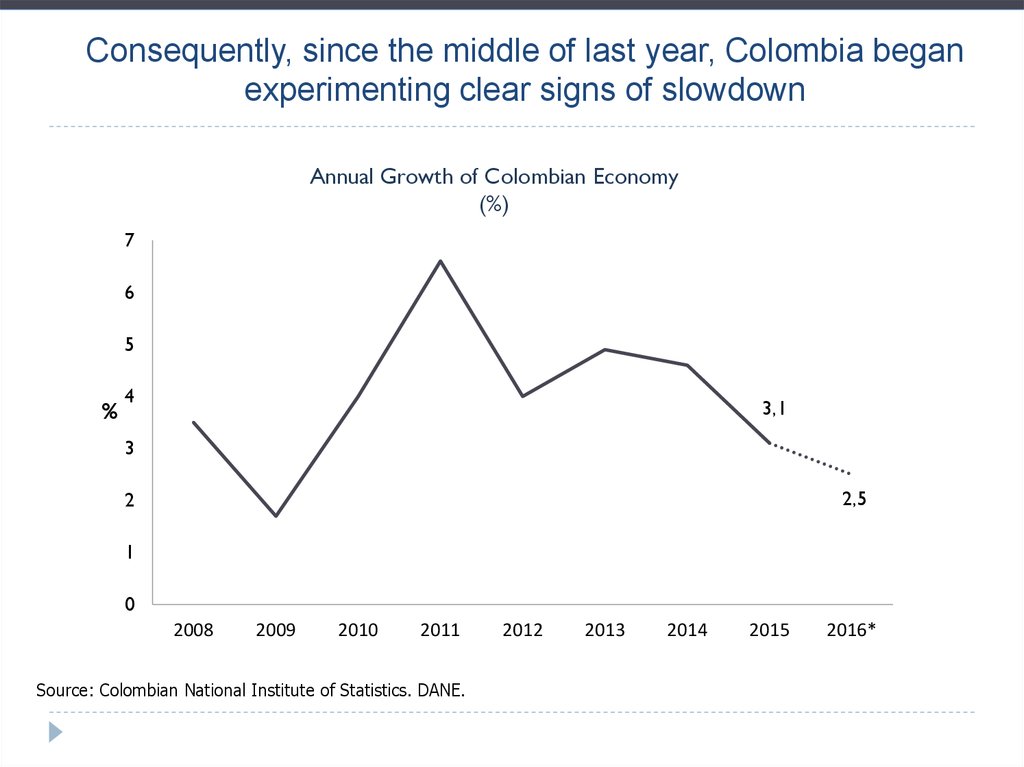

Consequently, since the middle of last year, Colombia beganexperimenting clear signs of slowdown

Annual Growth of Colombian Economy

(%)

7

6

5

%

4

3,1

3

2,5

2

1

0

2008

2009

2010

2011

Source: Colombian National Institute of Statistics. DANE.

2012

2013

2014

2015

2016*

38.

