")

")

")

")

Реклама

РекламаПохожие презентации:

Productivity of Branches Home Credit Bank

1.

Productivity of Branchesapplications CL

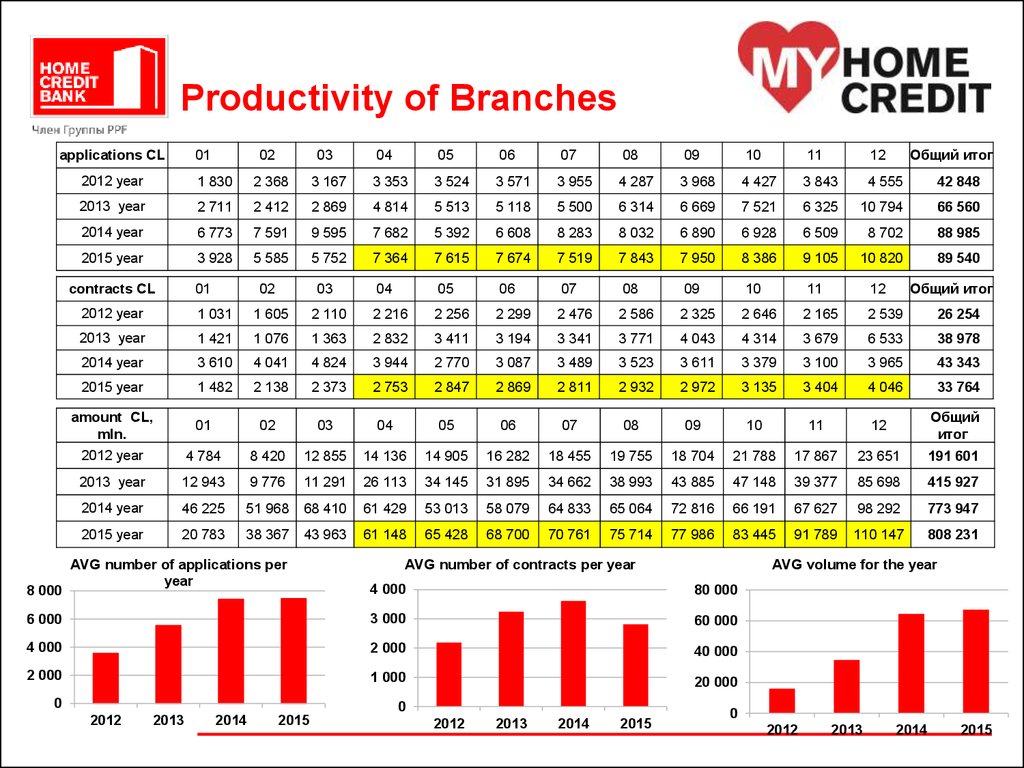

01

02

03

04

05

06

07

08

09

10

11

12

2012 year

1 830

2 368

3 167

3 353

3 524

3 571

3 955

4 287

3 968

4 427

3 843

4 555

42 848

2013 year

2 711

2 412

2 869

4 814

5 513

5 118

5 500

6 314

6 669

7 521

6 325

10 794

66 560

2014 year

6 773

7 591

9 595

7 682

5 392

6 608

8 283

8 032

6 890

6 928

6 509

8 702

88 985

2015 year

3 928

5 585

5 752

7 364

7 615

7 674

7 519

7 843

7 950

8 386

9 105

10 820

89 540

02

03

04

05

06

07

08

09

10

11

12

contracts CL

01

Общий итог

2012 year

1 031

1 605

2 110

2 216

2 256

2 299

2 476

2 586

2 325

2 646

2 165

2 539

26 254

2013 year

1 421

1 076

1 363

2 832

3 411

3 194

3 341

3 771

4 043

4 314

3 679

6 533

38 978

2014 year

3 610

4 041

4 824

3 944

2 770

3 087

3 489

3 523

3 611

3 379

3 100

3 965

43 343

2015 year

1 482

2 138

2 373

2 753

2 847

2 869

2 811

2 932

2 972

3 135

3 404

4 046

33 764

amount CL,

mln.