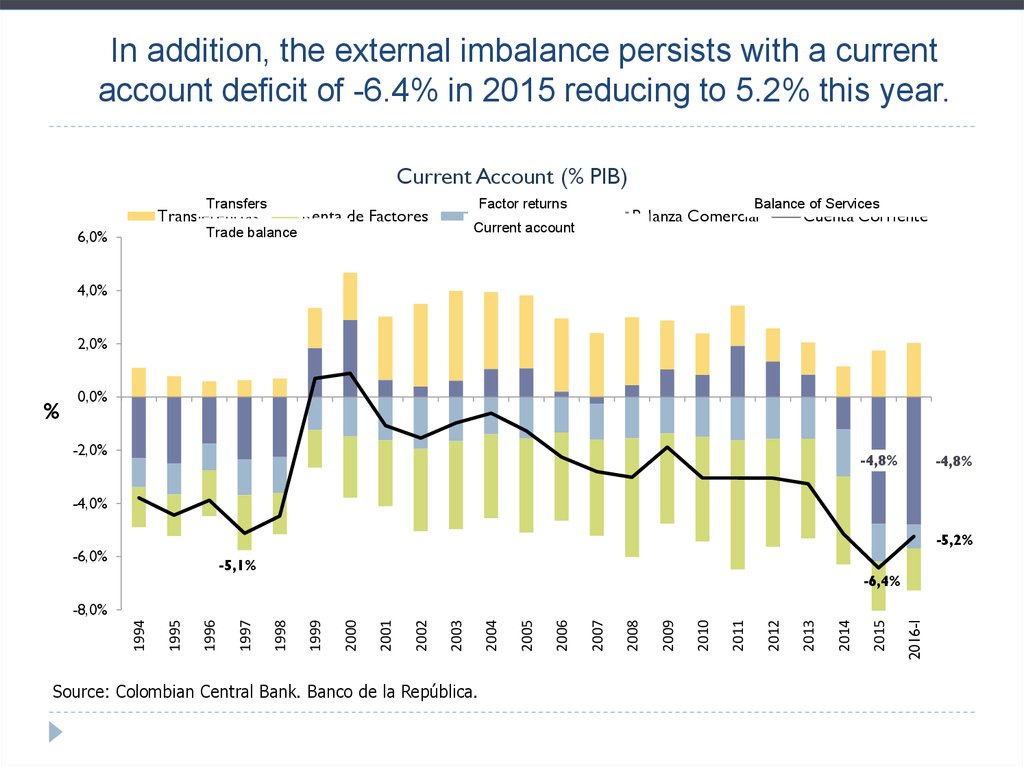

In addition, the external imbalance persists with a currentaccount deficit of -6.4% in 2015 reducing to 5.2% this year.

Current Account (% PIB)

Transfers

Transferencias

Factor returns

Renta de Factores

Balanza Comercial

Current account

Trade balance

6,0%

Balance of Services

Balanza Servicios

Cuenta Corriente

4,0%

2,0%

%

0,0%

-2,0%

-4,8%

-4,8%

-4,0%

-5,2%

-6,0%

-5,1%

-6,4%

Source: Colombian Central Bank. Banco de la República.

2016-I

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

-8,0%

39. In part due to the marked deterioration in the trade balance

Trade Balance, monthly exports and imports (12 months cumulative)65

USD Billions

55

-3

50

45

-8

40

35

Balanza

der.)

Tradecomercial

balance (eje

(right)

Exportaciones

Exports

-13

Importaciones

Imports

30

Source: Colombian National Institute of Statistics. DANE.

июл.16

май.16

мар.16

янв.16

ноя.15

сен.15

июл.15

май.15

мар.15

янв.15

ноя.14

сен.14

июл.14

май.14

мар.14

янв.14

ноя.13

сен.13

июл.13

май.13

мар.13

-18

янв.13

25

USD Billions

2

60

40.

But unlike 1999, the CA has been financed properly, preventing furtherinternal adjustment. However, It’s cause of concern that part of the funding

comes from short-term capital flows

Capital Account (% PIB)

10,0%

Net Foreign

Crédito

ExternoCredit

Neto

Inversión

de Portafolio

Neta

Net Portfolio

Investment

Net Foreign

Direct

Investment

Inversión

Extranjera

Directa

Neta

Cuenta

Capitales

Capitaldeaccount

8,0%

2,8%

1,5%

6,0%

5,2%

%

3,3%

4,0%

5,6%

4,2%

2,0%

2,6%

0,0%

-2,0%

Source: Colombian Central Bank. Banco de la República.

2016-I

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

-4,0%

41. The country's external debt has risen sharply to over 40% of GDP due to the depreciation of the peso

The country's external debt has risen sharply to over 40% ofGDP due to the depreciation of the peso

Debt as a share of the GDP (%)

50

Saldo

/ PIB

Total Total

debt/GDP

Public

Saldodebt/GDP

Pública/PIB

Private

debt/GDP

Saldo Privada

/PIB

37,9

%

40

30

23,0

20

10

42,2

22,5

15,9

22,5

13,8

8,8

7,1

21,3

12,6

9,9

12,5

8,8

2011

2012

24,2

26,8

13,7

10,5

22,7

15,8

15,2

25,3

16,9

11,0

0

2009

2010

* Projected to 2016 using debt data until March.

Source: Colombian Central Bank. Banco de la República.

2013

2014

2015

2016

*

42. While capital inflows of portfolio increase fiscal vulnerability due to the high percentage of bond holdings in foreign hands

Share of foreign funds as holders of TES25

22,4

20

%

15

10

6,4

5

Source: Colombian Treasury Ministry. MHCP

авг.16

июн.16

апр.16

фев.16

дек.15

окт.15

авг.15

июн.15

апр.15

фев.15

дек.14

окт.14

авг.14

июн.14

апр.14

фев.14

0

43. On the fiscal front, revenues have fallen substantially pushing the government deficit to an estimated 3.9% in 2016, setting up

ascenario of twin deficits

Revenue, Expenditure and Fiscal Deficit (% GDP)

2010

2011

2012

2013

2014

2015

2016*

25,0

0,0

-0,5

20,0

-1,0

-1,5

15,0

-2,0

-2,0

-1,8

-2,2

-2,5

-2,4

10,0

-3,0

Déficit

fiscal

(eje der.)

Fiscal

Deficit

(right)

5,0

-3,4

Expenditure

Source: Colombian Treasury Ministry. MHCP

-3,5

Ingresos

Revenue

Gastos

0,0

-3,0

-3,9

-4,0

-4,5

44. While experts have said that the fiscal needs for 2020 are of about 3.3% of GDP

Fiscal requirements(% GDP)

3,5

3,3

% GDP

3,0

2,8

2,5

2,0

1,5

1,5

1

1,0

0,5

0,3

0

0,0

2014

2015

2016

Source :Tax Experts Report and OCDE.

2017

2018

2019

2020

45. According to the government, the structural imbalance for 2016 will be approximately 2.1%, and the oil imbalance of the order

of 1.8%Total revenue

Tax

Oil

Non Tax

Special Funds

Capital Resources

Ecopetrol

Total Expenditure

Interests

Operating costs

Investment

Total Balance

Ciclical Balance

Structural Balance

2015*

16,1

14,5

0,7

0,1

0,2

1,3

0,5

19,2

2,6

13,5

3,1

-3

-0,8

-2,2

Source: Colombian Treasury Ministry. MHCP

2016*

15,0

14,2

0

0,1

0,2

0,5

0,1

19,0

3,2

13,8

1,9

-3,9

-1,8

-2,1

• But the government seems

to be overestimating the

growth of the economy.

• And the non-oil tax

revenues.

• Moreover, it is not doing all

the necessary budget cuts.

• So the structural

imbalance could be of

around 2.5% of the GDP.

46. Tax revenue in the country is low when compared with other countries in the region and the OECD. There is a high tax burden on

businesses.Fiscal Revenue in Colombia, LATAM and

OECD (%GDP, 2013)

Fiscal Revenue (% GDP)

60

Empresas

Business

Personas

People

42

40

80%

40%

% GDP

60%

30

17%

75%

80%

83%

12%

36%

55%

70%

3535

25%

20%

Colombia

90%

Chile

50

Perú

Peru

100%

72%

50%

20

20

17

14

10%

0

88%

45%

20%

10

60%

64%

Latina

América

LATAM

30%

Argentina

40%

28%

Source: OECD (2014) and ECLAC (2013)

Source: OECD.

Brasil

Brazil

Mexico

México

OECD

Finalandia

Finland

Grancia

France

Secia

Sweden

Italia

Italy

Grecia

Greece

Eslovenia

Slovenia

Portugal

Portugal

Brasil

Brazil

Slovakia

Eslovaquia

Estonia

Estonia

England

Inglaterra

Israel

Israel

Argentina

Argentina

Irlanda

Ireland

Korea

South del

Sur

Corea

México

Mexico

Colombia

Colombia

0%

47.