2012 year

01

02

03

04

05

06

07

08

09

10

11

12

Общий

итог

4 784

8 420

12 855

14 136

14 905

16 282

18 455

19 755

18 704

21 788

17 867

23 651

191 601

2013 year

12 943

9 776

11 291

26 113

34 145

31 895

34 662

38 993

43 885

47 148

39 377

85 698

415 927

2014 year

46 225

51 968

68 410

61 429

53 013

58 079

64 833

65 064

72 816

66 191

67 627

98 292

773 947

2015 year

20 783

38 367

43 963

61 148

65 428

68 700

70 761

75 714

77 986

83 445

91 789

110 147

808 231

AVG number of applications per

year

AVG number of contracts per year

AVG volume for the year

4 000

80 000

6 000

3 000

60 000

4 000

2 000

40 000

2 000

1 000

20 000

8 000

Общий итог

0

0

2012

2013

2014

2015

2012

2013

2014

2015

0

2012

2013

2014

2015

2. Productivity of Branches (2)

Productivityper 1 Branch 01 02 03 04 05 06 07

specialist (CL)

08

09

10

11

2012 year

14 17 23 25 26 26 27 28

25

27

21

24

24

2013 year

15 14 17 29 33 28 33 36

38

42

30

49

31

2014 year

30 33 38 30 20 23 29 29

24

25

24

33

28

2015 year

15 23 27 45 49 51 50 54

55

58

80

75

44

Productivity

per 1 Branch 01

specialist (CL)

02 03 04 05 06 07

08

09

10

11

12

8

12 15 16 16 17 17 17 15

16

12

14

14

2013 year

8

6

8 17 20 18 20 22 23

24

18

29

18

2014 year

16 17 19 15 10 11 12 13 13

12

11

15

14

2015 year

6

22

30

28

17

Productivity

per 1 Branch 01

specialist (CL)

11 17 18 19 19 20 21

02 03 04 05 06 07 08

09

10

11

12

0

01

03

04

2012 year

05

06

07

2013 year

08

09

10

2014 year

11

12

2015 year

CL productivity (contracts)

10

0

01

02

03

2012 year

36 61 93 104 108 117 128 131 117 131 98 127

106

400

2013 year

73 55 66 159 203 175 205 225 248 266 188 386

192

200

2014 year 205 225 269 240 193 202 226 232 257 235 250 371

242

0

2015 year

399

04

05

06

2013 year

07

08

09

10

2014 year

11

12

2015 year

CL productivity (Sales volume)

AVG year

1 000

productivity

per 1 Branch 800

specialist

600

2012 year

80 157 209 373 425 455 469 526 542 579 805 765

02

AVG year

productivity 40

per 1 Branch 30

specialist

20

2012 year

9

CL productivity (applications)

AVG year

productivity 100

12

per 1 Branch

specialist

50

01

02

2012 year

03

04

05

06

2013 year

07

08

09

2014 year

10

11

12

2015 year

3. Status of Branches closing

№ Branch1

2

3

4

5

6

7

8

9

10

507

603

403

404

703

108

503

506

605

106

City

Molodechno

Krichev

Slonim

Grodno

Minsk

Bereza

Sluck

Borisov

Bobruisk

Kobrin

Number Number

Branches Branches

(now)

(after)

2

1

1

3

6

1

1

2

2

1

3 Branches already closed

2 Branches – will be closed in April

3 Branches – will be closed in May

1 Branches – will be closed in June

1 Branches – will be closed in August

1

0

0

2

5

0

0

1

1

0

March

April

May

June

August

closed

30.apr

27.apr

closed

closed

11.may

18.may

25.may

03.jun

01.jun

4. Action plan to increase productivity at Branches

Change chart with coefficients in bonuses of Branch specialists – since April 2015

Regular monitoring of Ratings (report) of Branches and specialists – since March

2015

Optimization of work processes with activities to attract client (setting goals and

monitoring) – since May 2015

Introduction of a system of mentoring – since June 2015

Development of project «Service standards». Cultivation in the minds of people that

«Standards = additional sales». Adoption of standards by all employees of the

Branches – in 2-3 quarter 2015

Closure of 10 Branches – till August 2015

Relocation of 6 Branches to better placement

Advertising promotion of products – hole 2015 year

5. POS

POS Applications40 000

30 000

2012 year

20 000

2013 year

2014 year

10 000

2015 year

0

01

02

03

04

05

06

07

08

09

10

11

12

POS Contracts

40 000

30 000

2012 year

20 000

2013 year

10 000

2014 year

0

2015 year

01

02

03

04

05

06

07

08

09

POS Sales volume, mln. BYR

10

11

12

200 000

150 000

2012 year

2013 year

100 000

2014 year

50 000

2015 year

5

01

02

The title of the presentation

03

04

05

06

07

08

09

10

11

12

6. NNC

2012 year2013 year

2014 year

2015 year

contracts NNC

2012 year

2013 year

2014 year

2015 year

amounts NNC,

mln.

2012 year

2013 year

2014 year

2015 year

290

2 319

1 456

404

2 781

1 843

637

3 405

2 232

1 203

3 064

2 709

1 050

1 562

3 195

977

1 745

3 456

990

1 811

3 567

1 430

2 027

4 573

1 729

1 166

4 946

2 479

1 722

5 350

2 388

1 961

5 786

95

95

4 341 17 918

2 716 26 279

6 543 45 654

01

02

03

04

05

06

07

08

09

10

11

12

Общий

итог

143

1 039

541

179

1 188

745

276

1 324

912

601

1 248

1 092

523

633

1 288

466

574

1 393

491

592

1 437

636

667

1 843

758

528

1 993

1 122

792

2 156

1 146

786

2 332

59

59

2 554

8 895

1 025 10 396

2 637 18 368

01

02

03

04

05

06

07

08

09

10

11

12

Общий

итог

441

441

985 1 154 1 658 3 673 3 579 3 255 3 720 4 580 5 361 8 893 9 089 22 008 67 956

9 462 10 730 12 151 12 899 7 513 7 139 7 750 8 668 6 678 11 679 12 537 18 293 125 498

6 168 8 620 10 461 19 029 22 831 25 118 26 374 34 286 37 715 41 486 45 635 52 480 330 203

6

planned number of conracts and sales

volume in 2015

The title of the presentation

7. NNC

NNC Applications7000

6000

5000

4000

3000

2000

1000

0

2012 year

2013 year

2014 year

2015 year

1

2

3

4

5

6

7

8

NNC Contracts

9

10

11

12

3000

2500

2000

2012 year

1500

2013 year

1000

2014 year

500

2015 year

0

01

02

03

04

05

06 volume,

07

08

NNC

Sales

mln.

BYR09

10

11

12

60000

50000

40000

2012 year

30000

2013 year

20000

2014 year

7

10000

2015 year

The title of the presentation

0

01

02

03

04

05

06

07

08

09

10

11

12

8. Actions to increase productivity

The introduction of ratings for SA and group VA - launch of the project in May 2015(in progress)

Continuation of the project in April to replace the top 10 administrators at the AP at

the 10 worst administrators at the AP, the pilot started in Vitebsk and Gomel. (Acting

administrators)

Permanent employment at AP with big sales as extra motivation administrators. (In

work).

Opening new AP due to the transfer of unprofitable AP.

Replacement SA unable to cope with the plans of sales. (Due to the administrators

Delta Bank)

Development of the project "Service Standards". Adoption workers thought

"Standards = additional sales."

Carrying out the "first wave" began in February

2015 and will end in June 2015. It is planned two waves per year.

8

Since April planned permanent attraction at the expense of the borrower bonus

offers from third parties (cosmetics stores - IVRoshe, DNK, food Euroopt).

9. Deposit portfolio

Term ofdeposit, BBYR

<30 days

30 - 60 days

90 days –

1 year

Total

01.12.

08.12.

15.12.

22.12.

29.12.

05.01.

12.01.

19.01.

26.01.

02.02.

09.02.

16.02.

2014

2014

2014

2014

2014

2015

2015

2015

2015

2015

2015

2015

138 737 187 275 208 168 341 861 321 116 309 431 312 605 299 439 297 139 312 219 251 028 214 429

102 837 85 886 50 762 35 311 130 942 127 795 125 260 118 745 84 426

8 631 29 095 94 761

605 532 575 082 588 281 395 467 306 786 292 112 288 321 285 213 329 681 414 456 456 068 482 269

847 106 848 242 847 210 772 639 758 844 729 338 726 186 703 397 711 246 735 306 736 191 791 459

Structure of deposit portfolio

900 000

800 000

700 000

600 000

500 000

400 000

300 000

200 000

100 000

-

90 days –

30 - 60 days

9

16.02.2015

09.02.2015

02.02.2015

26.01.2015

19.01.2015

12.01.2015

05.01.2015

29.12.2014

22.12.2014

15.12.2014

08.12.2014

01.12.2014

<30 days

10. Deposit portfolio

Term of deposit,BBYR

<30 days

30 - 60 days

16.02.2015

23.02.2015 02.03.2015 09.03.2015 16.03.2015 23.03.2015 30.03.2015 06.04.2015 13.04.2015