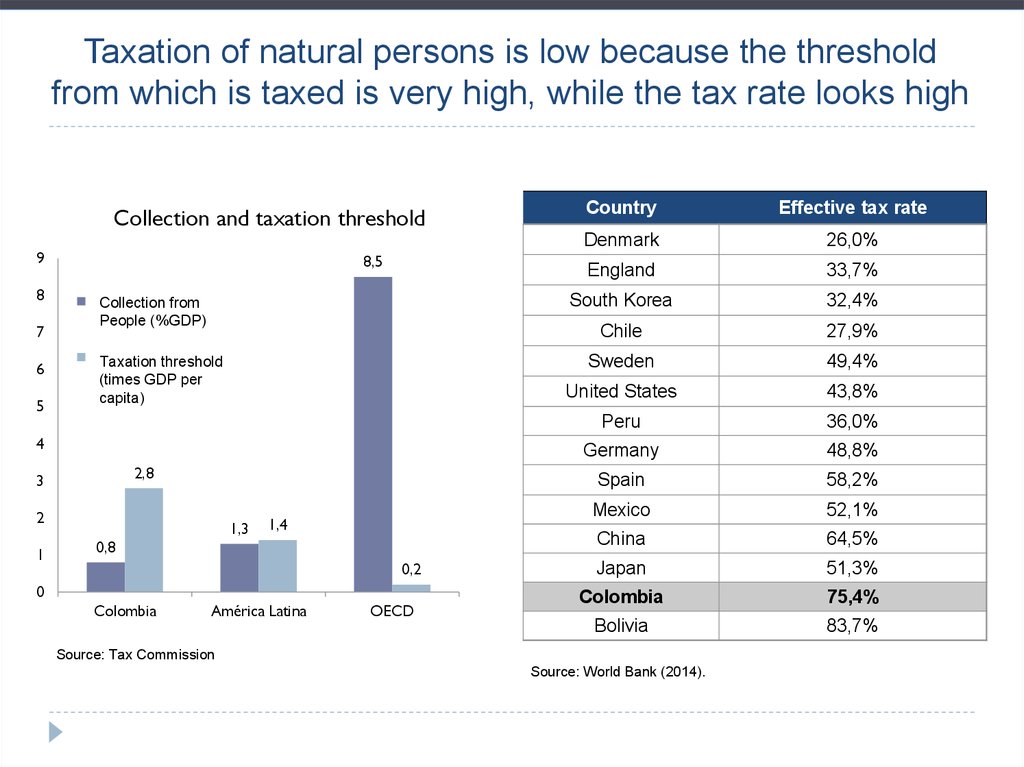

Taxation of natural persons is low because the thresholdfrom which is taxed is very high, while the tax rate looks high

Collection and taxation threshold

9

8

7

6

5

8,5

Recaudo

personas

Collection

from

(%People

PIB) (%GDP)

Umbral

pago

renta

Taxation

threshold

(veces

PIB

per

(times GDP per

cápita)

capita)

4

2,8

3

2

1

1,3

1,4

0,8

0,2

0

Colombia

América Latina

OECD

Country

Effective tax rate

Denmark

26,0%

England

33,7%

South Korea

32,4%

Chile

27,9%

Sweden

49,4%

United States

43,8%

Peru

36,0%

Germany

48,8%

Spain

58,2%

Mexico

52,1%

China

64,5%

Japan

51,3%

Colombia

75,4%

Bolivia

83,7%

Source: Tax Commission

Source: World Bank (2014).

48.

Macroeconomic and fiscalsituation

Perspectives

49. The slowdown is deepening, with the exception of the industrial sector

июл.16-8

апр.16

-6

окт.15

-4

янв.16

-2

июл.15

1,4

апр.15

% 0

янв.15

2

окт.14

4

июл.14

6

7

6

5

4

3

% 2

1

0

-1

-2

-3

апр.14

Industrial production

янв.14

-8,66

окт.13

июл.16

апр.16

янв.16

окт.15

июл.15

апр.15

янв.15

окт.14

июл.14

апр.14

янв.14

окт.13

-10

июл.13

% 6

4

апр.13

5

июл.13

8

апр.13

10

янв.13

10

янв.13

15

окт.12

12

окт.12

-5

июл.12

0

20

июл.12

-15

июл.16

апр.16

Cement shipments

апр.12

Source: Colombian National Institute of Statistics. DANE.

янв.16

окт.15

июл.15

апр.15

янв.15

окт.14

июл.14

апр.14

янв.14

окт.13

25

июл.13

8

апр.13

янв.13

окт.12

июл.12

июл.11

окт.11

янв.12

апр.12

июл.12

окт.12

янв.13

апр.13

июл.13

окт.13

янв.14

апр.14

июл.14

окт.14

янв.15

апр.15

июл.15

окт.15

янв.16

апр.16

июл.16

%

апр.12

янв.12

The slowdown is deepening, with the exception of the

industrial sector

14

Retail

2

0

-2

-1,3

Energy demand

-1,0

50. The economy faces high levels of industrial confidence paired with historical low levels of consumer confidence

Consumer Confidence IndexIndustrial Confidence Index

13

37

27

8

17

3

3,70

ICI

7

-2

Source: Fedesarrollo.