214 429

147 824

127 133

100 552

93 578

90 234

90 903

108 091

107 567

94 761

174 388

203 332

274 478

235 813

205 835

225 329

216 064

209 085

2 213

3 887

5 122

10 955

14 771

16 376

<90 days

90 days –

1 year

Total

482 269

497 340

523 117

567 744

577 687

583 961

654 032

703 168

725 240

791 459

819 552

853 582

944 987

910 965

885 152

981 219

1 042 094

1 058 268

1 200 000

1 000 000

800 000

90 days –

600 000

<90 days

400 000

30 - 60 days

<30 days

200 000

0

10

offset the

deposit

portfolio

towards longterm deposits

11. Short-term deposit strategy

Tasks:1.To stop deposits outflow. To manage portfolio for optimal volume

to be self-funded with optimal cost of funds - Done

2.To make branches self-funded

3.To change structure of deposits portfolio. To move short-term

deposits (less 30 days) to mid-term deposits (90, 180 max) - Done

4.To decrease dependency of “speculated deposit players”, mostly

located in Minsk:

•To start activities for clients attraction with more stable behavior

May 2015 – Advertising in Underground and Internet

•To increase share of non-Minsk branches in deposit portfolio – in

progress

To launch Card Saving Account - May 2015

11

The title of the presentation

12. Deposits of individuals. Action plan

1.To make analysis of each region/branch by the following aspects: portfolio structure dynamic,

customer profile, profitability incl.deposit portfolio, potential of branch location – 13.02.2015. done

2.To develop deposit portfolio plan for each region/branch - 20.02.2015 – in progress

3.To make changes in motivation system (to include bonus dependence from the deposits

portfolio plan fulfillment) – 2.03.2015 - in progress

4.To develop action plan for deposit’s products and bank image promotion as sustainable and

reliable (to do in most effective promotion channels – internet, transport, etc.) – in Plan May 2015

– Slide 7

5.To develop action plan for each branch (clients and deposits attraction at the local level) –

2.03.2015 - in progress

6.To redesign sales logic and scripts, training course for deposit sale – 2.03.2015 – in progress

7.To make SMS campaign for existing deposit and salary clients (who have relatively high

regular balance on their accounts) – 2.03.2015 - in progress

8.To redevelop deposits products to achieve key targets (increase portfolio and increase share of

longer terms deposits, decrease of interest rate, promotion to more stable clients) – 2.03.2015 Done. Slide 3 - offset the deposit portfolio towards long-term deposits

9. to avoid mistakes of past years with the introduction of the Deposit product for a long time

under a big bet

To launch Card Saving Account - May 2015

The title of the presentation

12

13. Deposit portfolio Analysis (Deposit Sum)

Size of thedeposit, mln

to 5

from 5 to 10

from 10 to 50

from 50 to 100

from 100 to 500

from 500 to 1000

16.02.2015

23.02.2015

5 588

15 771

120 727

108 239

328 530

113 789

6 101

16 997

129 276

113 907

347 256

121 617

6 367

17 671

134 586

118 303

355 856

133 777

7 098

19 012

146 037

128 815

394 762

152 475

6 407

17 725

137 317

121 488

370 339

150 290

5 733

17 202

132 654

116 767

360 829

149 920

5 636

17 348

137 694

120 584

388 070

168 529

5 423

17 054

141 890

126 030

413 650

174 794

5 230

16 885

140 812

126 957

419 072

176 291

98 815

84 399

87 023

96 790

107 402

102 047

143 360

163 257

173 022

791 459

819 554

853 583

944 988

910 967

885 153

981 221

1 042 097

1 058 270

from 1000

Total

02.03.2015 09.03.2015 16.03.2015 23.03.2015 30.03.2015 06.04.2015 13.04.2015

1 200 000

1 000 000

800 000

from 1000

from 500 to 1000

600 000

400 000

200 000

from 100 to 500

from 50 to 100

from 10 to 50

from 5 to 10

-

to 5

13

14.

Deposit products andbank image promotion

Underground

Адресная программа

Период размещения

Я. Коласа

Октябрьская

Купаловская

01.05.2015 - 31.05.2015

Каменная горка

Пушкинская

Internet

Адресная программа

Период размещения

Google AdWords (контекст)

01.05.2015 - 31.05.2015

Yandex Direct (контекст)

14

The title of the presentation

15. Main competitors Card saving Account

NameIR

"Сберегательный“ from 500 000 - 35%

Fransabank

from 3 000 000 - 1,5%

from 3 000 000 to 15 000 000 -37%

"Супер карта" Idea

from 15 000 000 to 30 000 000 - 38%

bank

from 30 000 000 to 50 000 000 - 39%

from 50 000 000 - 40%

to 800 000 - 0,01%

"Супер карта лайт" from 800 000 to 3 000 000 -36%

Idea bank

from 3 000 000 to 15 000 000 - 36,5%

from 15 000 000 to 200 000 000 - 38,5%

"Супер- карта to 50 000 - 0,01%

капуста" Idea bank from 50 000 до 20 000 000 - 35%

41%

"Потенциал роста"