-7

июн.16

мар.16

дек.15

сен.15

июн.15

мар.15

дек.14

сен.14

июн.14

мар.14

дек.13

сен.13

июн.13

мар.13

-12

дек.12

янв.16

июл.15

янв.15

июл.14

янв.14

июл.13

янв.13

июл.12

янв.12

июл.11

янв.11

июл.10

янв.10

июл.09

янв.09

июл.08

-23

июл.16

-14,9

сен.12

-13

июн.12

-3

51.

During 2016 the country will experience the worst economicgrowth since the financial crisis. By 2017 a slight rebound is

expected.

Real anual GDP growth (%)

7

6

5

4

3,1

2,9

3

2,5

2

1

0

2008

2009

2010

2011

Source: Colombian National Institute of Statistics. DANE.

2012

2013

2014

2015

2016* 2017*

52.

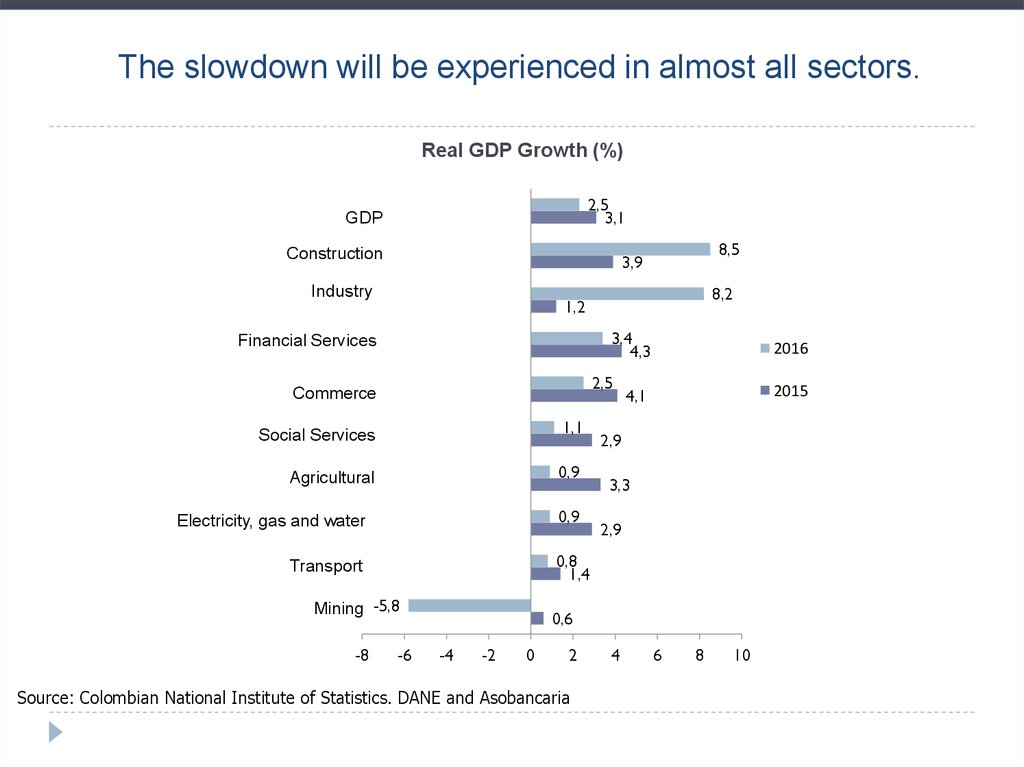

The slowdown will be experienced in almost all sectors.Real GDP Growth (%)

2,5

3,1

PIBGDP

Construction

Contrucción

Industry

Industria

8,2

1,2

3,4

4,3

Financial

Services

Servicios

Financieros

2,5

Comercio

Commerce

Servicios

Sociales

Social

Services

1,1

Agricultural

Agro

0,9

0,9

Electricity,

gasagua

andy water

Electricidad,

gas

2016

2015

4,1

2,9

3,3

2,9

0,8

1,4

Transport

Transporte

Mining -5,8

Minas

-8

8,5

3,9

-6

0,6

-4

-2

0

2

Source: Colombian National Institute of Statistics. DANE and Asobancaria

4

6

8

10

53.