Idea bank

to 10 000 000 - 30%

Сберегательная

from 10 000 001 to 100 000 000 - 33%

карта Tehnobank

from 100 000 001 - 35%

to 9 999 999 - 28%+ 6%

MTBank (Халва from 10 000 000 to 99 999 999 -37%+6%

Плюс)

from 100 000 000 to 199 999 999 - 36%+6%

from 200 000 000 - 26%+6%

from 500 000 to 2 000 000 - 10%

MTBank(сберегаел from 2 000 000 to 5 000 000 -12%

from 5 000 000 to 50 000 000 - 33%

ьная карта)

from 50 000 000 to 200 000 000 - 37%

от

Minimum balance BYR

Fee for maintenance / issue /

reissue cards BYR

-/-/25 000

MC Standart - 800 000

Maestro - 100 000

Withdrawal comm.

2% in the Bank

3% in other banks

30 000 - 100 000 release reissues 0,9%-2% in other banks

of basic and additional cards

MC Standart - 800 000

Maestro - 100 000

30 000 - 100 000 release reissues 0,9%-2% in other banks

of basic and additional cards

50 000

15000 release reissues of basic

and additional cards

-

0,9%-2% in other banks

Minimum balance can be

100000 release reissues of basic 0,9%-2% in other banks

chosen by the client from

and additional cards

100 mln to 1 bln, if the summ

is less then MB, IR 20%

Insurance deposit 900 000 30%

-/80 000/80 000

2% in other banks

-

99 000 yearly /-/-

2,5% in other banks

-

-/150 000/55 000

2,5% in other banks

16. Interesting competitors products

Deposit card «Халва Плюс»to 9 999 999 - 28% + 6%

► from 10 000 000 to 99 999 999 -37%+6%

► from 100 000 000 to 199 999 999 - 36%+6%

► from 200 000 000 - 26%+6%

► Deposit card with loyalty program in

partners shops. To get bonus points the

client should pay for goods using the

card to get till 3% bonus points. Than the

client could use the bonus points to

purchase for the goods in partners shops.

16

17. Card Saving Account. New Product.

On the basis of Card AccountParameters:

till 100 000 – 0,01%

► from 100 000 till 9 999 999 - 26%

► from 10 000 000 till 99 999 999 - 32%

► from 100 000 000 till 199 999 999 - 30%

► from 200 000 000 и более - 26%

Distribution – Bank Offices

17

The title of the presentation

18. Key CRM initiatives on 2015 The results of the visit Mr. Ludek Mraz (progress)

Project/TaskStart date Finish date

TeleSales project (project will be led by

Project Office). Goal is to start in mid March 25.11.201

31.05.2015

(with soft testing of Homer TS aplication since

4

February).

Responsible

person

E.Prybylskaya

Status

In progress

Pilot projects for full-scope teleSales process

with complete application to be filled in during

from

conf call (with online request to banking

01.05.201 31.05.2015

register) with courier pickup of customer

5.

document and photo (pilot has been agreed

with Karel from Risk).

A.Drebenchuk

In progress

Copy-paste point 3 with online application,

with same process of BKI and courier

from

services for docs-photo. Also agreed with 01.05.201 31.05.2015

Risk. Timing – start of Pilot at the same time 5.

as TeleSales project is implemented (Point 1)

A.Drebenchuk

In progress

from

Xsell on PPF Insurance database; Xsell of PPF

01.06.201 30.06.2015

Insurance product on HC database.

5.

A.Drebenchuk

In progress

Fulfillm

ent in %

Comment

Project was open 25.11.14

Done:

- 11.02.15 - Office for telemarketing is equipped

- 16.03.15 - Recruitment of Head of TLM

- Recruitment and placement of staff (10 specialists)

- Training of staff

- Start of outgoing calls - 31.03.15

- First application (in TLM-department) - 02.04.15

- 08.04.15 - end of testing of a new module Telemarketing

85% - 09.04.15 - Recruitment and placement of staff (additional 10 spec.)

- Development of employee motivation

Plan:

- 22.04.15 - Release

- beginning of incoming calls in TLM (after x-sell mailings) - 22.04.15-04.15.15

- Business trip in the call center in Obninsk (Head of TLM and coach) - May 15

- Online applications 11.05.15

- POS by phone - 25.05.15

- Sales of NNC with delivery by courier (NNC online) - 04.05.15

- Refinansing - 20.05.15

Will be realized within NNC-online project

In progress:

50% description of the process

plan:

definition of logistics cards (including delivery to the client)

Will be realized within NNC-online project

In progress:

50% description of the process

plan:

definition of logistics cards (including delivery to the client)

50%

Negotiations were completed. The item that allows us to send DM, SMS, E-mail etc. was added

in insurance contract (02.02.2015)

The 1st pilot of x-selling is planned from 01.06.2015

Others projects with low priority

Project/Task

Start date Finish date

To help BY CRM team to include into analysis

and compaigns generation process usage of

1Q 2015

data of client’s contacts history (datamarts).

TBD.

31.05.2015

Responsible

person

J.Sklenicka

Status

In progress

Fulfillm

ent in %

0%

Comment

CRM have restored the table with the contacts. It will be loaded after the april release.

18

19. Key CRM initiatives on 2015 The results of the visit Mr. Ludek Mraz (progress)

Start date Finish dateResponsibl

Fulfillment in

Status

e person

%

from

01.05.201 31.05.2015

5

A.Drebench

Delayed

uk

0%

The analysis was prepared. After april releas, crm

must prepare request.

2016

2016

A.Drebench

Delayed

uk

0%

After april releas, crm must prepare request. All

modifications of Web Client will be possible not

earlier than 2016.

CBU (offices) process to be created to

identify customers eligible for Xsell offer (also

those who goes to Cash-desk only).

Responsibility – BY CRM+ BY Sales

-

A.Drebench

Closed

uk D.Dronov

0%

The task was closed due to lack of budget (as a lot of

money spent on the BelCard project ) and no

possibility (limitation of legislation) to install

additional software in cash desk.

CRM analyst is leaving. Agreement done to

replace by external more experienced person

(RU, CZ, UA, KZ) sice April as Jan Tabacek

is leaving. Possible issue if Risk will insist on

Tabacek replacement by CZ person (as

quota is 10 person for entire BY HC)

-

Closed

0%

There is no possible candidate

When requirements to Internet Bank and

Mobile Bank will be preparing to include into 2016

them x-sell requirements.

2016

D.Dronov

Delayed

0%

plenty of them, will not mention, but BY CRM

will prepare in 4 weeks the (quarterly based) 4Q 2014 09.03.2015

plan for entire 2015

D.Dronov

Done

100%

Draft of the work plan for 2015 was prepared

move of CRM unit from Marketing directly

under Dmitriy Dronov to reflect the

from

growing demand for Xsell activities as

01.03.201 01.04.2015

well as enlarging the scope of CRM

5.

„radar-screen“. Timing is on Sergei to

decide

D.Dronov

Done

100%

Done from 01.03.15

J.Sklenicka Done

100%

CRM have restored the table with the contacts. It will

be loaded after the april release.

Project/Task

Contact policy analysis+cleanup (HCI)

followed up by full redesing (BY CRM with

HCI).

Entry data cleaning process (phone(s) +

addreess + email + social networks) on each

contact point to be included in the soonest IT

release. Responsibility for business rules –

BY CRM (in coordination with BY Risk),

implementation on IT

Prepare the table with the contacts

2014

Q4 2014

Comment

The possibility of improvements will discuss in 2016

because lack of budget (as a lot of money spent on

the BelCard project).

19

20. The development plan of subdivision Telemarketing

MARCHAPRIL

16. 17. 18. 19. 20. 21. 22. 23. 24. 25. 26. 27. 28. 29. 30. 31.

10. 11. 12. 13. 14. 15. 16. 17.

3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 3 1.4 2.4 3.4 4.4 5.4 6.4 7.4 8.4 9.4 4 4 4 4 4 4 4 4

DONE

Recruitment of Head of

Х

Telemarketing division

Recruitment of operators

Recruitment of senior operators

primary training

Training 'Telephone Sales'

study of the script

Calls according the call lists

Number of working operators

number of the application (filled by

operators)

Recruitment of coach

Business trip in the Vitebsk call

center (Head of TLM and senior

specialist)

Business trip in the Vitebsk call

center (coach)

8

Х Х

1

1

Х Х Х Х Х

Х Х

1

4

Х

5

Х

Х Х Х Х Х

Х Х

Х Х

215 481 420 440 398 684 670 706 825 681 295

6 7 5 4 4 6 6 7 7 6 3

0 3 2 2 0 1 6 4 2 0 2

Х

Х Х

Х Х Х

APRIL

PLAN

MAY

22. 23. 24. 25. 26. 27. 28. 29. 30.