Colombia in the regionalcontext

54.

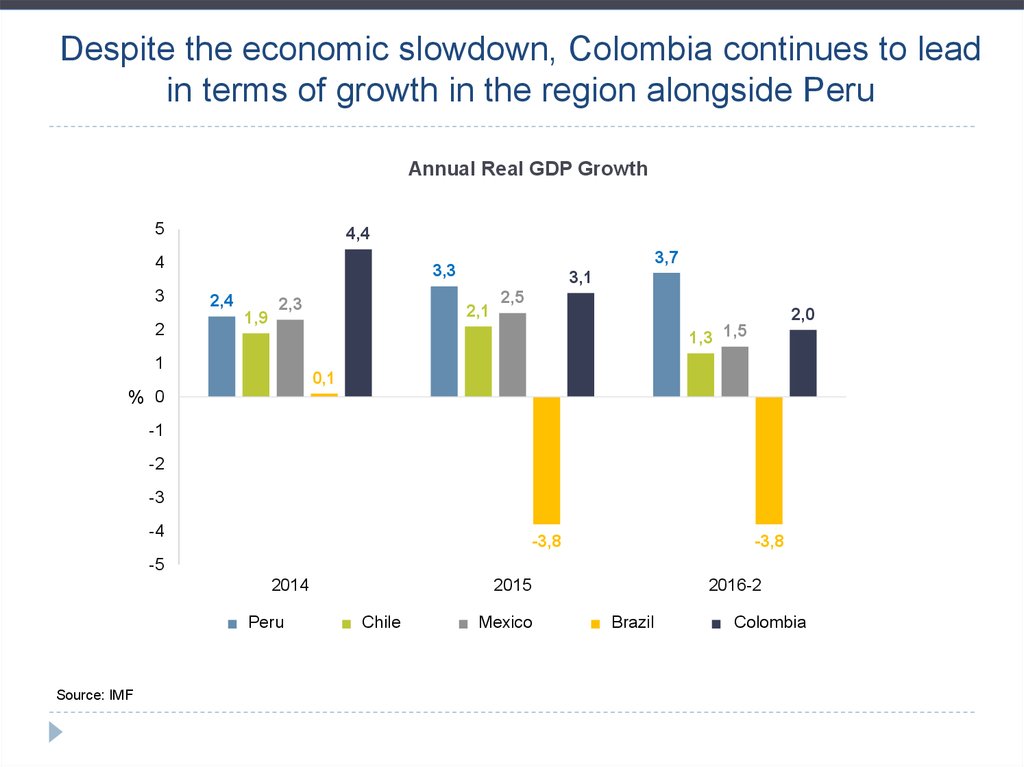

Despite the economic slowdown, Colombia continues to leadin terms of growth in the region alongside Peru

Annual Real GDP Growth

5

4,4

4

3

2

3,7

3,3

2,4

1,9

2,3

3,1

2,1

2,5

2,0

1,3 1,5

1

0,1

% 0

-1

-2

-3

-4

-3,8

-3,8

-5

2014

Peru

Perú

Source: IMF

2015

Chile

Chile

Mexico

México

2016-2

Brazil

Brasil

Colombia

Colombia

55. The Colombian peso is among the most depreciated currencies in the region alongside Mexico

Exchange Rate Index (Base 100 = june 2014)180

Jun-2014

160

140

120

100

Source: Bloomberg.

Perú

sep.-16

jul.-16

mar.-16

ene.-16

nov.-15

sep.-15

jul.-15

Brazil

Brasil

may.-16

Chile

mar.-15

ene.-15

nov.-14

sep.-14

jul.-14

México

may.-15

Colombia

may.-14

mar.-14

ene.-14

nov.-13

sep.-13

jul.-13

may.-13

mar.-13

80

56.

While inflation has risen more than in other countries in theregion except Brazil

Total annual Inflation

12

10

Chile

Chile

Peru

Perú

México

Mexico

Colombia

Colombia

Brasil

Brazil

%

8

6

4

2

0

авг.11

авг.12

Source: National Estadistic Institues of each country

авг.13

авг.14

авг.15

авг.16

57.

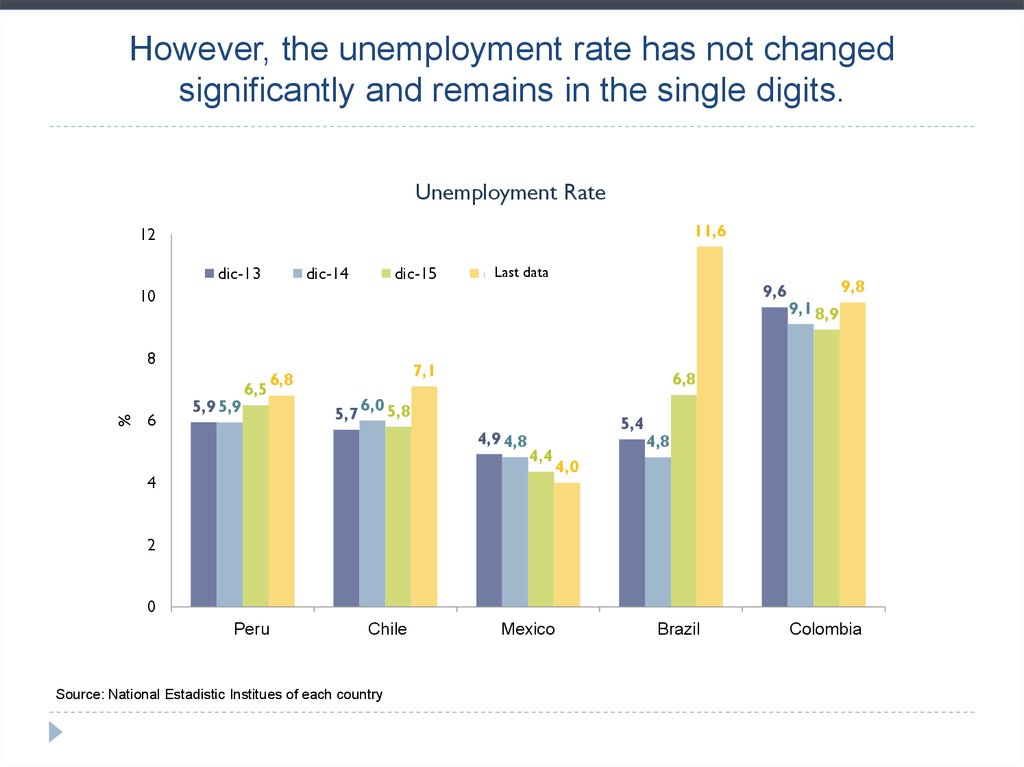

However, the unemployment rate has not changedsignificantly and remains in the single digits.

Unemployment Rate

11,6

12

dic-13

dic-14

dic-15

Last data

último

dato

9,6

10

%

8

6

5,9 5,9

6,5

7,1

6,8

5,7

9,8

9,1 8,9

6,8

6,0 5,8

4,9 4,8

5,4

4,4

4

4,8

4,0

2

0

Perú

Peru

Chile

Chile

Source: National Estadistic Institues of each country

México

Mexico

Brasil

Brazil

Colomiba

Colombia

58.