10. 11. 12. 13. 14. 15. 16. 17. 18. 19. 20. 21. 22. 23. 24

4 4 4 4 4 4 4 4 4 1.52.53.54.55.56.57.58.59.5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 .5

Business trip in the call center in Obninsk (Head of TLM

and coach) - May

Incoming calls to the number 229 89 99

Incoming calls to the number 229 89 77

Х

Х

Incoming calls to the numbers 229 89 71-76,78

Online applications

POS by phone

Х

Sales of NNC with delivery by courier (NNC online)

Refinansing

Х

Х

Х

20

21. Telemarketing results

900800

700

7

7

6

6

6

7

6

6

5

600

4

500

5

4

3

825

400

684

300

481

200

100

8

7

420

440

706

670

681

4

3

2

398

295

215

Number of TLM call

0

Number of TLM employees

1

0

1-Apr

2-Apr

3-Apr

4-Apr

5-Apr

6-Apr

CL number of applications

18

16

14

12

10

8

6

4

2

0

7-Apr

8-Apr

9-Apr

10-Apr

11-Apr

Results from 01.04.15 till 13.04.15:

5815 calls

22 CL-applications (filled by TLM operator by phone)

1.34%- Response rate (78 appl. by all products)

0.67 % - Conversion rate ( 39 appl. by all products)

458 M BYR - New volume (all products)

Number of loans (filled not TLM)

Number of loans (filled TLM)

21

22. Bonus scheme for administrators 1/2

Bonus = (P1 + P2 + P3 + P4 +P5 + P6) – P7 - 2 * (P8 + P9)P1 bonus for new volume in POS

P1 = new volume POS * bonus for 1 mln * V

for 1 mln POS loans

for 1 mln Rassrochka

12 000

6 000

BYR

BYR

12 000

BYR

8 000

3 000 BYR

3 000

BYR

P2 - bonus for new volume in NNC

P2 = new volume NNC * bonus for 1 mln * V

for 1 mln

P3- bonus for new volume in Leasing

P3 = new volume Leasing* bonus for 1 mln * V

for 1 mln

P4 - bonus for new volume in RL

P4 = new volume RL * bonus for 1 mln * V

for 1 mln

V - plan realization index

22

23. Bonus scheme for administrators 2/2

V - plan realization indexPlan for SA Group

0-49%

50-59% 60-69% 70-79% 80-89% 90-99% 100-109% 110-119%

120129%

130139%

более

140%

Administrator's individual plan

less than

50%

0

0

0

0

0

0

0

0

0

0

0

50-59%

0,3

0,5

0,5

0,5

0,5

0,5

0,5

0,3

0,3

0,3

0,3

60-69%

0,5

0,6

0,6

0,6

0,6

0,6

0,6

0,5

0,4

0,4

0,4

70-79%

0,6

0,7

0,7

0,7

0,7

0,7

0,7

0,7

0,7

0,5

0,5

80-89%

0,7

0,8

0,8

0,8

0,9

0,9

0,9

0,8

0,8

0,7

0,6

90-99%

0,8

0,9

0,9

1

1

1

1

0,9

0,9

0,9

0,9

100-109%

1

1

1,1

1,1

1,2

1,2

1,4

1

1

0,9

0,9

110-119%

1,1

1,1

1,2

1,2

1,4

1,4

1,6

1,6

1,4

1

1

120-129%

1,2

1,2

1,4

1,4

1,6

1,6

1,8

1,8

1,8

1,5

1,5

130-139%

1,4

1,4

1,6

1,6

1,8

1,8

2

2

2

2,2

2,2

more than

140%

1,6

1,7

1,8

1,9

2

2,1

2,2

2,3

2,4

2,5

2,5

23

24. Bonus scheme for administrators 3/2

P5 - bonus for insurances quantityP5 = insurance agreements quantity * bonus for 1 insurance agreement * R

for 1 insurance agreement

R - insurance penetration =

insurance penetration

less than 60%

60 -79%

80 - 89%

90% and more

P6 - bonus for Financial Protection quantity

P5 = Financial Protection quantity * bonus for 1 FP * F

for 1 Financial Protection (Kanikuly)

for 1 Financial Protection (Perezagruzka)

for 1 Financial Protection (2 in 1)

F -Financial Protection penetration index

Financial Protection penetration

less than 25%

25 - 50%

50% and more

P7 - penalties for errors in the credit documentation processing

P7 = (P1 + P2 + P3 + P4 + P5 + P6)*K

К - errors index - according to the errors table in the local legal regulation

P8 - bonus got for POS credit agreements that were located into FSPD30 *2

P9- bonus got for NNC credit agreements that were located into FSPD30 *2

10 000

BYR

R

0

1,0

1,3

1,5

20 000

20 000

50 000

F

0

1,0

1,5

BYR

BYR

BYR

25. Bonus scheme for OKR 1/3

Bonus = (P1 + P2 + P3 + P4 + P5+ P6 + P7 + P8 + P9) - Кошибок - P10P1 - bonus for new volume in CL the 1st block

P2 - bonus for new volume in CL the 2nd block

P1 = (new volume the 1st block_CL * bonus for 1 mln) * V

P2 = (new volume the 2nd block _CL* bonus for 1 mln) * V

Bonus for CL for every block

for 1 mln (1st block) Branch

4 000 BYR

for 1 mln (2st block Branch) after 1st block TLM

2 000 BYR

4 000 BYR

for 1 mln (2st block) Branch

V - Plan realization index

Plan for Branches

Teller

cashier's

individual

plan

<50%

50-59%

60-69%

70-79%

80-89%

90-99%

100-109%

110-119%

120-129%

130-139%

>140%

0-49%

50-59%

60-69%

70-79%

80-89%

0

0,3

0,5

0,6

0,7

0,8

1

1,1

1,2

1,4

1,6

0

0,5

0,6

0,7

0,8

0,9

1

1,1

1,2

1,4

1,7

0

0,5

0,6

0,7

0,8

0,9

1,1

1,2

1,4

1,6

1,8

0

0,5

0,6

0,7

0,8

1

1,1

1,2

1,4

1,6

1,9

0

0,5

0,6

0,7

0,9

1

1,2

1,4

1,6

1,8

2

90-99% 100-109% 110-119% 120-129% 130-139% > 140%

0

0,5

0,6

0,7

0,9

1

1,2

1,4

1,6

1,8

2,1

0

0,5

0,6

0,7

0,9

1

1,4

1,6

1,8

2

2,2

0

0,3

0,5

0,7

0,8

0,9

1

1,6

1,8

2

2,3

0

0,3

0,4

0,7

0,8

0,9

1

1,4

1,8

2

2,4

0

0,3

0,4

0,5

0,7

0,9

0,9

1

1,5

2,2

2,5

0

0,3

0,4

0,5

0,6

0,9

0,9

1

1,5

2,2

2,5

26. Bonus scheme for OKR 2/3

P3 - bonus for insurances quantityP3 = (insurance agreements quantity * bonus for 1 insurance agreement) * R

Bonus for 1 insurance agreement:

for 1 insurance agreement

R - insurance penetration index:

10 000

Insurance penetration

Insurance penetration

index

less than 60%

60-79%

80-89%

90% and more

0

1,0

1,5

2,0

P4 -bonus for new volume in RL Street

P5 - bonus for new volume in payroll service

P4 = (new volume RL_street * bonus for 1 mln) * V

P5 = (new volume PL_SP * bonus for 1 mln) * V

Bonus for 1 mln in RL и SP (Salary project)

for 1 mln (RL)

for 1 mln (RL SP)

V - Plan realization index

P6 - bonus for teller transactions quantity

P6 = teller transactions quantity * bonus for 1 teller transaction

Bonus for 1 teller transaction

for 1 teller transaction

1 000 BYR

1 000 BYR

2 000 BYR

BYR

3 000 BYR

3 000 BYR

27. Bonus scheme for OKR 3/3

P7 - bonus for new volume in POS and LeasingP7 = new volume_POS* Bonus for 1 mln

for 1 mln POS

for 1 mln Leasing

P8 - Bonus for Financial Protection quantity

P8 = (Financial Protection quantity * Bonus for 1 FP) * F

for 1 Financial Protection (Kanikuly)

for 1 Financial Protection (Perezagruzka)

for 1 Financial Protection (2 in 1)

F - Financial Protection penetration index

Financial Protection penetration

less than 25%

25 - 50%

50% and more

P9 - bonus for property and legal liability insurance

12 000

5 000

BYR

BYR

20 000

20 000

50 000

BYR

BYR

BYR

F

0

1,0

1,5

P9 = property and legal liability insurance quantity * bonus for 1 property and legal liability insurance quantity

bonus for 1 property and legal liability insurance quantity

1 Economical (apartment)

1 Standard (apartment)

1 Premium (apartment)

1 Economical (private house)

1 Standard (private house)

1 Premium (private house)

8 700

17 400

34 800

BYR

BYR

BYR

11 300

33 800

67 500

BYR

BYR

BYR

errors index - according to the errors table in the local legal regulation

P10 - bonus got for CL credit agreements in the 2nd block that were located into FSPD30 *2