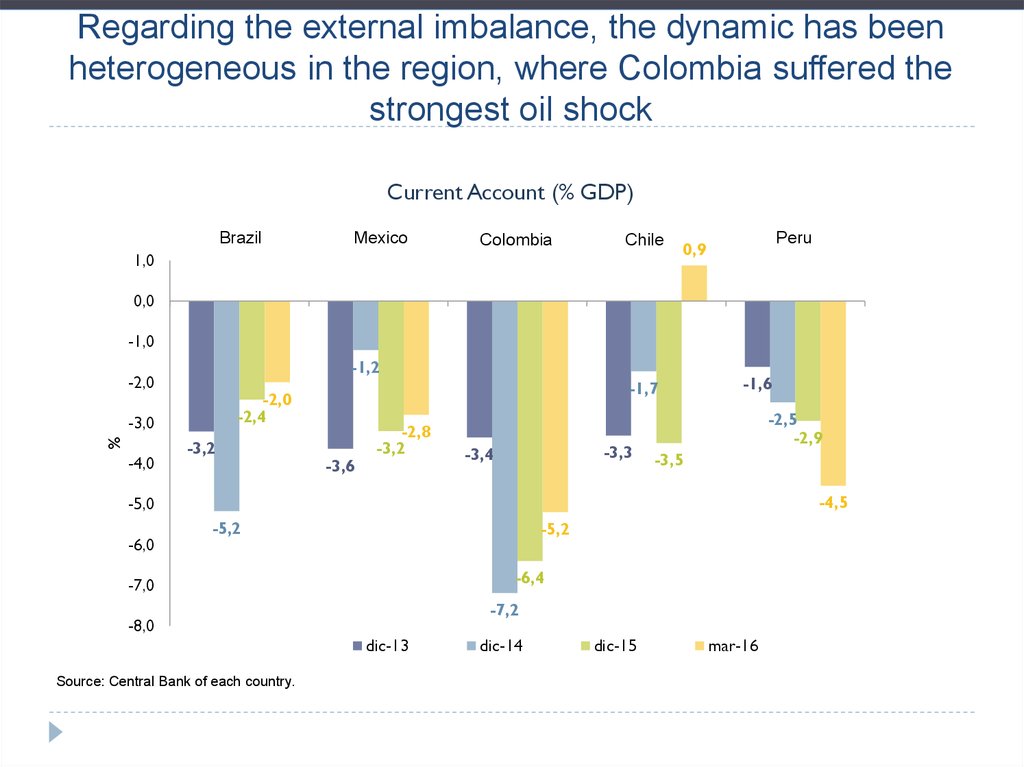

Regarding the external imbalance, the dynamic has beenheterogeneous in the region, where Colombia suffered the

strongest oil shock

Current Account (% GDP)

Brazil

Brasil

Mexico

México

Colombia

Colombia

Chile

Chile

1,0

Peru

Perú

0,9

0,0

-1,0

-1,2

-2,0

%

-3,0

-4,0

-1,7

-2,0

-2,4

-3,2

-3,6

-2,8

-3,2

-3,3

-3,4

-1,6

-2,5

-2,9

-3,5

-4,5

-5,0

-6,0

-5,2

-5,2

-6,4

-7,0

-7,2

-8,0

dic-13

Source: Central Bank of each country.

dic-14

dic-15

mar-16

59.

It is expected that by 2016 the Colombian economy will continue to lead interms of growth with Mexico and Peru, while Argentina, Brazil and

Venezuela will remain in crisis

Real anual Growth , 2016 (%)

4

3,3

2,8

2,5

2,5

2

2,2

0,1

0

-0,7

-2

-1,0

-4

-6

-6,0

Source: IMF – WEO april 2016.

Venezuela

Brazil

Argentina

Ecuador

Uruguay

Chile

Colombia

Mexico

Peru

-8

60. In the long term it is expected that Mexico will be the country with the largest contribution to growth in the region followed

by Brazil despite its current crisis,while Colombia will be the fourth

Incremental GDP* (USD Billions)

637

G-6 Average

Incremental

GDP

416

Incremental

GDP

Italy

277

222

140

133

-1

México

Brazil

Brasil

Argentina

Colombia

Chile

Perú

Venezuela

*Is the difference between the nominal GDP in 2030 and the nominal GDP in 2015 expressed in USD. The size of the circle represents the size

of each economy.

Source: IMF.

61. In fact, Venezuela will be the only country that will not increase its per capita income while Brazil could stagnate. Chile and

Colombia willcontinue to lead

GDP per capita PPP Projections. USD

38 729

40 000

Argentina

Chile

Mexico

Venezuela

35 000

Brasil

Colombia

Peru

34 536

30 000

28 270

25 285

25 000

20 935

20 000

20 527

16 289

15 000

Source: IMF

2030

2029

2028

2027

2026

2025

2024

2023

2022

2021

2020

2019

2018

2017

2016

2015

10 000

62. Conclusions

In the present global economic environment LatinAmerica growth was sharply reduced and its average rate

of inflation increased.

In the case of Colombia and the Pacific Alliance countries

the impact has been less severe due to their flexible

exchange rate regimes and responsible fiscal policies.

Nevertheless, in the next few years the greatest challenge

will be to find new sources of growth that will have to

involve the diversification of their exports.

In order to achieve this they need to attract high quality

FDI and better competitiveness policies